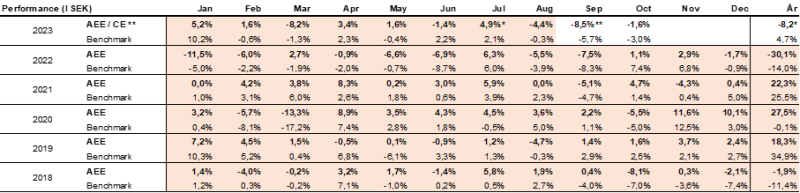

Note that the information below describes the share class (I SEK), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class' return. The information below regarding returns therefore differs from the returns in other share classes.

Before making any final investment decisions, please read the prospectus, its Annual Report, and the KID of the relevant Sub-Fund here

This material is marketing communication

Monthly Newsletter Coeli European – October 2023

OCTOBER PERFORMANCE

The fund’s value decreased by 1.6% in October (share class I SEK) while the benchmark decreased by 3% for the same month, measured in SEK.

*Adjusted for spin-off of Rejuveron.

** AEE: Absolute European Equity, CE: Coeli European, Benchmark: MSCI Europe SMID Cap Net Total Return SEK.

Please Note: On the 4th of September 2023, the strategy of the fund officially changed from a European long biased equity long/short fund to a European active long only fund. Simultaneously, the name changed from Coeli Absolute European Equity to Coeli European. The track record highlighted in colour in the table above is that of Coeli Absolute European Equity.

EQUITY MARKETS / MACRO ENVIRONMENT

October was an unusually intense month that was dominated by Hamas's vile attack on innocent Israelis leading to a new and ongoing war, by continued rising interest rates and by a slew of company reports. The first two events contributed to a negative climate in the world's stock markets, and companies with quarterly reports that were below expectations saw their share prices come under significant pressure. It took extraordinary reports for share prices to rise. So far into the reporting season, the price movements on weak reports have been the biggest since the third quarter of 2008! Having said that, we were pleased to see that the fund's reporting companies have fared very well and we are satisfied with the fund's performance in November in a challenging environment. There are still a number of important reports for our companies in November.

Measured in local currency, the broad European stock market fell in October by 3.7%, while European small and medium-sized companies fell by 6.0%. The S&P500 and Nasdaq fell by 2.3 and 2.8%, respectively. In Sweden, the OMX fell by 3.7% and the Carnegie Small Cap index by 3.2%. The fund value measured in Swedish kronor fell by 1.6%.

October was a weak month and up until October 27th, the Eurostoxx50 had fallen for six weeks in a row, which has only happened three times in the last 25 years (1998, 2008 and 2011). SBX, Stockholm's broad index, was down 10 out of 11 days from mid-October, which is extremely unusual. That investors are record depressed is no exaggeration and therefore we also see share prices that, on the contrary, are priced at unusually attractive levels for those who can persevere to own shares over a slightly longer period of time. Here we are mainly referring to small and medium-sized companies, which by Swedish standards are companies with a market capitalization of up to SEK 100 billion.

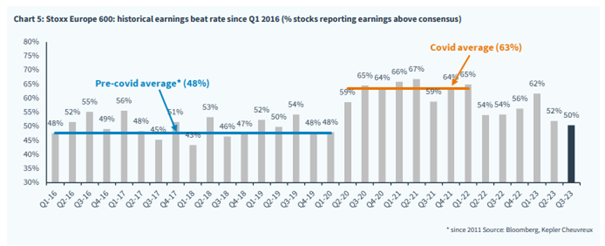

The proportion of companies that beat market expectations has been falling during the first three quarters of the year. The third quarter is still looking good with 50%of the companies surprising on the upside. However, future prospects have become somewhat clouded.

Source: Kepler Cheuvreux

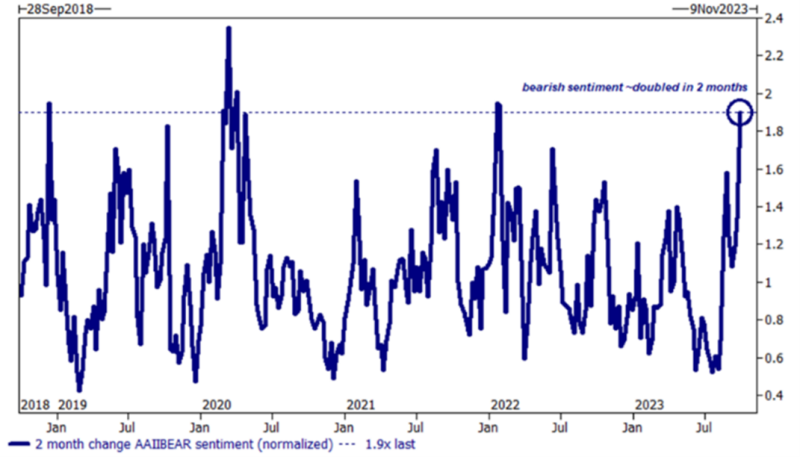

Investor sentiment has been and continues to be at very low levels. It can always get worse, but it is often a good contraindication when the sentiment indicator looks like the one below. At the end even the last seller in the market will have finished selling.

