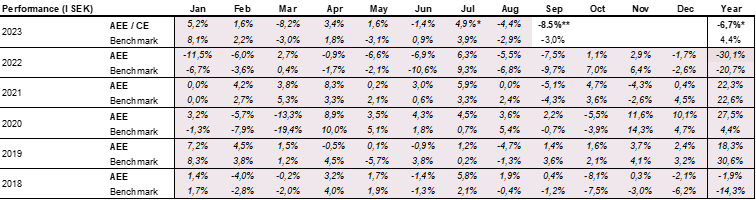

Note that the information below describes the share class (I SEK), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class' return. The information below regarding returns therefore differs from the returns in other share classes.

Before making any final investment decisions, please read the prospectus, its Annual Report, and the KID of the relevant Sub-Fund here

This material is marketing communication

Monthly Newsletter Coeli European – September 2023

SEPTEMBER PERFORMANCE

The fund’s value decreased by 8.5% in September (share class I SEK). The Benchmark decreased by 3% for the same month, measured in EUR.

*Adjusted for spin-off of Rejuveron.

** AEE: Absolute European Equity, CE: Coeli European, Benchmark: MSCI Europe SMID Cap Net Total Return EUR.

Please Note: On the 4th of September 2023, the strategy of the fund officially changed from a European long biased equity long/short fund to a European active long only fund. Simultaneously, the name changed from Coeli Absolute European Equity to Coeli European. The track record highlighted in colour in the table above is that of Coeli Absolute European Equity.

EQUITY MARKETS / MACRO ENVIRONMENT

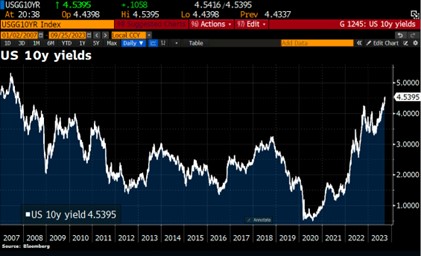

September is, so far, the weakest stock market month of the year, which is normal. The main reason why the stock markets came under pressure was the central banks' message of higher for longer, i.e. the previously communicated interest rate paths were adjusted and now project a slower return to a more neutral level. The US central bank kept its interest rate unchanged during the month. The difference compared to the last meeting in June was that they then predicted that the key interest rate would be lowered by one percentage point next year, which was now changed to a half percent reduction. The European central banks, including the Riksbank (Swedish Central Bank), delivered a similar message. This meant that, for example, the US 10-year interest rate reached its highest levels since 2007.

Source: Bloomberg

The historical development per month for the S&P500 since 1928. September has clearly been the weakest month and that was also true this year with a decline of 4.8%.

Source: Goldman Sachs

Further reference points, and all measured in local currency, were that the Nasdaq fell by 5.9%, the DAX by 3.8%, the MSCI European SmallCap by 3.0% while the FTSE in the UK was one of the few indices to end at plus with 2.3% in return. The driver behind that was the oil companies' success on the back of a rising oil price.

The fund had a weak month and fell by 8.5%. The principal reason for that was that the Swedish krona had a strong development against the euro and above all against the pound, where we have around 20% exposure. The weakening of the euro and the pound adversely affected the fund's return by approximately 2% points. The other contributing factor was that the CMA (Competition and Markets Authority) in the UK unexpectedly announced on the 7th of September that it would review the veterinary industry to ensure fair and good competition. This led to strong price reactions in, above all, our holding in CVS but also in Pets at Home. Our view is that the markets’ reaction was exaggerated and following the sharp decline, we have increased our holding in CVS. This news, in isolation, affected the fund's development by approximately -1.6% points. More about this and the fund's development in the portfolio companies section.

