Monthly Newsletter Coeli European – October 2024

This material is marketing communication.

Note that the information below describes the share class (I SEK), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class’ return. The information below regarding returns therefore differs from the returns in other share classes.

Before making any final investment decisions, please read the prospectus, its Annual Report, and the KID of the relevant Sub-Fund here.

October Performance

The fund’s value decreased by 3.2% in October (share class I SEK), while the benchmark decreased by 1.2%. Since the change of the fund’s strategy at the beginning of September last year, the fund’s value has increased by 21.6% compared to an increase of the benchmark by 9%.

Source: Coeli European

* Adjusted for spin-off of Rejuveron

** Includes September 1 (strategy change to long-only implemented September 4 2023)

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

Equity Markets / Macro Enviroment

At the end of October, the autumn darkness set on the stock markets, and we experienced some of the weakest days in over a year. The month’s conclusion resulted in the broad European index falling by 3.4%, the S&P500 by 1.0% and the MSCI Europe SMID Cap by 3.8% (measured in euros) for October. The main driver can be explained by a rising US long-term interest rate, but also a generally increased nervousness about the outcome of the US election and pressured sentiment. Below is the development of the US long-term interest rate in recent months.

Source: Bloomberg

Volatility for individual stocks during this reporting season has been and continues to be very high. Weak reports have been punished hard. The fund had a weak month with -3.2% development compared to our benchmark, which fell by 1.2% (measured in SEK). A weakening of the Swedish krona in recent weeks dampened the decline in the SEK class. For the full year, the fund has risen by 13.9% compared to the benchmark, which rose by 10.7%.

The single biggest reasons for the month's development were weak reports from Lindab and Campari, more on that in the later section about our portfolio companies. Positive contributors during the month were Bonesupport, Cargotec and Accelleron. Negative contributors were Lindab, Biotage and Campari.

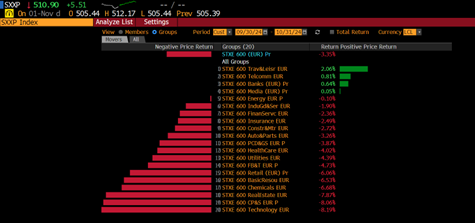

European interest rates also rose in October, which put pressure on real estate and technology companies, among others. Below is the sector development for October.

