Note that the information below describes the share class (I SEK), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class' return. The information below regarding returns therefore differs from the returns in other share classes.

Before making any final investment decisions, please read the prospectus, its Annual Report, and the KIID of the relevant Sub-Fund here

This material is marketing communication

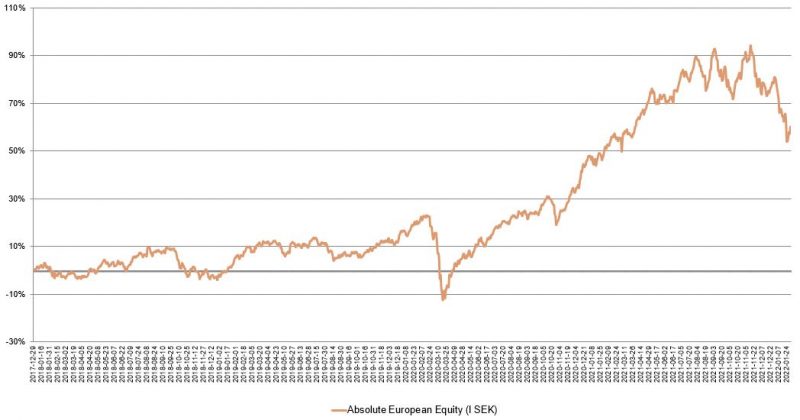

Monthly Newsletter Coeli Absolute European Equity - January 2022

January performance

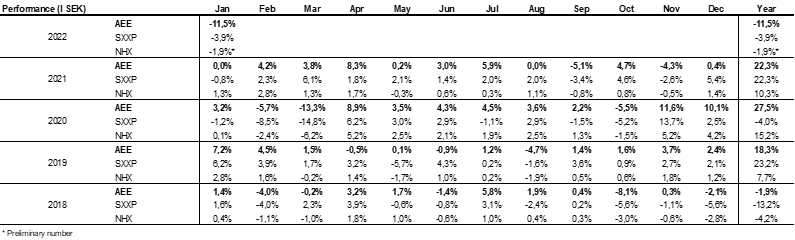

The value of the fund decreased 11.5% in January (share class I SEK). The Stoxx600 (broad European index) decreased during the same period by 3.9% and HedgeNordic's NHX Equities fell provisionally by 1.9%.

Equity Markets / Macro Environment

Source: Bloomberg

The front page of Bloomberg Businessweek sums many investors’ feeling right now. A strong finish to 2021 abruptly ended a few hours into the New Year, when the US 10-year interest rate rose sharply on Monday, the 4th of January. After that the strongest sector rotation that the author has experienced (in almost 30 years) began, coupled with a severe turbulence between different sectors and asset classes. After only 10 trading days, there were plenty of examples where companies with a high valuation and growth rate lost 40% (!) in relative returns compared to, for example, a typical European bank share. The magnitude is not unique, but the speed at which it occurred was rare. We believe this movement is exaggerated and that it will reverse. We also believe that the stock market will rise from today's levels and deliver a positive return for the year, but the terrain will be punchy. More about that under summary.

The broad European indices performed relatively well as they are higher weighted in energy, commodities, and bank shares. The S&P500 and Nasdaq were down 5.3% and 9% while the FTSE (UK) rose by 1.1%. The Stockholm Stock Exchange was among the weakest in Europe and the broad index decreased by 9.8% percent. The fund had a very weak development and decreased by 11.4%. More about that below.

The picture below shows winners and losers on the S&P500 in January. The trend is quite clear. Underweighted value companies at the top and Covid winners at the bottom. It feels like investors have declared the pandemic dead faster than the Swedish Public Health Agency.

Source: Bloomberg

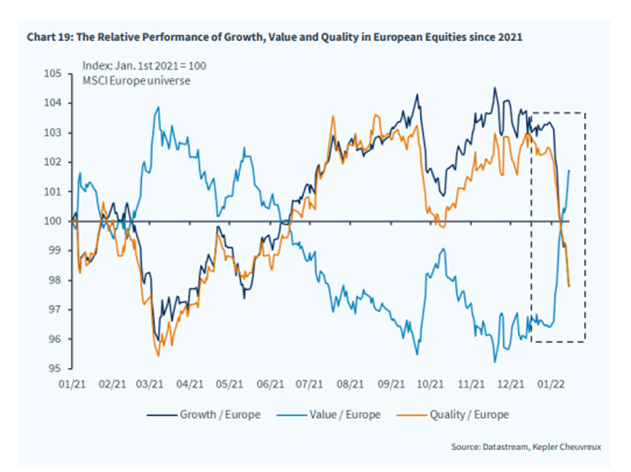

The rotation from growth to value shares has been extremely rapid.

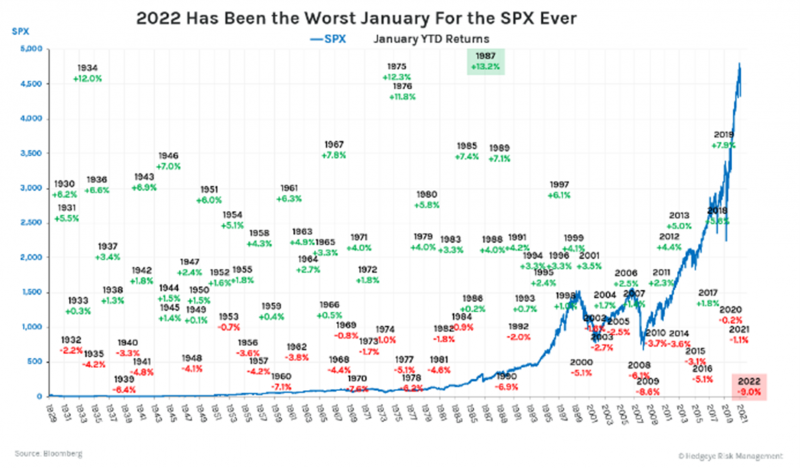

It can only get better, right? The beginning of 2022 has been weak, to say the least. The picture below is as of January 27th and the beginning of the year was at that time the worst ever - to put things in perspective.

