Monthly Newsletter Coeli European – April 2025

This material is marketing communication.

Note that the information below describes the share class (I SEK), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class’ return. The information below regarding returns therefore differs from the returns in other share classes.

Before making any final investment decisions, please read the prospectus, its Annual Report, and the KID of the relevant Sub-Fund here.

April Performance

The fund’s value increased by 4.5% in April (share class I SEK), while the benchmark increased by 2.5%. Since the change of the fund’s strategy at the beginning of September, 2023, the fund’s value has increased by 13.8% compared to an increase of the benchmark by 10.2%.

Source: Coeli European

* Adjusted for spin-off of Rejuveron

** Includes September 1 (strategy change to long-only implemented September 4 2023)

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

Equity Markets / Macro Enviroment

How does one summarize a month like April? The month was the most intense since the global financial crisis, where every piece of news has been epic and has almost literally moved the continental plates between the US and the rest of the world. President Trump continues to charm the pants off dictatorships and Putin while savagely attacking old and faithful allies. The EU urged its officials not to use USB sockets and to use burner phones for security reasons when traveling to the US. The Walpurgis fire had long since burned out when all the facts and news events had been gathered for this monthly newsletter, but we are attempting a summary and conclusion. The time is out of joint and there will naturally be a lot of focus on the US in this letter.

After yet another historic press conference on the evening of April 2, the gates opened to one of the most turbulent weeks in financial history and absolutely the worst ever if you consider that it was just one person's completely self-inflicted crash. By the end of April, however, the declines were modest due to a few retreats by the US administration. The Stoxx600 fell by 1.2%, the S&P500 by 5.5%, the Nasdaq by 3.4% and the MSCI European SMID rose by 1.5%. Two worthy notes; 1) smaller companies fared better and 2) all measured in euros. The US dollar fell by a whopping 4.5%.

We are very pleased with the fund's return of 4.5%, where KKR's bid for Biotage contributed significantly to the monthly return. The stock was depressed to ridiculous levels before the bid came in, which we wrote about in last month's newsletter. The bid premium was a whopping 60%. The fund's best contributors in April were Biotage, Euronext and SLP. The worst were HBX Group, Kalmar and Vallourec. More on that later.

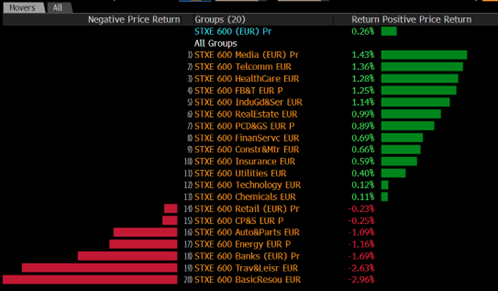

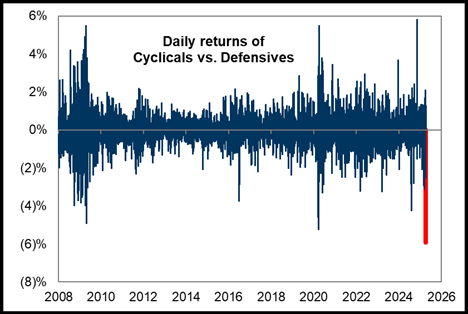

Defensive sectors were clear winners versus more cyclical sectors in April.

Source: Bloomberg

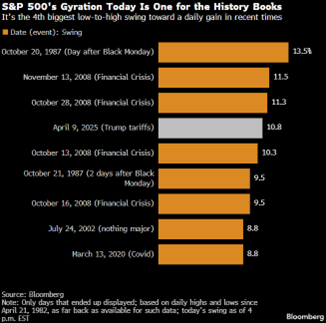

The US administration's capriciousness and, to put it mildly, lack of knowledge about how the global financial system and world trade are interconnected, led to extreme volatility with historic intramonth movements. It's easy to forget, but on April 4th the S&P500 fell by 5%, on April 5th by another 6% and on April 9th the index rose by 9%. The market reversal in the US on April 9th was almost 11%, which is the fourth largest ever. Absolutely crazy. What a fantastic sense of foresight President Trump had when he communicated a few hours before the reversal that it was a good time to buy stocks. Truly impressive.

