Monthly Newsletter Coeli European – January 2025

This material is marketing communication.

Note that the information below describes the share class (I SEK), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class’ return. The information below regarding returns therefore differs from the returns in other share classes.

Before making any final investment decisions, please read the prospectus, its Annual Report, and the KID of the relevant Sub-Fund here.

January Performance

The fund’s value increased by 1.1% in January (share class I SEK), while the benchmark increased by 5.2%. Since the change of the fund’s strategy at the beginning of September, 2023, the fund’s value has increased by 22.7% compared to an increase of the benchmark by 15.2%.

Source: Coeli European

* Adjusted for spin-off of Rejuveron

** Includes September 1 (strategy change to long-only implemented September 4 2023)

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

Equity Markets / Macro Enviroment

2025 kicked off with stock market optimism and extensive news flow about macro, politics and Chinese technology successes. Despite an explicit very low level of interest in Europe from a global investment perspective, it was Europe that took the lead with significant increases particularly in the broad stock indices. For example, the Eurostoxx 50 rose by 8% in January compared to the S&P500, which rose by 2.6%. The German DAX, which rose by 19 and 20% respectively in 2023 and 2024, rose further in January by a full 9% and was thus one of the world's best stock markets. As has been pointed out many times before, the stock market does not reflect the underlying economy.

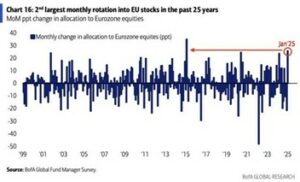

The gains were fuelled by substantial inflows to European stock markets. Only once before in the past 25 years have inflows to Europe been greater in a single month. This is of course encouraging and stands in stark contrast to the doomsday headlines we have seen in recent months about Europe's dysfunctional stock markets. As is often the case on occasions like these, and so in January, smaller companies could not keep up when capital was needed to be put to work quickly. The MSCI European Small Cap index rose by 3.9% in January.

Source: BofA Global Fund Manager Survey

Another “trend” that has been clear at the beginning of the year is that last year’s losers are now winners. Unfortunately, the fund felt this in January with an increase of only 1.1%. We are of course unhappy about that, but we have been around for long enough to know that when you work with a concentrated portfolio, this sometimes happens. The fund’s three worst contributors in January were all strong contributors in 2024 and they were Bonesupport, Biotage and Lindab. January’s best contributors were 4imprint Group, Scandic and Diploma. More about that in the portfolio company section.

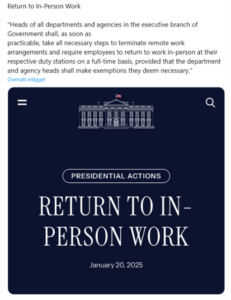

As of January 20th, Donald Trump is the 47th president of the United States and one must be impressed by the speed at which he works. It was interesting to see how many business leaders were in the rotunda, under the dome of the Capitol, when he placed his hand on the Bible and swore the presidential oath.

On the same day, new instructions were issued to all employees in the departments to cease working from home. No more yoga during working hours is the conclusion.

Source: X

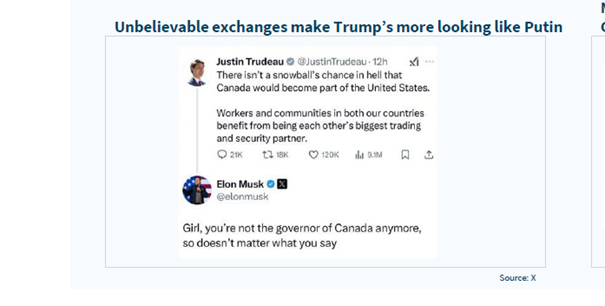

Elon Musk certainly had a hand in the game and was overall in an excellent mood.

Source: X

The fact that Elon Musk is interfering and trying to influence the political development of various countries must be considered deeply worrying. There has been a lot of focus on Germany and the support for the AfD lately, but there are other examples as well.

Source: X

Politically correct ESG funds that resisted investments in the defense industry despite a war of aggression by Russia in Europe probably have reason to wonder whether Tesla matches their investment criteria.

Most notable, however, was Trump's statement regarding Greenland, where military intervention could not be ruled out. As was said by one NATO member to another who is also one of the most loyal members and has been with the alliance since its formation in 1949. Absolutely crazy. In an interview with Fox News, Vice President J.D. Vance calls Denmark a "bad ally that is not doing its job well enough to protect the island".

The Financial Times reported on a disastrous 45-minute phone call between Donald Trump and Danish Prime Minister Mette Frederiksen, which led to Ms. Frederiksen traveling around Europe a few days later and visiting leaders in Germany, France, and London to ensure a common view on the matter. The evening before she left, she invited the Nordic leaders to her home for traditional sandwiches to have a status report.

