This material is marketing communication

Before making any final investment decisions, please read the prospectus, its Annual Report, and the KIID of the relevant Sub-Fund here

Coming into the earnings season, all eyes were focused on the Mag 7 stocks. Investors were keen to see whether the substantial investments in AI data centres would begin to be reflected in their earnings or future guidance. If these investments did not translate into immediate financial gains, would the momentum behind AI investments stall or at least decelerate? For the power sector and many renewable energy companies, the anticipated surge in power demand driven by data centres has emerged as a significant growth driver. Any slowdown in AI investments would therefore pose a risk to the long-term prospects of these companies. We discussed this dynamic in detail in our March-24 report “ROADBLOCKS ON THE AI HIGHWAY”.

Alphabet was the first of the hyperscalers to report and despite its search revenues beating expectations and the claim that AI-related revenues had reached a scale of ‘billions of dollars’, the stock sold off and pulled down the rest of its peers and the market. Thankfully, Microsoft, Meta and Amazon later confirmed that not only did they see returns on the huge investments, but they also expect significant growth in spending on AI over the next years.

While Microsoft claimed that demand for AI was outgrowing supply and that it could not build data centres fast enough, Meta revealed that its upcoming Llama 4 AI model will require 10x the compute power versus the current Llama 3 model, warranting “significant” capex growth in 2025. From the renewable energy industry’s point of view, there is still momentum in the AI trade and demand for power is only going to increase.

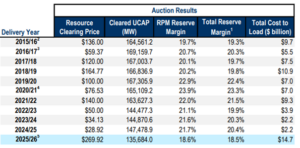

We have discussed in several monthly reports how demand for powering data centres is likely to raise the price of renewable Power Purchase Agreements (PPAs). This was likely confirmed in July as we received an additional tangible data point signalling stress in the supply/demand balance of the power markets. At the end of the month, PJM, the largest Regional Transmission Organisation (RTO) in the US coordinating wholesale electricity in 13 states covering 65 million customers, announced that the clearing price in its capacity auction for 2025/26 delivery year had increased by a staggering 900% versus last year. As can be seen from the table below, the total cost in the auction jumped nearly sevenfold to USD 14.7bn from USD2.2bn in the prior period.

Source: PJM 2025/2026 Base Residual Auction Report – July 30

The capacity market auction serves to ensure there is sufficient load (power) to meet predicted energy demand in the future period with a margin called reserve margin. Historically, when reserve margins deteriorate, high capacity auction prices result in a surge in new power generation capacity investments. This is thus a good omen for both new renewable development and grid expansion.

Nevertheless, the high auction prices in PJM are only partly due to increased electricity demand from data centres and electrification of other industries. The high prices are also reflecting closure of mainly coal plants as well as new market rules to better account for extreme weather risk and adjustments to each power resource’s value in the auction. Either way, there is a supply/demand imbalance, and someone will have to pay for increasing the power generating capacity in the region.

In general, capacity payments are only a small part of the total bill for electricity customers in the US, e.g. it was only 8% of the total bill for customers last year, according to PJM. However, it is not difficult to predict a substantially higher share of capacity payments for PJM customers next year.

How will the consumers react to the higher electricity prices? On the one hand, the tech industry is creating a lot of new jobs through their large investments in the PJM states, but on the other hand, no one likes substantially higher utility bills. This is likely to continue to be a hot topic of discussion for some time and the blame game in the media is just starting. Thus far, the RTO has received most of the criticism by failing to plan for increased generation and grid upgrades. However, electricity bills are not yet reflecting the new capacity prices and we find it likely that finger pointing towards the tech industry could also become a topic.

This might have been one of the first tangible examples of the ensuing imbalance of supply and demand in the power markets, but more are sure to follow.

- Portfolio Manager and Founder of the Coeli Energy Opportunities Fund.

- Over 15 years of investment experience spanning both public markets and private equity.

- Managed the Coeli Energy Transition Fund from 2019 to 2023.

- Spent six years at Horizon Asset in London, a market-neutral hedge fund.

- Started working with Vidar Kalvoy in 2012.

- Five years in Private Equity at Morgan Stanley.

- Began his investment career in the technology sector at Swedbank Robur in Stockholm in 2006.

- Holds an MSc in Engineering from the Royal Institute of Technology (KTH), Stockholm.

- Portfolio Manager and Founder of the Coeli Energy Opportunities Fund.

- Has managed energy equities since 2006 and brings more than 20 years of experience in portfolio management and equity research.

- Managed the Coeli Energy Transition Fund from 2019 to 2023.

- Head of Energy Investments at Horizon Asset in London for nine years, a market-neutral hedge fund.

- Experience from energy investments at MKM Longboat in London and equity research in the technology sector in Frankfurt and Oslo.

- Holds an MBA from IESE in Barcelona and a Master’s in Business and Economics from the Norwegian School of Economics (NHH).

- Before entering finance, he served as a lieutenant in the Royal Norwegian Navy.

IMPORTANT INFORMATION. This is a marketing communication. Before making any final investment decisions, please refer to the prospectus of Coeli SICAV II, its Annual Report, and the KID of the relevant Sub-Fund. Relevant information documents are available in English at coeli.com. A summary of investor rights will be available at https://coeli.com/financial-and-legal-information/. Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested. Please note that the management company of the fund may decide to terminate the arrangements made for the marketing of the fund in one or multiple jurisdictions in which there exists arrangements for marketing.