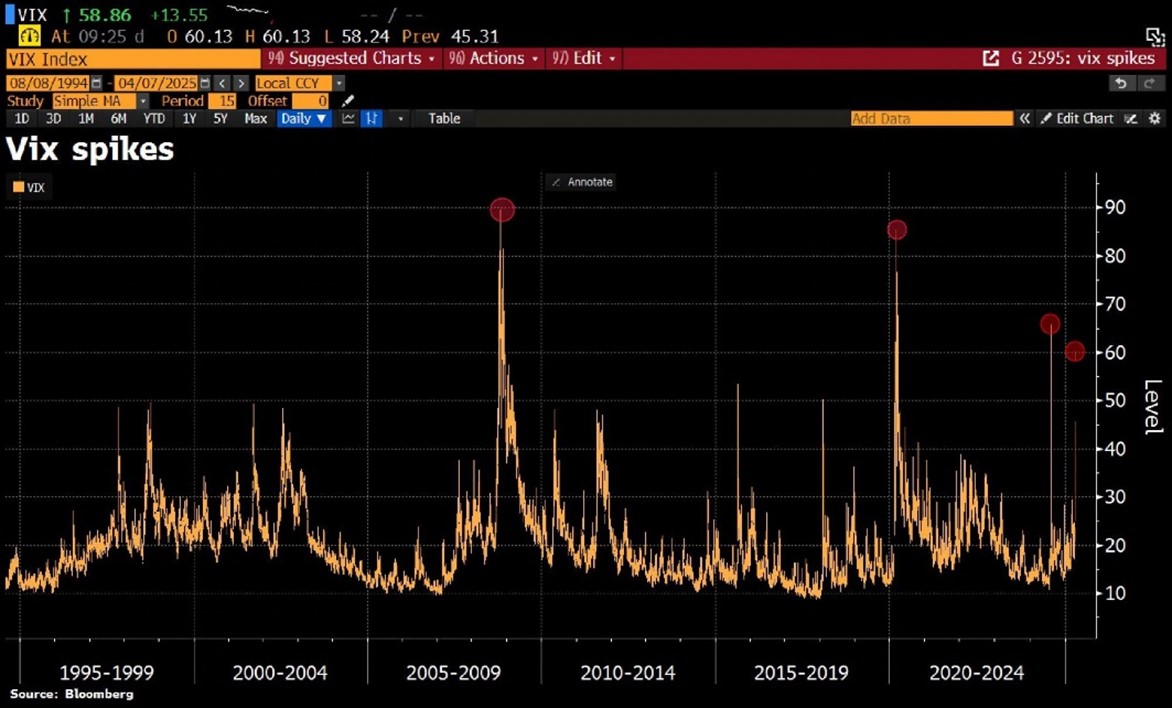

Since the market bottomed out on April 9th, the Stoxx600 rose by just under 14%, the S&P500 by 13%, the Nasdaq by 16% and the MSCI European SMID by 15%. The fund rose from the bottom by 16.5%. Below the VIX index in the last 30 years, which almost reached levels not experienced since the global financial crisis and the Covid crash. When the month ended, the VIX was down to 26.

Source: Bloomberg

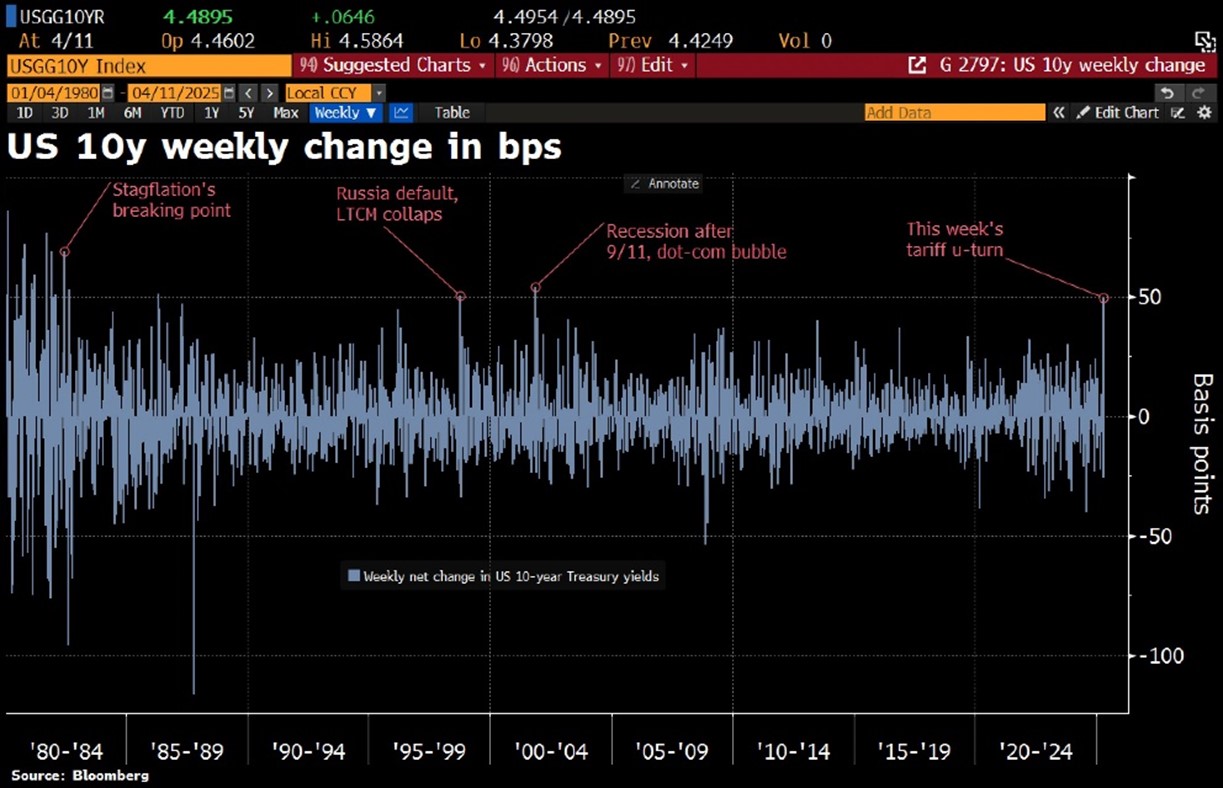

Trump has created enormous uncertainty and damage in a short time. Investors suddenly realized they had too much risk, which led to very sharp declines in the stock and bond markets. See the image below where investors ousted US bonds.

Same was true for US stocks.

Massive sales of US assets resulted in considerable pressure on the US dollar. Below is the development against the euro, which has strengthened by around 10% in two months.

Source: Bloomberg

There is only six months' difference between these two front pages of The Economist.

