Note that the information below describes the share class (I SEK), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class' return. The information below regarding returns therefore differs from the returns in other share classes.

Before making any final investment decisions, please read the prospectus, its Annual Report, and the KIID of the relevant Sub-Fund here

This material is marketing communication

Monthly Newsletter Coeli Absolute European Equity – October 2022

OCTOBER PERFORMANCE

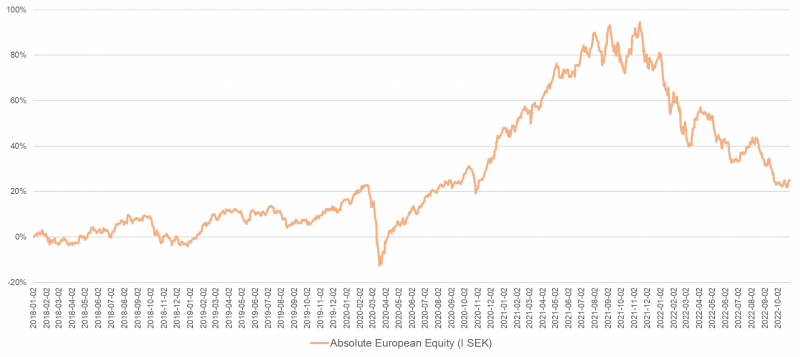

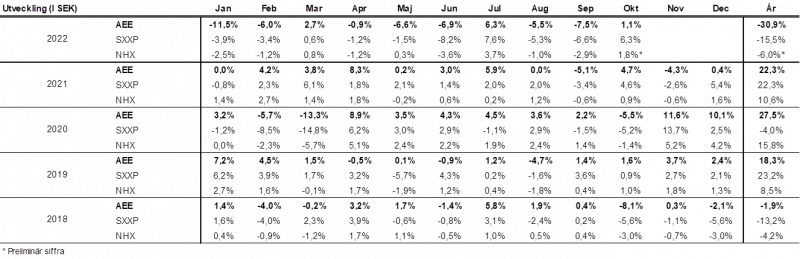

The fund’s value increased by 1.1% in September (share class I SEK). The Stoxx600 (broad European index) increased during the same period by 6.3% and HedgeNordic’s NHX Equities increased provisionally by 1.8%. The corresponding figures for 2022 are a decrease of 30.9% for the fund, -15.5% for the Stoxx600 and -6.0% for NHX Equities.

EQUITY MARKETS / MACRO ENVIRONMENT

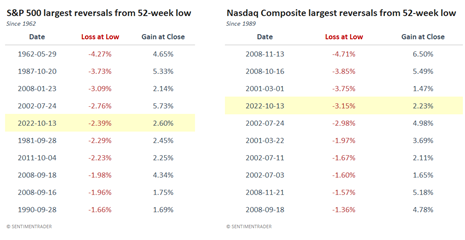

Another eventful month has passed, this one also with continued high volatility. Unlike most other months this year there was a positive undertone in the market. After a strong start to the month, risk appetite fell as nervousness increased ahead of October 13th when the year's most important macro data was due to be presented. In the hours before the announcement, there was complete silence. Someone said it felt like being in the dressing room before the most important game of the year. The S&P 500 had six negative days behind it and was at a new 52-week low. Since US futures began trading in 1982, there is only one time period that can match such a sharp decline and that was around October 8th, 2008…

At 2:30 p.m., inflation figures trickled in, which showed an increase of 0.4% month-on-month against the expected 0.2%. This led to significant but short-lived turbulence and later in the evening we experienced the fifth largest swing in the S&P 500 history (5%). The fourth largest in Nasdaq's history (5.4%). Crazy of course, but the string was taught and had been for a long time.

Source: SentimentTrader

We increased risk after that mainly by closing various short positions. We kept our long positions largely unchanged. Below is the development for the S&P 500 between October 6th and October 13th. It is impossible to be bored in this line of work!

Source: Bloomberg

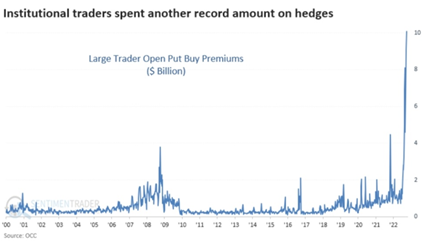

One way to try to explain the turnaround in the market despite worse data is the astonishing picture below. Put option buying volumes have literally exploded in recent months, which implicitly means that everyone was waiting (and is waiting?) for the big crash. So far it was an excellent contraindication signaling a rebound in the market.

Source: OCC

The calamity in Britain continued at a high and improbable pace. The Monty Python gang feels like amateurs compared to the bigwigs of the British Parliament. If it hadn't been so serious, it would have been very entertaining. In two months, the former British Empire has had a queen, a king and three prime ministers.

