Note that the information below describes the share class (I SEK), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class' return. The information below regarding returns therefore differs from the returns in other share classes.

Before making any final investment decisions, please read the prospectus, its Annual Report, and the KIID of the relevant Sub-Fund here

This material is marketing communication

Monthly Newsletter Coeli Absolute European Equity - February 2022

February performance

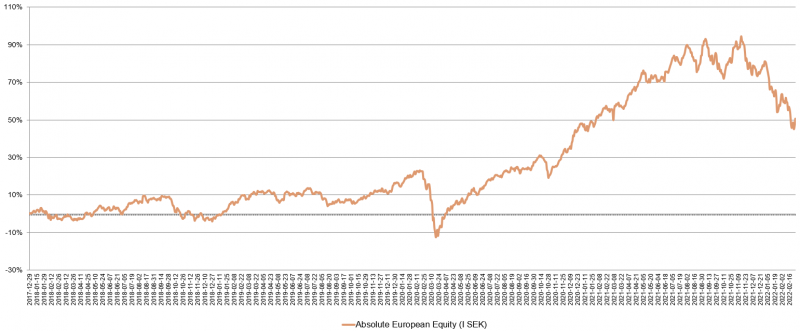

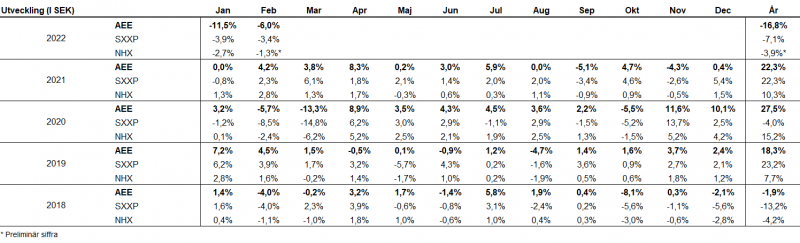

The fund's value decreased 6.0% in January (share class I SEK). The Stoxx600 (broad European index) decreased during the same period by 3.4% and HedgeNordic's NHX Equities fell provisionally by 1.3%. The corresponding figures for 2022 are a decrease of 16.8% for the fund, -7.1% for Stoxx600 and -3.9% for NHX Equities.

Equity Markets / Macro Environment

On Thursday, February 17th, the author along with several international investors, were invited to the annual security conference in Munich to participate in roundtable discussions with heads of state, foreign ministers, defence ministers and high-ranking military officials. All the world's leaders were there, including the Vice President of the United States. The consensus was that a major military intervention by Russia against Ukraine was unlikely. It would be incomprehensible why Putin would risk so much for so little. In addition, it was said that President Putin grossly underestimated the joint force of the Western world and NATO in response to Russia's aggressions. Unfortunately, one of those assumptions were wrong and that became painfully apparent on Thursday morning, the 24th of February. That morning was the most dramatic and brutal awakening for Europe since World War II.

During a few minutes Putin delivered an icy cold and threatening speech at 04.00 on Thursday morning and thus the geopolitical map of Europe, for the last 25-30 years, dramatically and irrevocably changed. It was a hefty and terrible day for Europe and the rest of the world. With full force, a paranoid ex-KGB agent attacked his brethren and forced young people on each side to kill each other in order to satisfy an old Tsar dream and the desire to go back to a time before the collapse of the Soviet Union.

Source: The official Twitter account of Ukraine

At the same time, the dream of a reasonably synchronized and globalized world was also shattered. Immediately and from now on it is the Western world against Russia and China.

The following two authoritarian leaders (a politically correct description of dictators) are now being helped to disrupt the democratic forces of the world in various ways. They were last seen together in connection with the Olympic opening ceremony, where they concluded an agreement based on a partnership "without borders". Well thank you, we noticed that it took effect immediately. China's Foreign Ministry spokesman refused to call the Russian attacks an invasion and blamed the United States instead. "They lit the fire and gave oxygen to the flames. How are they going to put out the fire now,” she wondered? She also said that the United States went into Iraq and overthrew Saddam Hussein, so what's the difference?

Partners in Crime

Source: Getty Images

The Russian news agency, Interfax, reported that Putin and Xi spoke on the phone on Friday evening, February 25th. Xi emphasized his respect for the actions of the Russian leadership in the current crisis. How long (weeks?) will it take before China seriously threatens Taiwan while the West is under pressure? The Chinese threat to the West is palpable and growing, and the entire West must step up to face it.

