Note that the information below describes the share class (I SEK), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class' return. The information below regarding returns therefore differs from the returns in other share classes.

This material is marketing communication

Monthly Newsletter Coeli Absolute European Equity December and Summary of 2021

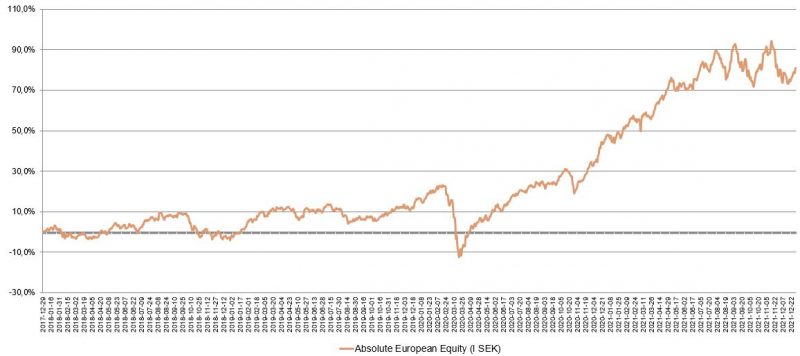

The fund's value increased by 0.4% in December (share class I SEK). Stoxx600 (broad European index) increased during the same period by 5.4% and HedgeNordic's NHX Equities tentatively increased by 1.2%. The corresponding figures for 2021 are an increase of 22.3% for the fund, 22.3% for Stoxx600 and 9.8% for NHX Equities.

EQUITY MARKETS / MACRO ENVIRONMENT

History repeated itself and it was once again a strong end to the year. After a hesitant start with risk on and off every other day, investors increased their risk during the last 10 days of the year. The broad European index returned 5.4% in December, while the S&P500 increased by 3.7%. The fund's return ended at a more modest 0.4% and we will come back to the reasons for that later.

The main event of the month, together with the development of the omicron virus, was the US Federal Reserve's meeting on the 15th of December. It was a dramatic change of language to a more aggressive policy to curb the acceleration of inflation. “We tend to use the word transitory to mean that it will not leave a permanent mark in the form of higher inflation. I think it's probably a good time to retire that word”. After contemplating for a few days, the world's investors realized that they might have had a too gloomy view on markets and began to increase their equity exposures again.

As previously mentioned, the trump card for the development of the world's economies is how assertive politicians want to be with varying degrees of social restrictions. Increasing the vaccination rate by restricting the freedom of those who have been vaccinated will probably be difficult. Compared with many other countries, Sweden is, once again, faring relatively well.

Media coverage of the virus and the new restrictions remain relatively one-sided. The focus is primarily on infection control, while the consequences for individuals, companies and other businesses are described in much less detail. The aim is to ensure that the healthcare system does not get overloaded. Why no one among the traditional media questions why Sweden is at the absolute bottom in Europe in terms of beds per capita (including intensive care units), while we have the world's fourth highest tax burden, should be of some interest to the citizens.

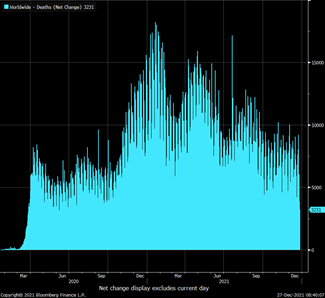

The image below from Bloomberg data shows the global Covid-19 death toll. It is encouraging to note that we just saw a new low point and we are now at the same level as in June 2020.

Source: Bloomberg data

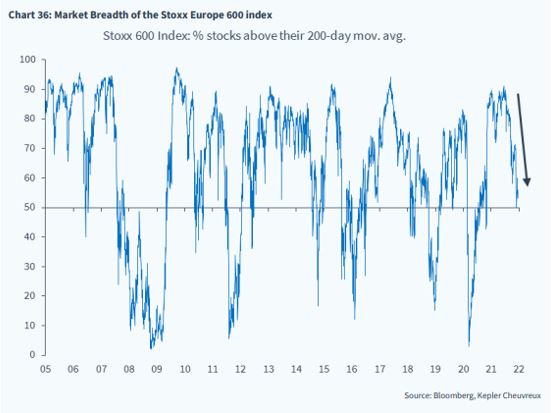

There was still an extremely high concentration of companies that drove the broad stock indices upwards in December. Many of the members of the broad indices (equities) were well below their peak levels. A trend that started before the summer and which also had an impact on our fund's return in recent months. The picture below shows the breadth of the 600 largest companies in Europe and, as is clear, it is a sharply declining proportion of companies whose shares trade above their 200-day average (now at a low of 50%). The corresponding figure for the fund's long holdings at the end of the year was 50%.