Source: Instagram

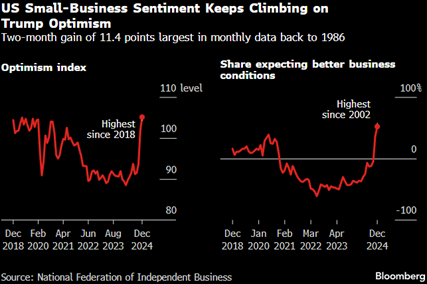

Regardless of all this, optimism among smaller US companies has risen significantly since the US election in November. A meeting with one of our companies before Christmas with significant US exposure confirmed just that. Optimism is rising sharply.

Source: Bloomberg

Bernard Arnault, founder and main owner of LVMH and who was also seen around Donald Trump at his inauguration, praised the new administration's economic policies and criticized Europe's. “I have just returned from the US, and I have witnessed the winds of optimism in that country,” he said. “Coming back to France is a bit like taking a cold shower.”

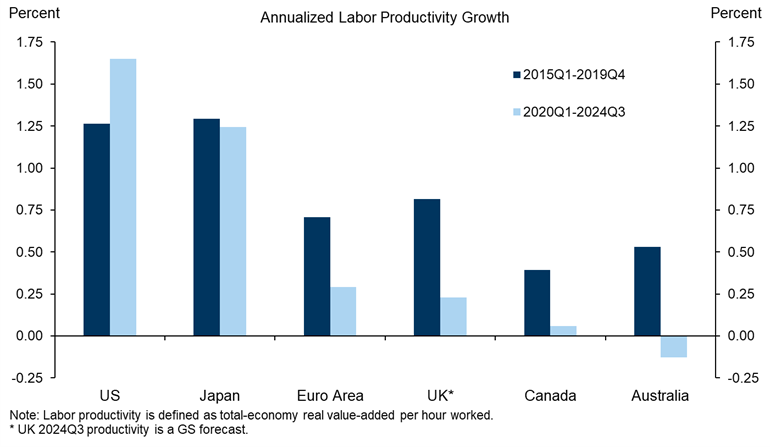

Americans have reason to be optimistic. Study the chart below, which shows productivity growth in different countries and regions. It is mainly in the last five years that the US has raced past the rest of the world in efficiency.

Source: Goldman Sachs

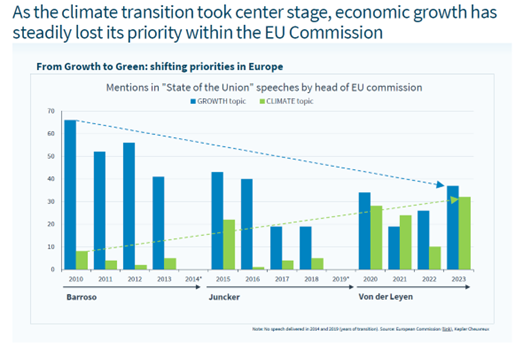

One advantage of the new US administration's progress is that sleepy European politicians and officials finally seem to understand that things are serious now and that the focus must be on economic growth. It is quite obvious that the rest of the world is not impressed with Europe's ambitions in terms of regulations, ESG and politics in general. The picture below is illustrative and clear.

Source: European Commission, Kepler Cheuvreux

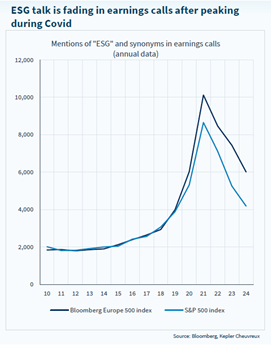

There is less talk about ESG now compared to a few years ago, both among European and American companies.

Source: Bloomberg, Kepler Cheuvreux

If you have politicians who, in many cases, have never been in business and who also pursue ideological politics, it rarely ends well. The positive thing is that in a very short time, many points have come up on the political agenda in Europe about a more growth-oriented policy with fewer and less extensive regulations such as GDPR and CSRD.

On the last weekend in January, the world was made aware of a Chinese AI company called DeepSeek, which claimed that, with significantly less computing power, it could compete with companies like ChatGPT and at significantly lower cost. We are far from experts in the subject, but it can be considered a major step forward in the democratization process as more people will be able to afford to invest and use AI, which should then have a positive impact on world GDP growth in the coming years.