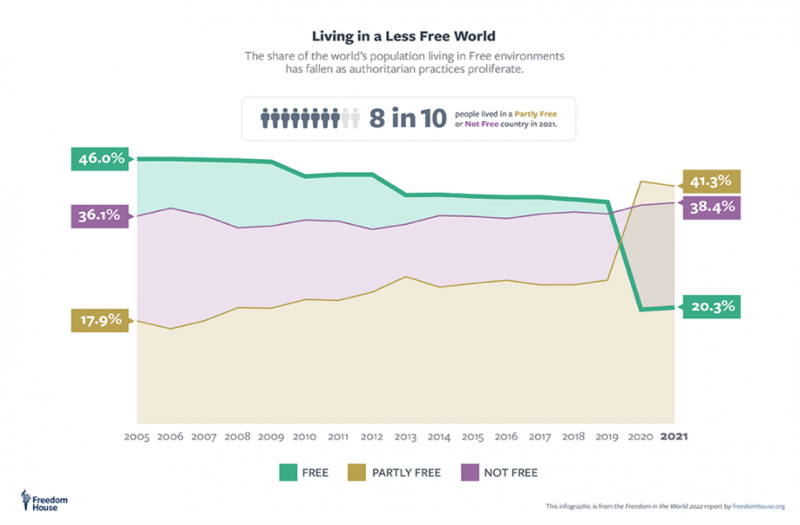

On the theme that the world's democracies are under pressure. Only 20% of the world's population lives in completely free conditions, compared with 46% as recently as just over 10 years ago. Scary and this is what we must defend with all available means.

As I write this on Sunday, February 27th, the news is pouring in regarding re-armament and energy supply. True to habit, Europe has lived in a fairy-tale dream since the fall of the Berlin Wall in 1989 and believed that there would never be another war. Naively and eagerly encouraged by populist leaders, defence spending has fallen while rising sharply in Russia and China. In the financial world, some illusionist officials have concluded that it is unethical to invest in companies that manufacture weapons that protect democracies against attacks from aggressive foreign powers. However, it is no problem to invest in Russian or Chinese funds. It's almost more than you can handle.

Europe's politicians trump the above mistake by also underinvesting in the energy sector for many years and becoming dependent on Russian gas and oil. Green energy is not yet sufficient and is not reliable enough. Sweden took out 10% of electricity production in 2019 with the closure of Ringhals (nuclear power plant). At the turn of the year, Germany shut down three of its nuclear power plants and within a year, three more (the last) nuclear power plants will be taken out of service. Congratulations. That makes Stefan Ingve's (Governor of the Swedish central bank) rate hike in the days before the Lehman crash appear brilliant. With the clock about to strike midnight on Monday, news is breaking that Germany is debating whether to reassess their decision on nuclear power and keep the plants. At least you cannot complain about the flow of news.

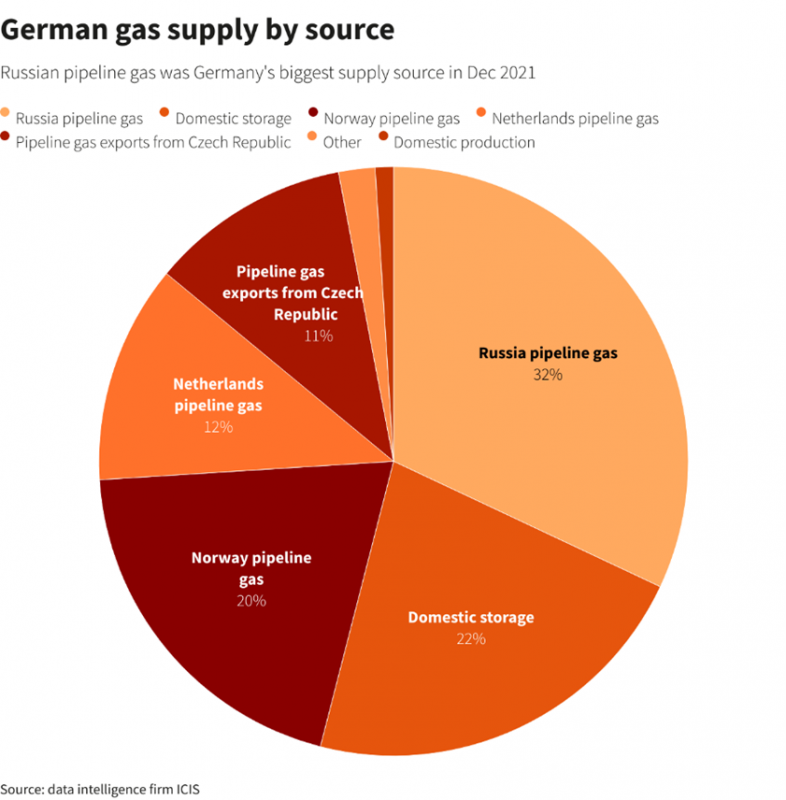

As the picture below illustrates, Russia accounts for almost a third of gas supplies to Germany. It will hurt Europe a lot and most likely it will hurt Germany, who is basically sitting in Russia's lap in terms of its energy supply. The United States does not have these problems at all. There you control the supply yourself and can increase your domestic production.