Source: The Economist

Virtually all asset classes came under heavy pressure after the press conference on April 2nd. A very unusual thing happened: At the same time as US interest rates rose sharply, the dollar weakened. The US 10-year yield, one of the world's most important reference rates and which has basically always been considered a safe haven in uncertain times, rose from 4.0 to 4.5% in one week. The last time the world experienced such a sharp rise in US long-term interest rates was when the planes flew into the World Trade Center, which says a lot about the seriousness of the situation.

Source: Bloomberg

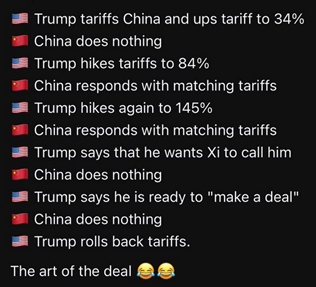

The magnitude and consequences of all the madness from the American administration meant that the reference rate suddenly stopped working, something that had previously been unthinkable. The big drama was thus in the fixed income market and that is what led to a retreat for Trump when he capitulated on the evening of April 9th and gave all countries except China another 90 days of respite to negotiate. This led to one of the biggest increases ever on the American stock market, 9%, and European indices followed suit the next day and rose by about 5%.

The US leadership is reminiscent of an oligarchic regime and we think it is pathetic to say the least that the same individuals that donated money to Trump and who pledged allegiance on his inauguration day, nervously started pointing out how much their shares had fallen and that something should be done, which of course contributed to the capitulation on April 9th. This is what they submitted to on January 20. See the clip below with Professor Jeff Sachs from Columbia University and his view on current politics. Link to video on X.

Currently, Trump's tariffs are at about the same levels as in 1929, and that didn’t go very well.

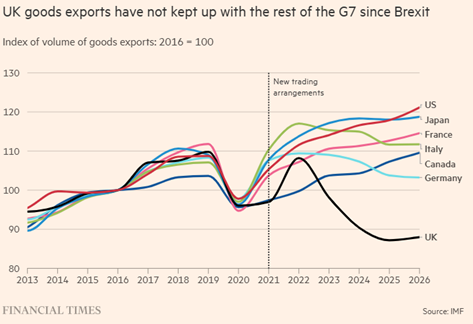

Our British friends have unfortunately engaged in a great deal of self-harm in terms of Brexit. The trade agreements negotiated in 2021 hardly seem to have given the British economy the boost it expected. Something for the American administration to study.

Donald Trump's closest advisor clearly demonstrates how the new administration thinks and acts. Rude, arrogant and exceptionally unintelligent. Link to video on LinkedIn.

If, like the US, you have a national debt of 122% with large budget deficits for several years in a row and at the same time you break up historical structures and partnerships, then you end up in the hands of the market. No other similarities, but it was the same for Greece almost 15 years ago when they howled and called Germany and the EU worse than the last. They had to graciously align themselves when the bond market dictated the terms (and look how good it turned out)!

Source: X

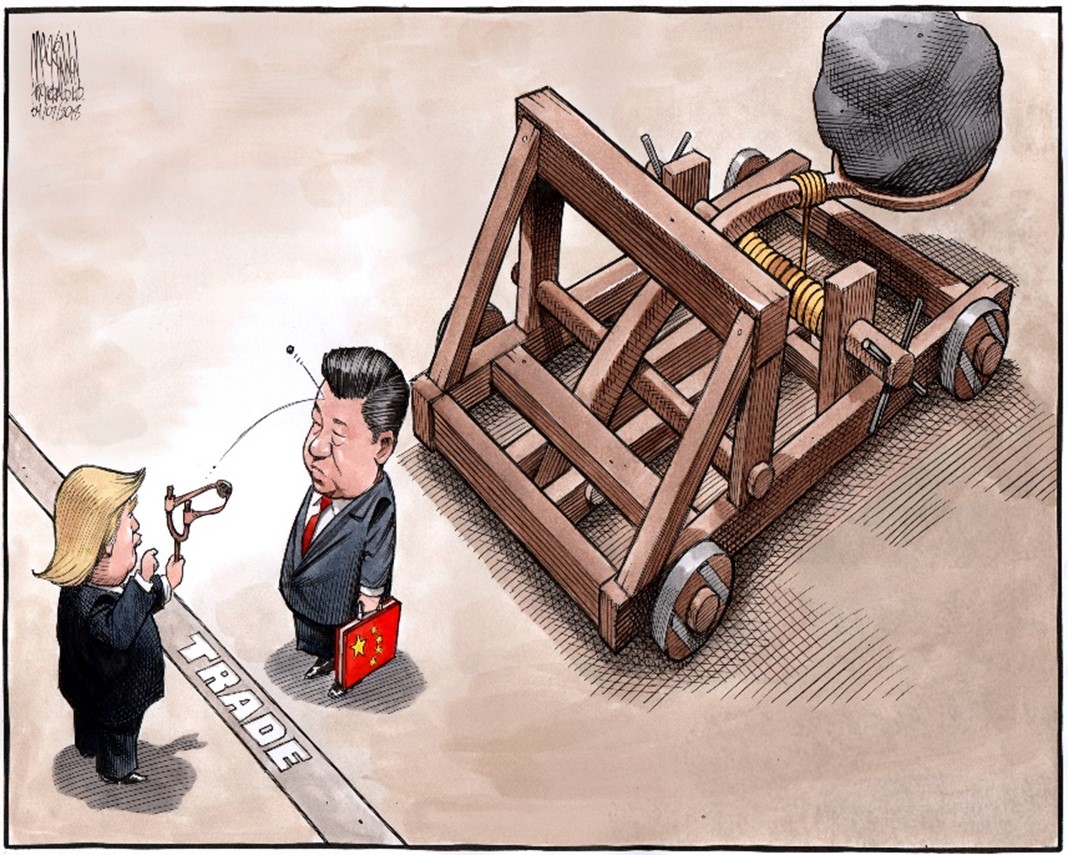

Notwithstanding several other retreats such as certain electronics from China being excluded, certain adjustments for the automotive industry being introduced, that China's high tariffs will not last, constant meaningless comments about how many countries one is discussions with despite anything to show for it, China must be considered a great winner so far as they have been ice cold.