- I am a fighter, not a quitter. That's what Liz Truss said when she was booed in the British Parliament after dismissing her Chancellor of the Exchequer and humiliatingly presenting a replacement who in turn scrapped basically all the proposals previously presented. Two days later she too was out of the picture and the author of her autobiography, which was scheduled to be released just in time for Christmas, is likely to have had some sort of nervous breakdown.

We wish the new Prime Minister Rishi Sunak all the best! Britain is needed in Europe, despite their serious self-harming behaviour and in some contexts distorted self-image (there are several European countries that have that).

Source: Twitter

At home in Sweden we got a new prime minister, Ulf Kristersson. We wish our new government the best of luck. They will be busy. From a stock market perspective, it was, as usual, a total non-event.

When the British turmoil began just over a month ago, bond yields rose sharply all over the world. Among other things, it put further pressure on the Swedish real estate sector, which generally and from a European perspective, took more risk both operationally and financially. It has in many cases been topped by a strange culture of high cross ownership. As the owner of a real estate company today, it has recently become important to have a principal owner who has no debt. The world's largest real estate deal ever, Akelius' sale to Heimstaden at the end of 2021, seems unusually well-timed from Akelius’ perspective. His entrance back into the market did not take long and on October 6th it announced that he had bought 12% of Castellum through the acquisition of a large part of M2's shares (at a discount).

Our fund owns, since spring, the logistics property company SLP and has recently also built up a position in Wihlborgs. Common denominators for these companies are commercial and inflation-adjusted leases, no or very low bond financing, and strong balance sheet. Both also happen to be Malmö companies! We see significant value potential in these two holdings with a controlled risk. When everyone runs in the same direction and sells their real estate shares, it offers great opportunities to buy in at low valuations. Our view on inflation and interest rates, which we have discussed all year in this forum, means that we would not be surprised if many investors want to re-enter the sector sometime next year when central banks are nervously sitting on the rate cut card to get the economy going again. We take the liberty of quoting Sven-Olof Johansson and his Fastpartners interest rate view which was communicated in their latest quarterly report and which we fully subscribe to.

"Our assessment is that in November the Riksbank will raise the repo rate by 75 points from the current 1.75% to 2.5%, on the back of current inflation data. With cost increases for households and large interest rate increases mean that the consumption space for the individual will be very limited. This means that demand in the economy will fall dramatically, with a sharp deterioration in the economic cycle as a result, and this already in the first quarter of 2023. We can already see a slowdown in the European economic cycle with falling commodity prices and above all lower prices on the energy side, which has been driven forward by large elements of speculation. Taken together, these factors will mean a rapidly falling inflation rate, which will clearly show in the statistics as early as the second quarter of 2023. This will enable the Riksbank to begin interest rate cuts to avoid too deep a recession. Our scenario is that we see a key interest rate at the end of the second quarter that is lowered by 75 points to 1.75%, then during the third quarter it is lowered by a further 50 points and then reaches a level of 1.25%, which corresponds to the ECB's current level. A further adjustment of 25 points may be made during the fourth quarter to reach a long-term balance level of 1%. This is because in the 21st century we created a world that is not designed for high interest rates. With this interest rate scenario, Fastpartner sees a sustainable profit level of around 1 billion based on the current situation with the current property portfolio as a base and which assumes an indexation of our rental income by 10% from the year ahead".

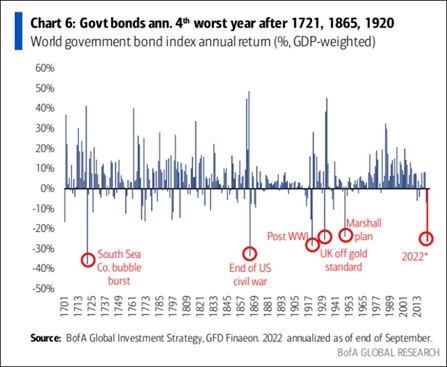

There are always those who have it worse. If you think that the stock market has been unusually weak this year, it is even more dramatic in the bond market. 2022 has so far been the fourth worst year in 322 years. Only the years 1721, 1865 and 1920 have been weaker (if that's any consolation).

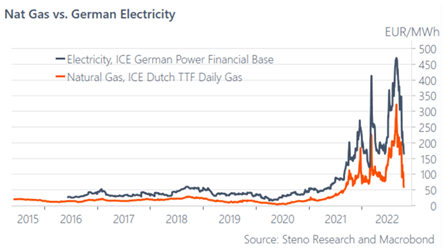

Gas prices in Europe have collapsed from the extreme levels of a month or so ago. It is of course very gratifying in many ways and the stock levels have been replenished at a better rate than expected. It is also good for the rate of inflation. But criticism must also be directed at how the purchases of gas took place during the late summer. It does not appear well thought-out, and volumes were bought at any price. Most of us have to pay the cost of that in the form of very high electricity bills and in addition subsidies in most European countries so that we can afford to pay the bills. Likely there was some speculation into this as well. With the proposal that has now been announced for support in electricity areas 3 and 4, for example, the undersigned will get SEK 40,000 back sometime this winter. That, in combination with the fact that it looks like the price of electricity will be lower this winter than previously predicted, probably gives marginal support to the private consumption.

