Before making any final investment decisions, please read the prospectus, its Annual Report, and the PRIIP of the relevant Sub-Fund here

This material is marketing communication

Last month we wrote “there is blood in the streets” and we tactically increased our net exposure. We may be wrong, or just early, but for the first time in many years, there is strong valuation support in many of the great companies involved in the energy transition.

Nevertheless, this year has presented a complex narrative for investors. Are renewable energy investments something that only works when interest rates are zero? Or is the energy transition just a big hoax? The answer to both questions is no.

In the last monthly, we explained why renewable developers would be able to incorporate the higher cost of capital and still make good returns on their investments. In this report, we will discuss the longer-term structural opportunity which is unique to the energy sector.

Even though fighting climate change and ESG are important factors to mention, they pale in comparison to the need to grow energy supply to meet increasing demand. We need more gigawatts of energy, period.

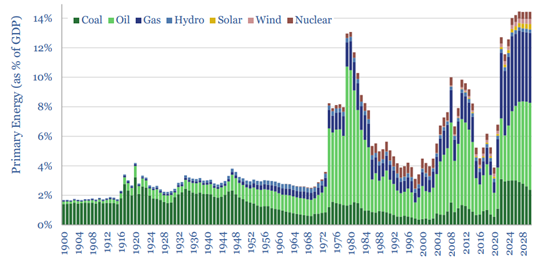

The year 2022 marked a critical inflection point in the global energy landscape, revealing the vulnerability of our energy systems, in particular to geopolitical shocks. Primary energy consumption, a measure of the total energy consumed across all energy sources, surged to over 12% of global GDP, according to Goldman Sachs, and even higher in Europe, from a 5-6% average since the mid 1980’s. This signalled not just a post-pandemic economic reboot or supply chain anomalies, but more importantly an underlying chronic underinvestment in energy infrastructure.

ThunderSaid Energy, a leading energy consultancy firm, estimates that energy markets could be undersupplied by 2.5-5% between 2025 and 2030, translating to a shortfall of about 2,500 to 5,000 terawatt-hours or a staggering USD 1 trillion of underinvestment per annum. Note that this is predicated on conservative energy per capita growth assumptions. It is this growing mismatch between supply and demand for energy which is one of the key reasons why we are long term optimistic to renewable energy.

The undersupply will cause energy costs as percentage of GDP to stay structurally higher in the second half of this decade, according to ThunderSaid Energy. This will likely put significant strain on the global economy.

The solution is more investments in energy, but due to ESG and the fight against climate change, many investors find it difficult to invest in fossil fuels. Others see fossil fuel investments as too risky since carbon taxes will only become a more fervent topic as the planet warms. We therefore anticipate that investments in renewable energy will only accelerate to cover the impending energy supply shortfall. This trend will likely result in structurally higher power prices over the next decade, hurting the global economy, but growing the total addressable market (TAM) for renewable companies while boosting their financial returns.

Moreover, historically, in periods with high energy prices, real economic growth has been relatively weak and brought about a challenging investment environment. In these instances, investing in energy companies has been an effective hedge as they benefit from the higher power prices.

The quicker the shift away from fossil fuels, the greater the returns for renewable investments as they stand to fill an ever-widening gap. This transition is not only about adhering to environmental imperatives but also about pragmatic economic planning.

Joel Etzler

Portfolio Manager Coeli Renewable Opportunities

- Portfolio Manager Coeli Renewable Opportunities

- Joined Coeli in 2019

- More than 13 years of experience from the financial industry

- MSc from the Royal Institute of Technology

Joel Etzler is Portfolio Manager and Founder of the Coeli Renewable Opportunities fund and has more than 13 years in the industry, with investment experience from both the public and private equity side. Etzler joined Kalvoy at Horizon Asset in London in 2012 and spent five years before that within Private Equity at Morgan Stanley. Etzler started his investment career within the technology sector at Swedbank Robur in Stockholm, 2006.

Vidar Kalvoy

Portfolio Manager Coeli Renewable Opportunities

- Portfolio Manager Coeli Renewable Opportunities

- Joined Coeli in 2019

- 25 years of experience from the financial industry

- MBA from IESE, MSc from Norwegian School of Economics and Business Adm.

Vidar Kalvoy is the lead Portfolio Manager and Founder of Coeli Renewable Opportunities fund. He has 25 years of experience from portfolio management and equity research. For nine years he was responsible for the energy investments at Horizon Asset in London, a market neutral hedge fund. Kalvoy also did energy investments at MKM Longboat, another hedge fund in London. He started his financial career as a sell side equity research analyst focusing on the technology and telecom sector, working six years in Oslo and Frankfurt. Prior to working in finance, he was a second lieutenant in the Norwegian Navy.