Source: Hedgeye

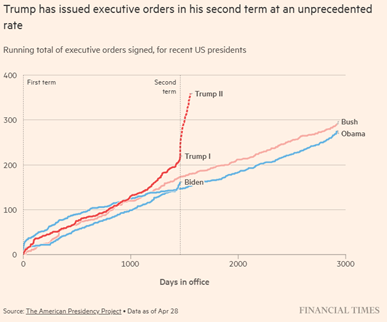

Trump has been busy, and it is of course part of the tactic to come up with so much news all the time that it is impossible to defend yourself and respond to it.

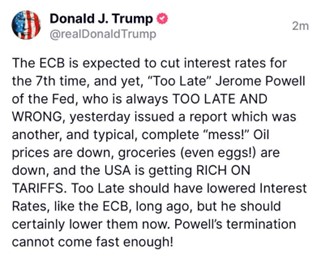

On Monday, April 21, the dollar fell sharply, and the stock market came under pressure once again when Trump commented over the weekend that he had considered firing Fed Chairman Powell. Something he shortly afterwards retracted. The similarities to a banana republic are obvious.

Source: X, Truth Social

In a speech to mark 100 days as president, he continued to criticize Powell. “You shouldn’t criticize the Fed, you should let him do his thing, but I know a lot more than he does about interest rates.”

The reporting season is in full swing and a little over a third of companies in Europe have reported. Simplified, it can be summarized as:

- No major effects from the trade war yet

- Slightly lower sales than expected

- Results more in line

- Unusually uncertain future prospects

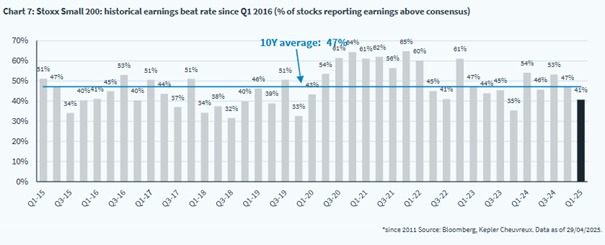

The picture below shows that the smaller companies are initially below their historical average in terms of beating the market’s profit expectations. For the fund, the reporting season has been well received so far, which we will come back to.

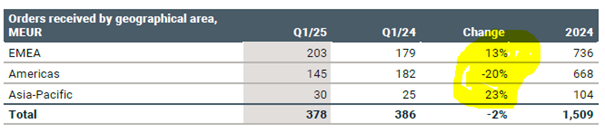

Although tensions were running high among Europe's leaders, outwardly they remained calm. What looked like a really good economic year for Europe has changed in a short time, but it is still too early and uncertain to calculate the extent of the damage. However, there is no doubt that Europe is currently developing relatively better than the US. An example of this is when our company HIAB presented its excellent results for the first quarter at the end of April. The table shows the difference in order intake between the different geographies.

Source: HIAB

Another example is the GDP data for Q1, which was presented on April 30th. For the first time in several years, the US had a negative GDP growth of 0.3% compared to a year ago and to be compared to +2.4% in the fourth quarter. What was particularly interesting was that falling exports reduced the GDP figure by 5% (!) which was the largest decline ever. Trump responded, as usual, humbly and with nuance: “NOTHING TO DO WITH TARIFFS”. He also blamed the decline on Joe Biden and “When the boom begins, it will be like no other!” As is well known, Trump really wants the Nobel Peace Prize and he can keep hoping. He will probably never receive any economics prize.

Peter Navarro, the man Elon Musk recently called an “idiot”, speaks out after the weak GDP figure, which he believes is actually good news. Link to video on X.

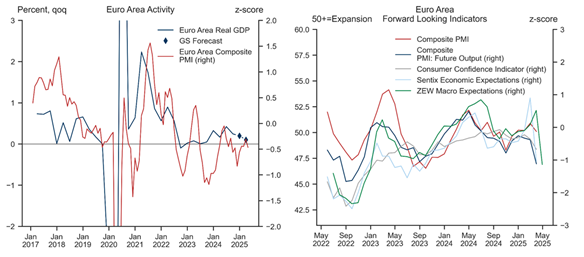

The corresponding GDP data for Europe was +0.4% in the first quarter compared to +0.2% in the fourth quarter last year. However, growth and inflation expectations fell in April, with the PMI coming in at 50.1, indicating barely perceptible GDP growth in Q2. The picture on the right shows sharply declining leading indicators. The strongly strengthened euro has a positive effect on inflation and a marginally negative impact on GDP growth.

In mid-April, the ECB cut its key interest rate by 25 basis points to 2.25% as planned. A few weeks ago, several members of the executive board made it clear that they did not want to lower the interest rate, but the chaos from the American administration made the decision unanimous.