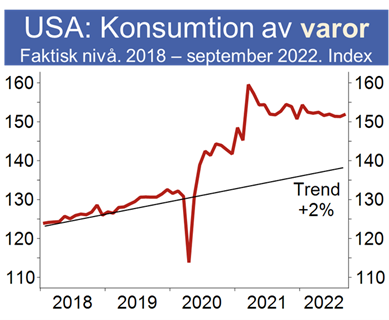

Private consumption in Europe, including Sweden, has so far surprised on the upside. People have consumed more goods than electricity, although it's hard to believe when you listen to the media. Below US consumption.

Source: SEB

A big event for Europe is that the world's largest chemical company, Germany's BASF, announced last week that it is scaling back its operations in Europe due to 1) high energy prices 2) an (excessively) high level of regulation 3) ever-increasing volatility in the chemical market. The evidence that Europe's industrial competitiveness is declining is abundantly clear as BASF instead chooses to increase its investments in the USA and Asia. We have said it many times, our politicians leave a lot to be desired and they are busy transferring subsidies to their residents instead of coming up with structural reforms. The European economy accounts for approximately 25% of the world economy. In 1973, it was just over 42%.

Illustrated in another way: Below shows 22 years of development of the broad European index Stoxx600. In 22 years, the index has risen by 6.8%... Admittedly excluding dividends, but still. The corresponding figure for the S&P500 measured in the same currency is 139%. In Sweden, we only need to study the crown jewel Ericsson. Zero shareholder value for the last 20 years and right now busy defending themselves against IS pay-outs and supplies to Russia despite claims to the contrary (not investable from an ESG perspective?). Thankfully, there are also many fine companies in Europe with valuations that are significantly lower than in the US.

Source: Bloomberg

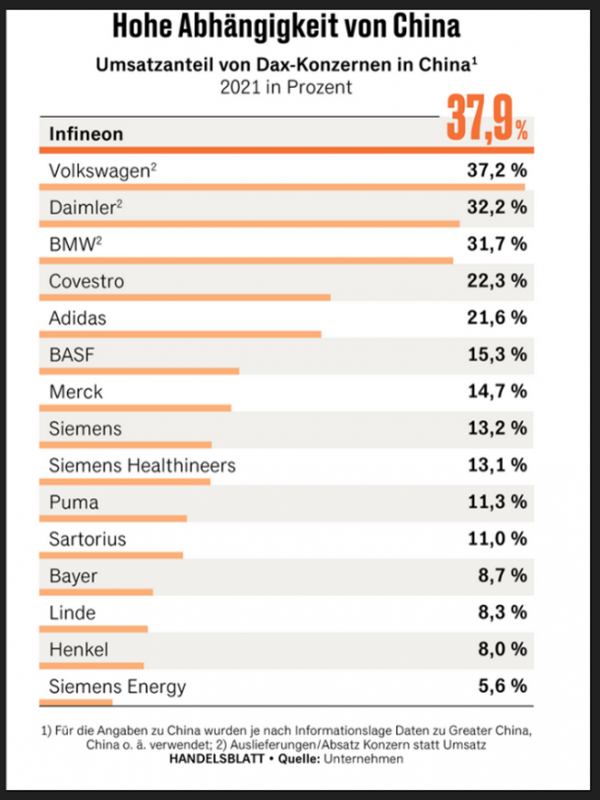

Europe's engine, Germany which invested wholeheartedly in energy supplies from Russia, is also suffering from China's slow burn. Below is China's share of the turnover of a number of large German companies. The German companies were huge winners in the first 10 years of the 21st century, but now face greater challenges.

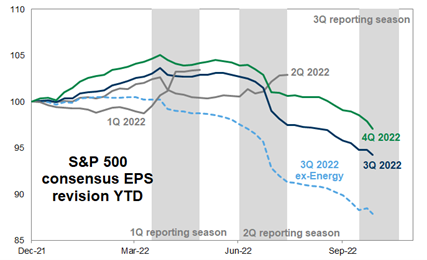

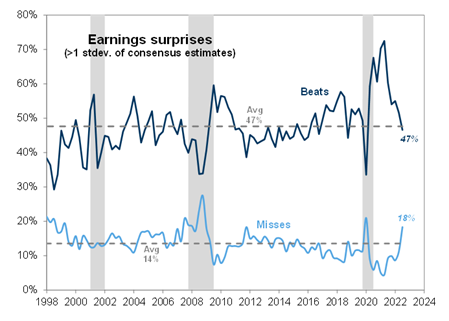

We wrote last month that we expected significant downward revisions to analysts' earnings estimates. It has now started to trickle in, but more is to be expected. That said, there are always downgrades at the end of the year, as analysts as a collective are always too optimistic.