Source: Goldman Sachs

If we zoom out and ignore the tragic geopolitical development, then the single biggest explanatory factor for how the stock market developed during the autumn is the continued and rapidly rising interest rates. Only three months ago, expectations were that the US economy would have a modest GDP growth of 0.5% for the third quarter. On Thursday, October 26th, the result came and it was almost 10x higher at 4.9%. A real failing mark for all the world's forecasters and fantastically impressive for the world's largest economy. This in an economy where two-thirds is made up of private consumption. It has also succeeded in creating 2.8 million new jobs. Hat off.

For the stock market, the battle between recession and soft landing continues and whether the highest levels in the interest rate market are behind us. Formerly strong historical connections work worse in today's complex world. It is also the reason why investors have an unusually short investment horizon where they wait for the outcome in each situation.

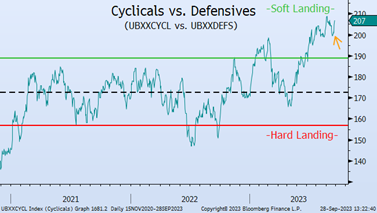

Those who invest capital coldly count on an economic soft landing. Cyclical companies have developed significantly better than defensive companies in the last six months.

Source: UBS

The talk of The three Big Bills in October: The first is the US Treasury bill, T-bills. The other is Bill Ackman, successful hedge fund manager, who tweeted that they were closing their short position in US Treasuries, causing interest rates to drop significantly from their highs.

Source: X

The third is Bill Gross, legendary bond manager who tweeted that higher for longer is yesterday's mantra.

Source: X

The recent sharp rise in the US 10-year yield is equivalent to a 75 basis point hike by the Fed. Jerome Powell admits that the US budget deficit and the FED's QT have contributed to the rise in interest rates, which in practice means that the FED has to some extent lost control over its policy. Now it is the bond market that dictates the conditions and if interest rates do not fall in the coming months, the risk of a recession increases, even in the world's most powerful economy. Hence Bill Gross's comment above, central banks are closer to interest rate cuts than they communicate. Maybe we'll see a break in QT soon? Incidentally, inflation is old news in the financial market and the decline will likely continue in the coming months.

Below shows that the yield curve will soon turn positive, that is, the 10-year interest rate exceeds the 2-year interest rate, which is more of a normal situation and what Bill Gross believes will happen before the end of the year. The difference now compared to how it usually is, is that the central banks have a policy which says that interest rates should be at high levels for a long time to come and that, all else being equal, will affect the economy negatively, which in turn is negative for stocks. The big question is therefore, how much should the earnings estimate go down before we turn back up? Soft landing or recession?

Source: Bloomberg

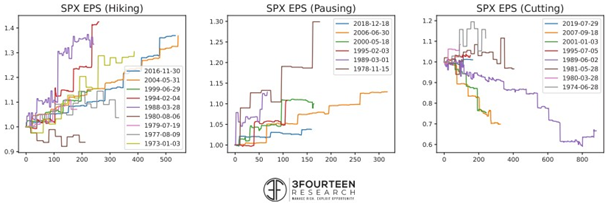

Below illustrates how earnings per share typically move when 1) the Fed raises rates 2) leaves interest rates unchanged and 3) lowers interest rates.

Source: 3FOURTEEN RESEARCH

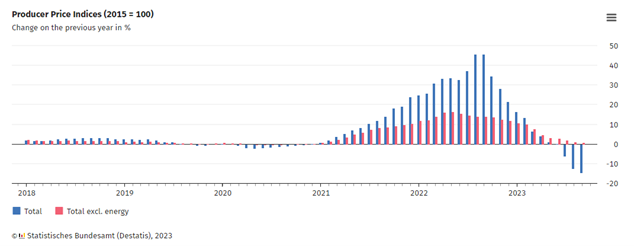

The latest data on German producer prices shows a decline of 15%! The corresponding figure excluding energy was around zero.

Who will finance the US budget deficit going forward? The figure below shows the Chinese government's holdings of US Treasuries. There is likely some depreciation included in the graph below, but clearly appetite has diminished. There is probably a political element here as well, as the relationship between China and the US is frostier than it has been for a long time. Coincidentally, we hear that preparation is underway for a meeting between Joe Biden and Xi Jinping later in November.