Illustrated in a different way and for the 500 largest companies in the USA (data from the end of November 2021). When Nasdaq had risen by 23%, only 61% of the companies showed a positive return and the average decline from its highest level for equities in the Nasdaq index was as much as -41%.

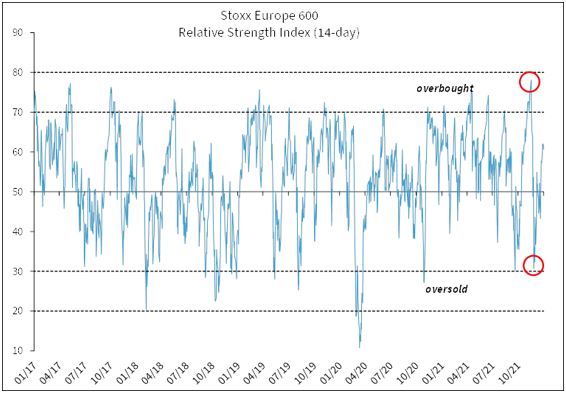

In recent months, the world's stock markets have behaved a bit like an addict who sometimes does not get his fix (stimuli from central banks). The risk appetite has fluctuated sharply, which the picture below clearly illustrates. From an oversold position a month ago, the market is now back at a more normal position.

Source: Kepler Cheuvreux

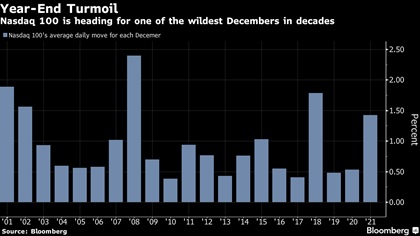

The volatility in the market during December is clearly seen in the chart below, which shows the average daily movement of the Nasdaq index. We experienced the third highest volatility in 20 years.

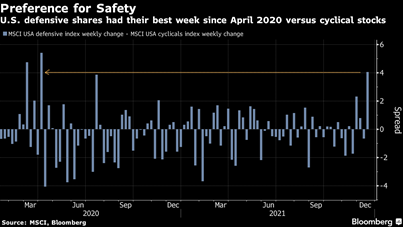

This led to a clear preference for defensive stocks over cyclical stocks. The difference between the two types was the largest since April.

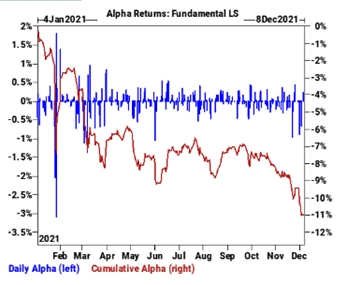

Goldman Sachs hedge fund customers with a long/short strategy (like us) have had a tough year with sharp underperformance. The blue bars in the image below show weekly excess returns (positive and negative). The red curve shows the accumulated downside return, which is -11% for the year.

As the picture below suggests, it seems that Price/Sales is the new P/E ratio.

Elon Musk has sold Tesla shares to pay some tax, more specifically USD 11 billion. Democrat Elisabeth Warren is not impressed. Not Elon either.

We present a good laugh in a less serious feature about Elon Musk.

Last but not least more headlines about Boris Johnson. The crisis is getting worse and anger over new pandemic restrictions and alleged Christmas parties last year on Downing Street is growing. Critical voices are also being raised within his own party.

Source: Ryan Air / Twitter

Our new energy minister, Khashayar Farmanbar, probably has the country's greatest self-confidence. When asked what they should do about electricity prices, the answer was: "we work around the clock to push back the price of electricity".

Our new Minister of the Environment did not do well in the hearing on how many nuclear power plants Sweden has in operation and how many have been taken out of service. She guessed that two have been shut down and three are in use. The correct answer is that six have been shut down and six are still in use. She's probably great at other things.