All this leads to a rise in the risk premium in Europe compared to other regions. It was very revealing on the day the war broke out as the US dollar rose at the same time as the euro fell sharply. European stock markets were down just over 4.0% while they rose (!) in the United States.

The euro has fallen sharply since last summer and the US dollar has risen. We save you from a picture of the Swedish krona, but we can reveal that it is not the first priority when world trembles.

Source: Bloomberg

Europe's leaders are now in a hurry. Every two hours during the weekend as this is being written, there are updates, one more ground-breaking than the other. We see in real time a fundamental reorganization of European defence policy and a complete course correction to Putin's Russia. Germany sends weapons to Ukraine, which was previously unthinkable due to the collective bad conscience from war crimes during World War II. The defence budget is raised from 1.2% to 2.0% of GDP. This year, the German defence will receive 100 billion euros (!) in special funding for arming and equipping.

Let us hope that the violence is reduced, and diplomatic negotiations begin. A positive development in this tragedy is that the United States has stepped up as the world leader they are and is driving development forward. Their actions have led to Russian banks being excluded in the SWIFT system, which makes it very difficult for the country to bank. We should probably be grateful that the former American president is not in power, as it probably had not led to a calmer development.

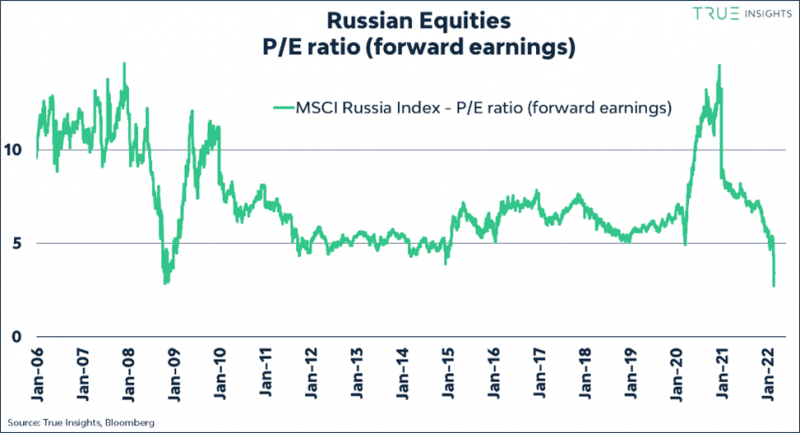

It's starting to get cheap now. Russian shares are traded at P/E 3x. We adhere to old principles of not allocating capital to Russia. On Sunday evening, news came out from Norges Bank that they will sell all their Russian holdings. The sales pressure will probably reach biblical proportions.

Source: True Insights, Bloomberg

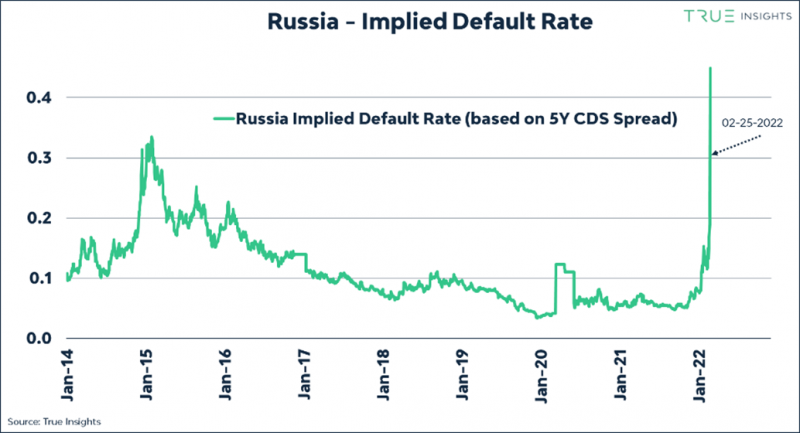

The risk that Russia will not be able to repay its bond debts exploded to 44% on the day of the outbreak of war.