Source: Goldman Sachs

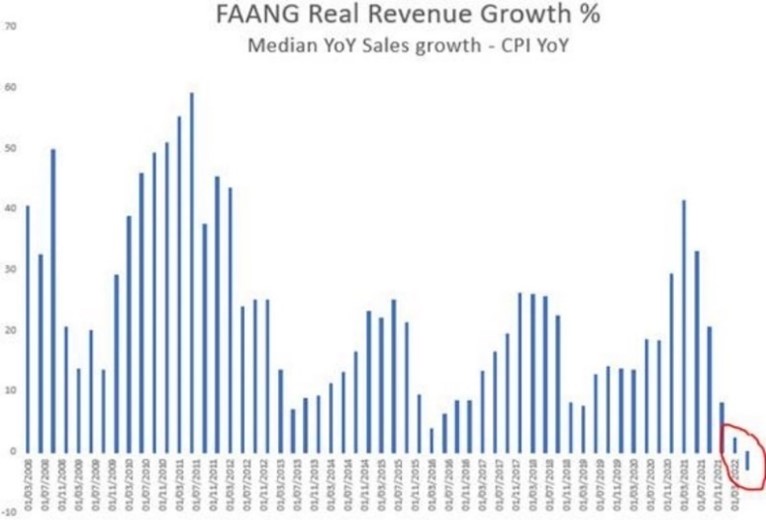

So far, the companies have generally delivered good reports. It is probably not the development that the central banks wanted, as much of the turnover growth comes from price increases. What has undoubtedly been extraordinary this reporting season is the sharp declines in the share prices of the major US technology companies. In the last week of October, the FAANG companies reported, and the outcome was, from a financial perspective, close to catastrophic. The companies' share price movements on the report day were for Microsoft -9%, Google -9%, META (Facebook) -24% and Amazon -13%. Here the FED was probably a little more satisfied. Apple was the only technology giant to see its share price rise by +8%. If you had had the above information last Sunday, you most likely would not have guessed that the market would rise despite that. For example, the S&P500 rose 4% in the last week. Absolutely incredible.

Source: Goldman Sachs

META's share price has now fallen by roughly 70% this year, which corresponds to close to USD 700 billion, which is approximately 10% more than Sweden's entire GDP. The share trades at just under 10x 2023e in P/E, which should be compared with about 100x a few years ago. A pretty significant multiple contraction (to put it mildly). One who wasn't entirely happy with having recommended buying in the META was CNBC's Mad Money's Jim Cramer.

To add fuel to the fire, a month ago Tuttle Capital Management launched an ETF that buys and sells exactly the opposite of what Jim Cramer recommends - the Inverse Cramer ETF. It must have had a good day last week.

The chart below shows the turnover growth of the FAANG companies over the past 15 years. Something has just happened.

Source: Goldman Sachs

Former Fed chief Ben Bernanke received the economics prize in memory of Alfred Nobel. He invented QE, ("quantitative easing"), or fiscal policy easing, and has researched the time around the 1929-1932 depression where the central bank was too restrictive, which in turn led to the Great Depression. He was also called Helicopter-Ben for all the money he distributed to the public. We are attaching what we think is a very entertaining video that CBS made many years ago. Tune in!

As expected, the European Central Bank ECB raised interest rates by 0.75 percentage points at the end of the month. Christine Lagarde was also clear that this third increase will not be the last. In September, inflation in the euro area was 9.9%. This is the same institution that subsidized bond purchases until June this year to stimulate the economy…

Someone with a good sense of humor posted this video on Twitter to visualize the central banks and the economy in 2022.

It has been a challenging year for many. "Buy the dip" is for sale.

Source: Twitter

Long positions

Bonesupport

Bonesupport is one of our newer core holdings. We used the slow pace of the summer to build up a position in the company. In October, Bonesupport delivered a third quarter report that beat estimates by ~10% and showed revenue growing 54% (39% adjusted for currency), compared to last year. Pleased to say that business is growing nicely in North America, where sales grew by as much as 72% (49% adjusted for currency). We hope and believe that the market will soon realize that the US has the potential to be bigger than what lies in expectations. Especially as the new product, Cerament G, was launched in the second half of October and is not included in the figures for the third quarter. To put the size of the North American market in perspective Bonesupport's customer, Cleveland Clinic, has a budget as large as the entire healthcare budget of Sweden.

Adjusted for a one-off cost, the operating profit amounted to -4.4 million SEK. In other words, it is not many quarters before the company is cash flow positive. We guess the market took note of the exceptional performance in North America and sent the stock up 9.3% on the day of the report, which was followed by further gains the day after.

SLP

Swedish Logistic Property also reported during October. Operationally there is no drama and thins are running as expected. The market also took the report calmly and the stock was unchanged for the day. Unfortunately, the share fell roughly 16% during October, which is largely (in our view) explained by a placement of 6 million shares that was made well below the last payment. Our strong feeling was that some of the buyers tried to make a few kronors, which put pressure on the stock. We are of the opinion that the seller was added as a shareholder in connection with a real estate acquisition that took place a year ago. We continue to like SLP, its management team and focus on logistics and "last-mile hubs". SLP is valued at a premium to the sector. Something we think is reasonable. The company is expected to grow faster than the sector and has a strong balance sheet that will be able to be used in turbulent times.