Source: Steget efter

Long positions

Evolution

After a challenging November, to say the least, where the share fell by as much as 32%, the Evolution share recovered significantly in December. (As most of you readers probably know, in November Evolution was subjected to anonymous allegations that the company operated in blacklisted countries. When the stock fell, the journalist corps followed with critical eyes.) As the worst part of the storm subsided, Evolution began repurchasing programs that have partially restored some of the confidence lost in November. We increased our position at low levels, which contributed to the share being the fund's largest contributor in December. By the end of the month, the share had risen by 35% and the gain for the full year was 54%.

Lindab

Lindab was the fund's second-best contributor for December after the share rose just over 9%. Among other things, the sale of Building Systems was approved by Russian competition authorities. With this, Lindab now has a wholehearted focus on its core business. In addition to this, Alig Ventilation, a Swedish company in residential ventilation, was acquired. Thus, Lindab acquired four companies during the fourth quarter, and we hope that the pace will continue in 2022. Finally, it was announced that Lindab has now been moved to Nasdaq's large cap list after Lindab continued two positive years with an increase of 89% during 2021 - impressive.

Wincanton

One of the fund's more distinct value cases, the British transport and logistics company Wincanton, made a positive contribution to the fund after a few challenging months. The stock has been hit by the news flow regarding the shortage of truck drivers, which has affected Europe in general and in particularly the UK. This in turn has the marked worried above wage inflation. However, Wincanton has shown that this can be managed with the help of proactive price increases. The management has for a long time worked to improve the balance sheet and for the first time in many years, Wincanton has a net cash position. We estimate the profit will increase by 10-15% per year for the foreseeable future. As such, today's valuation of 8-9x free cash flow, based on our estimates, appears very attractive.

Sedana Medical

Sedana leaves an eventful December behind. At the beginning of the month, the decision to invest in in-house sales staff in the USA was announced, which resulted in a direct share issue. The net proceeds will be used to build up operations in the United States. This is in preparation for the commercial launch that is expected after market approval in 2024. In addition, the company received a so-called IND approval, which means that it is now possible to start phase III studies in the USA. Sedana continues to deliver within its communicated time frame, which is far from guaranteed for this type of business. The share rose 9% in December, but only by a modest 14% in 2021. However, the fund's earnings were better as we bought at low levels and sold at high levels.

ISS

The ISS share also recovered after some tough months. Since we invested during the first half of 2021, it has been mainly positive tones around the company. The financial results have been in line or better than market expectations. Management has bought shares across the market and the overall feeling is that market participants are gradually regaining confidence in the company. However, we are still waiting for that sharp course, which has probably been partially halted by renewed Covid worries. The share rose 6% in December and by 21% in 2021.

Atai Life Sciences

The fund's great despair is spelled Atai. The holding has had a negative effect on returns for several months. In December, a lock-up period ended for some early investors (including ourselves). This created an enormous selling pressure which in just two days caused the share to fall from 11 dollars to about 7 dollars and affected the return for the fund by about -1.4%. Although the share was a major headwind during the second half of the year, it has been a very good investment for the fund. Our average acquisition cost is approximately $1.30. At the time of writing, we have invested approximately two percent of the fund's capital in the company.

Short positions

The short portfolio contributed with a negative result during the month. Our short derivative positions in Swedish OMXS30 and German DAX had the largest contribution. Some stock-specific short positions that contributed positively to the result were German Daimler, Swedish Dometic and American Teva Pharmaceuticals.

Exposure

The net exposure, adjusted for our unlisted holdings, at the beginning and end of the month was 70 and 77%, respectively.

The Year that’s been

First, a brief attempt to sum up our 2021.

- Performance: When we breathe a sigh of relief and find that the fund has risen by 22.3% during the year we are satisfied, even though we gave back some gains from our peak two months earlier.

- Largest contributors: This year's five largest contributors were Truecaller, Surgical Science, Lindab, Swedencare and Victoria. CVS Group came in at a strong sixth place. The top five accounted for a total of 17% points of the fund's positive performance. Truecaller rose by 119% since the IPO on October 8. The corresponding annual return for Surgical Science was +201%, Lindab +89%, Victoria +83% and CVS +49%. At the end of 2021, we chose to sell our Swedencare shares after a phenomenal price increase (+137%) during the year.

- Unlisted holdings: Within this asset class, the contribution in 2021 eventually became relatively modest. Until Atai's IPO in June, the contribution was significant, but when the year ended, the contribution finished at a modest +0.7%. For other unlisted holdings, there are good opportunities for more value-creating transactions in the coming months.