Source: Bloomberg, Hedgeye Risk Management

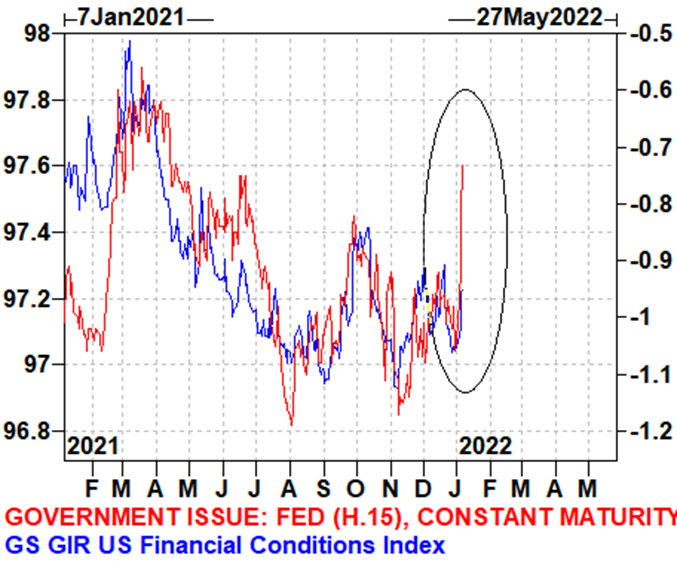

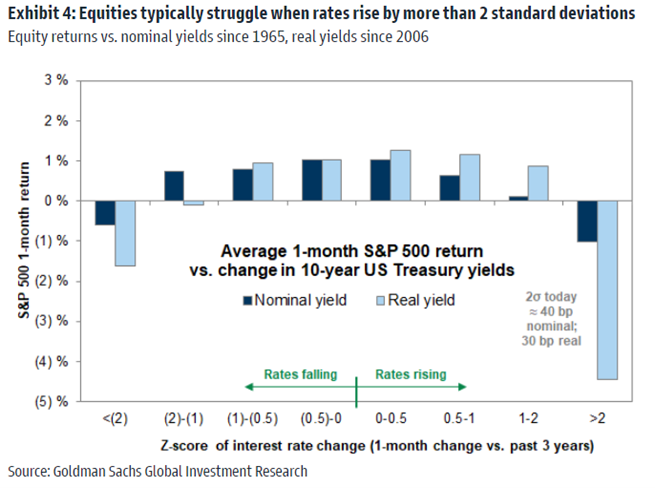

The rise in the US 10-year interest rate on Monday, January 4th, was more than two standard deviations from the mean. Below is the US 10-year interest rate and Goldman Sachs' Financial Conditions index. It is not the level itself that triggered the turbulence, but the rate at which interest rates moved. An important addition here, which no one can stomach when the gunpowder smoke overcast the markets, is that the interest rate can rise by another 100 points from today's level and still be positioned in the most favourable interest rate climate that has been experienced during the 2000–2019 period.

Source: Goldman Sachs

Below is an illustration of how shares have historically developed in response to various interest rate movements. It is the tails that cause significant disruption, which is shown here as the movement of more than two standard deviations. In all other environments, a positive development is ordinary. January 2022 certainly added to the historical database.

When US Federal Reserve Chairman Jerome Powell was re-elected by President Biden on November 22nd last year, inflation was defined and accelerating. Our own US contacts, which are close to US politicians, then indicated that President Biden, in connection with the re-election, wanted a clear change in communication about how the Fed should tackle inflation. One reason for this is the declining popularity of the president, which correlates well with rising inflation and drains the purchasing power of the population.

After his first year as president, President Biden is the second least popular in US history (only Trump has had worse numbers) and he is desperately trying to regain command. The trend of weak politicians is obvious everywhere in the world and in this event, Sweden also boasts great successes.

As you know, the word transitory was officially buried by Powell on December 15th and was followed by several surprisingly aggressive comments from various Fed members. This further contributed to the turbulence, as the market interpreted it as the Fed lagging developments. The above events together with an accelerating inflation became the spark that caused the interest rate to rise sharply on the first day of the year.

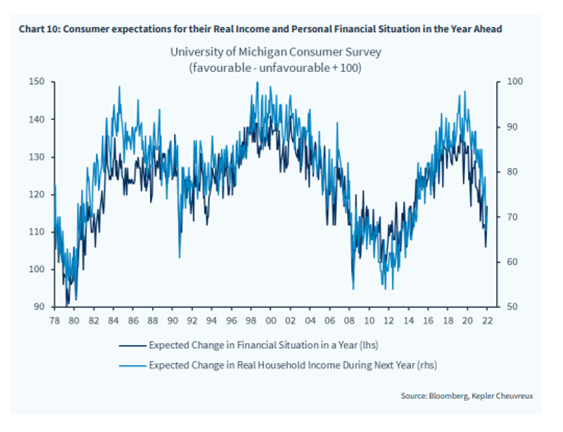

Despite a hot labour market and economy in the United States, Americans are increasingly negative about their own financial situation over the next 12 months.

When, in the first week of January, the market listened in anticipation to Powell giving the first speech of the year it failed to give a clear impression that the Fed was in control and was in line economic developments. On the contrary, in fact, and that was probably Powell's worst speech. The famous Put option that has been in play since the financial crisis and which has meant that if it gets bad enough, the central bank comes in and supports, has at least temporarily disappeared or is far from the exercise price. Powell said that the US economy is very different today compared to the one that existed when they last started raising interest rates.