A major advantage in everything that has happened in recent weeks is that Europe has become more united, determined and shows greater self-confidence. The global private equity firm KKR recently announced that Europe is undergoing a renaissance after Trump's speech. They believe that there is now a clear growth agenda in Europe and that money is actually being put to work. KKR has bought companies for USD 10 billion in a short time, including our Biotage. They do not want to repeat the mistake they made in 2008 when they just sat on their cash without taking advantage of the situation. Here and now, it looks like exceptionally good timing.

Source: The Economist

Anyone who speaks the truth is considered hostile. Link to video on X.

Source: CAGLECARTOONS.COM

The most bizarre and frightening incident of April was when a government meeting was filmed a few weeks ago and the various ministers showed their worship of the great leader. You must see this. Link to video on X.

Portfolio Companies

Ahead of the reporting season for the first quarter of 2025, we have said that this is in some ways perhaps the least interesting reporting season in a long time:

- The numbers as such are difficult to rely on for any guidance going forward, since they were largely produced at a time when tariffs did not affect the world economy.

- The outlook is also said to be difficult to interpret because companies know as little as we do about what will happen with tariffs in the future, and their possible consequences for the world economy.

On the other hand, comments regarding the start of April have been interesting. Although several companies have noted a distinctly higher uncertainty for the future, our (highly unscientific) impression is that order intake among many industrial companies looked quite okay in April. Many companies confirm that in Europe there are signs that some end markets seem to have bottomed out and may be starting to grow again. We see this not least among several construction-related companies. At the same time, we see, not surprisingly, many comments about longer lead times and decision-making processes in the USA.

For our part, the reporting period has started well for the fund. Most of our companies have beaten analysts’ expectations. At the same time, we have managed to avoid major bumps, except in the case of Biotage where we were “saved” by a bid from KKR (more on that below).

As many readers know, we own shares in the Finnish trio of Kalmar, Hiab and Konecranes, all of which have undergone relatively major structural changes in recent years. These are high-quality industrial companies that would probably have had much higher valuations if they had only been listed on the other side of the Baltic Sea. In the short term, we are of course grappling with tariffs and their potential impact on costs and demand for these companies, but given where these companies’ valuations stand today, we think the tariff threat is more than well-built into the valuations.

Konecranes

The Finnish industrial company, known for its lifting equipment and cranes for ports and industries, has developed very strongly in recent years. In five years, the return on capital employed (as we estimate it) has risen from around 17% to 30–35%, driven by both margin improvements and higher capital turnover. Towards the end of the year, we anticipate that Konecranes will approach net cash, which, with a refreshed acquisition agenda and recession concerns, could create some interesting investment opportunities.

Konecranes surprised us with an unexpectedly good report during the month. Order intake in the first quarter was 8% better than analysts had predicted. Although Konecranes noted that customer decision-making processes in the US have started to take longer, we do not get the impression that Konecranes has encountered any dramatic deterioration in demand. In Europe, there are signs of some improvement. The tariffs are unlikely to affect Konecranes more negatively than its competitors, which have similar value chains. In Konecranes' port segment (Port Solutions), it can benefit from tariffs as most competitors have a larger share of the value chain located in China.

Our estimate is that Konecranes will trade at single-digit EV/EBITA multiples in the coming years. This is slightly below historical averages, despite major structural improvements in the business in recent years. As the price stands today, the market seems to implicitly expect a profit warning. The risk of that decreased in connection with the first quarter report, in our opinion. It should also be remembered that most of the Konecranes' profit is generated by relatively stable and highly profitable service revenues.

Konecranes shares were unchanged in April and had fallen by 4% in 2025 by the end of the month.

Euronext

Euronext's stock has continued to perform well this year. Looking back over the past year, Euronext has clearly outperformed its closest market peers – the London Stock Exchange and Deutsche Boerse.

Source: Bloomberg

An important reason for Euronext's strong price performance this year has to do with their relatively high exposure to stock volumes. The enormous volatility caused by Trump this year has benefited Euronext as volumes on the European exchanges have increased enormously.

When we started buying our first shares in the summer of 2023, volumes on the exchanges were significantly depressed and Euronext's market capitalization was around 7 billion euros. Today, volumes are unusually high, and the market capitalization is around 15 billion euros. Although earnings have improved, Euronext multiples have also expanded relatively sharply. We believe that there is a certain risk that the share will lose momentum when today's unusually high volumes normalize and have therefore reduced our position for the first time in a very long time. It has gone from being a large position to what we see as a medium-sized position – we see continued potential in Euronext but are consequently taking some profit.

Euronext shares rose 10% in April. For the full year, the share had then risen 36%.

Asker Healthcare Group

As we mentioned in the previous monthly newsletter, we participated in the IPO of Asker Healthcare Group in March. We then took advantage of the volatility in the market in April to further increase our position at prices around SEK 75 – 76 per share. As we increased our position significantly at these levels and the stock price closed at SEK 85.50, trading in Asker had a significant positive impact on this month's result.

In total, Asker rose by just over 6% in April and we hope to return to the company in the next monthly newsletter after Asker releases its first quarterly report as a listed company in May.

4imprint

During the month, we sold our last 4imprint shares. Around 50% of the company's products come from China. With tariffs over 100% and an end market that is currently very weak, we believe that 4imprint may be forced to issue a profit warning once or twice this year. A profit warning may be discounted in today's price, but we believe that we will get better risk-adjusted returns elsewhere at the moment.