Although the Swedish Krona contributed with a negative return for the fund this month, it is gratifying that the Riksbank is finally starting to sell Euros and Dollars from the currency reserve and buy Swedish kronor. The fact that they are now doing it and, at least in the short term, have had a great success is reassuring. If it continues, which we believe and hope, foreign capital will gradually begin to return to, among other things, the Stockholm Stock Exchange. The Swedish krona has been a major short position for many global currency speculators, and one reason for the strengthening last week is likely that they have started to cover their positions.

Source: Bloomberg

Inflation is now falling on a broad front and even in Sweden it is starting to loosen up properly. On the last day of the month data published showed that the inflation rate in EMU fell to 4.3% in September from 5.2% in August. The expected change was 4.5%. The decline was broad and core inflation fell to 4.5% from 5.3% the month before. The expected change was 4.8%. The probability that the ECB has already made its last rate hike is relatively high. The important question that follows is how long it takes for them to lower the rate.

Source: X

We believe that the coming months will continue to bring positive news regarding inflation and by the end of the year, Sweden can be close to the goal of two percent. The fact that the Riksbank says interest rate will possibly not be lowered until the second half of 2025 is just as likely as when they said last spring that the interest rate would not be raised until the second half of 2024.

We don’t!

Quote:” I think it is worrying that people believe in our forecasts.” Erik Thedeen, Chairman of the Swedish Central Bank. Source: SVT

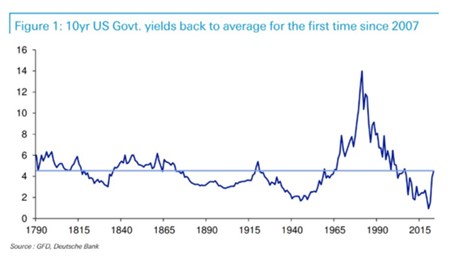

If you zoom out a bit, to get a 233-year perspective, we are now at a normal interest rates level.

Source: GDF, Deutche Bank

The oil price rose 23% during the quarter. Oil, arguably the world's most politicized asset class, has risen in price as Russia and Saudi Arabia have cut output. It is not demand that currently determines the price of oil, but supply. It is speculated that both Russia and Saudi Arabia would like to see Donald Trump become president again and rising oil prices are a good way to make life increasingly difficult for President Joe Biden.

Source: Bloomberg, Holger Zschaepitz

A rising interest rate indicates rising economic activity and there is a clear correlation between the interest rate and the price of oil.

Source: Bloomberg, Holger Zschaepitz

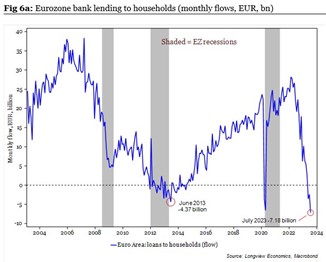

The effects of the sharply rising interest rates are beginning to show in the real economy. Europe is bordering on a mild recession, and it seems reasonable to believe that interest rate hikes are over. Below is the lending to European households. A certain slowing down can be noted, to put it mildly.

Source: Longview Economics, Macrobond

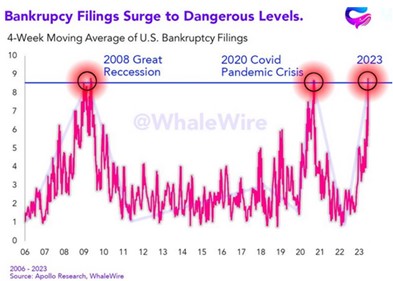

Even in the United States, which has shown extraordinary strength in the economy, some cracks in the facade are beginning to surface. Household living costs are now at higher levels than at the outbreak of the financial crisis in 2008 and bankruptcies are increasing, see image below.

Source: Apollo Research, WhaleWire

The 76-basis point increase in US long-term interest rates in March led to the collapse of Silicon Valley Bank. Six months later, the interest rate has now risen by a further 60 basis points. Will anything else break in the coming months?