Wihlborgs

As usual, Wihlborgs released a stable report that came in somewhat better than expected. During the last 30 quarters (!), the company has delivered positive net rental, which can be considered an achievement. The stock is concentrated in southern Sweden, which means that Wihlborgs can move tenants around to optimize letting.

We like Wihlborgs for their strong balance sheet and commercial property portfolio. In principle, the leases are exclusively adjusted for inflation, which means that higher costs are passed on to the tenants. The balance sheet is strong and only 10% of the debt comes from the bond market, which itself has been extremely messy this year. With a loan-to-value ratio of 49%, where 40% of the interest portfolio is secured, Wihlborgs is one of the most defensive real estate companies on the Stockholm Stock Exchange. At an unchanged NAV, Wihlborgs could handle an increase in the yield requirement of ~40 basis points before the price takes a hit. Next year, the company will trade at a cash P/E of around 12-13x, which we believe is attractive.

Common to both SLP and Wihlborgs are strong balance sheets with low LTV where basically all debt is bank financed. Having strong bank contacts in a year like this is worth its weight in gold.

Biovica

We have been the owner of the small cancer diagnostics company for 3.5 years and in July the company announced that it had finally received approval from the FDA for DiviTum, which aids in monitoring disease progression in patients with breast cancer. The stock rose sharply at the beginning of August and closed after the first day around SEK 40. It came as no surprise that it needs to fund its offensive plan for the US market. In October, it was announced that it was making a rights issue of SEK 148 million. The issue is fully guaranteed. In recent months, in a negative market, the share has been heavily beaten and is now trading around SEK 9, which is slightly above the subscription price. We reduced our position over the summer, but with such a sharp decline in recent weeks, the stock was the fund's worst contributor in October. Current position size is now under one percent. If the company continues to deliver, current levels should reasonably indicate an attractive risk/reward.

Vinci

France's Vinci, a company whose value mainly consists of toll roads in France, delivered as usual a strong quarterly report with no signs of slowing down. Organic growth of 12% contributed to the share rising by 12% in October and gave a profit contribution of approximately 0.5% to the fund's value development.

ISS

The fund's strongest contributor in October was the Danish ISS. We have not noted any significant fundamental news, apart from the company signing a couple of major contracts in the UK. The French sector colleague Sodexo has also reported good results for Q3, which certainly spilled over to the ISS share. Finally, two equity analysts have raised their sell recommendations to neutral, and we have noted that the number of shares shorted has decreased.

At the time of writing (Thursday, November 3), ISS has just reported results for Q3, and organic growth landed at 8.1% against the expected 5.6%. At the same time, the growth and profitability targets for the full year were raised.

Bic

For a period, we have built a position in French Bic. The company came about after its founders were among the first to commercialize ballpoint pens, but today is perhaps best known for their lighters. Bic has large market shares in many geographies but has had a tough time growing in a market that has some structural headwinds. However, there is a turnaround strategy in place that we believe in, and which seems to have delivered some underlying improvements. Before the third quarter report, the stock had risen 38% in 2022, which combined with tepid report numbers caused the stock to fall a total of 10% in October. At the time of writing, the stock has recovered somewhat.

Sedana

Another of October's mourners is named Sedana Medical, which fell 18%. In the Q3 report, the company's sales landed a few million below the preliminary tips. (Sedana has faced tough comparison figures in 2022 as the company's product sold like hotcakes during the pandemic.) But particularly serious, we guess the market thinks, was the fact that the launch in the UK is postponed to 2023. In addition to this, the risk of the launch being postponed in a couple of other geographies increased slightly, although not definitively. Most of these problems appear to have been caused by factors outside of Sedana's hands, and we think the reaction to the report was clearly exaggerated. The stock is valued low, around 5x and 3x on EV/Sales for 2023-2024e. A large part of the investment thesis is the North American market, which is expected to be up and running in 2025.

Short positions

The short portfolio overall contributed with a negative result during the month. The biggest negative contribution was our short positions in a Swedish small company index and put options on the German DAX. Several stock-specific short positions contributed positively, among them were Swedish Addtech, SCA and Holmen.

Exposure

The net exposure, adjusted for our unlisted holdings, at the beginning and end of the month was 53% and 76% respectively.

Summary

More than half of the world's listed companies have now reported for the third quarter and so far, they have passed. The simple conclusion is that price increases have accelerated turnover growth at the same time as record high margins have started to decline. In addition, most people are cautious with their forecasts.