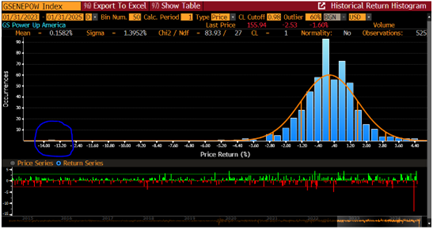

The world's most important stock, Nvidia, fell by 18% on Monday, January 27, which in value corresponded to the entire GDP of Sweden. Below is a picture showing the Goldman Sachs “Power Index Basket” which fell by a whopping 13.5% that day. The picture shows the distribution of daily returns over the past two years and on the far left you can see January 27. When the month ended, the basket still closed up by 7.7%.

Source: Goldman Sachs

Source: X

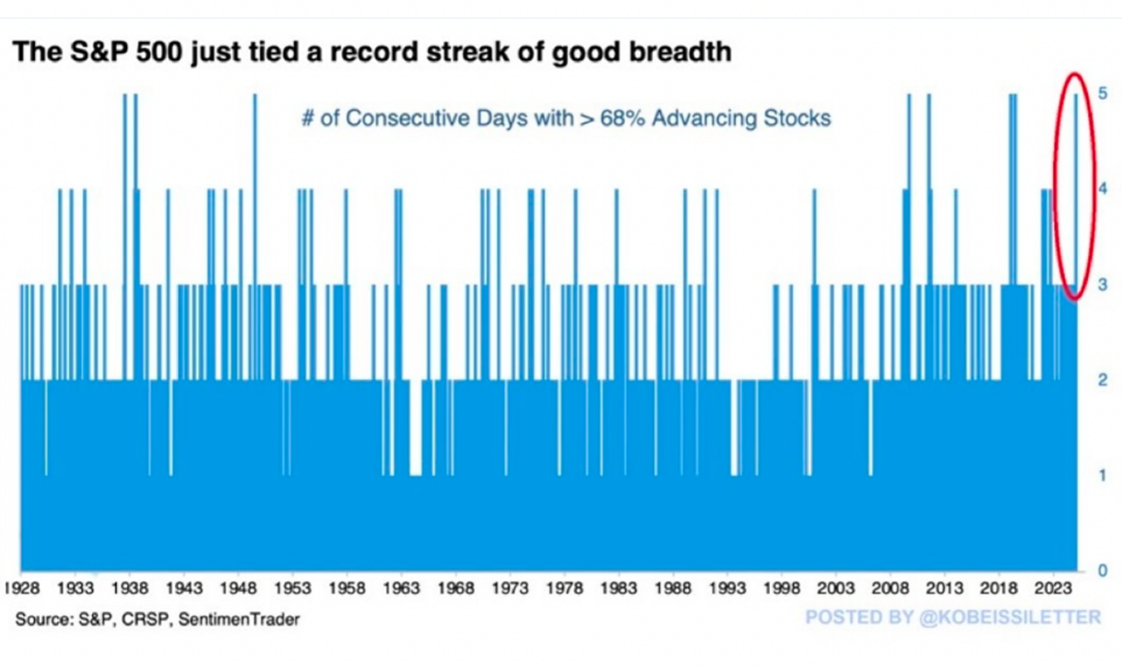

On January 27th, the S&P500 fell by 1.5% while more than 300 stocks in the index rose, which should be seen as a plain positive. This has never happened before since the index was constructed in 1957. The breadth of the market has thus increased, which is a clear and a strong hallmark of a positive market.

The image below shows the history of the breadth of the market since 1928. For five days in a row, more than 68% of the stocks in the index rose, which has only happened a handful of times in the last 97 years.

Source: S&P, CRSP, SentimentTrader

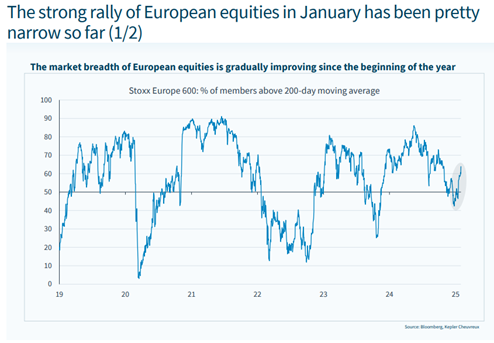

The strong start in Europe also led to increasing market breadth.

Source: Bloomberg, Kepler Cheuvreux

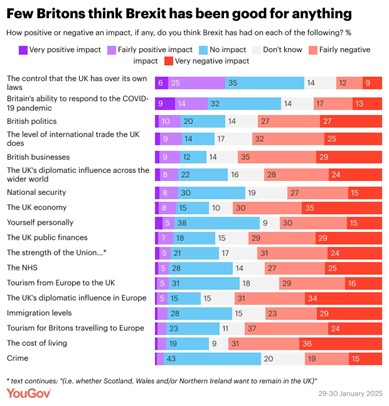

YouGov, a British-based global public opinion and data company, published the following data at the end of January. The conclusion is that Brexit is a total failure and that many people now regret it. A sad chapter in European history.