Source: Bloomberg, Goldman Sachs

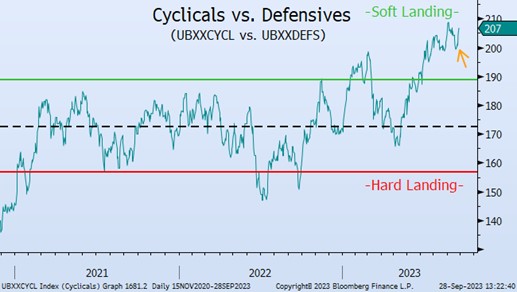

The stock market is of course concerned about interest rates, but sector developments clearly show that investors believe in a soft landing in the economy. The relationship between yield in cyclical vs. defensive companies is the highest in several years.

Source: Bloomberg, UBS

However, consumer stocks have recently come under heavy pressure. That includes luxury stocks such as our holding in LVMH whose share price fell by 8.4% in September (after -7.7% in August). For the year, the rise is now a modest 5.4%. Our view from here is that we are near a bottom in the share price for LVMH, as the image below could indicate. The stock has fallen a lot in a short time and a P/E ratio of 20x for 2024e is low for one of the world's best companies.

Source: Bloomberg, UBS

The decline in the LVMH price has meant that Bernard Arnault lost the lead to Elon Musk in Bloomberg's "Billionaires Index".

Source: Bloomberg

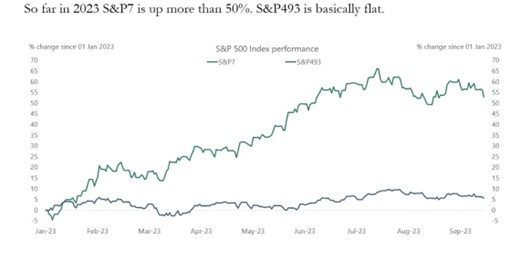

This year's rise in the American stock markets has, as is well known, been extremely concentrated to “the magnificent 7”, which has risen by an average of around 50%. A consequence of that is that if you buy into the S&P500, you get 34% exposure to these companies that trade at a valuation around P/E 50x. "S&P493" is trading around unchanged levels on the year.

Source: Bloomberg, Apollo Cheif Economist

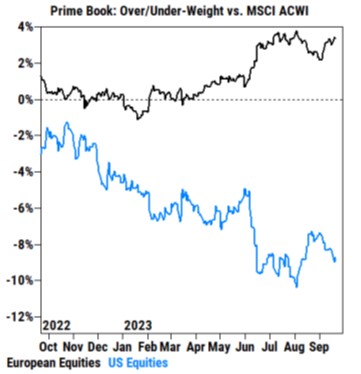

This is likely a contributing factor to the development of recent months, where the allocation to the American stock markets has decreased in favor of the European ones. The valuation difference has never been greater and for us as European investors it is of course positive with inflows.

Source: Golman Sahs

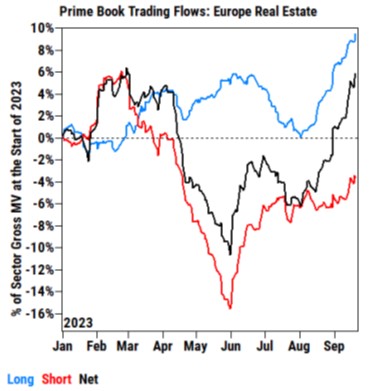

Another development that favors us is that, since a month ago, hedge funds are now net long European real estate shares. It is a sharp change since last summer (see black curve) and we think it will continue now that most people believe we are at or near the interest rate peak.

In Sweden, the listed real estate sector is disproportionately large and the vast majority of investors are underweight the sector. We ourselves have noticed a rising interest in the sector in the last month. Through its holdings in SLP and Corem, the fund has approximately 10% exposure to the sector.