Source: True Insights, Bloomberg

The Moscow Stock Exchange was having a bit of a hard time. The index fell by 39% on the day the invasion began. Trading stopped, but on the London Stock Exchange on February 28, some of the major Russian bank shares fell by 75%, in one day.

Source: Bloomberg

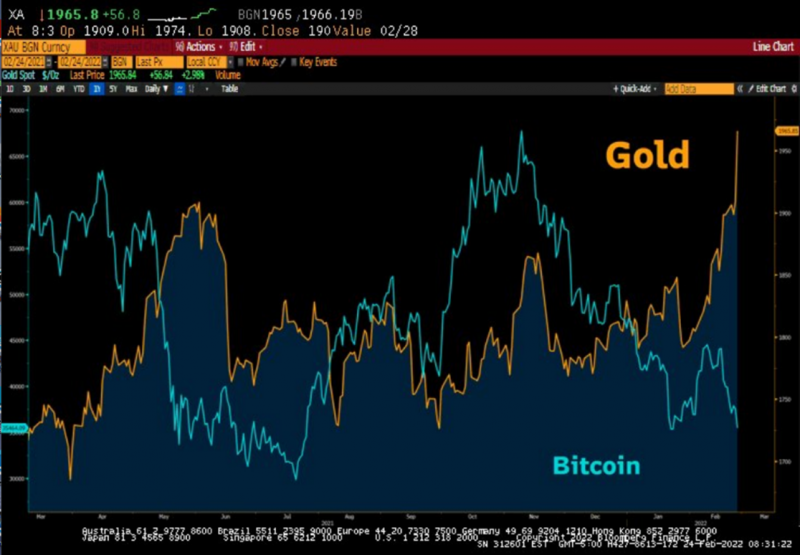

Gold has made a grand comeback and won by far the first round this year over Bitcoin in the discipline “store of value”. Prices are from middle of February and bitcoin finished the month strong.

Source: Bloomberg

Elon Musk - The King of everything and everyone. Ukraine's Vice President tweets to Elon Musk and asks for access to Starlink's internet service. 10 hours later, Elon replied that it was activated.

Source: Twitter

We were probably all surprised by the power and speed of Russia's attack. Prime Minister Magdalena Andersson had a hard time finding words to describe her reaction.

When you thought you had seen everything. The Taliban in Afghanistan are calling for peaceful talks between Russia and Ukraine.

Source: The Islamic Emirate of Afghanistan

Long positions

Photocure

During the month, Photocure released its financial statements for 2021. Sales were about 7.0% higher than expected, which was enough for the share price to rise on the reporting date. The company has had a few tough years where growth has been weak due to the pandemic but has under the circumstances done an acceptable job. In a presentation, the management said that they increased volumes sold in the US by 24% in 2019–2021, even though the number of procedures where Photocure's product is used has decreased by -11% in 2019–2021 due to the pandemic.

As we now approach a reopening of society, Photocure should be able to approach growth levels of 40-50% in the US and 20-30% in Europe from the second half of 2022 onwards. The business will benefit from societies starting to manage the healthcare debt accrued during the pandemic, partner Karl Storz launching new hardware, increased investment in health care in general and improved accessibility for sales staff in hospitals. The stock rose 7.0% in February and is valued at a low 9x EBIT 2024e (our estimate).

Surgical Science

Surgical Science offered a nice year-end report. For comparable units, currency-adjusted sales grew by as much as 38% in the quarter and the operating margin was 26%. Overall, operating profit beat analysts' expectations by 34%. The company seems to have done a good job of integrating the two acquisitions that were completed in 2021 and the prospects ahead look promising. As in the case of Photocure, the business will benefit from increased investments in healthcare in the future. Despite the good report, the share price fell by -7.0% in February.

Tate & Lyle

The British ingredient company Tate & Lyle is a new medium-sized position in the fund. The company has a product portfolio that mainly consists of sweeteners, starches and fibers that are sold to manufacturers of food and beverages. A couple of well-known customers are, for example, Coca-Cola and Nestle. The core competence of the company consists of replacing sugar with sweeteners. This is a structurally growing market with a growth of at least 5.0% per year.

The company has long been one of the lowest valued in its category. European ingredient companies are often highly valued. The reason for the low valuation can be explained by Primary Products - a segment within Tate & Lyle's operations that is characterized by low margins, low growth, and high exposure to volatile commodity prices. Last year, it was announced that Tate & Lyle will sell 50% of this business to the private equity company, KPS. The transaction is due be completed before the end of March and following that Tate & Lyle's exposure to Primary Products decreases significantly.