The first message was that the speed of future increases will be faster. The second was that the uncertainty is greater than usual. The third was that the word steadily replaced the word gradually on how to reduce current monetary policy. In summary, their actions in the future will be less predictable and thus increase market volatility.

The most recent austerity cycles (1994, 1999, 2004 and 2015) inflation was close to or below target. Now it is far over. Powell's performance received a sour reception from the market.

Aware that the inflation target is paramount for the central bank, we do not believe that the Fed will be the one driving the country into a recession. But leading indicators clearly show that growth among the world's developed economies will enter a calmer phase with lower growth.

We believe that inflation is to some extent transient and that it will most likely be a softened choice of words communicated over the next six months. It took just 48 hours for Minneapolis Fed President Neel Kashkari to say:

"The way we bring that into balance is, we will tend to tighten monetary policy by raising interest rates. That would then not tap the brakes on the economy, but it would let our foot off the accelerator just a little bit. We just don 't know "how many rate hikes that will take.” This, together with Apple's fantastic quarterly report, contributed greatly to a strong finish in the last week of January.

The picture below shows the market's estimate of how many interest rate hikes the Fed will make in 2022 (4.75). Neel Kashkari's comment above made the curve come down a bit (you must look closely).

Source: Bloomberg

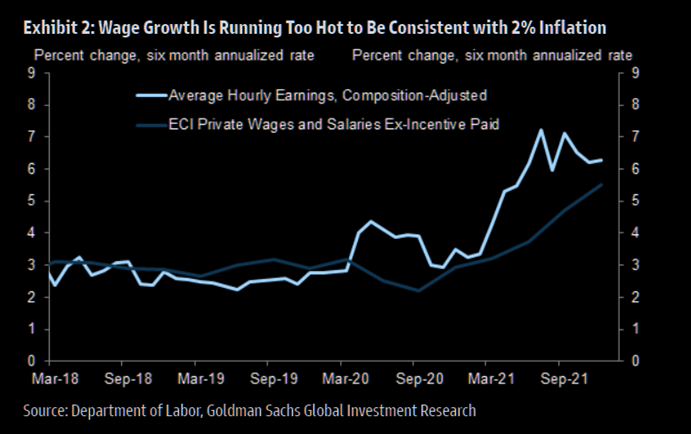

Current wage growth is too strong to reach the target of two percent inflation. Perhaps a new workforce will enter the market when those who have stopped working to stay at home and trade stocks, cryptocurrencies and options feel that they are worse off than in the past two years?

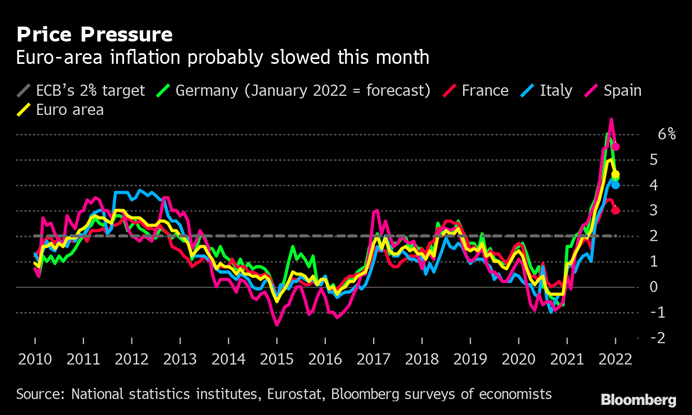

Inflation in the Eurozone is expected to have declined slightly in January, according to the latest survey.

In addition to inflation data and the Fed, Russia/Ukraine were in the spotlight during the month which created uncertainty in the financial markets. It will probably continue in the coming weeks, and we hope for an abatement. The author is invited to the annual security conference in Munich, which takes place in a few weeks, together with some other international investors. It's going to be very interesting.

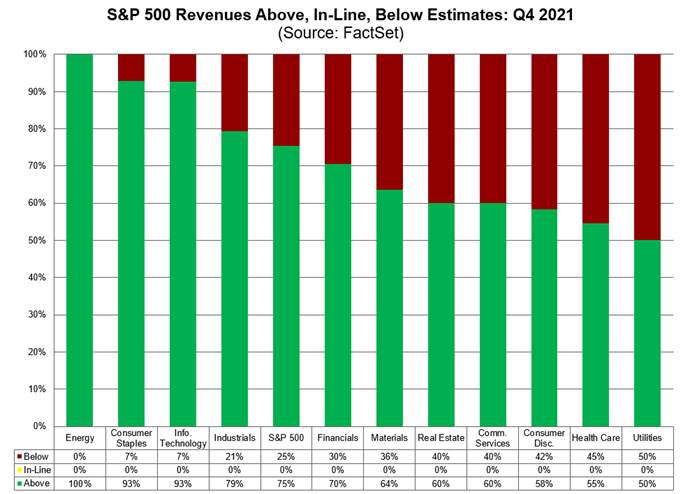

"An apple a day keeps the doctor away". It's not just Apple that has delivered good quarterly reports so far. 75% of the S&P companies have so far beaten expectations compared with the five-year average of 68%. Note the differences between sectors. Above all, note technology. It is a long way to go, but our companies also delivered strong or very strong figures in January. More about that under company comments.

Source: FactSet

Gardengate! Prime Minister Boris Johnson did not think the Downing Street party was a party but just a work session in the garden. He is now fighting his most difficult battle and the odds of him being forced to resign in February are low.

Source: Twitter

We are doing our best for the “Corona Commission," says Minister of Social Affairs, Lena Hallengren. Wondering what it looks like when things go really bad?