Source: Bloomberg, Holger Holger Zschaepitz

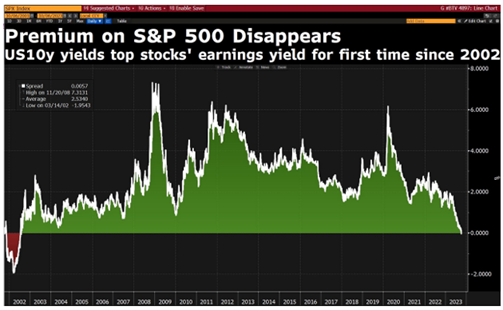

The high interest rate sucks capital out of the stock markets. For the first time since 2002, the earnings yield on US stocks is lower than the US 10-year yield. In Europe, however, the picture is completely different with significantly lower interest rates and valuations.

Source: Bloomberg, X

There are some glimmers of light even if you have to put in a little effort. The German IFO index shows a slight increase at the latest reading, but is still at low levels.

Source: Bloomberg, Holger Holger Zschaepitz

We note that the Greek interest rate is now lower than the American one. Spontaneously, one would think that as a bond investor you would want to be paid more for owning Greek government bonds than US ones.

Source: Bloomberg, Holger Holger Zschaepitz

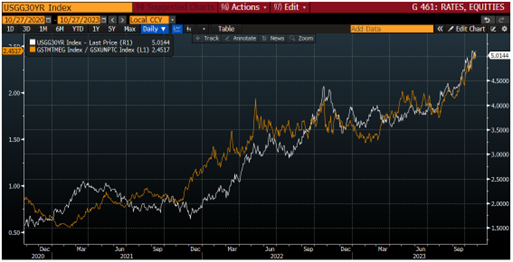

The white line below is the US 30-year. The orange line is the relationship between the big tech companies and a basket of unprofitable tech companies. The point is crystal clear, the large companies with extremely strong balance sheets are considered a safe haven despite rising interest rates, while unprofitable company shares are hit hard.

Source: Goldman Sachs, Bloomberg

The image below illustrates the share prices of the seven major tech companies (BT7) which have been almost completely decoupled from the rising interest rate. The yellow line shows BT7's price development and the white the inverted US long-term yield.

The breadth of the market (the percentage of companies trading above their 200-day moving average) is again, just like in September 2022 when the market bottomed, at an all-time low. It is a risk that one must be observant of, and this reporting season, BT7's reports have not led to any major price movements upwards, rather the opposite.

Only twice has the concentration of the most valuable companies been as great as today, and that was in July 1932 and November 2000. In the defence of the big tech companies, the expectations for the third quarter were a profit growth of around 33%. The other 493 companies in the S&P500 were expected to have earnings growth of a more modest 8.6% (source Bernstein).

Source: Bloomberg, Kepler Cheuvreux

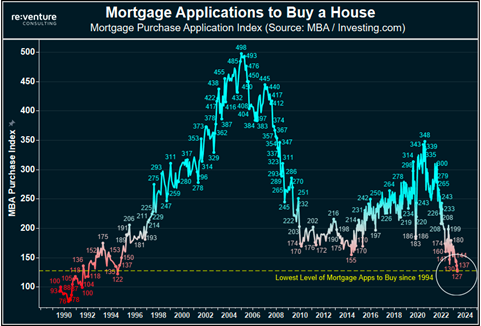

New home loan applications in the US are down 50% since the start of the year and are now at their lowest level since 1994. Even lower than during the financial crisis! The mortgage interest rate in the US is now over 8%, but all of 90% of those with mortgages have locked in the interest rates at significantly lower levels. Since statistics began to be kept, there has never been a worse time for private individuals to buy a home than now. At the same time, the rest of the economy is picking up steam thus indicating that these are unusual times.

Source: Reventure Consulting, X

It was a feeling of unease when Hungary's Prime Minister Viktor Orbán shook hands with the war criminal Putin during a visit to China in mid-October. The meeting took place in connection with the leaders of China, Russia and Hungary celebrating the tenth anniversary of the Chinese New Silk Road project. Orbán and Putin are said to have discussed bilateral cooperation in nuclear power, natural gas and crude oil. It is, to say the least, remarkable and quite bizarre that Hungary, which is a member of both the EU and NATO, has for a long time acted as an effective brake on Sweden's membership in NATO, probably eagerly encouraged by Putin.

Source: Associated Press

It shall not be easy. Microsoft’s share has had 10 times stronger price development than Philip Morris's over the past 10 years. Both had a growth in cash flow of 170%. Microsoft's earnings multiple increased from 9x to 40x, while Philip Morris fell from 17x to 8x. The bottom line is that there are only two things that drive a stock price over time - the company's ability to create value and the valuation when you make your investment. That's why we spend all our time on fundamental analysis.

Source: KochBank, X

Again, it shall not be easy.