Source: Golman Sachs

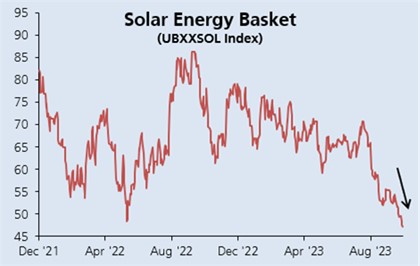

The year's worst sector so far, see image below. The hype in renewable energy, especially in 2021, led to large misallocations. The sector is dependent on large investments that require cheap financing, something that does not exist today.

Source: UBS

Something to keep an eye on. The difference between the Italian and German 10-year interest rates.

Source: Bloomberg

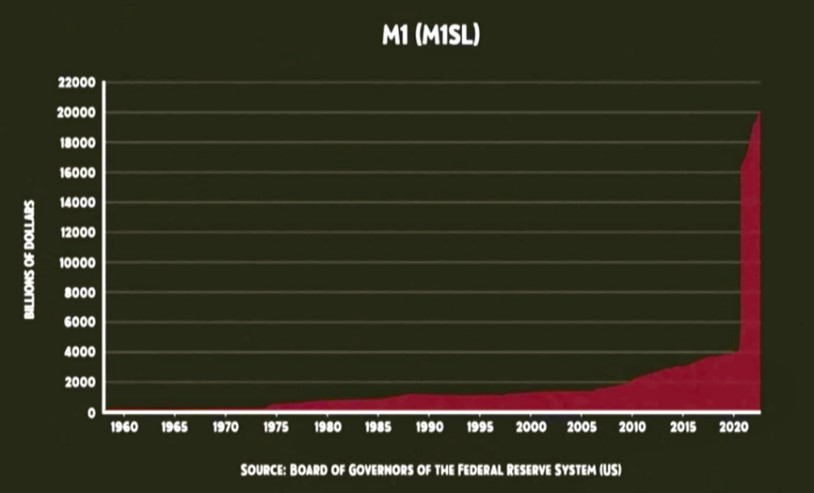

Roughly 80% of all US dollars in existence have been created between 2020-2023. Unfathomable.

Source: Win Smart, CFA

SEK 72,000 a month is the expected minimum wage for American workers. It feels high…

Source: Bloomberg News

Elon Musk has apparently refused Ukraine several times to use his satellite network Starlink, now jokingly renamed Tsarlink.

Source: X

On the last day of the month, the Center party meeting turns positive to nuclear power, after in recent years it has been involved in the dismantling of six fully functioning reactors with enormous social consequences as a result. Impressive…

Source: StegetEfter

Portfolio Companies

Wincanton

During the month, we received a positive message from Wincanton, our British logistics company. The company has long been burdened with a capital-intensive pension debt that in recent years has swallowed around £20 million in annual cash flows, which can be put in relation to the market capitalization of £340 million. During the month, Wincanton's pension trustee decided that the company no longer needs to pay more money into the pension plan, whose assets are now deemed to be large enough to meet the company's obligations. This was of course well received by the market, and the share price rose 13% in September. If we were to calculate the present value of 10 years of pension outflows at a discount rate of 10%, we conclude that this news in isolation is worth around £130 million, which corresponds to almost 40% of the company's value.

The pension issue has been something of a hurdle for the stock. The capital that is now freed up can be used for a combination of share buybacks (which we have argued for) and organic growth investments, for example in warehouse automation. On our estimates, Wincanton trades at a low P/E of 8x for 2024e.

CVS Group

As previously mentioned, in September came an unexpected announcement from the CMA that it intends to audit the veterinary industry. The reason for the review is that the CMA has noticed rising costs for veterinary services, at the same time as the market consolidated by several major veterinary players (including EQT-owned IVC Evidensia, CVS Group and several others). The authority wants to investigate whether there is sufficient price transparency in the industry, and whether customers can clearly know that the clinic they visit is owned by a larger veterinary chain.

