This material is marketing communication.

Note that the information below describes the share class (I SEK), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class’ return. The information below regarding returns therefore differs from the returns in other share classes.

Before making any final investment decisions, please read the prospectus, its Annual Report, and the KID of the relevant Sub-Fund here.

April Performance

The fund’s value decreased by 1.7% in April (share class I SEK), while the benchmark increased by 0.8%. Since the change of the fund’s strategy at the beginning of September this year, the fund’s value has increased by 17.8% compared to an increase of the benchmark by 7.5%.

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

* Adjusted for spin-off of Rejuveron

** Includes September 1 (strategy change to long-only implemented September 4 2023)

Equity Markets / Macro Enviroment

The fund decreased by 1.7% in April compared to our benchmark which rose by 0.8%. The corresponding figures for the year are 10.3 and 9.2%. After a very strong development for the fund in recent months, both on an absolute and relative basis, a bit of consolidation is normal. However, we had a worthy end to the month when Finnish Cargotec, which is a large core holding, presented its quarterly results. The stock rose by as much as 17% that day and taken in isolation, contributed about one percentage point to the fund’s result. Since we wrote about Cargotec at the beginning of November, the share has risen over 100%. More about this under the portfolio companies section.

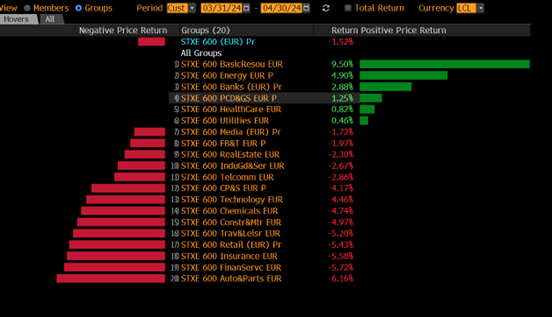

The spread in returns between different sectors was large. Below illustrates last month and at the top was basic resources which includes, among other things, mining companies that tend to rise when metal prices rise, which they did in April, in turn driven by inflation that surprised negatively. Banks also performed well when interest rates rose. Our own bank holding, Commerzbank, rose by just under 10% in April and has risen by 30% this year.

At the bottom was the automotive sector, which, among other things, is being firmly challenged by Chinese electric cars that are pouring into Europe with low prices, subsidized by the Chinese state. Our holding in Stellantis (minor position) had a weak development and fell, adjusted for dividends, by 16%. The P/E ratio for Stellantis this year is below 4x with around half of market cap being net cash. Adjusted for the net cash, the P/E number is therefore approximately 2x. Not very expensive and we took advantage of the situation and increased our position.

Source: Bloomberg

On the theme of European banks, this is the third year in a row that the sector is a winner. The conditions for European banks are at its best and many are now leaving the restructuring camp for the transfer of capital camp. Commerzbank is a great example and this year it is expected to pay out around 15% to its owners in forms of buybacks and dividends. The P/E ratio for 2025e and 2026e, respectively, after this year's strong rise, is approximately 6x and 5x. Since we made our first investment in November 2022, the stock has risen about 90% including dividends.

There are good reasons for why the banks are now enriching and repaying their hard-pressed shareholders. For the first time in almost 20 years, the banks have strong balance sheets and they are making an effort to become more shareholder friendly. The image below shows the development of the European banking index over the past 30 years. A total nightmare. The strong development of the past three years is barely visible. At the same time, the opposition in “the country of Oddness” (Sweden) is promoting a bank tax because they believe that the banks make too much money. The talent pool is not sufficient to understand that a new tax, beyond any doubt, would be transferred to the end customers.

Source: Bloomberg, Goldman Sachs

The world's stock markets began to wobble precariously right at the start of the month, and it was only at the end of April that risk appetite returned. Before complaining too much one should consider that the broad European stock market has risen in 19 of the last 22 weeks, so a pullback felt most reasonable and logical. The same mentioned period is the strongest development Europe has seen since 2012.