Source: Bloomberg

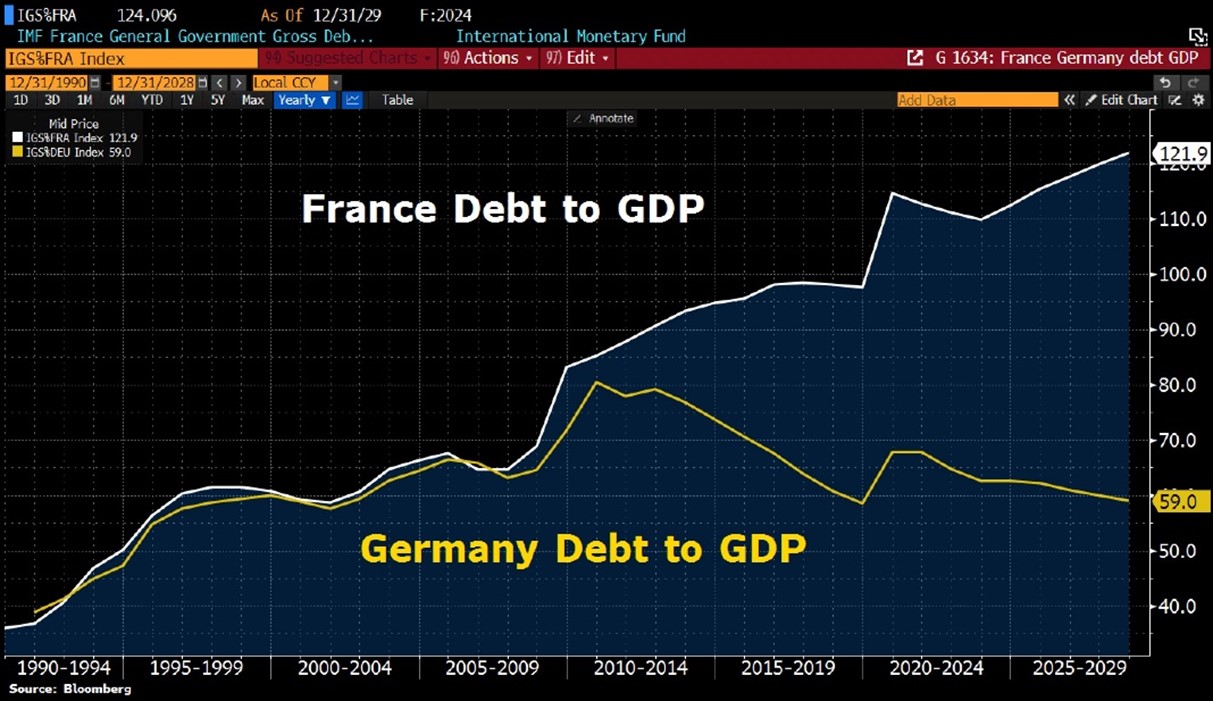

France, which has been a source of political European turmoil since Macron unexpectedly announced new elections in early June, had its outlook downgraded by Moody's from stable to negative. The willingness of the French population to face reality feels limited. It's time to realize that one must whine less, work longer and more efficiently if one wants to be able to compete with the rest of the world. It is nonetheless specific to France, but a widely practiced European phenomenon. The Financial Times also wrote that Germany now has 19.4 sick days a year and, according to a survey, GDP would have risen by 0.3% instead of -0.5% if sick leave levels had been in line with a European average. Before the pandemic, the number of sick days was 14. Sweden has around 15 sick days per year, which also seems high. Three weeks a year!

Source: Holger Zschaepitz, Bloomberg

Rising US long-term rates and generally lower risk-taking meant that the dollar strengthened against the euro. With Donald Trump as president, the euro could fall further, which in such case would dampen the negative economic impact on the eurozone.

Source: Bloomberg

Inflation in Europe remains under control even though the latest data point was marginally higher than forecasted. This meant that expectations of a double rate cut from the ECB in December were dashed. It was also followed by some hawkish comments from various ECB members. We have difficulty understanding how the ECB thinks and reasons, but this is nothing new. The combination of central bankers' power and their competence is one of humanity's greatest conundrums (slightly exaggerated and hastily written).

Source: HEDGEYE

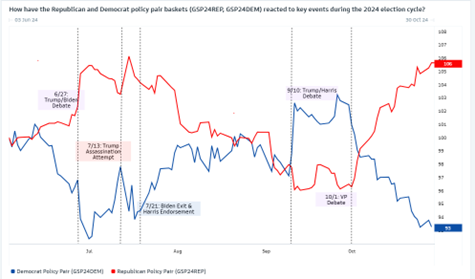

Below illustration shows how different baskets of shares have traded in recent months. One basket benefit from the policies of Kamala Harris and the other, the red one, benefits from the policies of Donald Trump. The financial market has been convinced for a month that Donald Trump will be the next president of the United States.

Source: Goldman Sachs

We can come up with some ideas.

Source: The Economist

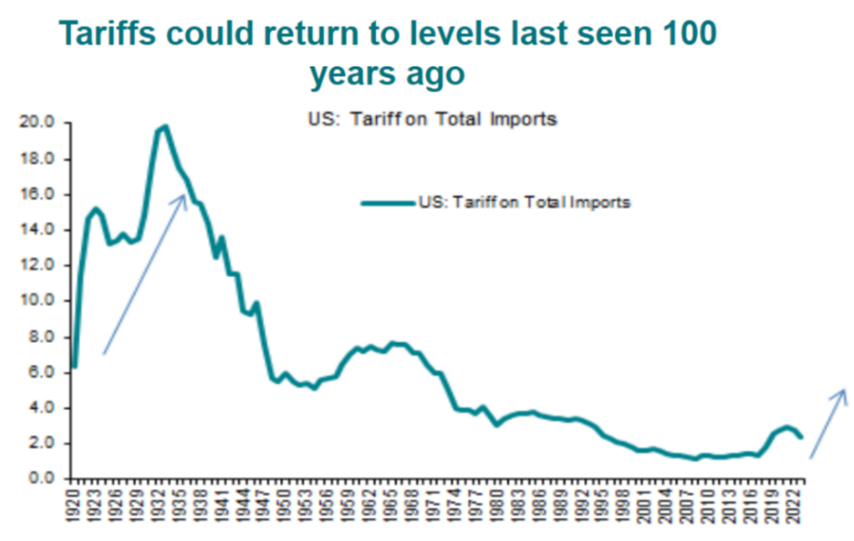

Trump has promised new tariffs on a broad scale. There are very few winners from that proposal, and it is also inflationary.