Source: YouGov

The fact that the Social Democrats at the end of the month demanded that the government develop an urgent action plan to address gang crime must still be considered a new high in terms of audacity and hope that the population has a very limited memory.

Source: Kluddniklas

Portfolio companies

In terms of performance, the fund had a weaker period in January, as mentioned. In terms of actual, operationally impacting company news, however, we would rather say that we saw predominantly positive things: 4imprint and Diploma came out with good reports. At the same time, weaker news came out from Lindab. Bonesupport has been in the spotlight in a way that is negative to the stock market. This is elaborated on below.

4imprint

The promotional gift company reported preliminary results that were a couple of percent better than the market had expected. Last year, 4imprint struggled with sluggish markets, but as the year is summed up, it has still grown its sales and taken market share. It has also improved its profitability. The feeling is that 2025 will be a better year for the company, which has historically grown by more than 10% per year with a return on capital employed of over 200%.

The share was rewarded with a relief rally in January and rose by a whopping 24%. We think the company deserves a reassessment, partly because profitability has been structurally raised from around 6–7% to 10–11%.

Rotork

A relatively new holding for the fund is the British industrial company Rotork. We have built a medium-sized position during the autumn and early 2025.

The company mainly manufactures and sells actuators that convert a signal into a physical movement, such as opening various types of valves. Rotork's strength is in electric actuators, a concentrated market that is mainly shared with its main German competitor AUMA. Rotork has its heritage in the oil and gas industry, which still accounts for just under half of its turnover. The market capitalisation is close to £3 billion.

Rotork is one of the finer industrial companies on the UK stock exchange. Historically, organic growth has been around 6% per year. Margins are likely to exceed 23% for the full year 2024, while the return on capital employed is expected to exceed 50%.

The investment outlook in the oil sector may not look very bright either in the short or long term. Rotork is, however, benefiting from ongoing electrification in the sector. This is being done, among other things, to reduce methane emissions, where Rotork's electric actuators have an important role to play. As for natural gas, the investment rate is higher, partly as a direct consequence of Russia's invasion of Ukraine, and partly because it is seen as a "less bad" alternative to oil while waiting for better energy sources to be developed. A calculation we recently saw estimates that the supply of natural gas will increase by 6% per year until 2030.

In addition to these growth drivers, Rotork has exposure to several different growth markets, for example in water infrastructure. Much of the Western world's water infrastructure is very old and needs to be upgraded. This benefits Rotork, which has its actuators installed in many water works around the world. (We also think we can see that water infrastructure is an increasingly important theme among many companies from all kinds of industries.)

We believe that Rotork can grow at a faster pace than it has done historically. After three weak years in 2019–2021 with negative growth, 2022–2024 have been clearly more positive years with growth exceeding 8% per year. After following the company for several years, we now believe that the drivers of growth are clearer than in a long time, while the valuation is at historically low levels. If our thesis is correct, we believe that we can achieve a return of approximately 15% per year.

In January, the share rose by 11% after several analysts recommended the share as a buy.

Diploma

The British serial acquirer delivered another strong report during the month. Although it maintained its guidance for the 2025 financial year (ending in September), organic growth of 7% was higher than the 6% that the market estimates for the full year. This was enough for the share to rise by 5% on the day of the report.

Diploma's valuation is hardly low, but quality also tends to come at a cost. The forward-looking EV/EBIT multiple of 21x almost seems cheap relative to many Swedish serial acquirers. That said, we believe that a somewhat larger acquisition is needed for the share to work in 2025. Last year the share rose by 19%. In January the share rose by 7%.

Lindab

The month's "operational blunder" came from Lindab, which issued a profit warning for the fourth quarter of 2024. The company referred to the fact that December was worse than expected (and thus we interpret this as October and November being in line with expectations). Presumably due to the longer Christmas break this year than last year.

As we interpret the profit warning, however, it was Lindab's Eastern European business within Profile Systems in particular that performed poorly. This is a business that will be closed down or sold in 2025. In the fourth quarter, we expect to find out how large the negative profitability contribution was from units that will soon no longer be part of Lindab. Had these units been reported as discontinued operations, perhaps the profit warning would not have been necessary?

With the Eastern European Profile Systems business soon out of the picture, and with the help of the ongoing program to reduce costs within Ventilation Systems, we believe that the conditions for better profitability in 2025 look good. This is especially true if volumes return, perhaps as early as the second half of the year?