Source: HEDGEYE

The reason for the April retraction was (in our opinion) accelerating US long-term interest rates, which is due to inflation being more difficult to control than previously assumed. Four months ago, the market assumed that the US central bank would cut interest rates 6 times this year. Fast forward to May 3rd, when this is being written, it was believed instead that it would only happen once and not until November. A huge difference. On May 3rd, US data showed that the unemployment rate rose by a tenth to 3.9% versus an expected 3.8% and that the number of new jobs was lower than expected. Salary costs were also slightly lower than expected. This caused interest rates worldwide together with the US dollar to plummet and share prices to skyrocket with real estate and growth companies in the lead. Expectations shifted in a blink of an eye to the first US interest rate cut happening in September instead. More on that in a month.

Source: HEDGEYE

The image below shows that since the start of the year, expectations for Fed Funds futures have risen from 3.5% to 4.8%. An increase of 130 basis points! The US 10-year interest rate has risen by around 60 basis points during the same period. On May 3rd, Fed Funds futures fell to 4.5%.

Source: Kepler Cheuvreux

How can it be that the stock market this year, despite very large changes in the fixed income market, still rose by 5–7%? Most likely due to an economy that surprised all forecasters and, on top of that, corporate profits have continued to be at high levels.

As an aside, which is considered tantamount to sacrilege is that an inflation of around three percent is good lubricant to maintain the companies' high margins. Another apropos is that the strong US growth is partly driven by their budget deficit that stands at a sky-high 6% of GDP. Unsustainable in the long run, but that's an extended discussion that we will spare our readers.

In Europe the picture is different with significantly lower growth, but also an inflation that is basically defeated and will soon be down to the two percent level. After five quarters of a stagnant economy in Europe, data for the first quarter finally showed growth of 0.3% (quarter-on-quarter) compared to expectations of 0.1% and all the major countries came in better than expected. Indications are that the development will continue into the second quarter. Growth is driven by rising real wages and thus rising consumption, a less restrictive monetary policy and increased activity among manufacturing companies as energy prices and global growth begin to normalize. The lowest point has therefore, with high probability, passed and we can look forward to accelerating growth albeit from low levels. The outlook is much better!

In this situation, it will take a lot for the ECB not to lower the interest rate in June, and it will also take a lot for our own Riksbank (Swedish Central Bank) not to make the first important interest rate cut already on May 8th. It would serve as an important injection into the economic system and psychologically it would be like rocket fuel for people's faith.

In several countries, including Sweden, we have now had four consecutive months of rising property prices, which is a good indication that the turn towards a stronger economy has begun. In addition, most people will soon have rising real wages, falling interest rate costs and reduced energy costs. In principle, Sweden has been the hardest hit in all of Europe and now a reversal is beginning.

On the political stage, people are now slowly beginning to realize that they have ended up in the backwaters of global economic development. Börje Ekholm, Ericsson's CEO, warned in the Financial Times that current developments will push Europe into an irrelevant counterpart that will soon be just a museum with great food, great architecture, beautiful views, and good wines but soon without any industries. Nicolai Tangen, head of Norges Bank, noted that in Europe we have regulations but no AI, while in the US we have AI but no regulations. Europeans also work significantly less than anywhere else in the world, and at home in Sweden, the Social Democrats just had a stroke of genius and proposed 35 hours of work. They forgot to disclose how it would work out financially and that economic growth pays for rising public spending. The timing, after we are just coming out of the worst period financially for Swedish citizens since the 1990s crisis, is dead on target. The Green Party's new spokesperson, Amanda Lind, did not want to be worse. She suggested simply capping economic growth. People usually say that you get the politicians you deserve, but one is starting to have doubts.

Despite the gloomy comments above, Europe is still an excellent hunting ground for us who work as stock pickers. Clearly, management and company boards are becoming increasingly frustrated with their valuation and realize that they must become more shareholder friendly. We note that there have been an unusual number of takeovers during the beginning of the year. When even the head of the Bank of England, Andrew Bailey, says that the valuation of British banks is a puzzle; well then it is come to such a pass. Also important in this context is that the companies included in the broad European index generate 60% of their revenues from regions outside Europe, of which 25% is from the US. The companies' jurisdiction is in Europe, but in many cases, they are highly international companies with an attractive valuation.

Note the development of buybacks among European companies. The right picture shows that buybacks and takeovers led to a reduction in the total supply of listed shares this year. We believe this is another reason, in addition to valuation and attractive companies, that you should consider allocating to European equities. Europe is probably 10 years behind the USA in terms of the process of driving the nature of value creation, but now it is underway like never before.