- What we are most satisfied with: The work that we put into Truecaller prior to the listing and the large allocation we made to the company in connection with the IPO. The fact that we then took measured risks and further increased our exposure prior to their first report did only added to the success. In addition, and in general, we made very few mistakes during the year, which of course had a positive effect on the year's results.

- What we are least satisfied with: That the fund's performance during the latter part of the year was negative by a couple of percent. Our explanation for this is 1) a weak development in Atai, which cost about two percent during the period. We had a lock-up here. 2) A weak price development in general for smaller companies 3) A sharply weakened Swedish krona in the last two months, which cost an additional two percent.

- Our company: We just marked the fourth anniversary since the undersigned started the business with SEK100 million in assets under management. Including the European Opportunities sister fund, which started on 1 April 2020, we now manage almost 2 billion. Even better is that we, ourselves, accounted for a significant part of the growth as the hedge fund has risen by just over 80% and the sister fund by just over 100%. Staffing has also never been stronger; we have more resources and we put another year of experience behind us.

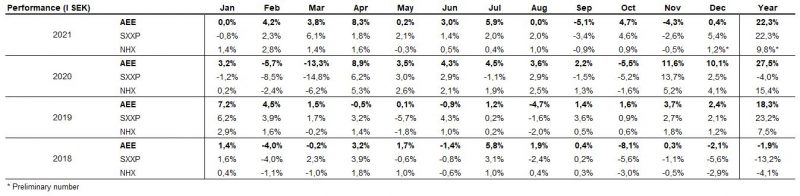

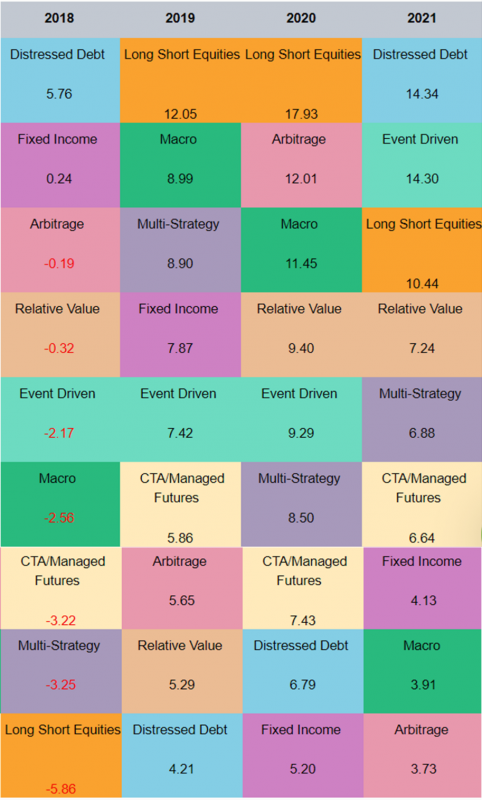

- Four years track record: We have consistently had a significantly higher return than other global long/short strategies. The annual return in 2018 was -1.9% for us (compared to -5.9% for our strategy group), in 2019 we generated 18.3% against 12.1%, in 2020 we achieved 27.5% against 17.8% and in 2021 we finished at 22.3% against 9.5%. The best strategies of 2021, Distressed Debt and Event Driven, are also lagging our performance.

Source: EurekaHedge

Now a brief attempt to summarize our environment during the past year.

- A strong stock market year is added to the books. Below are various indices measured in local currency and euros.

Source: Bloomberg

- Stoxx600 by sectors

Source: Bloomberg

- Out of the ten best shares last year in Stoxx600, five are Swedish. Unbelievable! We owned the Finnish QT Group in 2020 (and thus sold too early).

Source: Bloomberg

- It was finally 68 all-time highs on the US stock market in 2021. Second most ever after 1995 which had 77 ATH.

- The Qanon jackal embodied the madness of January 6th a year ago during the storming of the Capitol.

- (Temporarily?) Game over for Donald Trump

- The beginning of last year offered the biggest hedge fund destruction ever (short squeeze) when the people revolted against the establishment and pushed up some shares to unimaginable levels. Gamestop, which had a market capitalization of $800 million, was the world's most traded stock for one week. Higher turnover than Apple and Microsoft!

- Few had heard of Bill Hwang and Archegos Capital Management before Hwang broke world records in rapid losses. In a week or so, Archegos lost up to $30 billion in pyramid schemes. As recently as January 3rd this year, Credit Suisse announced that it had fired 69 people in the wake of the losses ($5.5 billion) incurred in connection with Archego's collapse.