We are now seeing that many construction-related companies with exposure to housing are starting to see growth again (see, for example, Inwido, BHG, Byggmax). The housing segment is usually the first to benefit from the recovery of a construction boom. The commercial segment will then follow. After a couple of years of high interest costs, many property companies are probably sitting on a “maintenance debt” that Lindab can help pay off with its ventilation products.

We will probably return to Lindab after the fourth quarter report is released. The share fell by 13% in January after being down 22% at its trough.

Biotage

Biotage was one of the fund's biggest losers in January. It emerged that the company's new CEO, Frederic Vanderhaegen, has begun to make his mark on the company with a greater focus on integrating the previous acquisition Astrea into the "old" Biotage, which we think is positive. From what we understand, there are a few former employees at Astrea who do not like this approach and have therefore chosen to leave the company. Turnover is natural in times of change, but the market does not like uncertainty and the share came under pressure.

Fundamentally, Biotage is a super healthy company that, according to our estimates, is valued at 15x EV/EBITDA 2026e. The underlying market seems to be recovering according to our expectations from last year. German Sartorius and Swiss Lonza have also released good reports, as have American Danaher and Thermo Fisher. Danaher guided for a weaker Q1 than expected, but the direction is clear with increased activity in the sector. Biotage shares fell 12% in January.

Bonesupport

It was a turbulent month for the Bonesupport stock, which began by reaching new highs of just over 400 kronor, then lost ground and closed at –10% for the month. It all started with a short seller flagging a position of more than 0.5% at the same time as a “short seller report” from The Analyst circulated in the market.

Later in the month, a fatality was reported in which Cerament BVF had been used. The investigation into the death is not complete, but there is basically no doubt that Cerament was not the cause of the tragic death. It was a case of a medical error where the doctor used the product incorrectly with the wrong indication and on a patient who should not receive the product at all (under 9 years old).

After a rise of 728% in three years, the share easily becomes the subject of critical scrutiny. As we see it, the basic story has not changed.

Scandic

The Scandic share has started the year brilliantly with an increase of 13%. In January, positive RevPAR data was released that likely exceeded market expectations and thus contributed to the price increase. At the same time, Scandic is doing everything right with its capital allocation. The company is consistently and methodically buying back shares in the market and, since the announcement of the buyback in December, has bought back just under 2 million shares (0.5% of the outstanding shares) for just under SEK 130 million at an average price of SEK 68. This can be compared to the month's closing price of SEK 77.

After meeting the German real estate company, Aroundtown, a few weeks ago, it is clear that demand for their hotel properties is very high. It is an asset class that is in demand by investors, and we are also hearing about a new large fund that has been set up in Europe that will invest exclusively in hotel properties.

Cargotec

Finnish Cargotec had a weak month without any particular news. We have taken advantage of that weakness and bought more shares in what we see as one of the finer Nordic industrial companies at a valuation of 12x EV/EBIT 2025e. The company is early in the cycle and no major recovery is expected. If we start to see early signs that the cycle is improving, Cargotec shares will perform strongly. The share fell by 6% in January.

Vallourec

For some time now, we have been building a mid-sized position in French Vallourec. The company manufactures seamless steel pipes that are used in the energy, industrial and construction sectors, among other things. Vallourec has been an “uninvestable” stock for many years. And for good reason. 2023 was the first year the company had positive cash flow in about 10 years. In 2025, the company will start distributing money for the first time in ages.

After being led by a French politician for 10 years, the company was on the verge of bankruptcy in 2021. The investment fund Apollo, which had lent capital to the company, converted its debt into shares, obtained 30% of the company and thus took charge of the company. The previous management had to leave the company, and a new CEO came in in the form of Philippe Guillemot, who has no fewer than seven reconstructions on his CV. His assignment from Apollo was to “clean up” the company thoroughly, both organizationally and financially. He has done this in a creditable manner. Divisions that did not deliver results were closed, which led to the closure of operations in Europe and investments in Brazil. The company also improved its working capital, which has contributed to strong cash flow.

The share is valued at less than 9x and 8x free cash flow for 2025e and 2026e, respectively, and on our estimates. The dividend yield amounts to a whopping 9%. These are far too low multiples when the return on capital employed is at the same time above 20%. Vallourec is also debt-free. On top of that, we have a management that is very focused on creating shareholder value (their compensation is based on the share price). As a free ride, ArcelorMittal bought 28% of the company (Apollo's shares) in August 2024. We believe that they may be tempted to buy the entire company in the long term. The share rose 12% in January.