Source: Steget Efter

Long positions

If we put on our critical glasses, it can be concluded that, despite some divestments, we owned too many companies in the same category in January. For each individual holding, however, there is an investment thesis that we believe in. Even though several of our companies suffered dramatic declines in January, the news flow was clearly positive. In several cases we have increased our positions as we believe that many of our companies are in better shape than ever, at the same time as valuations have fallen.

Truecaller

This stock went on a real downhill in January. We had anticipated some volatility during Q1 for a few simple reasons:

- Many shareholders' lock-up has ceased, which means that more shares are (were) for sale

- The stock has had a strong performance since the stock exchange listing

- At its highest price levels, we thought the valuation looked somewhat strained

Adding to the above an increasing rotation from growth stocks to value stocks, there was a cocktail of factors that spoke against the stock in the short term. For these reasons, we sold a lot of shares at high levels at the end of 2021 and on the first day of the year in January. The share was down as much as 35% in January and of course had a large negative contribution to the fund's development. Despite this, we are satisfied with how we acted. At the beginning of the month, our holding corresponded to about a third of the position in November.

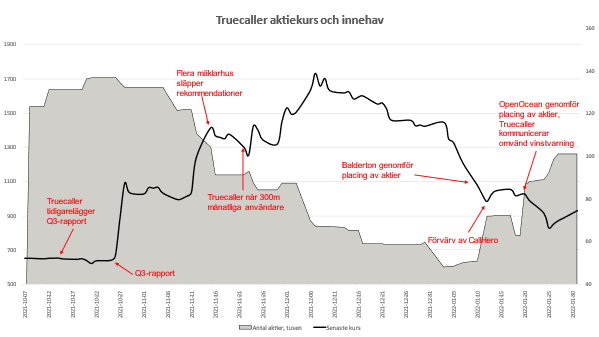

The graph below tries to give a picture of how we have traded the share since the stock exchange listing. The black line consists of the share price since the listing. The grey field represents the fund's holdings since the same time. We owned 1.7 million shares prior to the Q3 report and decreased it to 600k at the beginning of the year. We now own approximately 1.3 million, again purchased on the January sale. What is hopefully clear is that we have been consistent in our trading and sold shares when the share price was high. In the same way, we have significantly increased our position in recent weeks when the price we assess has been under too much pressure. We participated in two different placements (sale of large shareholdings via institutional brokers) carried out by shareholders who owned the share for a long time while it was unlisted. The picture below illustrates active management.

Source: Coeli Absolute European Equity

Operationally, Truecaller is doing very well. The company's report for the third quarter far exceeded analysts' expectations. This was followed up in January with a reverse profit warning which showed growth of almost 110% (!) and an operating margin (before depreciation) of 49%. That margin should be compared with the financial target of 35% after 2024. As it stands today, the margin target has already been reached.

We outline continued strong growth in Truecaller in the future, in line with the financial target of approximately 45% on average 2021–2024. At this point, the margin target appears to have passed and we believe that the company will continue to increase profitability because of the scalability of the business model. If we get our thinking right, the share trades at around 25x and 17x EV/EBIT on our estimates for 2023e and 2024e respectively. We find this attractive for a company with Truecaller's scalability and growth profile.

CVS Group

We have become accustomed to receiving good reports from the British veterinary company CVS Group. In January, it was time again. This time, the company grew by about 13% (of which 11 organically) and the operating margin improved. The company should be able to grow by 5–10% over a long period of time with a return on capital employed that exceeds 50%. Adding improved margins as the annual price increases are expected to exceed wage inflation. At the same time, the number of customer visits is expected to increase because of 1) increased pet ownership and 2) more veterinary visits per pet.

The company has been a cornerstone in the portfolio since the summer of 2020 and will probably continue to be so if nothing unforeseen happens. On our estimates, CVS is valued at approximately 14x EV/EBITA 2024e (the financial year ends in June), or alternatively approximately 16x free cash flow. It is lower than in a long time. Despite good news, the stock correlated with the January rotation and fell -12%.

Surgical Science

The growth profile and the high valuation meant that Surgical Science was hit hard by the rotation, with a decline of -30% in January. At the same time, the news flow has been positive. During the month, new financial targets were announced for 2026, by which time the company wants to reach SEK 1.5 billion in sales and an adjusted operating margin of 40%. In addition, the large customer, Intuitive Surgical, shipped more robots than analysts forecast, and we note a frequent and positive news flow from another important customer, CMR Surgical.

Sedana Medical

The Sedana Medical stock also had a tough month against the background of the rotation. The price fell -24%. Here, too, we were pleased with the positive news, when it was announced that the British Medicines Agency NICE is recommending Sedana's product Sedaconda ACD as an alternative to intravenous sedation. A cost model shows that the cost savings for using Sedan's product can amount to £4,000 per patient.

Victoria

Victoria did remarkably well for a long time in the gloomy stock market climate. As the stock was also in the upper part of its “trading range” (see graph below), we chose to sell a part of our holding. When stressed sellers later turned the share price on a downward path, we bought back the shares we sold, and more. Victoria is now the fund's third largest holding. We believe that analyst estimates are too conservative, and our best guess is that the share price will be higher at the end of the year than it is today.

The share fell -21% in January.

Source: Bloomberg

ArcticZymes

The Norwegian enzyme company ArcticZymes submitted a good report for the fourth quarter. Sales for the full year landed at NOK 128 million, compared with the company's announced target of NOK 120 million. Growth excluding Covid-related sales amounted to approximately 63% in 2021. With gross margins of almost 100% and a relatively fixed cost base, it becomes clear how scalable the business is when sales rise sharply. For the fourth quarter alone, the incremental operating margin was around 80%. With that said, we think it is best to analyse ArcticZymes on an annual basis, as results fluctuate sharply between quarters.

