Portfolio Manager comment Coeli Nordic Corporate Bond Fund R-SEK June 2019

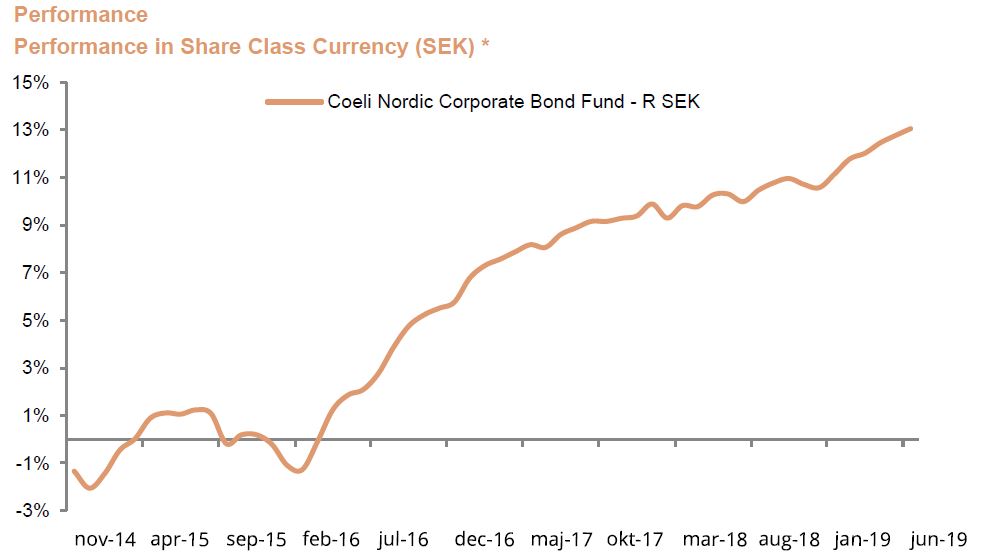

Nordic Corporate Bond Fund (Class R) advanced during June with 0.26 percent. Since year-end, the NAV per share has consequently increased by 2.24 percent. During June the corporate bond market performed well in both Europe and the Nordic region. Following the weak developments in May, investors’ risk appetite returned after the Federal Reserve together with the ECB signaled that monetary policy will focus on continued stimulus through interest rate cuts or maintained low policy rates.

The largest contributor in June was Telia, whose subordinated bonds appreciated 3 percent without any significant news being presented by the company. The strong performance is explained by falling European government bond yields and generally tighter credit spreads. The ever-lower interest rates in the euro area contributed significantly to the fund’s performance in June – the four main contributing holdings were all fixed-rate bonds in euro. The real estate company Kungsleden was also found high up on the winning list after the company received an official investment grade rating from Moody’s. In its report, Moody’s emphasizes that Kungsleden in recent years successfully has developed in line with its strategy and improved the quality of its property portfolio while maintaining a quite conservative financial risk profile.

On the negative side one primarily found the mobile operator Lebara, whose bonds fell sharply in value after the company once again exceeded the deadline for publishing revised annual accounts; in addition, the issuer announced that the interest payment for June would be delayed. In response to the issuer’s repeated breaches of the bond covenants, the bondholders have now initiated a procedure whereby the bond is accelerated and the share pledge will be enforced. The bondholders will thereby take ownership of the company after which a restructuring of the bond will be carried out, which will partly result in conversion to equity.

During the month, the fund participated in a new issue of bonds from the credit management company Intrum. Intrum has since the merger with Lindorff 2017 been a leader in its niche in most markets in Europe. In connection with the merger, the company’s leverage increased and has since remained at a relatively high level due to large investments. The company’s management is now guiding for a lower investment pace, which gives scope for the company’s credit profile to be strengthened. In addition, the fund invested in newly issued bonds from the consulting group ÅF Pöyry.

Akelius Residential left the portfolio at the end of the month, the bond was sold with good profit since the investment in March. Akelius has almost a quarter of its real estate portfolio in Berlin, where discussions are now underway to introduce restrictions on rent increases – something that, if implemented, could have significant negative effects on the properties’ market value. Icelandair left the portfolio when the company made an early redemption of what was outstanding in their bond loan. Lastly, the holding of bonds from Tele2 was divested as these were considered as fully valued.

During the month the American Federal Reserve decided to leave its main interest rate unchanged, with further communication that they foresee a rate cut in 2020. However, the market is of a different expectation with a cut as early as July already priced in, making the next Federal Reserve Board meeting highly interesting. S&P continued to show strength during the month with an increase in the index of 6.9 percent. With the first half of 2019 in the books, the S&P has showed a total increase of 17.4 percent. The last time the index started a year this strong was back in 1997.

As usual, it was an eventful month for U.S. President Trump, this time it started with removed threats of higher tariffs on Mexico. The two countries made an agreement on reduced flow of immigrants along the southwestern border. As well, Iran shot down an American drone which raised tensions in the Persian Gulf further. Lastly, at the G20 summit at the end of the month the U.S and China made an agreement to pause its trade dispute until further notice. It has been reported that a new round of negotiations will take place and that China will purchase additional agricultural products from the U.S. Some restrictions on the Chinese company Huawei will also be lifted and the introduction of new tariffs will be suspended.

In the Eurozone, ECB decided to keep interest rates unchanged, with further communication of its willingness to do whatever it takes to support the economy in the region. The Italian debt burden has once again come up for discussion, as the European Commission came out with a debt report noting that Italy’s public debt during 2018 violated the EU budget rules. Italy’s public debt reached 132 percent of GDP during 2018 and according to EU forecasts will reach 135 percent by 2020 with fear that the country’s budget deficit will exceed 3 percent of GDP next year. In an attempt to get the Italian government to revise its planned spending, the EU commission suspended its excessive deficit procedure.

Swedish inflation was reported somewhat higher at 2.1 percent for the month of May. The figure was spot on the Riksbank projections for the month.

The Nordic and European credit markets had a strong finish to the first half of the year with falling credit spreads during the month of June. Stibor 3-month fell once again below 0.0 percent and during the month the Swedish 10-year government bond was yielding below 0.0 percent. However, this was not for long, by the end of the month it was yielding above 0.0 percent once again. Long-term government bonds showed a positive trend with falling interest rates. Most notable was once again the German 10-year government bond, where the yield continued to fall and is now trading at -0.32 percent.

Coeli Nordic Corporate Bond Fund R-SEK

| Performance in Share Class Currency | 1 Mth | YTD | 3 yrs | Since incep |

| Coeli Nordic Corporate Bond Fund – R SEK | 0.26% | 2.24% | 10.74% | 14.59% |

Gustav Fransson

Portfolio Manager of Coeli Nordic Corporate Bond Fund

Alexander Larsson Vahlman

Senior Analyst

Fund Overview

| Inception Date | 2014-06-18 |

| Management Fee | 0.5 % |

| Performance Fee | N/A |

| Risk category | 2 of 7 |

Top Holdings (%)

| LANSBK 1.25% 16-20.09.23 | 4.1% |

| WHITE MOUNT FRN 17-22.09.47 | 4.0% |

| MARINE HARV FRN 18-12.06.23 | 3.7% |

| OCEAN YIELD FRN 18-25.05.23 | 3.7% |

| SHIP FIN IN FRN 19-04.06.24 | 3.2% |

DISCLAIMER. The information provided here does not constitute professional financial advice. Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested. The key investor information document (KIID) and prospectus are available at www.coeli.se.

{kind=link}