SLP

SLP continues to deliver according to plan. At the beginning of the year, it announced the purchase of logistics properties worth SEK 1.4 billion. The deal is the company's largest to date. The largest tenant is PostNord and the properties have existing and long-term contracts. At the same time, the company sees the opportunity for refinement potential over time, completely in line with their strategy. The share rose just over 4% in January.

Summary

At the time of writing during the first weekend of February, the world is on edge after Trump, on Friday evening on the last day of the month, imposed tariffs on goods from Mexico, Canada and China. It is impossible to predict what his next move will be, but he has just started a trade war between the US and Canada. An emotional Justin Trudeau (the Prime Minister of Canada) addressed his nation while they countered and implemented tariffs on American goods.

After listening to Trump at the World Economic Forum in Davos two weeks ago, what is happening now is far from unexpected, but it is sad and will undoubtedly affect the American consumer as well. The US stock market fell 1.5% after the news and it is something that Trump listens to after all. “Tariffs are the most beautiful words to me.”

Source: X

The coming months will be unusually interesting, and we will focus on following our companies and at the same time look for new investment opportunities. The analytical hub is currently firing on all cylinders and in January we held 35 company meetings in total, partly because we participated in conferences in both Copenhagen and Frankfurt. The simplified message from the companies is that given the conditions, things are going well, while many hope and expect an acceleration of economic activity in Europe after the summer following three years of having been trudging around in a bit of a vacuum.

Apart from Lindab, the reporting season has started well for the fund with significant positive performance post reporting for both 4imprint and Diploma, which are large core holdings. As you probably know, the fund owns a minor position in LVMH, which had risen a full 18% prior to its report in January and where we had reduced our position going into the report due to the strong development. Sales were better than expected, but profitability was worse, and the share fell by 5% afterwards. Since December 1st and up until the report, LVMH shares had risen by a whopping 30%(!) and it once again became Europe's largest company by market capitalization. For the stock market as a whole, 20% of the companies in the Stoxx600 have reported and the reports have generally come in better than expected.

The ECB and the Riksbank (Swedish Central Bank) continue to try to kick-start the economy with interest rate cuts. In January, both central banks lowered interest rates further to 2.75 and 2.25%, respectively. The Fed kept its policy rate unchanged, something that was not appreciated by Trump. “The Fed has done a terrible job.” Trump promised in his usual and unabashed manner that he himself would bring down both interest rates and inflation. “If the Fed had spent less time on DEI (policies for equality and representation), gender ideology, green energy and fake climate change, inflation would never have been a problem,” Trump wrote on social media. The odds of Powell being fired as central bank governor within a year feels slim.

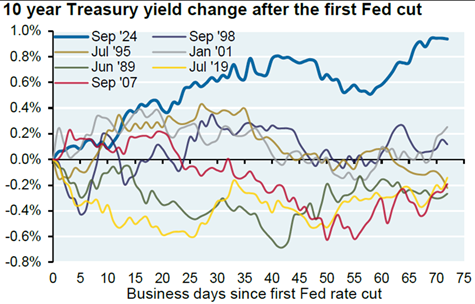

It is the picture below that makes Trump particularly upset. Despite interest rate cuts since September last year, the US 10-year yield continues to rise. One tip for the administration is to look for the answer to why this is. A further and humble comment is that tariffs will likely not cause interest rates to fall.

Source: Goldman Sachs

Talking of interest rate cuts, things are now turning in earnest in Sweden, as was evident in the data presented in January. Figures were consistently strong for the Swedish economy. Export orders are recovering, retail sales grew by four percent in December, and households are no longer worried about the labor market, including the badly battered construction sector.

Source: Macrobond & Nordea

Despite many challenges, the European stock market (Stoxx 600) has clearly dislodged from an old trading pattern at the beginning of the year, see the picture below. As we mentioned last month, when expectations are so depressed at the same time as valuations are historically low, this is usually the case. It remains to be seen how the coming months will turn out with a heated American administration that, after being in office for just over 10 days, is now fighting on several fronts against the rest of the world in a newly started and oncoming trade war.

.

Source: Bloomberg

To put the above picture into a more long-term perspective, despite significant increases in recent years, the Euro Stoxx 50 has not yet reached its highest level from 2000, which says a lot (however, the Stoxx 600 has).