For 2022, the management wants to reach sales of 155 million. Assuming Covid-related sales fall by 70–80%, this implies a growth of 53–56% for other products. By 2025, the goal is to have a turnover of at least 350 million. With 2021 as the base year, this corresponds to approximately 29% in annual growth. At the same time, there is a clear acquisition agenda to supplement the current product portfolio, which is therefore not included in the figures above. As with many of our other highly valued growth companies, ArcticZymes decreased in January, despite good news. The decline landed at 6%.

Wincanton

The British transport company was the highlight of the month as it was one of the few long positions that made a positive contribution to the month's results. In January, the company announced that it expected a full-year result which exceeded analysts' expectations. The price rose 13% on the message. The company's new management has done an excellent job of cleaning up the balance sheet and repositioning its operations towards sectors with higher growth, such as e-commerce. However, the stock market still seems to perceive Wincanton as the mismanaged company it once was. In our opinion, the stock is traded undeservedly at single-digit profit multiples, and we believe that it is a matter of time before the market values the company. It is the fund's lowest valued company and the share rose 5% in January.

Short positions

The short portfolio contributed with a positive result during the month. Our short futures on Nasdaq contributed the most. Some stock-specific short positions that contributed positively to the result were Vimian and Swiss Temenos.

Exposure

The net exposure, adjusted for our unlisted holdings, at the beginning and end of the month was 71 and 74%, respectively.

Summary

We had already begun to reduce our exposure to growth stocks when we entered 2022. For example, we sold our entire position in Swedencare during November/December at very attractive levels. In conjunction with the company making doing a stock issue last week, we bought again (smaller position). Due to the large shift in sentiment that took place in the market in the first days of the year, we accelerated the process. After about a week, we had sold about 15% more of these types of companies and at the same time we increased by the same amount positions in larger liquid companies with low valuation. Companies we bought were, for example, Volvo, Daimler, UBS and ABN Amro. We did this both to balance the portfolio and because we thought it was attractive levels. In addition, we increased our short-term equity positions and went short Nasdaq futures.

In total, we thus changed 35% of the gross exposure (in comparison to today's total gross exposure of about 140%), which is a high figure, but we felt it was necessary. It has so far been completely right as the portfolio after this responded better when the market moved in different directions.

We are of course frustrated and disappointed with the start of the year. At the same time, our confidence in our equity analysis strengthens (the factory that produces excess returns), as we have had several strong data points in recent weeks. The analysis is there to create a strong conviction about a position, a necessity if you have fewer and larger holdings. It is then the selection and concentration that over time creates excess returns. We have shown this historically and when we receive these strong data points, we know that the factory still works. Important.

With a unique and concentrated portfolio, it is difficult to protect oneself in a market with significant declines in several holdings. Many of the companies have no natural hedges as they are completely unique. How to effectively hedge Truecaller? The operations were in principle exclusively flow-driven as there was an outflow from several small caps and technology funds which then had to sell parts of their holdings. The picture below shows schematically where the declines were strongest in the portfolio. Last year's winning shares were aggressively sold.

Source: Coeli Absolute European Equity

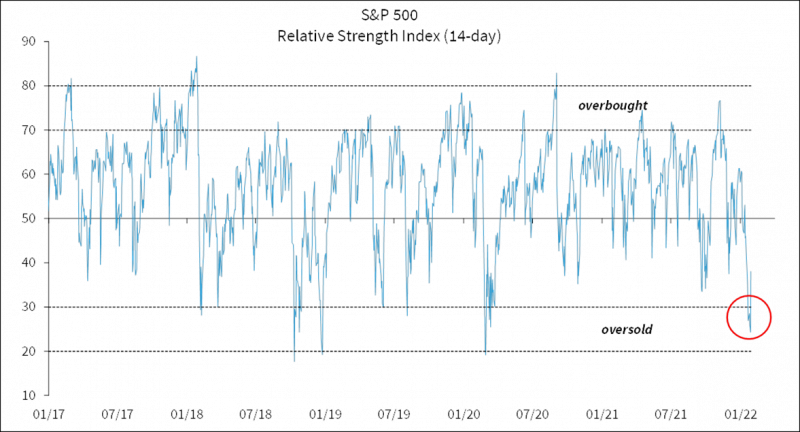

The markets have been really oversold in recent weeks. A bounce is on the cards.

Source: Kepler Cheuvreux

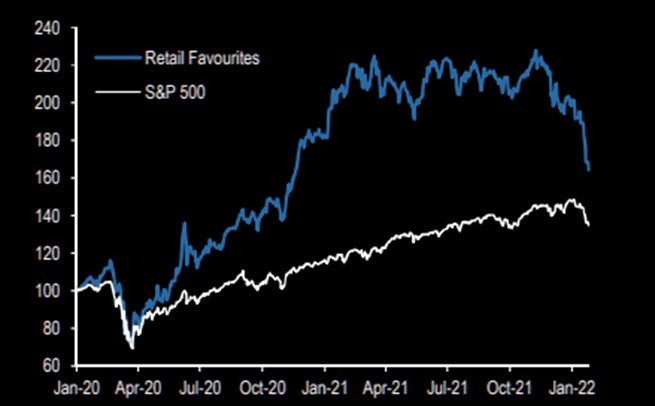

One of the better contraindicators available is to study the investment behaviour of retail investors. American retail investors are now more negative about the stock market than when covid struck in March 2020. The historical return for the S&P500 when small savers have been so negative (only January 2013 has been worse), has after three months been about +5%.