- Inflation rose from 1.4% yoy when the year began to 6.8% at the end of the year. At the risk of crediting ourselves too much, we take the liberty and quote what we wrote in November 2020 and April 2021. "It would not surprise us if next year's problem is going to be to tame the monster that the central banks have created when the economy is back with almost full force”.

- We allow ourselves another quote from our letter in September. "European gas prices which have risen in a seemingly uncontrolled fashion and recorded the highest September prices ever. A silent prayer for the mild winter. We guess that this development will soon be a major topic in the media, and it will undoubtedly create various problems and somewhat reduce next year’s expected growth. It feels reassuring that Per Bolund (Swedish Green Party MP) claims that there is no electricity shortage in Sweden because then the costs for ordinary people would be unbearably high during the winter (which of course they will be)”.

- Thank you Mutti!

Source: Nyhetsbyrån TT

- The front page of Bloomberg News from November 26th which became the worst trading day of the year after the first reports of the Omicron variant.

Summary

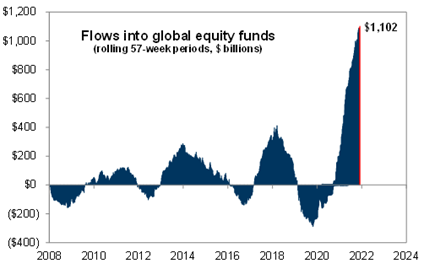

After absorbing and dissecting endless amounts of facts, events and noise during the year, it is now the time of year when you have to summarize everything and have an idea of how the coming year will turn out. With the risk of starting at the wrong end, had we known that inflation would rise from just over one percent to almost seven percent, that we would get a third Covid wave like the one we are now experiencing and that there would be huge bottleneck problems for various industries, we might have not guessed that the S&P would hit 68 all-time highs, that the inflow to the world’s equity funds in 2021 would be as high as the last 12 years combined and that the US 10-year interest rate would be around 1.5%. To quote Morgan Housel who, among other things, wrote the book Psychology of Money. “We think about and are taught about money in ways that are too much like physics (with rules and laws) and not enough like psychology (with emotions and nuance). Physics isn’t controversial. It’s guided by laws. Finance is different. It’s guided by people’s behaviors.”

As previously expressed - the inflow to the world's stock markets in 2021 was greater than the total inflow over the past 12 years.

Source: Goldman Sachs

When 2021 began, we were in the best of worlds. Company profits were in strong acceleration, fiscal and monetary policy at maximum levels and the optimism among investors that the vaccines would soon end the painful pandemic was strong. Now, after rising sharply in the second quarter, the US Federal Reserve has flagged several rate hikes in 2022. Acceleration of gains has slowed (but remains at high levels) and the Omicron variant has once again made world politicians react with determination and utmost care. That caution prolongs the problems most industries experience regarding various bottlenecks in the economy. Of course, it also further increases the fragmentation we see in society between those who have and those who have not. The picture below illustrates this well.

Source: Goldman Sachs

We are experiencing a historically strong recovery, see red line for current development.

The expansive policy will gradually decrease in 2022 and first out is, as usual, the United States. On the other scale is China, which after a very problematic 2021 is now communicating that it must accelerate to fuel growth in the economy. Europe, which still has a negative interest rate environment, will probably only experience minor changes in monetary and fiscal policy. A point of reference is the Swedish Riksbank (Swedish Central Bank), which last communicated that the interest rate would not be raised until 2024, despite high economic activity in Sweden. A rare, difficult-to-solve equation.

All the above has affected the world's stock markets where the leaders (in the stock market) have gone from the smaller companies to the larger companies and where the breadth of the market has gradually decreased to today's record low levels. One consequence of this is that as many as 85% of active managers in the US had a worse return than the S&P500 in 2021 (source Morningstar). The corresponding figure in 2020 was a high 64%. Underperforming two years in a row. Hedge funds have also had a challenging year as a collective. If you study the return on Goldman Sachs '"VIP basket" (which contains hedge funds' most popular stocks) and multiply it by 3x, they still do not reach the S&P500's return.

Nasdaq is at the highest levels, but only 35% of the companies are above their 200-day moving average.