Source: Bloomberg

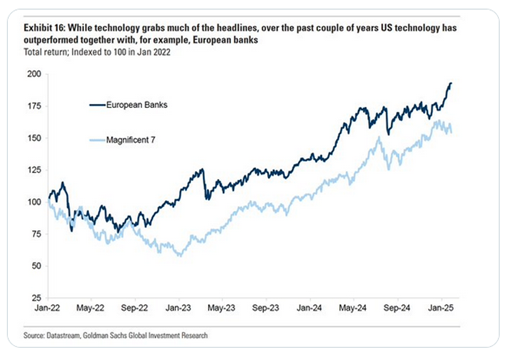

European banks have been experiencing the best conditions in decades for a few years now and it is also the sector in Europe that has had the strongest price development for four years in a row. In the last three years, they have developed stronger than Mag7 in the USA. The fund owned Commerzbank from November 2022 until last autumn when we (incorrectly) took profit. Since the beginning of the year, we have instead become owners of the Austrian bank Bawag.

Source: Datastream, Goldman Sachs Global Investment Research

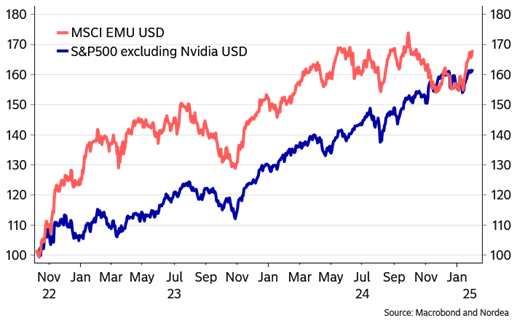

An updated image from last month's newsletter. S&P500 minus Nvidia (“S&P499”) compared to a broad European index measured in the same currency since the market turned up in November 2022. This image says a lot. The narrative about the European stock market compared to the American one is somewhat warp after all. Passive capital positioning probably hasn't thought about the image below (our guess) and at the same time DeepSeek has appeared, which changes a lot of conditions.

Source: Macrobond & Nordea

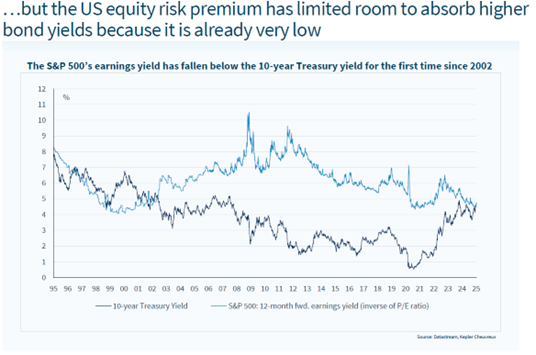

This should get the attention of the American investor. The American stock market offered a negative risk premium in January for the first time since 2002. The 10-year yield thus exceeded the profit you get on average as an American investor.

What happens if the American interest rate rises further? Our guess is that the stock market will come under pressure as there is no buffer left from a shrinking risk premium. In Europe, the risk premium is currently around six to eight percent, so strictly speaking from that perspective, there is no problem.

Source: Datastream, Kepler Cheuvreux

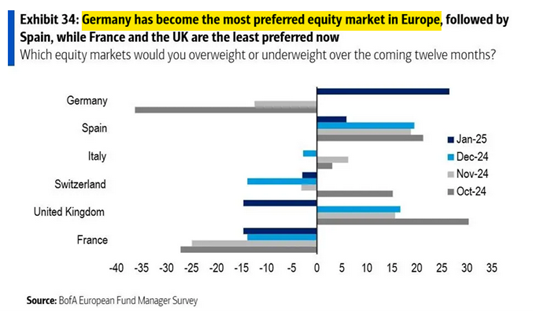

Germany's stock market is red hot! The picture below partly explains why the DAX had such a good start to the stock market year. Also note that Spain as a popular investment market and as a country outperformed the rest of Europe by around three percent in GDP growth in 2024. France at the bottom. Could it be correlated to highly mediocre politicians who, for example, propose a tax on share buybacks? You pull your hair out and wonder how one can be so out of touch with reality.

Source: BofA European Fund Manager Survey

But the poor Germans are still at record lows.

Source: Forschungsgruppe Wahlen: Politbarometer

The German election in a few weeks will be very interesting. It is chaotic to say the least in German politics and we guess that the picture of the year has already been taken, see below when Olaf Scholz (SPD) tries to prevent his coalition partner Annalena Baerbock (The Greens) from leaving the room. The differences between them regarding aid to Ukraine are significant, with the Greens having a much more proactive Ukraine policy than the SPD.

Source: Instagram, John MacDougall

Meanwhile, the far-right AfD in Germany has become a powerhouse, enthusiastically cheered on by Elon Musk in January. There's a lot going on in the world right now!