Source: BNP Paribas

It must be considered a little odd when Donald Trump started talking about his old friend Arnold Palmer's "anatomy" at a rally in Pennsylvania, see video: https://www.youtube.com/watch?v=ElY8QPtgMyQ

That statement was topped off with another rally where he said, "who the hell wants to hear questions?", and instead started playing music on full volume and danced/rocked for 38 minutes. You are recommended to watch the clip. https://www.youtube.com/watch?v=5NXion858gI. But you have to give it to him that it was a good playlist. Afterwards, speculation began about his mental health and Kamala Harris wrote on X: "Hope he's okay".

Elon Musk has got into gear and for the past two weeks has been handing out $1 million every day to a lucky few who attended Trump's campaign rallies. On his platform X, he has, to put it mildly, clearly disclosed his views of both candidates and has reportedly "almost always" been sober when posting. For his great support, he will reportedly be rewarded a place in the White House where he will clean up among authorities that hinder technological and economic development.

Source: X

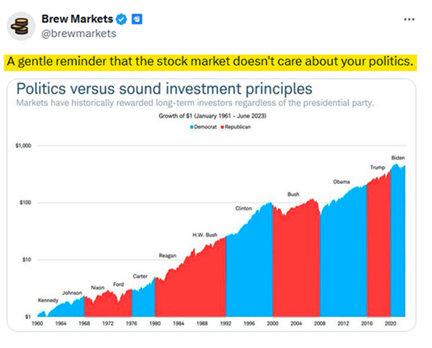

As consolation and to travesty Keynes: "In the long run we are all dead". The stock market does not seem to care about politics in the long term (thankfully).

Source: Brew Markets, X

Contrary to what many experts believed; the price of oil has remained at moderate levels. The graph below shows the development since the outbreak of the war in February 2022.

Source: Bloomberg

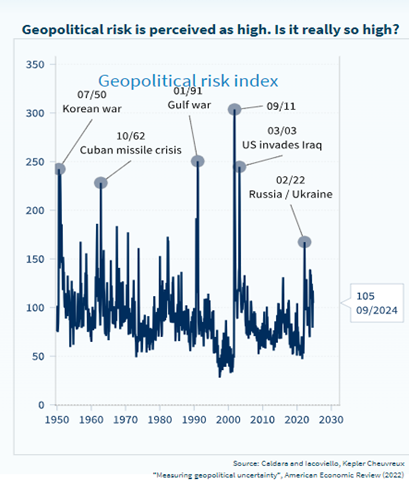

The geopolitical risk index below indicates that the current state of the world is almost normal. The feeling is that the situation is worse than what it appears to be from this particular index. For reference, OMXSGI rose 35% in 2023 when the US invaded Iraq.

Source: Cardara and Iacoviello, Kepler Cheuvreux

We congratulate Daron Acemoglu, Simon Johnson and James A. Robinson on being awarded the prize in economic sciences 2024 - "for studies of how institutions are formed and affect prosperity”. A warm welcome to Stockholm in December!