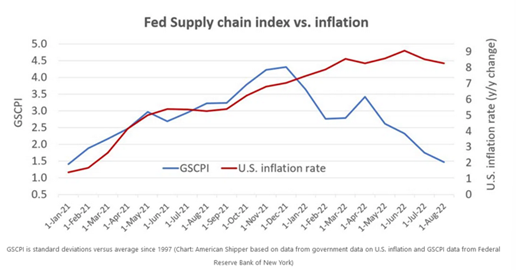

We note that the companies' various bottleneck problems have gradually improved, which is good both for profitability and the underlying inflationary pressure.

Source: Goldman Sachs

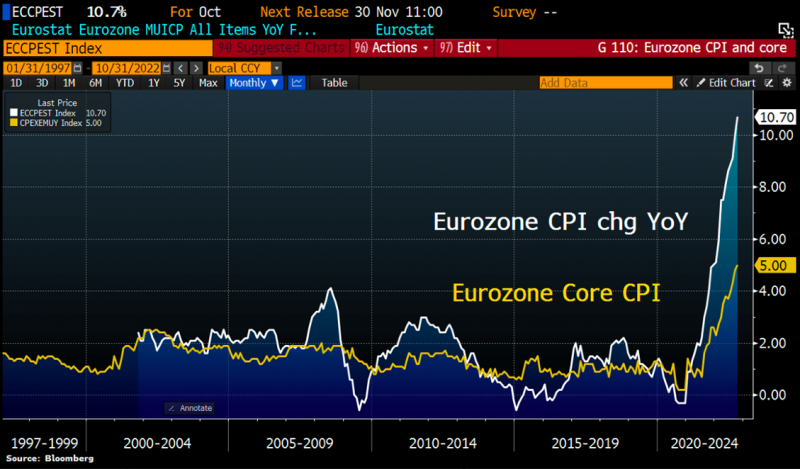

On the last day of the month, we saw a new high for European inflation, +10.7% compared to the same month last year.

Source: Bloomberg, Holger Zschaepitz

Most of the world's central banks continue with sharp interest rate increases and the risk of a recession increases, mainly in Europe, but also in the USA. While investors are mentally 6-9 months ahead of today's reality, central banks steer by looking in the rear-view mirror when analysing data that has a lag of a few months. It's a bit like watching a head-on collision in slow motion. ECB chief Christine Lagarde was interviewed this weekend where she said: "the inflation has, ahhm, just pretty much come from nowhere". You don't know whether to laugh or cry. The central banks started raising interest rates far too late and it seems obvious that they will be on the wrong side in the other direction too. The ratio between competence and power is not in perfect balance, to put it diplomatically.

One of the reasons the stock market had a strong month was that both the Bank of Canada and Australia surprised by raising interest rates less than expected. In addition, some of the Fed's members commented that they might start thinking about slowing down a bit and studying the incoming data. To be continued.

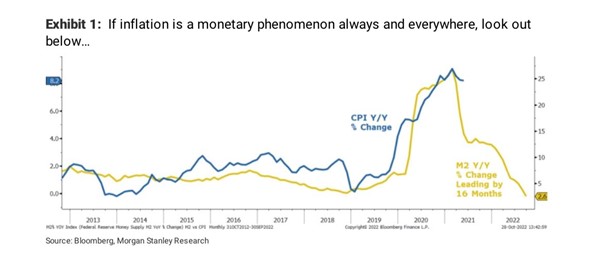

The American money supply falls at a rapid rate, which, other things being equal, reduces inflationary pressure. That the opposite applies is apparently something that Christine Lagarde ("Madame Inflation") does not know, considering this weekend's statement.

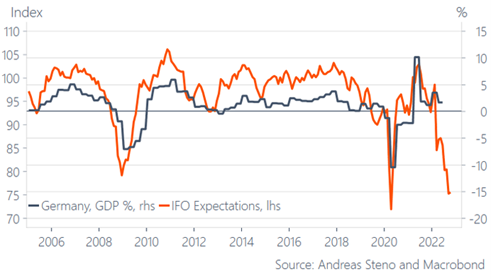

Below, German GDP combined with IFO, which is a German business climate index and a reliable economic barometer. The picture shows a clear and sharp drop in German GDP shortly.

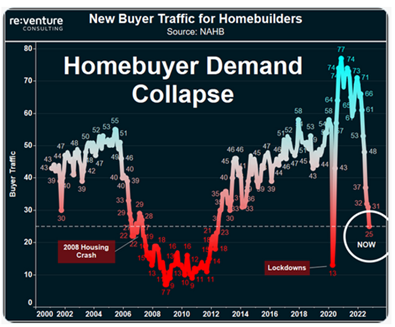

In the US, the demand for housing is falling dramatically. It should soon show in a weakened economy and probably also rising unemployment (which is what the FED wants).

Source: NAHB

High inflation also reduces debt. Despite nominal interest rates rising to two percent, inflation has also risen to around 10%. This gives a negative German real interest rate of a whopping -8%! German real interest rates have now been negative for 78 months. Unbelievable!