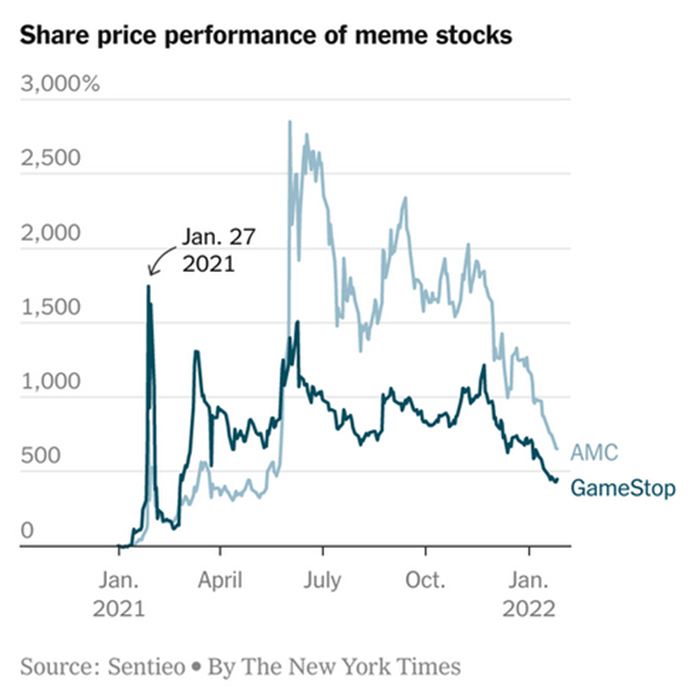

Maybe the depression of retail investors has little to do with the fact that they had too many meme stocks? Shares that have gone viral, had been declared cult and that were often aggressively shorted where average Joe/Jane wanted to get the big capitalists (woe betide the hedge funds that were short a stock). The Social Democrats' youth union also bought Gamestop and raffled off shares in January last year when the madness was at its greatest. An epic advertisement from SSU is reproduced in our monthly letter from January last year and offers entertainment at its best.

Biotech shares have not brought joy to the market in the past year either. It was actually the worst year for the sector since the early 2000s. Something we also unfortunately got to feel through our investment in Atai. Will the acquisitions come from the pharmaceutical industry this year? It does not feel unlikely.

Source: Fact sheet och Jefferies Research

Another image that explains the pessimistic view of retail investors right now. It feels like law of nature that the curves will meet before it turns.

Source: Bloomberg

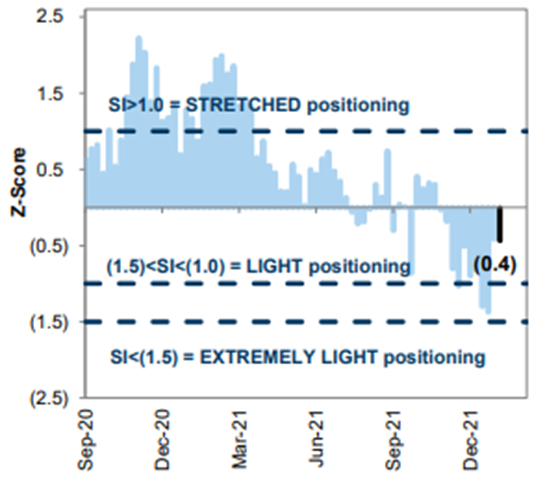

Goldman Sachs sentiment indicator shows that investors are still cautious, although the position has risen slightly in the past week.