Source: Kungliga Vetenskapsakademin

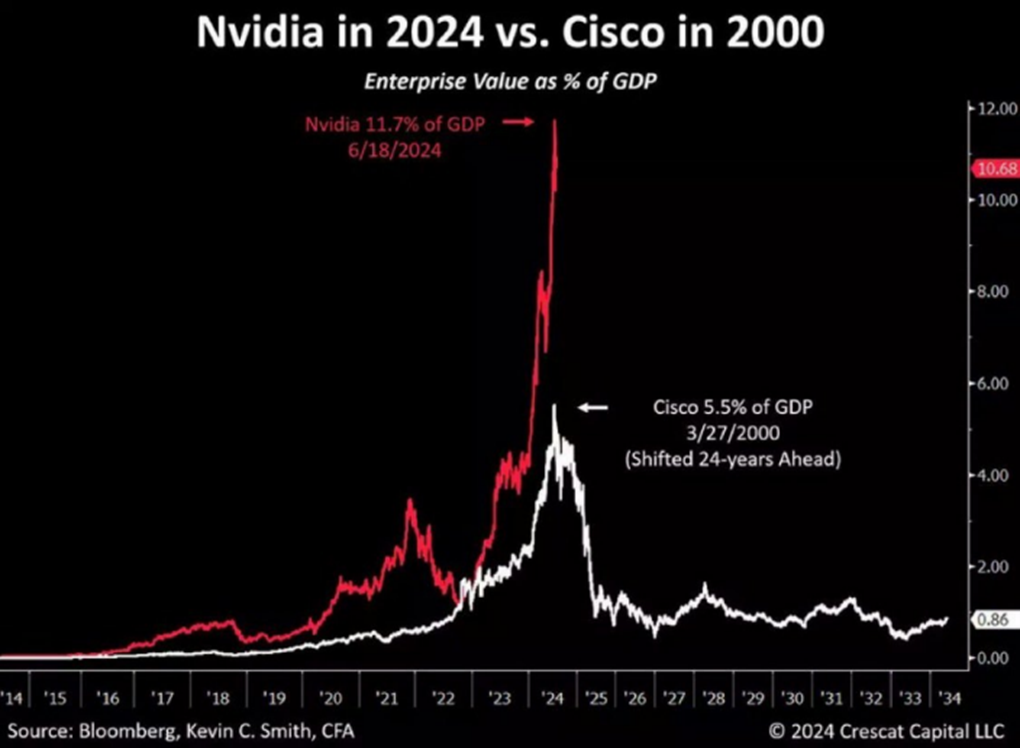

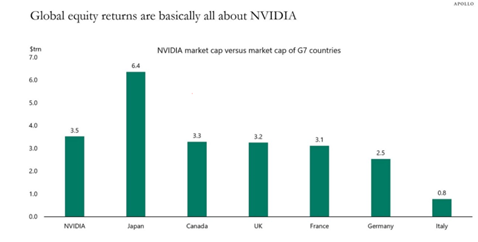

Nvidia is far from our focus, but we note that the world's most important stock continues its unprecedented success. 31 years after the company was founded, the market capitalization is now around 12% of US GDP. It's hard to take in actually.

Source: Crescat Capital

Below you can see Nvidia's market capitalization compared to the GDP of the G7 countries.

Source: Apollo

UN Secretary General António Guterres last week had astoundingly bad judgment and went to Kazan to be received by Vladimir Putin who hosted the BRIC summit. Shame!

Source: X

In conclusion, we cannot resist to include an unusual press release from the now bankrupt real estate company Oscar Properties. We have never had any interest in the company, but the CEO's words are worth reading. Unfortunately, there is not an English version of this, but for our English-speaking readers, the undersigned can assist if there is interest. https://mfn.se/a/oscar-properties-holding/pm-idag-forsattes-oscar-properties-holding-ab-op-i-konkurs-av-stockholms-tingsratt

Portfolio Companies

Normally, reporting periods tend to be good for the fund. This time: however, we have had more misses than beats so far. The "mistakes” are company-specific and we have not changed our analysis process for several years - which has been successful over time. We therefore continue as usual and look ahead. In addition, it is worth noting that several of the companies we owned prior to the report release have had positive share price developments prior. If a report then comes out that is weaker than expected, the price reactions are often large. Often too big. In several cases, we have taken advantage of the opportunities provided by the report reactions to increase or decrease our positions. Having said that, many reports remain for November before we conclude this reporting period completely.

Volution

In October, Volution released its financial results for the fiscal year ending in July. As Volution had already released preliminary figures for the year, it was the outlook that was the most interesting part of the report. On that point, management sounded cautiously optimistic. So far in the new fiscal year, Volution is showing organic growth. Some markets are showing signs of recovery (the Nordics) and others are at least not getting worse (Germany). The balance sheet is in good shape, even after the large acquisition that we wrote about in our previous monthly newsletter, which leaves room for further acquisitions.

Volution shares were in positive territory for a long time in October, but by the end of the month, the stock had fallen 6%, partly due to more insider selling and partly due to a generally weak stock market. For 2024, the stock has risen by 33%.

Lindab

Lindab's report for the third quarter was disappointing. Operating profit was around 13% lower than expected. This surprised us as we thought that the tone of voice from the management had been positive before the release of the report. In order to get back to 10% operating margin, Lindab has introduced cost-saving programs in the Ventilation Systems segment, while at the same time taking structural measures in the Profile Systems segment (sale/closure of certain loss-making units).