Source: X

PORTFOLIO COMPANIES

Bonesupport

During the month, Bonesupport delivered another brilliant report in the damp autumn weather. The company's sales were 8% better than the high expectations and a whopping 41% better operating profit. With a gross margin of over 90%, it is the leverage in the business model that really started to show its colours. The stock market rewarded the share with a rise of 21% on the day of the report and this year has risen by a whopping 86% (the fund's best share this year).

It is now exactly 1 year since the company launched Cerament G in the USA. The product's run-rate sales per Q3 now stand at 251 million, an unparalleled feat in such a short time. What the market especially noticed during the report day (we think) was that the company mentioned that it now has access to 1,000 hospitals in the US but only 200 of these have ordered at least one package of Cerament G. We wrote about the penetration in our July newsletter in connection with their Q2 report. However, it seems that the elevator now went all the way up for analysts and that there is a very long duration in the deal.

The company has also set a date for a capital market day at the end of November. Now the company has positive cash flow and with little investment required, Bonesupport will quickly become a cash flow machine with cash EBIT margins between 40 and 50%. The Capital Markets Day will likely give more colour on what this money should be used for.

We believe that "Spine" is one of the indications that Bonesupport will touch upon as their next step in the growth journey (despite Cerament G just starting its journey). The market estimates that "Spine" has an addressable market that is four times larger than the one Bonesupport is approved for today.

Our view is that the market values Bonesupport based on known facts and does not price in new products. We see at least 30-40% upside in Bonesupport over the next two years and we take our hats off to CEO, Emil Billbäck, and CFO, Håkan Johansson, as well as the rest of the team at Bonesupport. The risk of a takeover has undoubtedly increased after another phenomenal report.

The image below shows the development of the operating profit on a quarterly basis for Bonesupport and it is unusual to see such a clear inflection point for a company where profits suddenly shoot off.

Source: Bonesupport, Coeli European

SLP

SLP delivered one of the strongest quarterly reports we have seen in a long time. The profit from property management came in 16% above expectations, which is a lot for a real estate company. The operating net grew by as much as 50% compared to the previous year. What impressed the most was that the net asset value, despite a return requirement that rose by 30 basis points, increased by 10% this year. It is improbably strong, and we are slowly starting to think about what will happen on the day the yield requirement starts to be lowered again, which should not be too far off in the future.

It is clear that SLP is a winner when other real estate companies have concerns. We believe they are in a very strong position and have the balance sheet to buy properties at levels not thought possible 12-18 months ago. If we do a simple calculation exercise and assume a growth in the operating net of 10% per year for the next two years and that the required rate of return drops from 5.9% to 5.0%, property values rise by approximately 3.5 billion or approximately SEK 17 per share everything else equal (the share costs SEK 26 today). We continue to sit tight and wait for future returns.

Cargotec

Finnish Cargotec delivered an undramatic Q3 report. The company had a pre-silent call a few weeks earlier, which we believe provided many answers to analysts' questions. The operating profit came in 14% better than expected, but all the focus is on the order intake for industrial companies and in Cargotec's case it was in line with expectations. The company also announced cost savings to meet the uncertain situation and has been very clear that it must defend a 10% operating margin within the group. There are a number of clear triggers in Cargotec over the next two years linked to the spin-off of Kalmar and HIAB and a sale of MacGregor.

The company trades at a very low 6x and 10x P/E ratios for the current year and 2024. That is extremely low for a, basically, unleveraged quality company. Kalmar and HIAB belong to the top Nordic industry leaders in terms of sales growth and return on capital. If the company delivers on its plan to sell MacGregor next year, upwards of 500 million euros would flow in while profits would not change significantly. The adjusted P/E ratio is then 5x and 8x. It's almost unbelievable.

The low valuation constitutes a large cushion should the economy deteriorate. It also gives a big upside if the outcome beats the estimate next year. We easily see a 50% upside in the relatively short term in connection with spinning out Kalmar and HIAB.

Corem

Corem's report was undramatic with a management result that came in line with expectations. The positive thing is that the company continues to have positive net lettings, which indicates that the underlying business is healthy.

Something that was very gratifying and that caused the share to rise by 23% in October was that they signed letters of intent to sell properties for an additional SEK 12 billion. Of these, 1.2 billion have now been implemented. Our hope is that the Copenhagen portfolio is included in this 12 billion. It would have a positive impact on the company's cash flow as these properties are low yielding and instead you can buy back expensive bonds.

Corem is a play on the underlying real estate market and the company's ability to restructure. So far, they have sold and entered into letters of intent for close to 25 billion in one year. As long as the discount is around 70%, it's just a matter of continuing to sell, even if it requires some write-downs. You can simplify it and say if you sell for 12 billion and have loans for 6 billion, 6 billion is released. That cash should reasonably not be traded at a 70% discount but at a zero percent discount. In this example, that would remove 4 billion in discount, which is about 40% of today's market capitalisation. All simplified of course, but you see the point. With enough selling, and we don't think it's that far off, you could then start buying back shares which would have been extremely valuable at these levels.