The uncertainty surrounding the review caused the CVS share to fall as much as 23% in September. The authority regularly conducts reviews of industries that have undergone a major change, and the review itself does not have to imply knock-on effects. We will receive the outcome of the review in 6–9 months. We have done a lot of work on the potential outcomes of the investigation and feel comfortable with our holding in CVS Group:

- If we compare CVS Group's growth with the growth in the number of employed veterinarians, it is clear that most of the company's growth has come from volume growth, versus price increases.

- Inflation in the industry is above all driven by a lack of access to vets (which was the case for a long time), as well as recently increased prices for medicines.

- We have had several discussions with the company's management and feel confident that the company has not acted inappropriately in any way.

- It is worth noting that the CMA informed journalists in advance of the review during market open hours on a Thursday before the news was officially released on a Friday. This was motivated by the fact that the authority did not believe that it was information that could influence the share prices. This may indicate that the authority simply does not see this as a particularly big deal (and/or that they have a certain lack of competence regarding the stock market...).

In conclusion, we believe that the market's reaction to the news is clearly exaggerated, and we have bought more shares. The company is expected to grow sales by 4–8% per year in the coming years, while the company's strong cash flows can be reinvested organically and for further acquisitions at a good return. During October, CVS also came out with a report showing that the company is doing very well operationally. The stock now trades at around P/E 17x (EV/EBITA 12x) for next year's forecast earnings, which is clearly lower multiples than what CVS has been rewarded with historically.

Pets at Home

Pets at Home, which is part retail and e-commerce business, part veterinary business, also saw its share price fall against the backdrop of the CMA’s actions. In this case, however, the profit from the veterinary segment accounts for about a third of the group profit, and Pets at Home's price drop was about 11% for September.

LVMH

LVMH was one of the fund's worst contributors during September. It's been a less than perfect storm for luxury companies during the month. Investors remain concerned about the Chinese consumer, but there has also been talk of Europe starting to show signs of weakness. Several of the companies in the sector have been out and lowered expectations for Q3, but also commented that Q4 is more in line. In addition, interest rates have continued to climb, which is negative for this type of company valuation. Our view is that LVMH has come down too much in September (-8.4%) and is now down 20% from its peak and we think the stock could rebound strongly toward the end of the year. The stock trades at P/E 20x and 18.5x for 2024e and 2025e. Something we think is too cheap, given the long-term structural growth and a large element of value creation for us as owners.

SLP

The share price in our logistics property company, SLP, fell by around 10% during the month. The property sector in general was under pressure and in Sweden the sector index fell by 6.5%. During the month, there was also a placement of one of the founders' B shares (retaining its A shares). We guess he will use the money for other projects. The placement was made at a 7% discount and the company brought in Fidelity as a new major shareholder. We think this is very positive and great sign of quality!

Corem

After being the fund's top performer in July and August, Corem retreated about 23%, adjusted for a dividend. No significant news to report but it was largely sector- and flow-driven.

Summary

September was a difficult month where central banks and rising interest rates put pressure on share prices and, in addition, with very low liquidity in the market. We are of course disappointed with the outcome for the month, but to understand the result, we can conclude that if you adjust for currency movements and the unexpected event in CVS, the rest of the portfolio traded more or less in line with the market.

We believe that the market, in many cases, has been very quick and gloomy in its interpretations of various news. This applies both at the company and macro level. An example to show the nervousness in the market was when one morning a brokerage firm lowered the recommendation in Axfood from Hold to Sell and in addition trimmed its estimates by 0-3%, that is, basically nothing. The stock immediately fell 5-6% to the new target price amid heavy trading. By end of the day, the stock had recovered and was down a more modest two percent. It feels like the market is reacting without asking or analyzing new information. Another shining example is (unfortunately) our own holding in CVS, whose share price fell by as much as 25% on the news we reported. Our basic thesis, after a lot of analytical work, is that in 6–9 months when the review is out there will be no or minor adjustments for CVS's daily operation of the business. But the market has neither the patience nor the nerve to own the stock now. In our world, risk/reward has now gone from attractive to very attractive. However, the disclaimer is that we can of course be wrong.