In its new form, Tate & Lyle wants to grow sales by at least 5.0% annually and the operating margin will be improved by at least 0.5 percentage points annually. Overall, we expect profit growth of 10-15% per year. The company is already well on its way after recently upgrading its expectations for the full year regarding the remaining operations. With a net debt close to zero, organic growth will also be supplemented by acquisitions in growing categories for sugar substitutes (e.g. stevia).

The investment thesis is based on Tate & Lyle being gradually upgraded as the new company structure becomes clear to the market. In addition, the company must of course continue to deliver operationally. On our estimates, the stock is trading at approximately 13x EBIT 2024e (the year ends in March), which is not demanding compared to historical multiples or competitors, which are often valued at more than 20x EBIT on forward-looking estimates. The investment has so far been good for the fund as the share price rose 7.0% in February. We hope to have reason to return to this subject later.

Sedana Medical

Sedana Medical also delivered a good quarterly report. Sales expectations were beaten by 34%. We have owned Sedana for several years now and cannot recall ever been disappointed with the company’s performance. During the period, the first units of recently approved Sedaconda were sold to customers in Germany. In the coming quarters, Sedana will roll out the product to more European markets as price discussions in the various countries are completed. The share fell 8% in February.

Truecaller

After Truecaller released a reverse profit warning in January, the full report for the fourth quarter of 2022 came out during the month. For the full year, sales grew by 130% to just over SEK 1.1 billion (!) and the adjusted operating margin amounted to as much as 40%. The growth conditions for the coming years continue to look very bright. We outline that the company can grow 40–50% over the next five years to continued high margins. Combined with low capital requirements, the cash conversion will be very good. The stock is trading at 16x EBIT on our estimates for 2024e and rose 3.0% in February.

Lindab

After beating expectations in the last 8 of 9 quarters, Lindab released a report with 9.0% lower operating profit than analysts estimated. The main reason for the deviation was an operating margin that was lower than expected in the Profile Systems segment. If you sum up the full year 2021; however, it must be stated that the management has done a phenomenal job. Following the report, a string of insiders bought shares, including CEO Ola Ringdahl. At the time of writing, Lindab has also just announced its first slightly larger acquisition in a long time. The acquisition adds about 7.0% to full-year sales. The share fell 15% in February.

Rugvista

We continue to be impressed by Rugvista. Management has defied the laws of gravity in the e-commerce sector by delivering as expected or better since the IPO. In the fourth quarter, sales grew by 7.0% organically despite being compared to a “pandemic doping” quarter in 2020, when growth amounted to 55%. In 2022, a new website will be launched, which we believe will significantly increase the conversion rate (the proportion of web visitors who also shop). The valuation is very low. In our estimates, the share is traded at single-digit multiples 2024e. The share price fell 11% in February. During the last day of the month, 1 million shares in Rugvista were brokered, which is just under 5.0% of the company. This is positive as there has been an overhang of shares for a long time.

Finally, we would also like to mention the British companies Wincanton (which raised its full-year guide), CVS Group (which provided a positive trade update) and Finnish Sampo, which released good financial statements.

Short positions

The short portfolio contributed with a positive result during the month. Our short-term derivative positions in the German DAX and the American Nasdaq had the largest contribution. Some stock-specific short positions that contributed positively to the result were Swedish Vimian, Dometic and German Gerresheimer.

Exposure

The net exposure, adjusted for our unlisted holdings, at the beginning and end of the month was 74% and 60%, respectively.

Summary

Market development in February was volatile to say the least and the world's stock markets were under continued strong pressure. The broad European index fell by a relatively modest 3.4%, with the English FTSE dampening the decline. The German DAX fell by 6.5% and the fund's value decreased by 6.0%. Three companies, Victoria, CVS Group and Arcticzymes together negatively contributed with 4.0%. Our view is that there are no fundamental reasons for the negative price development of these shares, but that it is basically solely due to large sales flows.

There is an unusual amount of information to process right now for the world's investors and volatility and direction are determined, day by day, to a large extent by the war headlines on the screens. We continue to focus on our companies, risk management and trading gently. It is more important than ever to have an open mind and assume that what is apparent rarely happens and vice versa. The summary we made in last month's letter still applies, but with the invasion of Ukraine, we hit a new bottom on most European stock exchanges in February. However, the US stock market performed better.