Lindab

Over the years, we have been spoiled with good reports from Lindab. The Q3 report that came in October was no exception. The company's operating profit of SEK 351 million exceeded expectations by almost 20%. Despite lower volumes, Lindab has managed to defend margins in a good way with the help of cost programmes, completed capital investments and an improved inventory situation. In addition, the cash flow was strong, which is favorable for the next stage in the Lindab story: acquisitions.

When we invested in Lindab for the first time in 2019, the investment thesis was very much about CEO, Ola Ringdahl, succeeding in transforming the business structurally and via organic investments to increase profitability. Today, the major changes have been completed and the company is more forward-looking and focused on growth. In the Q3 report, an ambition to reach SEK 20 billion in turnover in 2027 was announced, to be compared with the 12-month rolling turnover of SEK 13 billion. Most of that growth will be acquired.

We recognize the acquisition strategy from other successful acquisition companies. Lindab wants to buy well-managed companies at a reasonable valuation, preferably with management retained and with a high degree of autonomy. Ideally, you make many, but slightly smaller acquisitions to reduce the risks. Since 2020, it has acquired more than twenty companies, and many more will be needed in order for Lindab to reach its turnover target in 2027. Despite the fact that Lindab wants to maintain a decentralized structure, there are clear synergies in, above all, purchasing. In the conference call, it was said, for example, that they had succeeded in raising profitability from 4–5 to 7–8 percent for Felderer, a German distributor business that was acquired in 2022.

As we value the company, the share is currently traded at around 10x operating profit in 2025. Such a valuation naturally reflects that the market is uncertain about the construction industry (and a higher interest rate situation). At the same time, we think it is too low for a Lindab that is becoming a better company year by year, and which should be able to take market shares in a tough climate. In the longer term, Lindab could be awarded a serial acquirer multiple and the latest report had a quality that for us was a clear step in that direction. The stock rose by 7% in October.

Volution

During the year, we bought shares in British Volution. The company sells ventilation equipment with a focus on housing. The housing focus has of course raised some question marks in relation to headlines about the every day situation, but in October Volution released its report for the broken financial year which ends at the end of July. Despite the circumstances, organic growth was 5%. The operating margin landed at just over 21%. The market liked what it saw and Volution rose 8% on the day of the report.

The company has good protection against the construction industry for several reasons: first, the proportion of revenue that comes from renovation is high, and second, more and more regulations (both at the EU level and for individual countries) provide a strong tailwind in sales. Many of Volution's products help customers improve energy efficiency/save money, which is of course desirable when consumers' wallets are getting thinner. We ask ourselves the question: How much should Volution grow when the construction industry turns? Clearly higher than 5%, we think. The stock trades at single-digit earnings multiples (in terms of operating profit), which we think is far too low.

LVMH

LVMH was the only report in October that did not meet our and the market's expectations. Organic growth came in at 9% against the expected 11%. The market has been spoiled for a long time with very strong reports, but this led to estimates being subsequently lowered by a few percent. As usual, the share reacted more than that and on the day of the report the share fell by 6.5%. When the rest of the stock market came under renewed pressure in the second half of October, however, the LVMH share held up well. We have maintained our position as we believe that around 20x in P/E ratio for 2024e is clearly attractive for one of the world's best companies.

Biotage

Biotage is a relatively new company that we started buying into during the summer with a small observational position, as we thought that the stock had come down a lot while there were some technical factors surrounding a larger acquisition. The stock continued to fall and as our knowledge of the company increased we bought more stock.

It is a global company headquartered in Uppsala , Sweden, that provides solutions for more efficient drug development (65% of sales), analytical testing (27% of sales) and water and environmental analysis (8% of sales). The company specializes in innovative separation and purification solutions. The company develops and supplies instruments, consumables and expertise to facilitate the purification and analysis of complex molecules. Today, the development of synthetic drugs is the largest division (white pills), but with the acquisition of Astrea (in May), the company expanded towards biopharmaceuticals. We will return to this.

Biotage is undoubtedly a quality company within its niche. The company has eighteen of the twenty largest pharmaceutical companies as its customers. In the last 10 years, it has had a turnover growth of an average of 14.5% per year, of which 6.6% organically. During the same period, EBIT has grown by 22% annually. In the period before Covid-19, organic growth amounted to 8.6% annually.

The company has a history of making smaller bolt-on acquisitions. In principle, one hundred percent of their sales are direct to customers. It is expensive and takes time to build such a sales organization and infrastructure, but once in place it is very effective in selling new products or integrating new products from acquisitions. The effect over time can be seen in the growth of the operating profit. This means that Biotage has a ROCE of 25% on average over the past five years. If we adjust for goodwill, ROCE averages around 41%, which should be a better benchmark given where the company stands and is going. It is thus a company that has created and continues to create significant shareholder value.