Source: Bloomberg, Holger Zschaepitz

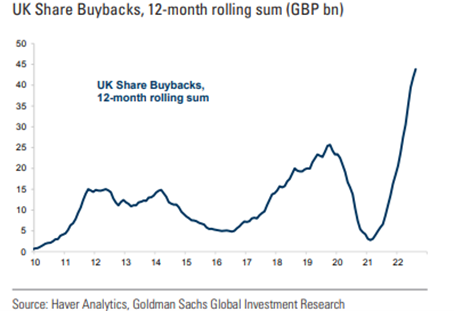

Share buybacks have just started up again after many companies have reported results for the third quarter. The year looks set to end at a new record high.

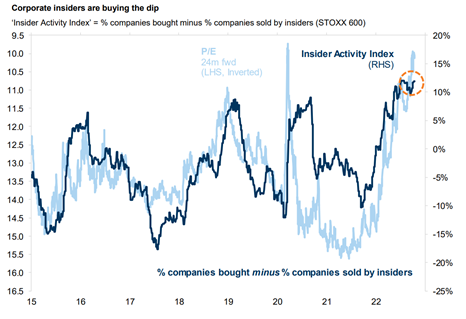

Insiders of European companies have during the year bought significantly more shares in their own company than were sold.

Source: Goldman Sachs

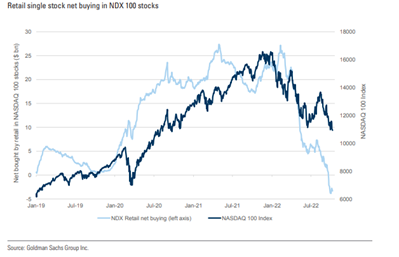

This contrasts with American private investors who sold a lot of their Nasdaq holdings.

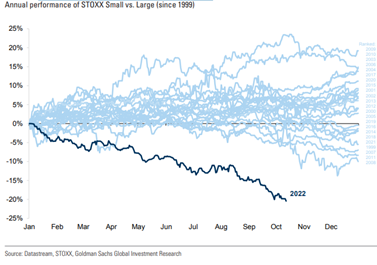

The following illustrates a fundamental problem for the fund in 2022. The price performance of small companies compared to larger companies is having its worst year since Goldman Sachs began measuring performance in 1999. We would be very surprised if this does not reverse to some extent next year.

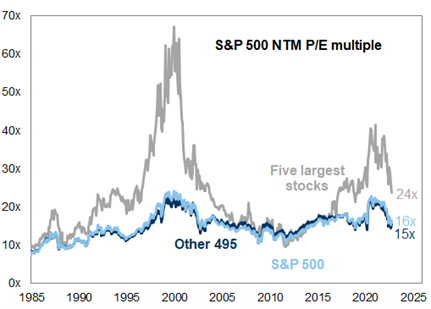

A short update on valuations in different regions illustrated in a few different pictures. The major technology companies have had a significant multiple contraction. META for example is now only 25th in the S&P500 measured in terms of market capitalization. The five largest companies' share of the entire index was at its highest around 25% and now around 16%.

Source: Goldman Sachs

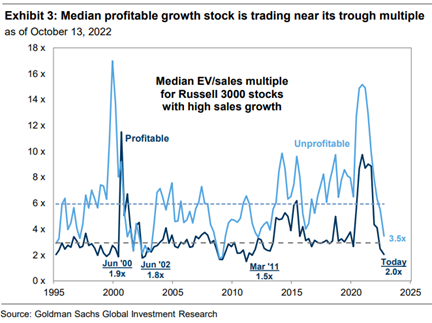

Half full or half empty? Based on history, valuations for smaller growth companies have now reached historic lows.

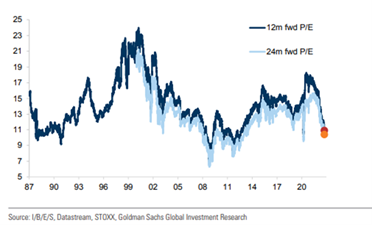

The European valuations are down to, by our standards, very attractive levels. As usual, it is unclear how much the profit estimate will decrease.

We save the best valuation picture for last. The European market has never (!) been quoted lower in relation to the American one. We are convinced that increasing allocation to undervalued well-managed European companies will pay off well. A special thanks to Joakim Tabet, strategist at Kepler Cheuvreux, who produced the image for us.

Source: Kepler Cheuvreux

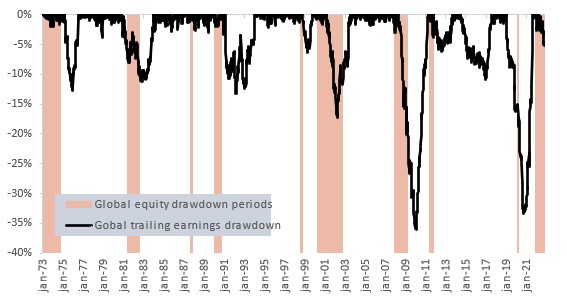

The image below shows 50 years development of how long each decline phase in the stock market took and how much the profits decreased in percentage terms. So far this year, profit estimates have fallen by around five percent, and we will likely see more of the same as time goes on. Historically, the stock market has bottomed when 75% of the downward adjustments have been made

Source: Berenberg

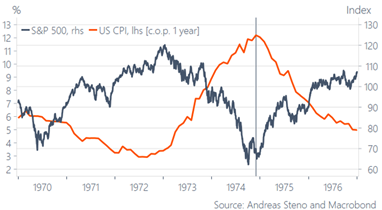

Below is an interesting picture from the early 1970s when the world was also struggling with high inflation. The peak inflation at the end of 1974 coincided with the market bottoming out and starting to rise. We are likely to see a similar pattern this time and likely to pass the high soon (our view).