It is paradoxical that we had the best reporting period ever in terms of outcomes compared to expectations while at the same time the fund has had a two-month negative streak. It is not the worst drawdown since inception four years ago and last time (February/March 2020) the fund experienced its largest drawdown we came back strong and recovered all losses in about three months. We cannot say that the recovery will be as quickly this time around, but we are confident in our process and believe that will pay off in the long term. We interpret this dispersion between company expectations vs. outcomes to be a result of that the correlation between different shares and asset classes has increased in recent weeks, which means that when there is a "risk off" in the market, selling occurs across the board. You care less about how the company has performed, you just want to increase your liquidity and sell fast.

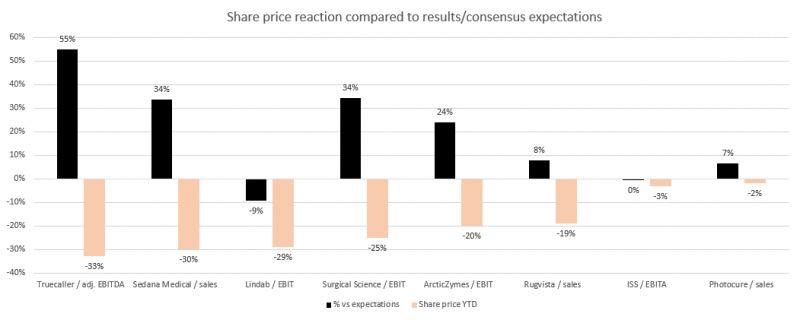

The picture below shows some of the Q4 market expectations for several our large holdings. For each we also show how the share price performed during the first two months of the year. It is evident that despite very strong company reports, most shares have been under great pressure. This has of course been frustrating in the short term, but in the longer-term fundamental development should correlate with share price development.

Source: Coeli Absolute European Equity

On the theme of having an open mind and being prepared for the unexpected. If you had received all the information the day before the invasion of Ukraine, you probably would not have expected the Nasdaq in the US, after an initial fall of just over 3.0%, to close, up just over 3.0%. The turnaround coincided quite precisely with a 20% decline since the peak at the end of 2021. The broad European index closed the next day, Friday 25 February, at +3.0%. It is the first Friday since November 12 (!) that the index closed on a positive number.

At the beginning of the year, German producer prices have risen to the highest rate since 1949. This means that central banks can hardly assist in lowering interest rates soon. Our view remains that inflation will reach its highest level in the next 2-3 months. However, the Ukraine conflict increases uncertainty, as it drives energy prices, among other things.

The above pushed up the German 10-year interest rate to over zero percent for the first time in three years. When the war broke out in Ukraine, interest rates retreated, and the ECB communicated that the conflict "may delay stimulus exit".

Source: Bloomberg

The US 10-year interest rate, which until recently largely dictated the stock market, has also come under pressure. Our view has been that the interest rate will probably reach its peak during the second quarter. The outbreak of war has probably preceded this event and we may have already passed the highest levels.

Source: Bloomberg

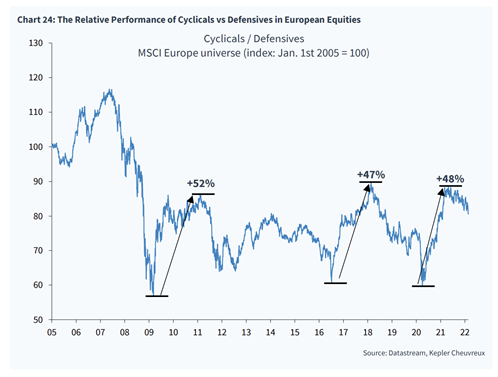

After a strong development, the cyclical companies are now starting to fall in relation to more defensive companies. A rising interest rate indicates increased economic activity. A falling interest rate has the opposite effect and cyclical companies tend to move when profit estimate rises or falls. We will most likely have lower growth in the coming period than we recently forecasted. Bank shares should also find it more difficult to assert themselves in this scenario.

All other things being equal, a falling interest rate should rekindle interest in growth equities.

