Portfolio Manager comment Coeli Global Select November 2022

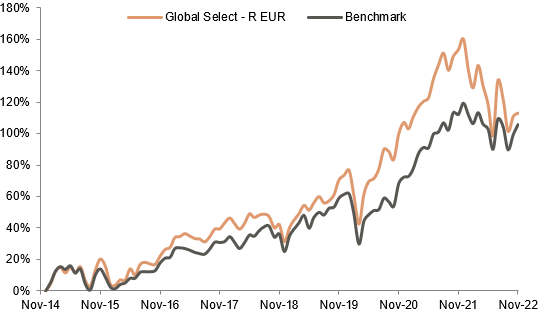

November proved to be a relatively good month for the stock markets, resulting in NAV increasing for Coeli Global Select. What most pleased the markets was the statement by Jerome Powell, the Fed chair, that the rate of increase in short-term interest rates will slow. In real terms, this means fewer large hikes in policy rates, which is positive for the economy. Coeli Global Select’s NAV for November was 1.03%, which was 2.26 pp short of our benchmark index. The shortfall to the index for the month can largely be explained by the index having had a more favorable closing on the last trading day of November than our global fund.

Our strongest performers in November were Sterling Infrastructure, ASML, and L’Oréal. Those that performed most poorly in the month were Pagseguro, United Health, and Amazon.

Sterling’s top performance was prompted by its superb report, in which revenues were up by 20% and net profits by 35% y/y. On the conference call, the CEO explained that the order book had expanded by double digits – a remarkable achievement in these challenging times for the weakening US housing market. The next best performer was one of our marvelous Champions, cosmetics and beauty products company L’Oréal. During November, we met its CFO and discussed sustainability and the company’s economic development. We also attended ASML’s capital markets day in Veldhoven and visited Société Générale in Paris.

Key market events and trends (what has influenced performance most?)

Good inflation figures from the US added most fuel to the market’s rise this month. As inflation drops, the market discounts that central banks will make fewer raises that will impact the market positively. If low inflation increases gladden the market, then it is currently looking negatively at good labor market reports. A too robust labor market puts wages at risk of rising too much, and this is exactly what central banks want to avoid. To take down inflation, wages increases must be held back. All this information on interest rates and the labor market is discounted in the US 10-year rate, which fell back during November.

During the reporting season, we saw signs that companies are reviewing their costs. The global tech sector, in particular, is holding back on new recruitments and even cutting the number of employees. This is especially true among companies that have grown without increasing their profitability, including Twillio, Salesforce, Twitter, etc. These companies are not holdings in the fund.

We see signals from China of widespread resentment toward the country’s harsh lockdown policies to hinder the spread of the coronavirus. People are out on the streets of some cities, showing their discontent by protesting. One measure the Chinese government has taken to lessen the effects of the lockdowns is to reduce collateral requirements for Chinese banks. This means more generous lending terms, which is positive for small and medium-sized companies.

Portfolio changes

During November, we sold software company Truecaller and in its place we bought the US’s AutoNation as a Special Situations holding. AutoNation reminds us of the Swedish Bilia, with two factors in particular that stand out: first, its valuation is especially low; and second, the company is buying back an enormous amount of shares. Share buybacks will do wonders for its earnings per share in the coming quarters.

The fund’s positioning – our market expectations

We believe the multiples contraction (narrowing P/Es) among quality companies with slightly higher valuations from the turn of the year to November has drawn to an end. We consequently see decent upside for our Champions thanks to their earnings growth. The combination of our Champions with our Special Situations holdings leaves us with a compelling portfolio. Remember, the best stock transactions are made in the worst of times. This bears repeating.

News

We have started a new global small cap fund, called Coeli Global Small Cap Select. All you need to do is sign up for our newsletter, where we will provide a link to access a list of the Small Cap Select’s holdings.

Coeli Global Select

| Performance in Share Class Currency | Mth | YTD | 3 yrs | Since incep |

| Coeli Global Select – R EUR | 1.03% | -18.07% | 24.99% | 112.97% |

| Benchmark | 3.29% | -6.20% | 29.47% | 105.68% |

Andreas Brock, CFA

Portfolio Manager Coeli Global Select

Henrik Milton

Portfolio Manager Coeli Global Select

Fund Overview

| Inception Date | 2014-11-28 |

| Management Fee | 1.4 % |

| Performance Fee | Yes, 10% |

| Risk category | 6 of 7 |

Top Holdings (%)

| HCA HEALTHCARE INC | 4,3% |

| MICROSOFT CORP | 4,2% |

| MASTERCARD INC – A | 4,1% |

| S&P GLOBAL INC | 4,1% |

| MARTIN MARIETTA MATERIALS | 4,0% |

DISCLAIMER. This is a marketing communication.

Before making any final investment decisions, please refer to the prospectus of Coeli SICAV I, its Annual Report, and the KIID of the relevant Sub-Fund. Relevant information documents are available in English at coeli.com. A summary of investor rights will be available at https://coeli.com/regulatory-information-coeli-asset-management-ab/.

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.