We have no problem buying 4imprint shares at higher prices again if it turns out that the uncertainty surrounding the company's long-term future is becoming clearer. If high tariff levels between the US and China remain for a long time, we believe that this could reduce 4imprint's total market significantly, which completely redraws our investment calculation.

Having said that, 4imprint has historically been very good at exploiting market downturns to gain market share, and the company will probably be in a stronger market position in a couple of years from now.

4imprint shares fell by 8% in April.

Biotage

A month or so ago, we wrote that we thought it was an excellent opportunity to buy up Biotage. In our eyes, the stock had taken too much of a beating. So much so that the market put a negative value on the “large molecules” segment (Astrea). It wasn’t long before an offer came. Biotage represents what we are looking for - something that is misunderstood with significant potential to create future value. What was missing was a management team that was focused on creating value.

We are quite certain that Biotage’s new CEO, Frederik, will do something good for Biotage, but it also requires that you can communicate with the market. We were clearly unhappy with this lack of ability and expressed this to the board. You can’t have a company in a public environment that is undergoing a major change if you can’t communicate this to the market in a good way. We told the board that we thought the company would be much better off in a private environment, something that obviously other people thought as well.

The bid of SEK 145 is bittersweet. We believe the company has great potential; the question is how long it will take to realize. Given how the world looked at the time of the bid, we thought it felt balanced. With a premium of 60%, the bid values Biotage at approximately 22x EBITA 2026e, which was a 10% premium to the sector.

Bonesupport

Adjusted for incentive programs and currency reporting, operating profit was in line with market expectations. The company increased sales by 50% adjusted for currency and if one takes a step back it is dazzling. When we invested in the company in 2022 (quite exactly three years ago), sales were SEK 66 million in the first quarter. In 2025, sales in the first quarter were SEK 284 million and SEK 998 million over rolling twelve months. This corresponds to an average sales growth of ~62% over the past three years, astounding. Below is the quarterly development since 2017.

Source: Bonesupport

The negative piece of news of the month was that CEO, Emil Billbäck, will leave his post this fall for a more strategic role within the company. However, the good news is that he will be a full-time employee within the company with a focus on strategic issues and report directly to the CEO. After 7 years as CEO going through at first a global pandemic, a failed PMA study and then a fantastically successful launch of Cerament G in the USA, we understand that private life has fallen behind. The company's organization is self-governing, and we believe the new role will suit Emil well. It is quite logical; the company will continue to grow in the USA and Europe but also start adding more markets, including Asia. Additionally, one can probably think about what inorganic growth opportunities there are for the company. More than one person is needed for this expansion. The new CEO will be Torbjörn Sköld, who most recently came from Stille. He has also been the highest-ranking person in Johnson & Johnson's orthopedics segment, DePuy.

SLP

We usually write that we are spoiled with good reports from SLP and this time was no exception as we call it their best report ever. Profit from property management was around 10% better than consensus. We note that the company has had 12 straight reports beating expectations. We are not alone in not keeping up with the value creation that this little factory is creating. The loan-to-value ratio is 48%, which continues to provide room for more acquisitions. In seven years, the company has gone from 0 to almost 1 billion in rental income (current earning capacity). Impressive.

As it stands now, SLP is expected to be added to the Stockholm Benchmark Index. If this happens, passive capital flows will need to buy shares equivalent to 17 days of turnover to reach the correct index weight, thus it may be a bit crowded. In addition, active funds will also need to consider buying shares given the weight in the index. The share rose 7% in April.

Hiab

Hiab released its first report as an independent company and was rewarded with an 8% share price increase on the day of the report. Orders were in line with consensus, sales were slightly better, but above all, profit was a full 24% better than consensus. The biggest driver of the margin improvement (from 15% last year to 16% this year) was the gross margin, which indicates that the improvement is sustainable.

The company is guiding for a minimum level of 12% in operating margin in 2025, something we believe can be adjusted upwards already in the second quarter. Order intake is still relatively weak but in line with how it has been over the past 10 quarters. They highlight Europe and its continued positive momentum in the defence segment. It was also interesting that construction was better (albeit still weak) at the same time as we read in other companies' reports that we are starting to see some green shoots in the construction market.

We like Hiab and think it is worthwhile to take the time to study the company. We believe they will reach their financial target of 16% operating margin in a year or so, while the company is capital efficient and generates a return on capital employed of 30%. Going forward, there are several opportunities to grow the service business and to add further growth through acquisitions.

The share was essentially unchanged on the month, after being down as much as 15% at its worst.

Kalmar

Kalmar also delivered a report for the first quarter in April. Sales were about 6% lower than expected, while slightly lower volumes meant that profit came in 8% below consensus. What stood out on the upside, however, was the order intake. A full 14% better than expected and 20% higher than last year. The previous quarter also had very strong order intake, which makes the sales forecasts for 2025 look less risky. Kalmar is trading at a low 8x EV/EBIT on 2026e. The share fell 8% in April.

Scandic

The Scandic share rose 4% on the reporting day. The first quarter is a small quarter for Scandic and what gave the share good momentum was the positive outlook for the upcoming high season. Both higher average room rates and occupancy rates are expected in the next quarter. The tariff chaos has basically no bearing on Scandic and there are very few guests coming from the USA. Given how chaotic the rest of the world is, Scandic feels relatively safe at EV/EBITDA ~6x, which is about a 30-40% discount to comparable hotel companies in Europe. As far as we can see, Scandic is clearly the best hotel stock this year in Europe.