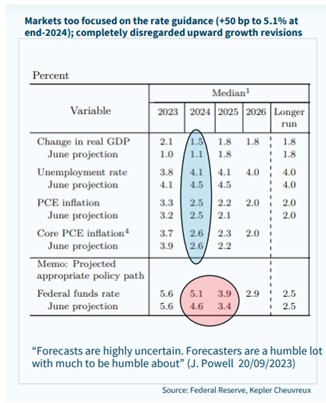

We also think the market was quite negative regarding the Fed's message about a longer and higher interest rate path. The main reason for the longer interest rate path was not that they saw higher inflation than expected, but because the economy was more robust than they had previously expected - thus they see a lower risk of recession.

Source: Federal Reserve, Kepler Cheuvreux

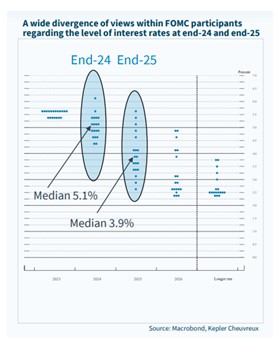

In addition to this, the new interest rate path is not a hard commitment, it is a forecast that contains, as they underlined at the press conference, an extraordinary uncertainty. We can also see that the 19 members of the FED committee have different views on the interest rate going forward and with a considerable spread.

Source: Macrobond, Kepler Cheuvreux

The fact that the Bank of England, the Bank of Japan and the Swiss National Bank all left interest rates unchanged in September was also ignored by the market.

Below is a picture that speaks against a lasting stock market rise. When the profit level among US companies falls below the short-term interest rate, it has historically led to declines in the stock market. However, if profits rise and interest rates fall, the fallout changes.

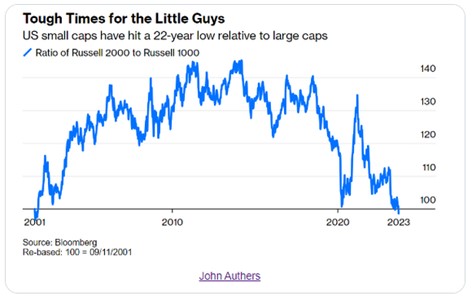

Even US small caps have had a weak year so far compared to the larger companies. They are now down to a 22-year low in relation to large companies and, reasonably enough, capital should soon find its way to these companies as well.

Source: Bloomberg, John Authers

The image below shows that Nasdaq's decline after the summer is now down to approximately the levels where the fall previously slowed down and led to new gains.

Source: Bloomberg

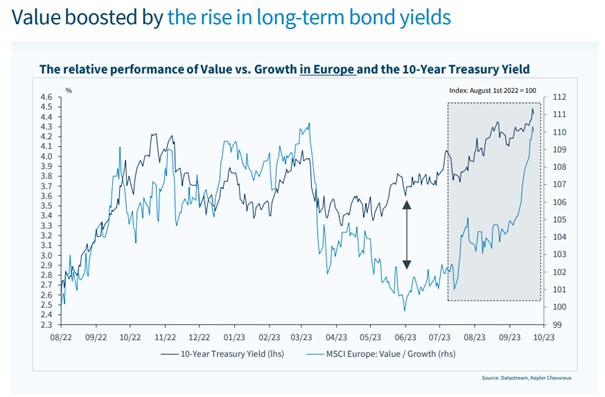

The rising interest rates have put considerable pressure on growth stocks, while cyclical stocks have benefited, see image below. There are great forces that have been set in motion.

Source: Datastream, Kepler Cheuvreux

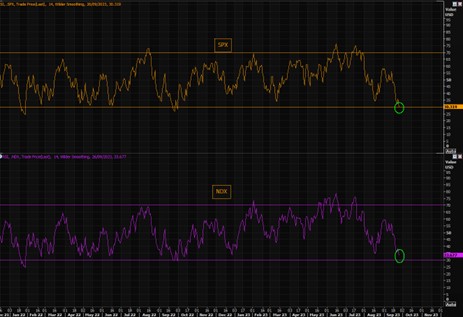

The S&P500 and Nasdaq are now down to their most oversold levels since September 2022.