October was the first month this year that gave a little extra time for analysis and company visits. It was true that there was continued high volatility, above all on individual shares, but it was still easier to understand various market movements. Capital was moved around in the market. The most obvious was from big tech to other companies, but the capital did not leave the market and in the U.S., there were relatively large inflows into equity funds. The fact that the market rose despite the world's most important shares crashing (FAANG) must be seen as a real sign of strength. The breadth of the market rose which is a sign of health.

The trend in interest rates continues to control the direction of the stock market daily, but over time the influence has diminished. At mid-year, the S&P500 was at 3,759 and the interest rate was the US 10-year interest rate at 3.07%. A month ago, the level was 3757 and the interest rate was 3.69%. On Friday, October 28th, the level was 3901 and the interest rate 4.01%.

For the first time in two years, the S&P500 delivered a strong return two weeks in a row. In October, the Dow Jones had its strongest development since the 1970s.

Source: Bloomberg

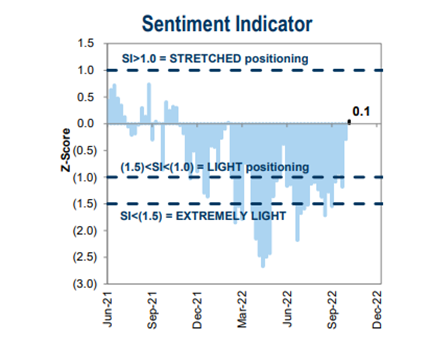

The Goldman Sachs sentiment indicator touched +0.1 last October. It was the first positive reading in 34 weeks (!) which is the longest negative period since they started collecting data in 2009.

Source: Goldman Sachs

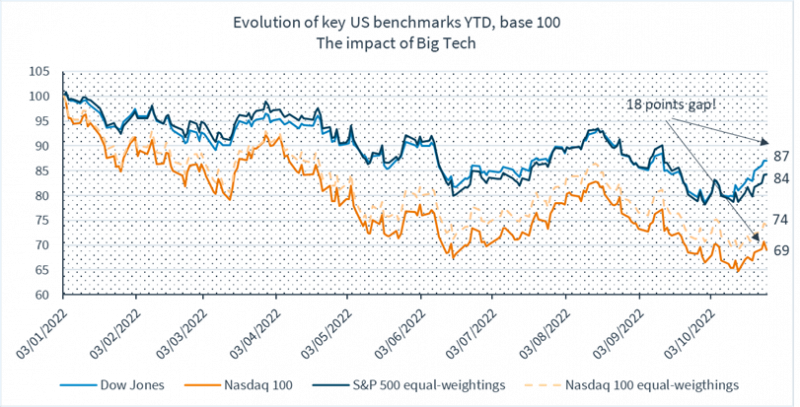

The equally weighted indices S&P500 and Nasdaq have had a significantly better development this year than the "official" counterparts, which have index weights based on market capitalization. Many smaller companies have had a significantly better development than the previous "champions". The breadth of the market is increasing.

Source: Kepler Cheuvreux

Nasdaq performance (white) in relation to the inverted US 10-year yield (orange). The odds of interest rates falling over the next year feel quite low (likely, that is).

Source: Kepler Cheuvreux, Bloomberg

It may seem simple with seasonal history, but the combination of the Nasdaq falling by 30% this year and the fact that the index in November has had a positive return for the past 10 years means that we probably think it will be the same this year. Some more statistics: Since 1950, the American stock market has always risen after the mid-term elections in the period from November to April. 18 out of 18 times.

Source: Bloomberg

We have written about our view of a "trading range" in the market for half a year and it has largely been correct. Most recently, the levels were properly tested on the downside before there was a strong rebound upwards. For the first time this year, we are starting to entertain the idea that we may be close to breaking out of previous levels.

Next week will set the tone for the end of the year. On November 2, the FED will come out with its new interest rate statement. Anything but an increase of another 75 points would be a sensation. On November 3rd, the Bank of England will issue its interest rate statement. The next day comes labour force statistics where we will hopefully see some slowdown (so the FED can slow down interest rate hikes). On the 8th of November, the mid-term election will take place and two days later new inflation data will be released. In addition, it continues to rain quarterly reports for another week or so.

Thank you for your interest and continued trust.

Mikael & Team

Malmö on 3th of November 2022