Source: Goldman Sachs

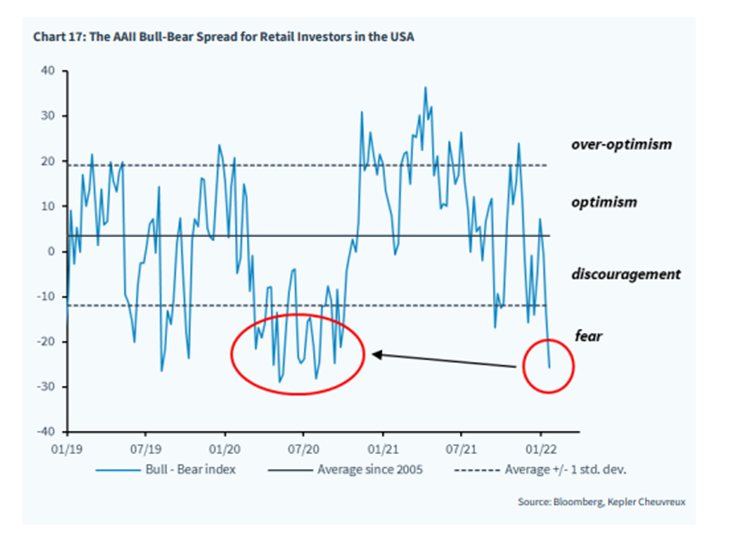

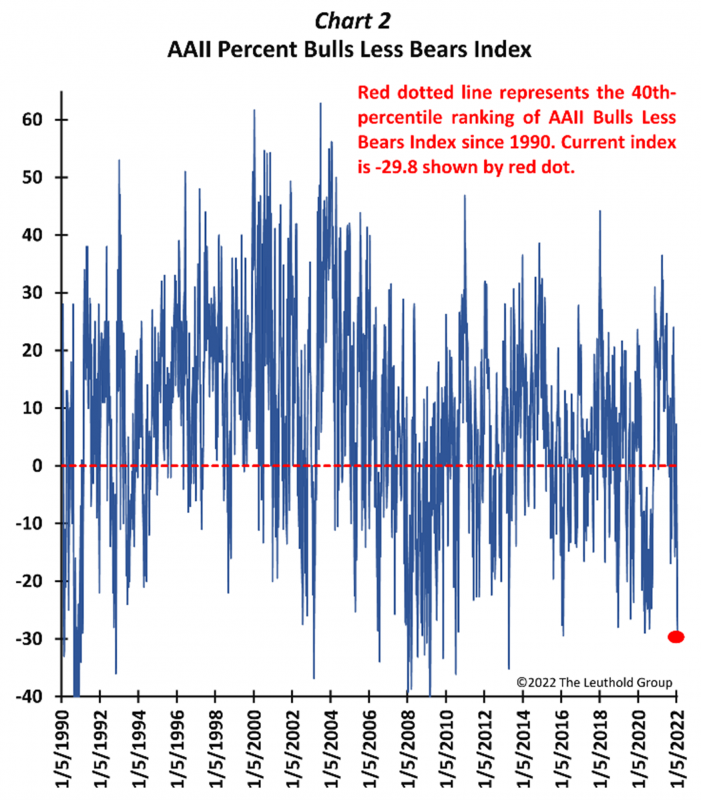

The so-called Bull/Bear index was around -30 at the end of January. Less than 98% of the time since 1990… Feels too negative.

Source: The Leuthold Group

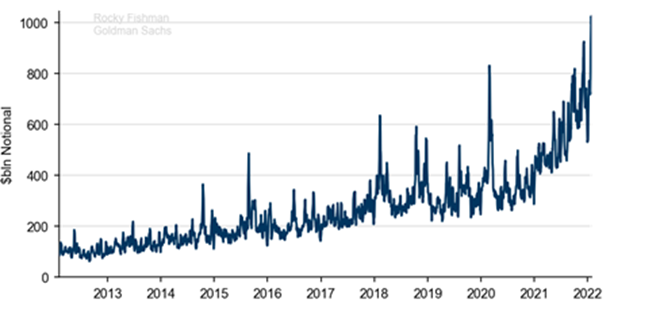

The next picture is a new favourite. Last week, private individuals and institutions bought put options as if the earth were going to collapse the next day. Last week, the average volume on the US stock exchanges, at face value, was USD 1,000 billion, per day! On Monday, January 24th, when the stock market, as we believe, reached its lowest level, turnover was USD 2.2 trillion in nominal value, with the majority being put options. Incredible. It feels like an excellent contraindication, even though we have no statistics on it.

Source: Goldman Sachs

One may wonder if there is any living life in Europe? In any case, liberalism is dying after the dependence on various subsidies and contributions to citizens has exploded in recent years. A good example is when S and V on the last day of the month round the pension group and distribute unfunded alms to the people. The first payment will be made in August one month before the election.

The similarity with the development in Japan is striking.

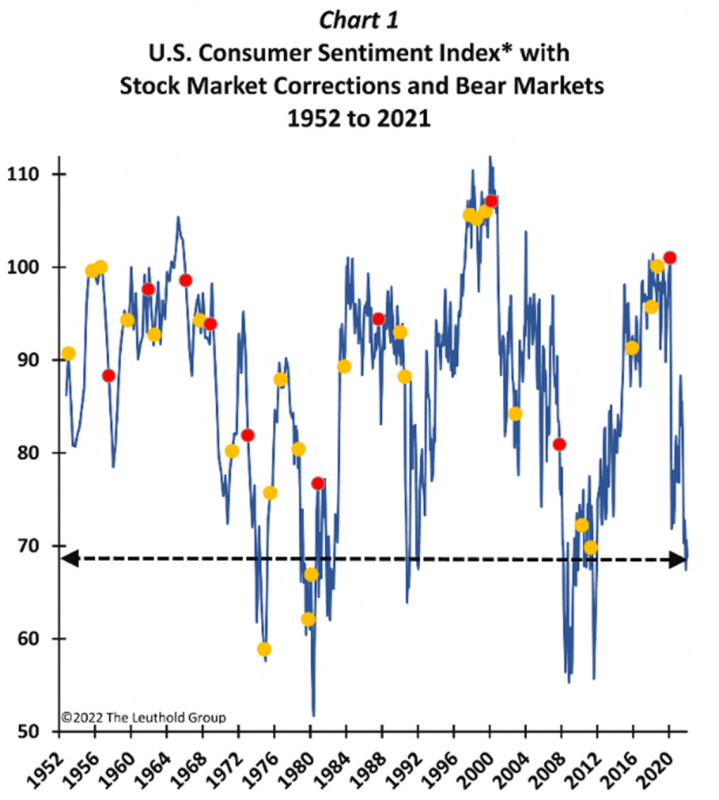

We continue with more pictures and history. The image below shows the Consumer Confidence among the American consumer for the past 70 years. Last week the level was 68.8 and that is a lower level than 90% of the times since 1952. Having such a low level after a record high economic activity and after a strong year in the stock market is very unusual (has probably never happened before).

Source: The Leuthold Group

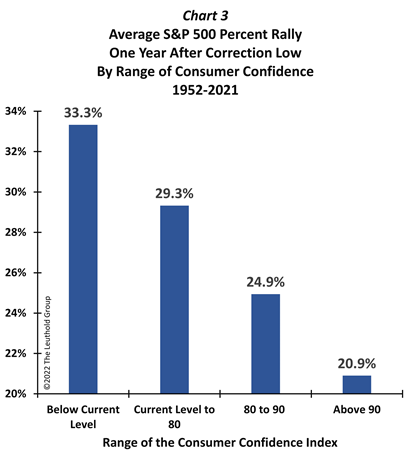

The correction in the stock market has not differed historically regardless of whether Consumer Confidence was low or high. However, the return period after a correction has differed significantly depending on the level it has been at. The historical return, when we have been around today's levels or lower, has been +33.3% the following 12 months compared to +20.9% when we were at high levels in Consumer Confidence. Nobody knows where we are in 12 months in terms of returns, but what we do know is that the apathy among average Americans is high. The last data point is that a "bear market" has never occurred before when Consumer Confidence is as low as today.