Traton

Traton delivered a report in which sales and profit were known after an earlier profit warning. However, order intake was significantly higher than the market expected (almost 13% better) and the company maintained its guidance for the full year. It is worth noting that orders in Europe have increased by 62% compared to last year, with Germany having its strongest quarter since the third quarter of 2022 with a 57% increase in order intake. The share rose 7% on the report day but still fell by 7% in April.

Summary

April was another month that will go into the financial history books where the main subject was the US introduction of tariffs. Few could have guessed that the magnitude of the tariffs would be so extensive, and few could have guessed that it would be communicated so pitifully, which led to enormous confusion and a risk premium that exploded.

As late as the end of March, many in the market were looking for cyclical companies that could offer attractive returns by leveraging an expected economic acceleration. Everything changed, at least temporarily, on April 2nd. The fund had and has continued to invest in engineering companies such as Finnish Hiab, Kalmar and Konecranes, all of which fell sharply after Trump's absurd press conference where he reviewed the upcoming tariffs of various countries. The confusion was absolute at all levels, as it was impossible to understand the implementation and outcome.

To understand the power, see the image below. The difference in returns between cyclical and defensive companies measured 6% in one day in early April. The biggest difference ever measured, including the 2008 global financial crisis. Incredible.

Source: Goldman Sachs

At its worst before the April 9 turnaround, Europe had fallen by roughly 20% in a few days, which felt like an overreaction. Many stocks fell substantially, and our view was that aggregate profits in Europe would not decrease by 20%, but rather that the market's risk premium was expanding. There were really attractive levels in many places and part of the team took the opportunity to increase their investments in the fund during these turbulent days. Below is the development for the Stoxx600.

Source: Bloomberg

When the market turns upwards, as it always does, and the risk premium falls, you want to own the stocks that are usually affected the most, such as bank stocks, thus we increased our holdings in our Austrian bank Bawag. Other stocks we took the opportunity to buy at a discount were SLP and, above all, Asker. Both SLP and Asker then became among the best contributors to the fund in April. We also initiated a new position in British Babcock, which, plainly, is a service company, specifically for the British military. Our largest sale was of shares in Euronext, which at the beginning of the month was the fund's largest position and where we took home significant profits. The Euronext stock performed extremely well throughout the turbulence and remains a significant core holding for the fund.

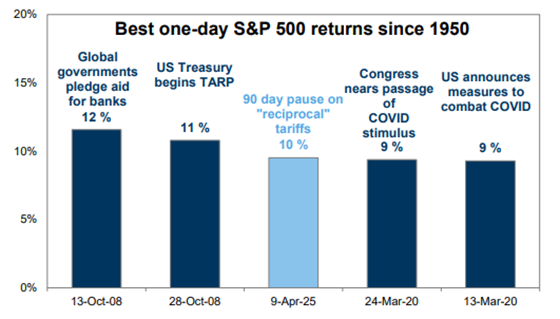

When the rebound came, it was very strong. The third best day ever for the S&P500 in the last 75 years.

Source: Goldman Sachs

In the turbulent and confused world, we have experienced in recent weeks, it is important not to waste too much time and thought on the constant flow of sensational headlines. Instead, we try to focus on how our companies may be affected by world events, adjust our estimates if necessary and follow our companies' valuations. If we notice distinct price anomalies, we act on it by changing our positioning.

One of the best protections for the portfolio in terms of tariffs is to invest in companies with high gross margins and pricing power. A good example is Bonesupport, which with gross margins of around 93% and thus only 7% in manufacturing costs would be virtually unaffected if they were to be subject to tariffs of, for example, 20%.

The next step is to try to understand whether this will mean that there will be major changes in terms of market shares within primarily the American and European markets. To continue with the Bonesupport example, there are no similar products on the market.

The last and probably most important thing to understand is what it will mean for the general investment climate among companies and individuals. Unfortunately, this is also the hardest thing to estimate now. Several of the companies in the portfolio with the highest tariff risk, such as the Finnish industrial companies, have already reported and given a good and balanced picture of the situation.

Worth noting is that consumer confidence in Germany has plummeted in the short term, despite gigantic stimulus packages being introduced.