Source: X

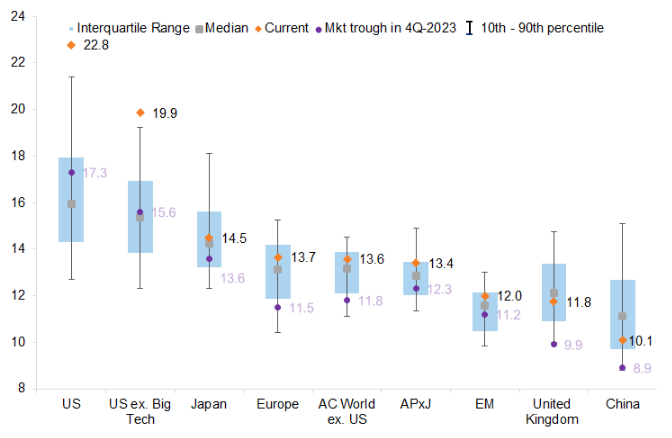

Below is a snapshot of valuations for several different stock markets.

Källa: Goldman Sachs

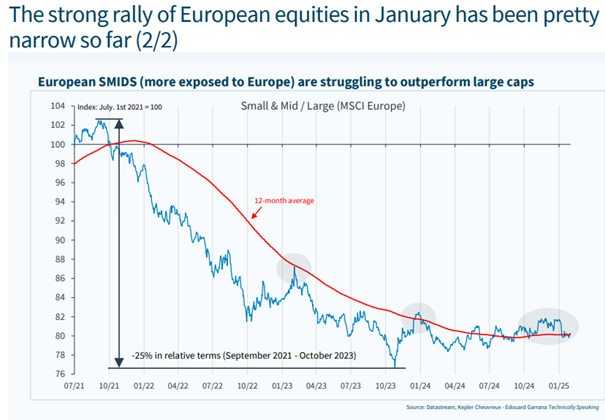

The answer to our question a month ago about whether small companies would pull ahead of large companies this time was no. To be continued.

Source: Kepler Cheuvreux

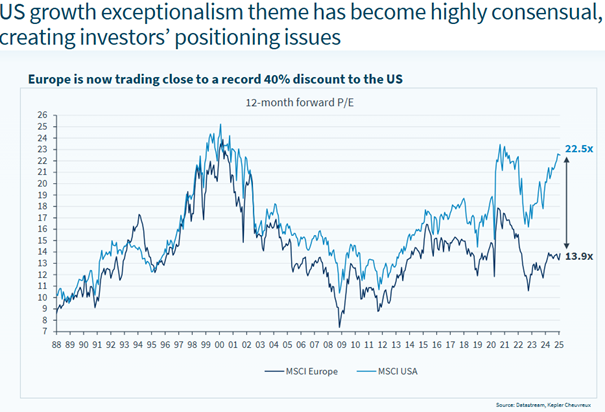

Europe has marginally caught up in the valuation gap with the US at the beginning of the year.

Source: Kepler Cheuvreux

In summary and after an unusually eventful start to the new year, we currently see the game plan as follows:

- Expect a continued deluge of news flow in the coming months from the US administration which creates volatility, both up and down.

- This should reasonably abate as proposals are implemented or eliminated.

- Trade tariffs are only negative, and the world has become less global in a short time.

- If this continues and escalates, it will hit US companies in a second wave as the rest of the world takes joint action against the US.

- Common sense says that reality will not live up to the headlines. Nevertheless, be quick to act, and slow to promise.

- Own companies that have little exposure to US tariffs or that have unique products with strong pricing power. Smaller companies have significantly more domestic exposure, which is positive from a tariff perspective.

- The EU and the UK will be busy repairing historical mistakes, which should result in certain positive contributions to Europe's economies (but it takes time).

- Some of Trump's tariffs are already discounted in European stock prices, but it is unclear how much. Valuations are historically low.

- Very little is likely discounted in US stock prices where valuations are at record levels.

- The stock market has weathered the heavy news flow gallantly so far. Large inflows have provided great support.

- The coming months are historically good months for stocks.

- Donald Trump listens to Wall Street.

- All of the above should, just like last year, be good for active managers.

- In addition, we have reduced some core holdings and taken profits, while some new holdings are being built up.

- February offers nearly 15 quarterly reports for the fund.

To be continued! Thank you for your interest and keep a cool head.

Mikael & Team

Malmö, February 5th, 2025

Source: Kepler Cheuvreux

IMPORTANT INFORMATION. This is a marketing communication. Before making any final investment decisions, please refer to the prospectus of Coeli SICAV II, its Annual Report, and the KID of the relevant Sub-Fund. Relevant information documents are available in English at coeli.com. A summary of investor rights will be available at https://coeli.com/financial-and-legal-information/.

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested. Please note that the management company of the fund may decide to terminate the arrangements made for the marketing of the fund in one or multiple jurisdictions in which there exists arrangements for marketing.