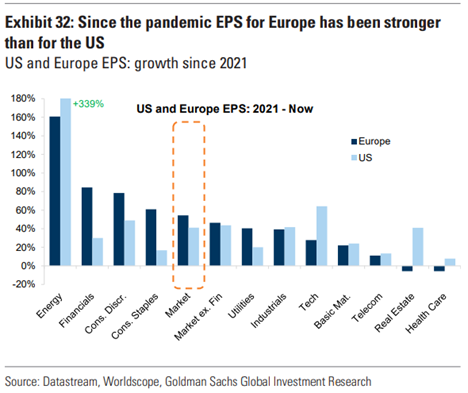

In addition, and probably surprising to most, after the pandemic, Europe has had a profit growth that exceeded the corresponding development in the US, see image below. The dividend level for companies within the Stoxx600 is today 4.8% compared to the S&P500’s 3.5%.

Portfolio Companies

Corem

Like many other companies, Corem reported in April. The first quarter’s management result was approximately 20% worse than expected. Having said that, Corem continues to have positive net rental (+ SEK 49 million), even after a strong 2023 (+ SEK 83 million). These numbers do not show in the results yet but will contribute to the future. Vacancies are still at high levels and the focus for the company is to fill up empty spaces.

Corem is something of a macro game where we can leverage on lower interest rates. Corem has higher debt and a lower valuation than many other real estate companies. When the Riksbank (Swedish Central Bank) lowers the interest rate, which we believe will happen in May, Corem’s interest rate costs will be impacted by approximately SEK 80 million on an annual basis. As interest rates are lowered, yield requirements also decrease. We have seen significantly smaller adjustments to the yield requirements during the first quarter, which suggests that we are now approaching the peak. Should Corem’s yield requirement be adjusted down by 25 basis points, the valuation of the properties would increase by as much as SEK 2.4 billion, or just over SEK 2 per share. It is very large in relation to the market capitalization, which today is just over SEK 9 billion.

Biotage

Biotage came out with another good report in April, this after two previous reports that were significantly better than expected. This time the result was 15% better than expected, largely driven by Astrea. Despite this, there were grumpy faces from the management team who wanted to see more growth. Organic growth decreased by 1% but if the company had had the capacity to deliver on demand, organic growth would instead have been as much as 8%. This can be compared to Sartorius, which reduced sales by 8% organically, Repligen by 20%, and Danish Chemometec, which issued a profit warning. Impressive by Biotage.

The big demand right now is for Biotage peptides, which are used for GLP-1 research. These have become extremely sought after lately following the success of Novo Nordisk and Eli Lilly’s in weight loss. This is naturally a relatively new area for Biotage. It is a quality stamp among many fine companies to find new ways to grow turnover, and Biotage is part of that crowd.

During May, Biotage will have a capital markets day in Cambridge where the company will guide the market on how the business will look after the acquisition of Astrea. We believe this can be a positive catalyst and we will be on site in Cambridge. At this point in time, we can forecast a 50% upside in the share in a year's time.

Cargotec

Finnish Cargotec delivered stellar figures in its report. Operating profit was a whopping 47% better than analysts' estimates. Delightfully, all three segments contributed to the result exceeding expectations. We are now getting closer to the spin-off of the Kalmar subsidiary, which is expected to be listed in Finland on July 1st. After that, Cargotec will try to sell its other subsidiary, MacGregor, in the second half of 2024. MacGregor has a few unprofitable off-shore projects in the order book and when these are delivered on, the company will be put up for sale. If all goes well today's Cargotec will only consist of the third subsidiary, Hiab, within a year.

In our October letter we wrote that the valuation was so low that we did not believe it was true. In hindsight, it was completely correct. The stock has since risen by around 110%. At SEK 36, where the share bottomed, one can say that the valuation implied a payment for Kalmar while getting Hiab and MacGregor complimentary. The stock rose 17% during April.

SLP

The small real estate company SLP, which soon will not be so small anymore, continues to spoil us with good reports. Operating result was approximately 10% better than expected. We feel very comfortable with SLP and think it ticks all the boxes to be put on the shelf. Net letting rose by SEK 20 million after a strong 2023 of SEK 76 million. Rental income rose 42% over last year, driven by acquisitions, indexing and project completions.