In May, Biotage acquired Astrea Bioseparations. Simplistically, you can say that Astrea does the same thing as Biotage in biopharmaceuticals. The seller of Astrea was a KKR-backed fund and the interesting thing about the deal is that they paid 100% with shares (at a price of 160) and that Astrea went in and took two board seats in Biotage. From what we understand, the companies have been discussing the deal for 5-6 years before it took place thus indicating that the companies are more intertwined than one might first think.

What’s the outcome of this deal then? Astrea gets access to Biotage's infrastructure, which has been built over several years. Biotage gets access to a market that is growing faster than the one it is active in today. Biological medicines are expected to grow by over twenty percent per year for the next ten years. Astrea has a very high percentage of recurring sales, which takes the group to 65% recurring sales per Q3.

In the past year, diagnostic and pharmaceutical companies have had the most challenging environment in twenty years. The hangover from doped Covid years was painfully reminded this year. The development of Covid related products and cheap financing meant that several of these companies were under high pressure in 2021/2022. It is only this year that we see a normalization. As far as we know, there is not a single company out there that has not profit warned or been guided down in the sector. To quote Bio Rad's conference call "a biopharma meltdown". This has put pressure on the companies' profits but also on the multiples.

Our initial thesis was that the market would bottom out in Q3 and that peak fear would hit around the report. We can confidently state that we were almost right. Adjusted EBITA came in 12% better than expected and the stock rose 17% on the day of the report. Astrea has grown 38% YTD, which is impressive given that the rest of the sector had and has negative growth. Organically, turnover decreased by 9%, but the company was positive about the future and said that instrument sales are starting to look brighter. Biotage faces simpler comparative numbers already in Q4, when it had -1% in organic growth, only to gradually become even simpler in 2024. Both Sartorius and Repligen (closest peer to Astrea) mention that orders probably bottomed out in Q3 and signs that it accelerated towards the end of the quarter.

To sum up, we think that Biotage has become a better company with the acquisition of Astrea. Higher growth, better margins, higher return on capital and more recurring revenue. All this at a lower valuation than what the company has been traded at historically. As the company has grown sales faster than the sector, it has historically been valued at a premium, but now it is at a roughly 30% discount. We see significant upside from here (50-60% in 12 months) and believe the stock will gradually re-enter the spotlight.

SUMMARY

October offered unwanted and tragic events which pressed down the risk appetite with lethargic trading as a result. 2023 is the worst year in Europe since 2014 in terms of trading volumes on the various stock exchanges. In the UK, volumes so far are the lowest since 2004! Completely unimaginable actually and something we also notice when we have to make adjustments in the portfolio.

Geopolitics often have less significance for the stock market than one might think. Regional wars, nasty as they may be, do not tend to upset the global economic cycle. The concern about an escalation has tightened the bow firmly downwards and a basiccondition for a more positive end to the stock market year is that the war does not escalate.

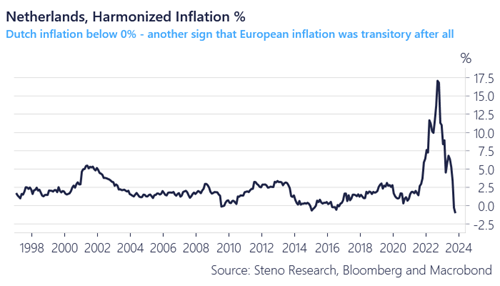

Significantly more positive is that inflation continues to fall at a rapid pace. On October 30th, we got Spanish and German inflation that was significantly lower than expected (m/m 0.3% in Spain and -0.2% in Germany). The Netherlands reported a few days ago that annual inflation is -1%! The ECB kept its key interest rate unchanged in October and we still believe that they will start lowering significantly earlier than communicated (Q1?). The downside of this is of course an economy that is slowing down.