We have owned Lindab since 2019 and have seen the occasional report bump in the past and are not worried about profitability getting back on track in 2025. In addition, we hope for a return to organic growth sometime next year, while the company will continue to acquire at low multiples at a high rate. If we get our estimates right, the operating profit will grow by around 50% from 2024 to 2026 and for this you pay EV/EBIT 12x 2026e on our estimates. We find that attractive.

The stock fell a whopping 21% in October and has risen 12% in 2024. We took advantage of the situation and increased our position significantly.

Smith & Nephew / Bureau Veritas

We have had a couple of monitoring positions in the British healthcare company Smith & Nephew and in the French Bureau Veritas which both reported during the month. Bureau Veritas beat expectations while Smith & Nephew lowered its guidance for the full year. We have retained Bureau Veritas and sold our holding in Smith & Nephew.

Campari

Campari delivered a weak Q3 report where they also lowered expectations for the last quarter of the year. A more challenging macro-climate than expected was mentioned and bad weather in several markets. Among other things, a hurricane in Jamaica and a lot of rain in Italy during September (it had not rained so much in the Milan area for 250 years). They also flagged that the recovery in 2025 will take place gradually and it is likely that it will only be in the second half of the year that they will be back with strong growth figures. The report was undoubtedly disappointing for us and for others.

In addition, it is our opinion that communication to the market in recent months has been, to say the least, deficient. The stock came under a lot of pressure and fell by 18% on the day of the report. Uncertainty has of course increased after an event like this, but with a current market capitalization of a low 7.6 billion euros, you now get one of the spirits world's most attractive portfolios with Aperol and Campari as the biggest and most valuable brands.

Bonesupport

Bonesupport continues to spoil us with brilliant reports. Organically, the company grew 54% (adjusted for currency) with the big driver continuing to be Cerament G. Sequential growth accelerated in the quarter and we believe it has to do with more doctors becoming familiar with the product. At the same time, it takes approximately 6 months for orthopedists to evaluate complete results. The explanation then becomes that existing doctors buy more at the same time as new orthopedists are trained and start using the product. The company mentioned on the conference call that to date it has trained approximately 1,000 orthopedists out of approximately 20,000 available in the United States. In other words, there is still considerable room for growth, in the US alone.

During October, Balder's main owner, Erik Selin, also bought around 60% of the largest owner, Healthcap's, shareholding. In our opinion, it is an optimal transaction where Healthcap after 18 years of ownership, frees up liquidity. At the same time, Erik Selin, with his long-term perspective and track record, becomes the largest owner in Bonesupport and now controls roughly 9% of the company. We agree with Erik in his comment "I think it's the beginning of the beginning for Bonesupport". The stock rose almost 10% during October and has thus risen 78% this year – after rising 134% in 2023 and 83% in 2022. Not bad.

Cargotec

Cargotec continued its delivery of good reports. The third quarterly report was better in terms of order intake, sales and operating profit. The stock rose 9% on the day of the report, which was in line with how much better the company performed compared to expectations.

Exactly one year ago, we wrote in the monthly newsletter that the valuation was so low that we didn't think it was true. The share was then at 36 euros and at the time of writing, the share is trading at 55.5 euros. It is an increase of 54, but since then they have received 2.1 euros in dividends as well as Kalmar which was distributed, which is today worth 32 euros per share. Kalmar in our books therefore has a purchase value of zero! The total return amounts to 152% in one year, so with hindsight it wasn't so strange that we thought it was too good to be true. Cargotec is still undergoing major changes which we do not think the market has fully recognized. The stock rose 6% in October. Below is one year's price development adjusted for the dividend of Kalmar.

Source: Bloomberg

SLP

Our little "Rolex" SLP continues to deliver exactly as we expect. The result came in a few percent better than expected. The required return on capital has been unchanged for 16 months. The last time SLP raised the yield requirement to the level of 5.9%, the 5-year swap was traded at 3.7%. Today, the swap is traded at 2.3% and the yield requirement is unchanged. In other words, it is only a matter of time before yield requirements start coming down, which will fuel property companies, not least the companies that sit on high-yielding properties such as SLP. The stock rose 3% during the month, while the Swedish real estate index fell by 10.7%. For the full year, the share has risen by 16%.