Source: Kepler Chevreux

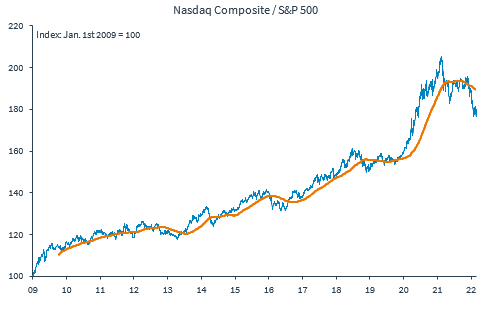

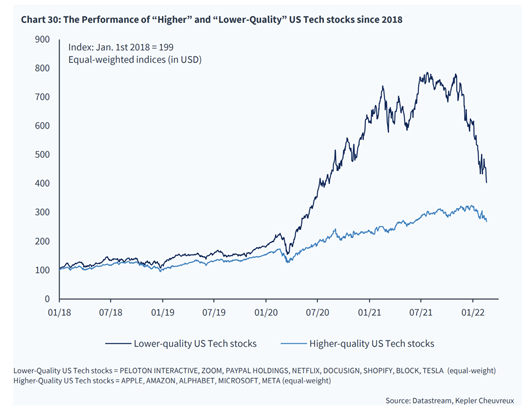

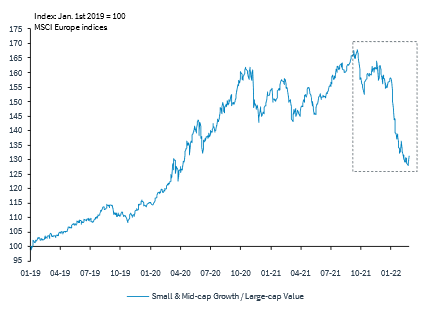

The difference in price development between "higher" and "lower" quality on Nasdaq is huge. A selection of companies that are included in each class can be seen at the bottom of the picture.

Europe's equivalent of growth stocks are small and medium-sized companies. The decline has in many cases been enormous (to be frank, in many cases we came from high levels). For smaller quality companies such as our own Surgical Science, there should be good conditions for the negative price trend to be broken soon.

Source: Kepler Cheuvreux

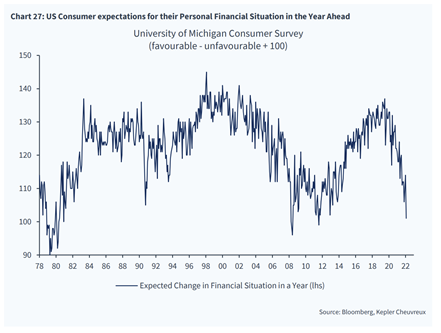

American consumers are really depressed despite a hot economy. High inflation has a negative effect on consumers, including rising interest rates. Sharply falling share prices in many private savers' favourites probably also play a role.

The application for new mortgages (below) has fallen sharply during the beginning of 2022. A rising interest rate level is of course a highly contributing factor, even though the levels remain historically low.

Source: Bloomberg, Goldman Sachs

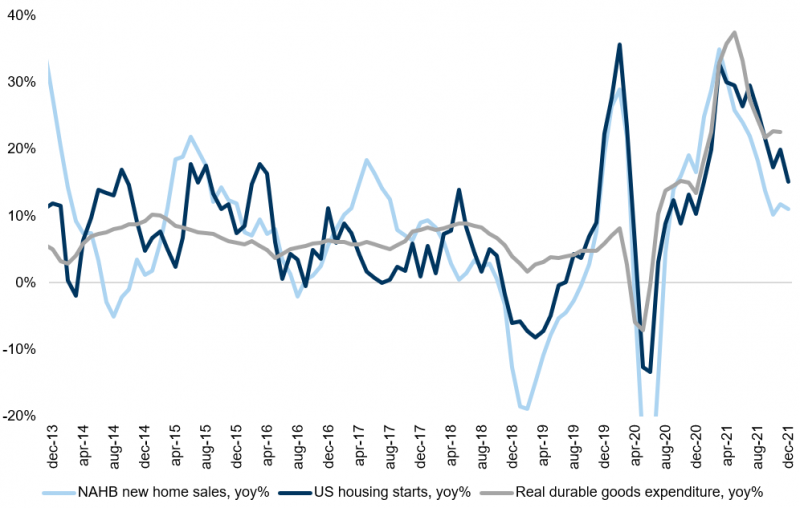

The picture below is relevant as the correlation between consumer goods and a strong housing market is strong.

Source: Goldman Sachs

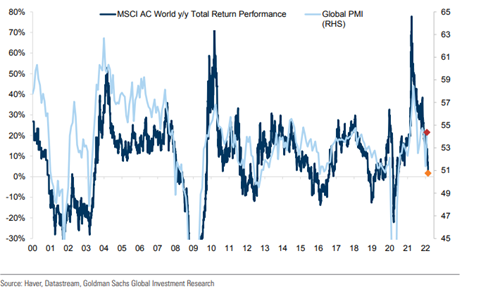

From covid to inflation concerns and now the (soon) focus on how strong the growth will be for the second half of the year. However, it appears that the market has already discounted a sharp slowdown, see below.