Historically, the company has made acquisitions at an average of SEK 1.7 billion a year and with a loan-to-value ratio of 42% the company today could make acquisitions at SEK 2.5 billion. On a rolling basis, net operating income has risen by SEK 154 million over the past year, while central costs have decreased by SEK 1 million. Simply put, a company that takes good care of its shareholders' money.

Bonesupport

Bonesupport delivered yet another good report with an operating profit that was roughly 20% better than expected. The share price developed strongly before the report but then fell on the day of the report despite a good result. We have seen this happen several times with Bonesupport in recent quarters.

Operationally it is clear that the company is firing on all cylinders right now. The company hints that things are going so well that they lack the capacity to reach out to all the hospitals where they have been approved to sell. We believe there is upside in the estimates toward the end of the year when the company starts selling products for the indication trauma.

Scandic Hotels

Scandic has been a new holding for us for some time now. Most people in the Nordics are familiar with Scandic and the business is easy to understand – it is a hotel operator in the Nordic region. Sweden and Norway are the largest with around 30% of sales each, followed by Finland with 23% and Denmark with 13%. In addition, the company has a few hotels in Germany and Poland. The company has its two best years behind it and now in 2024 the company can make some offensive investments after putting out fires in the wake of the pandemic.

Scandic is one of the cheapest companies on the Stockholm Stock Exchange. Based on our estimates, the company is valued at EV/EBIT 6x next year with an FCF yield of 12%. We have not found anything wrong with the company, but simply believe that it is misunderstood. There are three principal things that might scare investors:

1. Shorting. Scandic is the Stockholm Stock Exchange's most shorted company. 18% of the shares are shorted. However, 99% of these are linked to a convertible that was issued during the pandemic. Hedge funds own the convertible and have sold shares in return.

2. Foreigners' concern about the Swedish economy/property market/consumer. This concern arises every time there is a little turbulence in the market. The fact is however, that the Swedish consumer has better prospects this year than in three years. The general cost pressure with higher inflation and higher interest rates is beginning to ease. At the same time, this is the first year in a long time where Swedes have real wage increases. This of course also applies in large parts of Europe.

3. Accounting. IFRS 16 is very problematic for the company as the company leases (rents) most of its hotels. With the introduction of IFRS 16, Scandic is forced to record its leasing commitments as an asset and corresponding liability. This makes the company optically look very indebted, but in fact the company will have net cash at the end of the year. Almost 70% of leasing commitments are a variable rent based on the hotel's revenue, which provides a flexible cost base and stabilizes the margin.

We don't need to make any major assumptions to see a real upside in Scandic. Foreign hotel chains are starting to approach an occupancy rate that is in line with before the pandemic. Scandic isn't there yet, but we see that as an upside. In 2023 the rental rate was 61%, which can be compared to 65-67% before the pandemic. The company itself says that events and conferences are starting to increase, and the Asian tourists (mainly Chinese) are starting to return. The price per hotel room follows inflation quite well so it is relatively easy to estimate. This means that within a year or so we will probably be back at the same occupancy rate as before the pandemic.

If we disregard pandemics (which statistically occur every 100 years), we can look at a worst-case scenario: the GFC. At that time Scandic lost 13% of its turnover and about 40% of its profit. If that were to happen next year, it would mean that Scandic today trades at EV/EBIT 10x at absolute bottom profits. It is very cheap for a company that returns 23% on capital. During the GFC, Scandic was also more in debt compared to the net cash we estimate at the end of the year.

As mentioned, the company was heavily affected by the pandemic which forced it to make a rights issue, issue a convertible loan and take a bank loan. The management has been clear that they now want to give back to the shareholders. We believe it will occur in the form of buybacks and dividends. We are convinced that the company will redeem the convertible in a clever way this autumn.

Summary

We are now rolling into the summer months which have historically been a weaker period in terms of returns. However, it is wise to continue to have an open mind and be prepared for discrepancies in traditional patterns as after a pandemic and a war they tend to look different and to recognize that conditions have changed for everything and everyone. Rising inflation with interest rate hikes all over the world crushed the companies' valuations two years ago. Remember the summer of 2022 when the Fed raised interest rates three months in a row by 75 basis points each time. Now we probably have two years of interest rate cuts ahead of us and in Europe it is close to begin. Below, the traditional seasonal pattern for the S&P500 including election years.