Biotage

Biotage had the strangest report reaction of the reporting period. The stock has fallen 10% since the report despite adjusted operating profit being in line with expectations. We have taken advantage of the situation and bought more shares.

A few weeks ago, forecasts surfaced that Biotage will be excluded from a sector index in Stockholm at the end of November. When we study the volume traded around the report in combination with the fact that the stock price fell in a way that we believe could not be explained by fundamental causes, it leads us to believe that passive capital preceded and sold shares ahead of this possible event. The calculation of how many shares will be traded on the last of November coincides well with the unusually high turnover in the share around the reporting date. Did you know that there are more indices in the world than stocks?

Biotage grew 12% organically despite continued headwinds in China. This should be compared to other life science tools companies that have had growth of -4 to 0%. The development is mainly driven by the "Large molecules" segment, which grew 65% organically. We also see that the "Small molecules" segment seems to have bottomed out and is growing sequentially, which is in line with what peers have reported. We look forward to what the company can do with tailwinds from the sector next year. The stock fell 14% during the month but has risen 20% this year.

Scandic Hotel

Scandic delivered a report that was approximately five percent worse than the expected adjusted operating profit. However, the focus was on the new strategy for the company's capital allocation which was announced the night before. Scandic, which a few years ago was under severe financial pressure due to the pandemic is now starting to transfer significant capital to shareholders. In addition to regular dividends, the company intends to give back at least SEK 1.2 billion (SEK 5.50 per share) over the next two years. This is through extra dividends and buybacks.

The stock retreated on the day of the report. We think the main explanation for that was that the capital allocated to buybacks was slightly less than expected. There was also some confusion around the debt target which was lowered from 2-3x EBITDA to 1x. We understand why they lower the debt target, given the period they have been in. Worth noting is that we believe there will be more capital transfers than the 1.2 billion announced. The company's cash flow is extremely strong, and it is currently debt-free.

With our approach based on the company's fundamental variables, we think a more reasonable valuation is around SEK 100. When Scandic was bought by Hilton in 2001, the valuation was 8x EBITDA. Now the company is debt-free and in better shape than ever. Scandic trades on our estimates of around 5.5x and 4.5x EV/EBITDA in 2025e and 2026e, respectively. That's really low.

Summary

As this is being read, the world has found out that Trump will be the new President of the United States. This is probably better for the American stock market than it is for Sweden and Europe. Consider that Donald Trump, more or less supported a coup d'état on January 6, 2021. It is still incomprehensible.

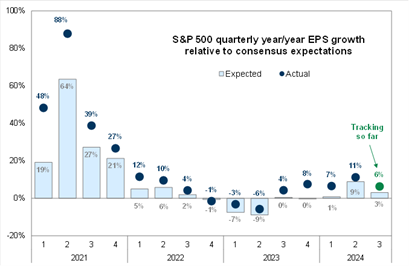

The reporting season will soon be completed and despite higher stock-specific volatility, it has been slightly better than expected at the broad index level, see image below. In Europe, it has been clear that the automobile sector has very big problems with a delayed roll-out of electric vehicles at the same time as cheap EVs are pouring in from China. Basically, all companies with exposure to China have also reported very low activity and with few signs of improvement. It remains to be seen whether the Communist Party's large stimulus package will begin to have any effect on the Chinese consumer.

Source: Goldman Sachs

Another theme in Europe, and where Sweden stands out for being at the forefront of development, is housing construction, which is slowly coming to life and, in addition, a renovation sector that’s helping. Increasing order books at several companies in this segment have been a positive surprise and have been rewarded with, in some cases, sharply rising share prices.

Another sector that feels very solid is the marine sector, where shipyards report on filled order books for the full four years ahead. This has benefited our holding in Swiss Accelleron which since we bought our first shares two years ago has risen by over 200%. One of the fund's smaller holdings is Kalmar, which we received when Cargotec distributed Kalmar on the 1st of July. It is also a company that indirectly benefits from this development. Kalmar also reported on November 1st and rose by 14% on a very strong report including better order intake. More on that next month.

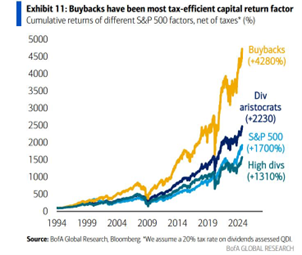

We continue to discuss with our companies about, among other things, capital allocation (our capital). In many cases, we argue for more and bigger buybacks due to low valuation and strong balance sheet. Scandic Hotel is a perfect example. Our view is that something happened this year as European companies are more responsive compared to before and this year more buybacks are carried out than ever before. The picture below speaks for itself.