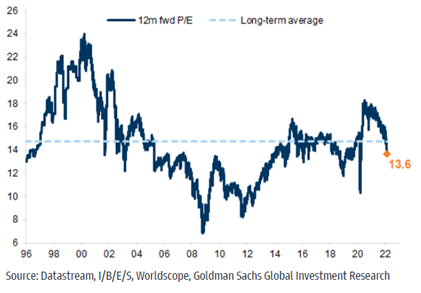

Valuations are starting to come down to low levels and are now trading below average for the last 25 years. The Ukraine conflict hangs heavily over stock market sentiment. What is positive is continued low interest rates, a world that is opening up after two years of pandemic and increased tax-financed investment in many countries. The companies' balance sheets are strong, and share repurchases are at a level not seen since the financial crisis.

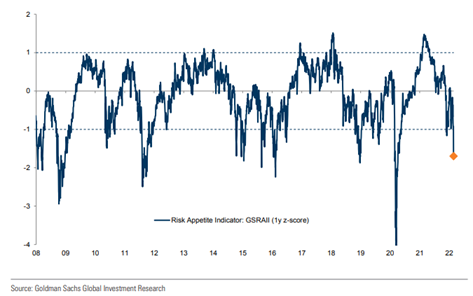

Goldman Sachs risk indicator is now down to -1.5, which historically are usually good levels to increase equity risk at. The difference this time compared to many times before is that central banks cannot influence in the same way, as inflation must first come down.

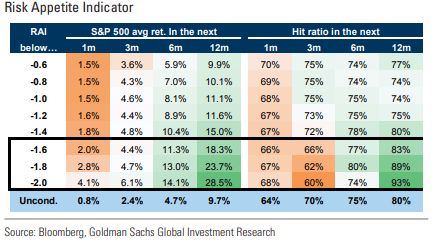

The table below shows on the left the historical return at different levels of the risk indicator and on the right the accuracy.

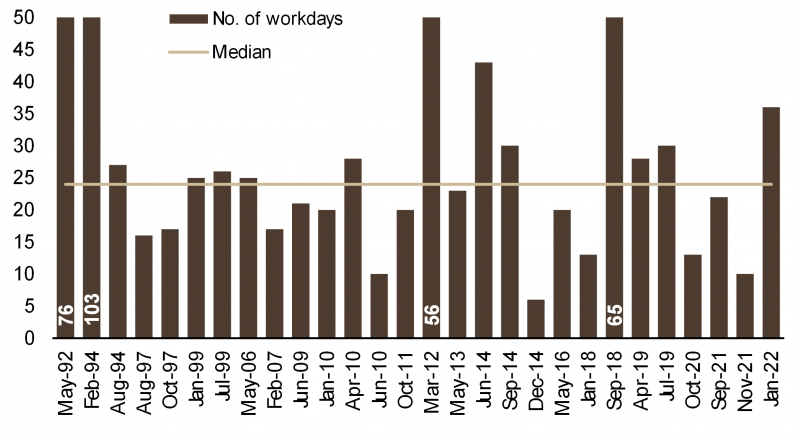

The image below illustrates how long historical corrections have been going on. We are beginning to approach historically high levels.

Source: UBS

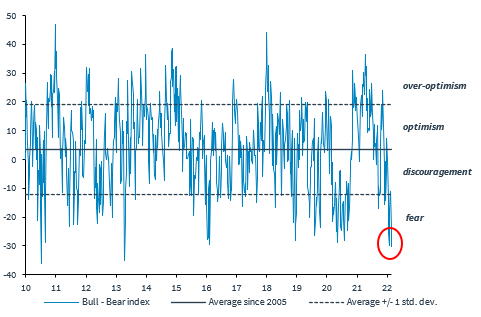

In summary, market sentiment is at rock bottom. Very few have a positive view of the stock market and the picture below sums it up well. That's a good starting point.

Source: Kepler Cheuvreux

The US stock market has so far held up well and we believe it will continue to hold up. If true, stock prices are likely to be traded flat until some new and visible information becomes available.

The risk on the downside is obviously the increasing problem in Ukraine and an inflation that continues to rise. On the upside, the opposite is true, as well as the fact that very few are positioned for a positive development. The interest rate risk itself is probably well discounted and the concern right now is mostly due to the geopolitical development. Let's hope it calms down and of course mainly for the sake of the Ukrainian people.

We end something unorthodox with a fitting clip.

Mikael & Team

Malmö, March 3, 2022