Source: Themarketear.com

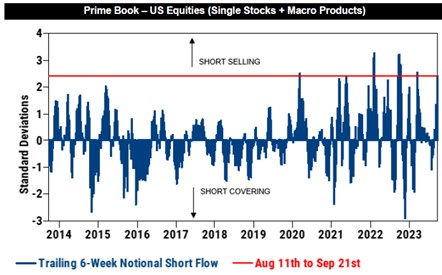

The volumes of short positions in the market have increased significantly in the last month and contributed to the declines. The reverse applies when the positions are to be closed.

Source: Goldman Sachs

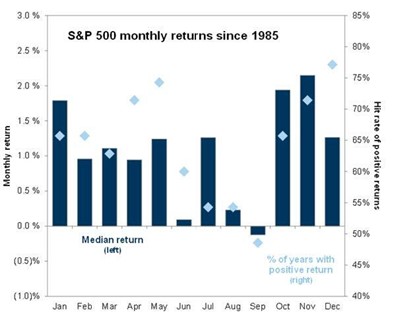

October and November are historically very strong stock market months, especially when the return has been positive until the end of the third quarter, as this year. Statistics say that since 1900, there have been 56 years where the stock market had more than a 10% return in the first nine months (like this year). In 48 of those cases, the stock exchange during the fourth quarter had a positive return of 4.6% on average. The best fourth quarter was 1985 with 17%. The worst was in 1929 with -28%.

Source: Goldman Sachs

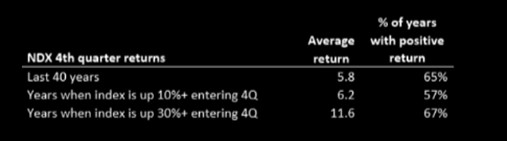

The return also seems to be stronger in the fourth quarter, the stronger the first nine months have been. Below are the data for the Nasdaq100, which in the first nine months of this year rose by a whopping 34.5%.

Source: Themarketear.com

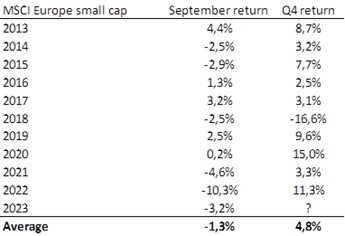

Below are the September data and the fourth quarter's development for European small and mid-caps.

Source: Coeli European

90% of American companies are now in a "black out period", i.e., they cannot make any buybacks as the reports for the third quarter are approaching. November and December are the months when the most shares are bought back in the market, which of course makes a positive contribution to the stock market.

Source: Goldman Sachs

So, what does all of the above mean for the end of the year?

In recent days, interest rates have continued to reach new highs, which has created some turbulence in the market, and the stock market needs to see a stabilization of interest rates before moving forward. We also noted that the sales flow of CTA's in the last week was at record levels, which left its mark on the stock market. The good news is that Goldman Sachs calculations also show that the programs should be completed within days.

Our best assessment is that the combination of the fact that many stocks are now oversold and that we are entering the seasonally strongest period means that we believe that the fourth quarter will also provide a positive return. In addition, we believe that the coming months will show continued falling inflationary pressure and it would be strange if this did not contribute to more positive market sentiment. In the long run, it leads to an expected first interest rate cut, but that is probably six months away (but earlier than what the central banks have communicated).

However, one must have respect for the fact that reduced globalization and the war in Ukraine, all other things being equal, pose a negative contribution to global inflationary pressure. The green transition is also driving up prices in some areas.

We thank you for your interest and look forward to the last quarter of the year.

Mikael & Team

Malmö on October 5th, 2023