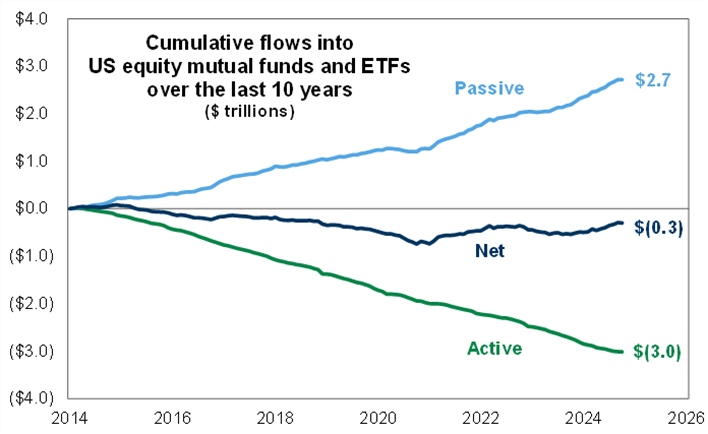

The trend of flows to active and passive managers is clear. We maintain that it should be more interesting for a manager and its clients to study company fundamentals and valuation compared to capital allocation depending on how many points a company weighs in a certain index. But of course, we could be wrong.

Source: Goldman Sachs

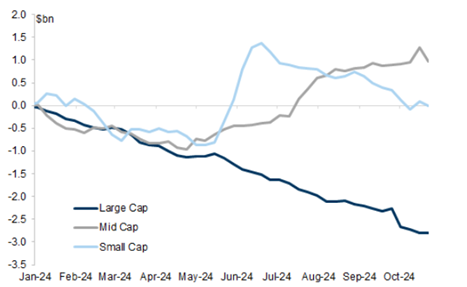

The picture below refers to European flows and it can be seen that inflows to small caps have (again) decreased in recent months. However, the development is significantly better than for large caps.

Source: Goldman Sachs

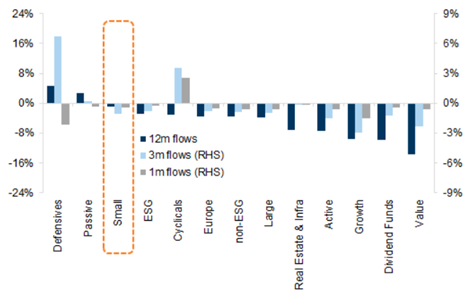

Flows to different types of sectors and strategies are shown here. Defensive and cyclical stocks are clear winners over the past three months. A bit contradictory it may seem.

Source: Goldman Sachs

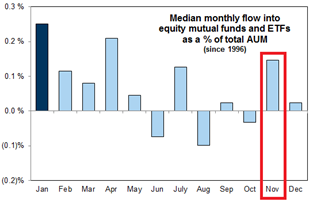

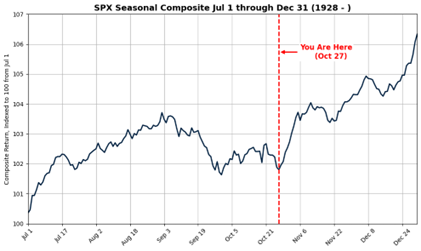

We are now rolling into the historically strongest period where inflows are usually significant, and the start of buyback programs are activated after the reporting period.

Source: Goldman Sachs

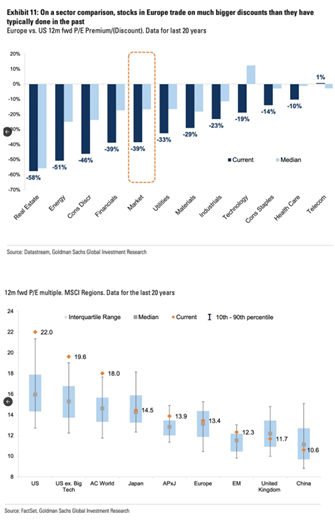

That the discount is at a historic record level between American and European shares is not news. But the fact that sectors such as real estate and oil, whose conditions and assets basically look the same on each side of the Atlantic, are traded at over 50% discount is, to say the least, remarkable.