Source: The Leuthold Group

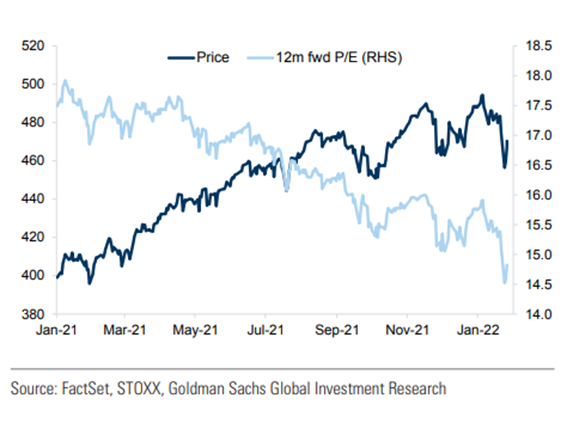

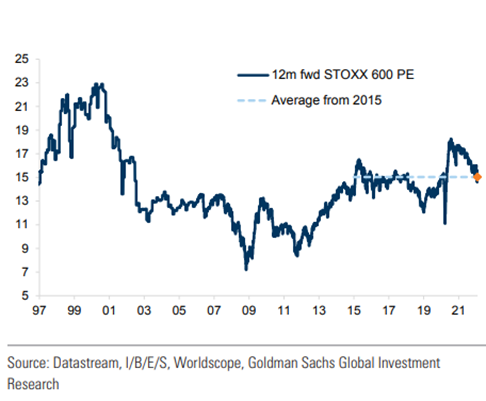

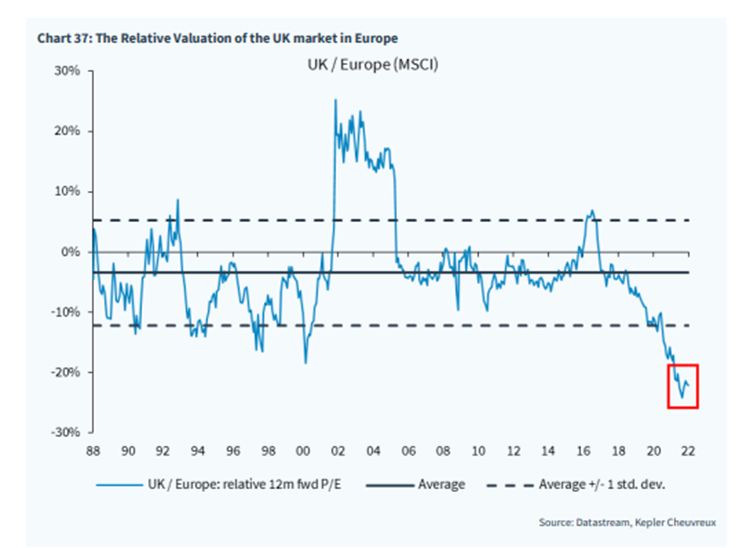

Below shows that share prices in Europe (Stoxx 600) have risen last year at the same time as valuations have fallen and are now at just under P/E 15x for the next 12 months.

This is in line with the historical average of the last 25 years.

A good picture that partly explains why we have allocated just over 25% of the fund's capital to the UK.

Small companies in the US and Europe have had headwinds since last summer. Our belief is that we are approaching a turning point, and this may coincide with when the US long-term interest rate reaches its peak in a few months (our view).

Given the extreme differences between the development of different sectors in January, how have different sectors developed in an interest rate hike cycle? The picture below shows the development of the last 30 years. Technology at the top and commodities and financial stocks at the bottom. This is one reason why there will probably be a reversal between the sectors in the coming months.

Source: Bloomberg, Strategas Securities, Nordea

To those of you who have not yet given up this extended reporting of this extraordinary month, now comes the summary. In a world of endless data and fast information transfer, it is important to find a point far away on the horizon and steer towards it. We divide our point into several sub-points below.

- We believe the lowest level in the market was set on Monday 24th of January. It will certainly be tested several times, but our best guess is that the level holds.

- Volatility will be persistent and at times high, primarily because no one really knows, not even themselves, how the Fed will act during the year.

- The US long-term interest rate is likely to reach its highest level before the summer of around two percent. Then the US dollar also peaks.

- Economic growth is gradually declining, and this is also dampening inflation and to some extent also the need for further interest rate increases.

- All other things being equal, it means that cyclical companies end up in the shadows in favour of fast-growing technology companies. An at least partial reversal of what January offered.

- Europe does not have growth companies such as in the USA, but it is the small cap companies that have taken that position, not least in Sweden. The capital will probably return to that asset class within a few months.

- Invest in companies that can pass on cost increases to customers so that cost inflation does not break earnings.

- Quality companies are more important than usual. Speculative companies have had their two years in the spotlight when liquidity in the systems was at its highest.

- Earnings growth wins by a certain margin over multiple compression. We believe that this year, too, will end with a positive return, albeit significantly lower than in 2021.

- And finally, the most important, really good stock-picking is the most important for a strong return.

The above theses and forecasts will be re-evaluated many times before the end of the year. It is extra important to be psychologically sensitive and flexible and be prepared for the unprepared and act when the terrain changes. As we did, for example, with the portfolio at the beginning of the year. The US stock market has just closed on January 31st as I write this and in two days the Nasdaq has risen by as much as 6%. Those who felt comfortable a few days ago with cash in hand are now stressed about too low exposure. It's like an unusually well-directed drama.

We extend an unusually large thank you to our investors for their trust and we continue the marathon.

Mikael & Team

Malmö February 3rd, 2022