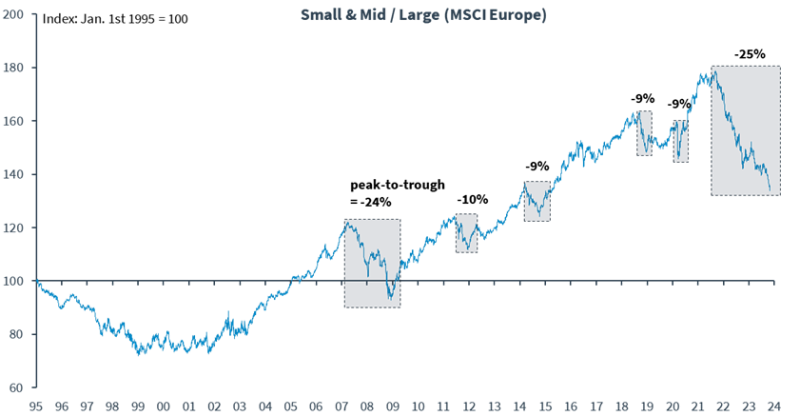

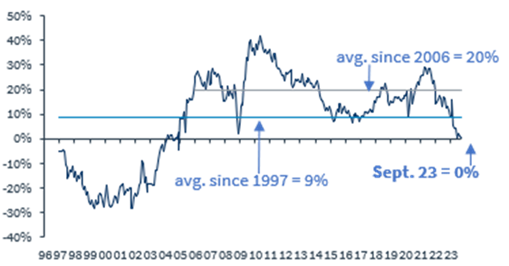

The larger companies continued to do better than smaller companies until the last days of October when it turned around in favour of smaller companies. It remains to be seen if that was the turning point, but in general you can say that the bigger the company, the better the return and the difference is now at record high levels. We are convinced that the smaller companies will get revenge, but it is unclear when the turning point will occur. The facts are that the differences are record-breaking, that smaller companies are early in the stock market cycle and are the most sensitive to a rising interest rate (and vice versa). Below is the relative development of smaller companies against larger companies since 1995. As of October 30, a new record was broken with -25% since the peak.

Source: Kepler Cheuvreux

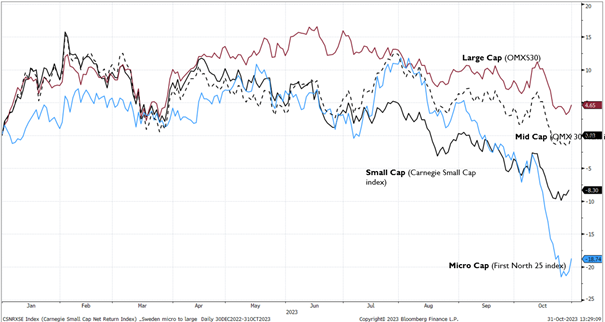

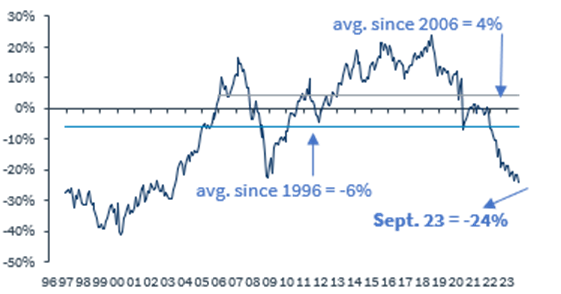

Below is the development on the Stockholm Stock Exchange during the year. The bigger the better the return. During August-September, when the American interest rate began to rise sharply, the development diverged significantly. The curves are likely to reverse in the next year (our view).

Source: Carnegie, Bloomberg

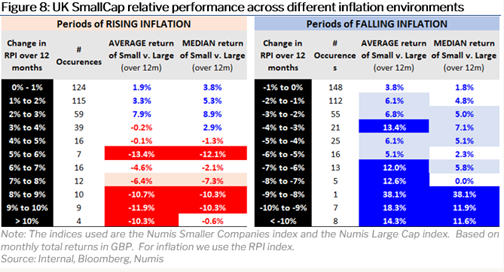

The excellent compilation below shows how smaller companies develop in times of rising and falling inflation. The numbers speak for themselves and inflation is, as you know, on the way down at a rapid pace.

Source: Montanaro, Bloomberg, Numis

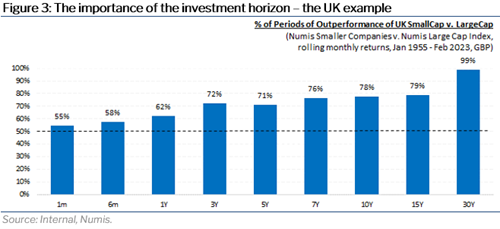

It all depends on what time horizon you have. A survey by the London Business School showed that between 1954-2022, British smaller companies developed 3.1% better than larger companies per year. This means a difference in the return over the period which was 7 times greater for the smaller companies and this is of course the reason why the asset class is so interesting, especially now after two years of very weak relative returns.

Another telling picture.

Source: Montanaro, Numis

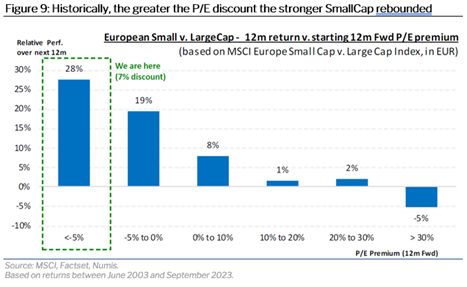

The greater the valuation difference, the stronger the return over the next 12 months. According to this we should be well positioned given the starting point today.