Source: Datastream, Goldman Sachs Global Investment Research

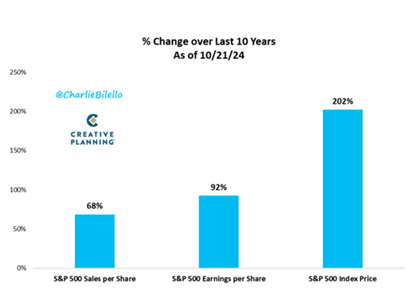

The multiple expansion in the US over the past 10 years accounts for about half of the past 10 years' price rise. Reasonably, the upside in terms of further expansion should be limited.

Source: CharlieBilello

The profit yield is lower than the yield on the US 10-year bond.

Source: Holger Zschaepitz, Bloomberg

European small caps are now traded at a higher discount to large caps than during the financial crisis. We guess it's due to passive capital dominating nowadays and not caring about valuations. Passive capital typically does not invest in smaller companies either.

Source: Bloomberg

Smaller companies tend to have a stronger performance when the purchase index exceeds 50. We should reach that level soon.

Source: Goldman Sachs

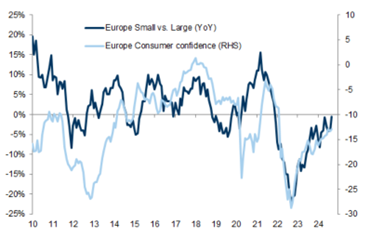

Smaller companies also tend to develop stronger than larger companies when consumer confidence is strengthened. This is also something that should happen within a few months.

Source: Goldman Sachs

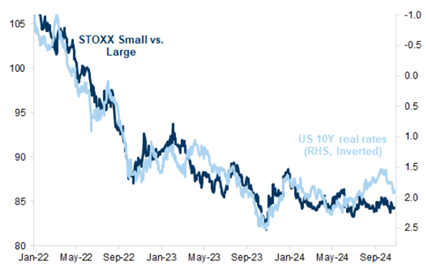

Smaller companies have historically developed stronger when interest rates fall and vice versa. The light blue line shows the US inverted 10-year yield that broke small cap valuations in 2022. There are good conditions for small caps to retaliate properly when interest rates are likely to fall in the future.

Source: Goldman Sachs

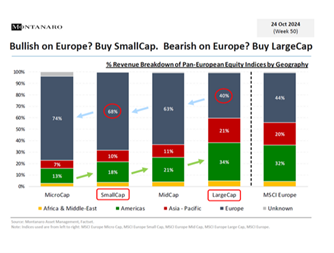

In the event of the introduction of new tariffs from the USA, European companies with a higher exposure to the USA will likely develop worse than companies with a higher European exposure, i.e. small companies.

Source: Montanaro Asset Management, Factset

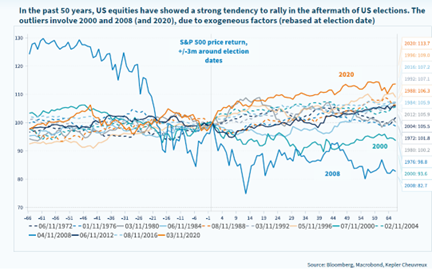

Finally, with the US election behind us, we are almost guaranteed a week of higher volatility than usual. Our guess is that we will, swiftly, be back on track again. See image below that shows the development of US equities after a presidential election.

We have a historical pattern that speaks a clear language. Since 1928, the US stock market has returned an average of 6.25 percent from the end of October to the end of the year. The corresponding return for smaller companies since 1979 is 7.99 percent.

Source: Goldman Sachs

With several adjustments completed where we bought shares at low levels, we are, despite a few weaker weeks, optimistic about the end of the year. We will now spend the remainder of the year visiting and analyzing companies.

Many thanks for your interest!

Mikael & Team

Malmö, November 7th 2024

IMPORTANT INFORMATION. This is a marketing communication. Before making any final investment decisions, please refer to the prospectus of Coeli SICAV II, its Annual Report, and the KID of the relevant Sub-Fund. Relevant information documents are available in English at coeli.com. A summary of investor rights will be available at https://coeli.com/financial-and-legal-information/.

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested. Please note that the management company of the fund may decide to terminate the arrangements made for the marketing of the fund in one or multiple jurisdictions in which there exists arrangements for marketing.