Source: Goldman Sachs

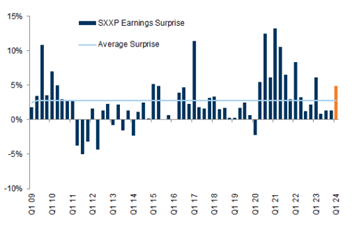

Many were skeptical about the companies' earnings power ahead of the reporting season, but so far it has been absolutely excellent with an average of 5% higher than expected profits. See bar on the far right.

Source: Goldman Sachs

There have also been positive surprises in the US.

Source: Goldman Sachs

This has contributed to the rise in profit expectations, both in Europe and in the US, compared to three months ago. The consensus for next year's earnings indicates strong earnings growth.

Source: BNP Paribas

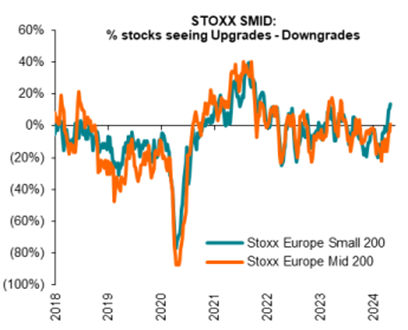

Even our focus area, small and mid-caps, has seen upward adjustments to profit expectations during the first months of the year.

Source: BNP Paribas

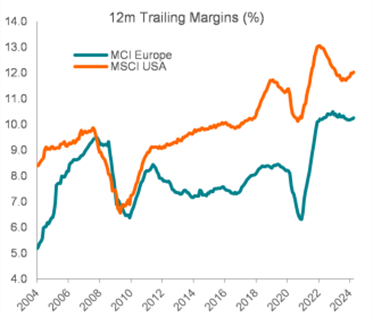

The picture below shows that companies have managed to maintain their relatively high margins. When valuing a company, the level of the margin is somewhat uninteresting but the company's return on capital is what largely determines the valuation. If you simplify and say that the picture below also applies to the companies' return on capital, then it is very easy to argue that the multiples today, all other things being equal, should be higher than they have been historically.

Source: BNP Paribas

Regarding valuation. The image below from Goldman Sachs (thanks) shows the performance of a basket of companies that have strong cash flows versus a basket that has weak cash flows. I quote an unknown financial legend: "Free cash flow is the corporate truth teller".

Source: Goldman Sachs

Earnings and profit growth are therefore in good shape. What does the current valuation look like for European stocks? Still attractive is the short answer. The image below shows the Stoxx600 compared to the S&P500 including and excluding the large growth companies in each region. The valuation difference is still at a historically low level.

The returns of smaller companies in relation to larger companies had an explosive development in November and December last year, while in the first quarter all excess returns were given back. Interest rates was the main driver. An improvement can be seen in the last month and our view is that this asset class, when the rate cuts actually happen, will be a winner.

The image below shows the difference in valuation between smaller and larger companies. As of the end of April (thanks Joakim Tabet), smaller companies were valued 7% lower than larger companies, which is a historic low. Historically, the average premium has been 17%.

Source: Kepler Cheuvreux

In conclusion, we still think conditions are unusually good. Geopolitically, it's mostly misery, but the market has currently decided that the wars in Ukraine and the Middle East are isolated conflicts that do not appear to be spreading. The temperature in the cold war between the United States and China drops by a few degrees every month, and most recently, Tiktok is to be banned in the United States. But economically, much is going in the right direction and there is high distrust in the market that this will last, which is positive. Above all, the permafrost and ice winter have left us in Sweden and now we have the best months of the year ahead of us!

Have a sunny and beautiful month of May and thank you for your interest.

Mikael & Co

Malmö on 7th of May 2024

IMPORTANT INFORMATION. This is a marketing communication. Before making any final investment decisions, please refer to the prospectus of Coeli SICAV II, its Annual Report, and the KID of the relevant Sub-Fund. Relevant information documents are available in English at coeli.com. A summary of investor rights will be available at https://coeli.com/financial-and-legal-information/.

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested. Please note that the management company of the fund may decide to terminate the arrangements made for the marketing of the fund in one or multiple jurisdictions in which there exists arrangements for marketing.