Source: Montanaro, MSCI, Factset, Numis

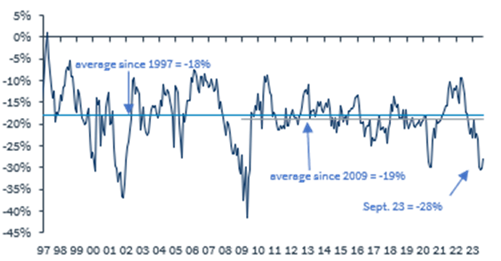

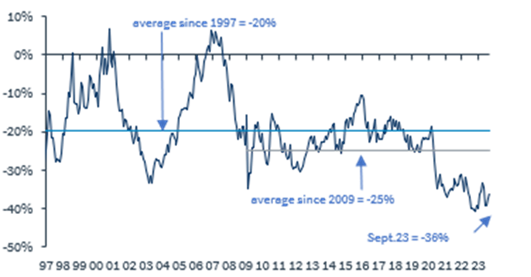

The images below show the valuation difference between European small and medium-sized companies compared to large companies since 1996. Relative P/E on the left and relative P/B on the right. We are at historically low levels.

Source: Kepler Cheuvreux

Below is shown the difference in valuation between European and American small and medium-sized companies. Relative P/E on the left and relative P/B on the right. Here, too, we are at historically low levels.

Source: Kepler Cheuvreux

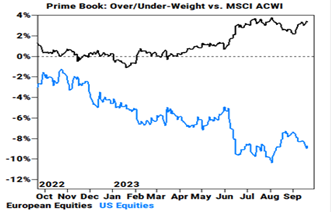

The valuation difference between Europe and the USA is probably the reason why American investors have sold American stocks since last summer and increased their exposure in Europe.

Source: Goldman Sachs

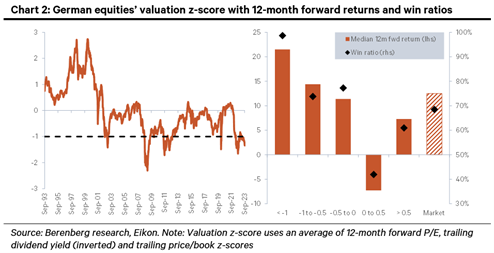

Berenberg has compiled the image below showing the Z-score for the German stock market. Z-score is a combination of P/E ratio, dividend yield and P/B. When the Z-score is below -1 (now -1.5), the German stock market has historically risen by 22% in the following 12 months and with almost 100% accuracy.

Source: Berenberg

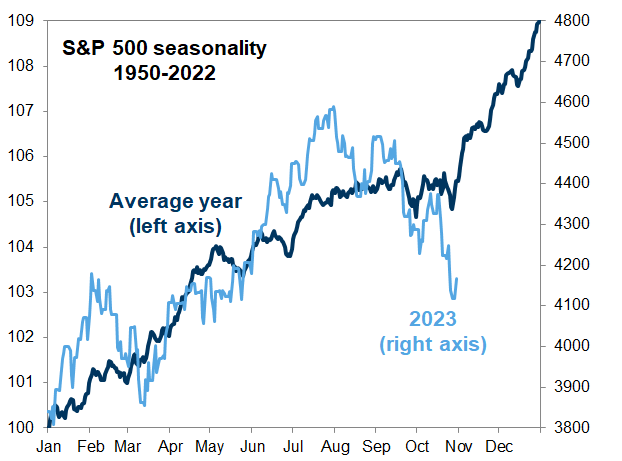

The last picture for this time shows the seasonal variation in the yield. There is no law of nature that says the return will be positive, but the seasonal effect over the long term is clear.

Source: Goldman Sachs

In summary, our market view a month ago was that we expected a positive return for the fourth quarter, which we maintain. We did not expect October to be so weak, but the Hamas attack and its consequences changed some of the conditions. The single greatest risk now in our view is if the war between Israel and Hamas escalates.

There are some signs that stock markets have began a recovery, and especially within the asset class small and medium-sized companies.

• In the last days of October, the indices for small and medium-sized companies developed a couple of percentage points better than broad indices. It had been a while since that happened.

• The reporting period is largely over and volatility from the reporting period is likely to decrease (predominantly negative volatility in October).

• The US 10-year yield has turned down a few times from the high of five percent as bond buyers have come in. If it breaks through five percent tough, it will be strained for a while.

• The sentiment among investors is downright depressed.

• The positioning in the market is not rigged for an upswing and many are sitting on a large cash register.

• The buybacks start rolling and November/December are the months with the largest volumes in terms of share buybacks.

• Most broad indices are down three months in a row. That is unusual.

• Most funds have had an outflow, and above all small company funds. At some point it will end.

• Many stocks are well oversold and largely due to large outflows.

When we then look into 2024, it's all about how much the profits will decrease, but we'll come back to that!

Thanks for your interest.

Mikael & Team

Malmö, November 6th, 2023