The biggest variable in the equation about the development of the stock market is inflation and how the US Federal Reserve should deal with it. It will be a delicate task and we would not be surprised if the Fed takes a step back in a few months from its now hawkish stance. This of course assumes that inflation stabilizes or falls back, which we believe is reasonable since much of the upward pressure comes from "Covid-related" causes. In the stock market, Omicron now seems to be history and even we are slightly optimistic that we are now starting to see the end of the pandemic. We have a difficult month ahead of us with high infection rates, but thankfully with much milder symptoms.

We would like to see the curves meet again during the year. It can be clearly seen that it was in the second quarter that the development changed in nature. The surprise index began to fall, and inflation rose.

If the fixed income market is right, the US ten-year interest rate will not rise above two percent. Global fixed income investors will continue to buy US government bonds in search of some form of return (Europe offers little). If the fixed income market gets it right, inflation will come down, which means that the real interest rate peaks around zero percent! Maybe even continue to be negative, which means that one should continue to own fixed assets and preferably those that contain some form of growth.

In summary, our best assessment for the year is that the world will continue to have high economic growth. Interest rates will rise to varying degrees from extremely low levels and, all other things being equal, it will put some pressure on multiples, but not enough to withstand earnings growth (in our opinion) and thus we expect a positive return, but significantly lower than 2021 and combined with a higher volatility.

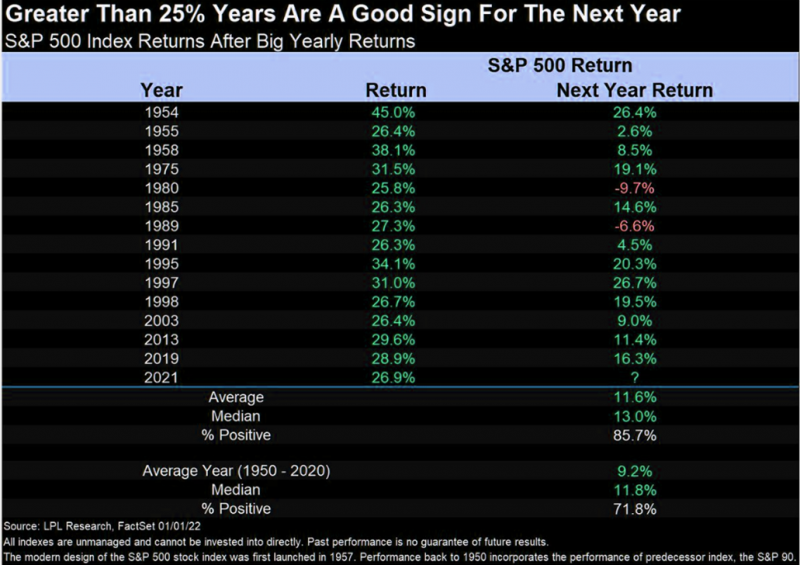

Historical median return 12 months after year with more than 25 percent return: 13 percent.

Source: LPL Research, FactSet

Value stocks are likely to challenge faster-growing companies. Below the index levels, cheap cyclical shares such as car shares that trade at 6-7x the profit will challenge, for example, Nibe which is trading at 75x the profit. For our part, we will continue in the same style, but probably increase the element of cyclical companies in combination with a gradual shift upwards in the size of the companies we invest in. Liquidity becomes increasingly important as the fund grows.

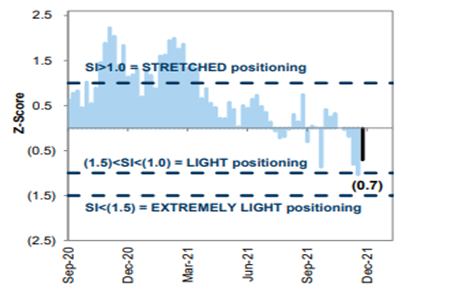

The positioning is below the normal level at the end of the year, which is a good starting position. The fourth quarter was turbulent, and many increased their cash positions.

Source: Goldman Sachs

In conclusion, I would like to extend a big thank you to Cecilia and Fredrik who in a brilliant way delivered a lot of value to the company and thus to you, the investors. That is also the reason why they are both now co-owners, which makes me both happy and proud. In a few weeks, Gustav Lill will also start working with us as an analyst. Gustav, who is 32 years old, is a trained industrial designer and economist and during his studies has worked as an analyst at Grenspecialisten in Malmö. A very warm welcome to Gustav!

A big thank you for your trust and we look forward to 2022.

Mikael & Team

Malmö January 10th.