Source: Bloomberg, Holger Zschaepitz

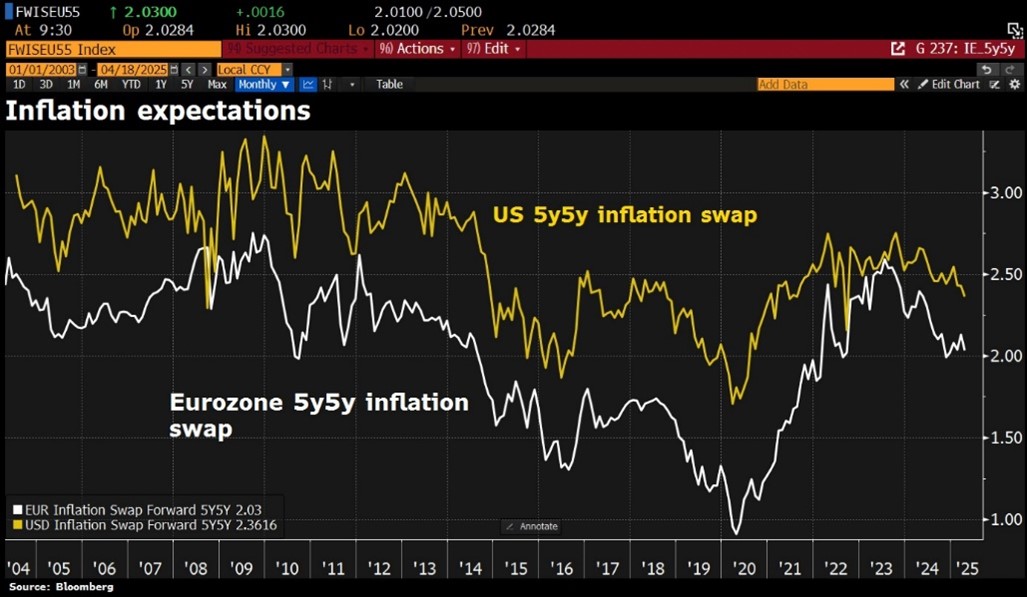

More positive is that inflation expectations in both the US and Europe were stable during April and actually fell slightly.

Source: Bloomberg, Holger Zschaepitz

But inflation in the US has been enormous in various segments in recent years.

Source: McDonalds

”Things are going great” - I

”Things are going great” - II

”Things are going great”- III

”Things are going great” - IV

As so many times before, dramatic front pages became the best contraindicator. That said, the ongoing drama is far from over.

Source: Dagens Industri

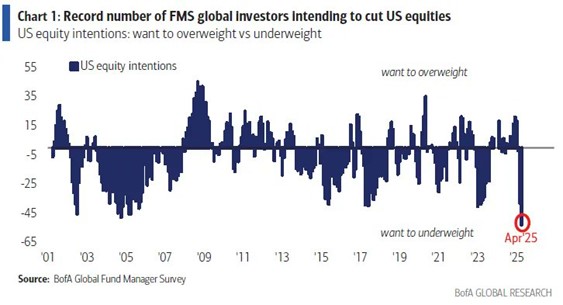

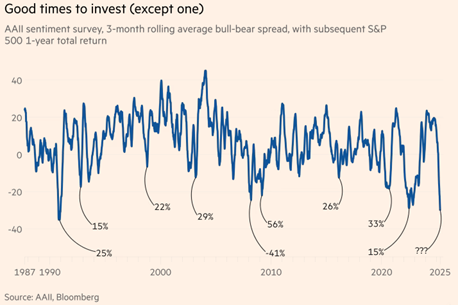

The image below shows the difference between bull and bear sentiment since 1987. When the difference was at such extreme levels as it was in April, it has always, with the exception of 2008, been a good time to buy stocks.

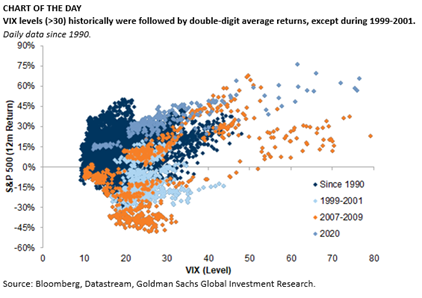

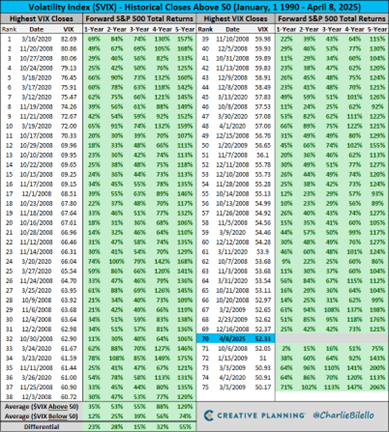

Illustrated it another way, when the VIX index exceeds 30 and measured since 1990, it has every time, except for 1999–2001, produced double-digit annual returns in the following 12 months.

And even more clearly illustrated, when VIX exceeds 50 and measured since 1990. Pretty clear pattern.

Source: Creative Planning, @CharlieBilello

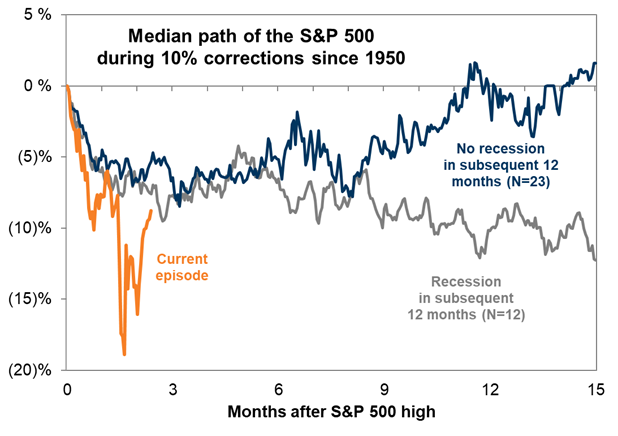

Many people stared at the graph below in April, wondering if the S&P500 would be able to withstand the technical levels from the Covid crash. It did.

Source: Goldman Sachs

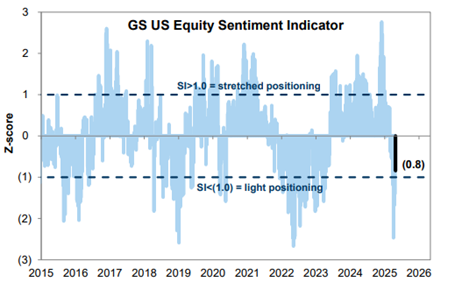

Goldman Sachs sentiment indicator below.

Source: Goldman Sachs

Source: X

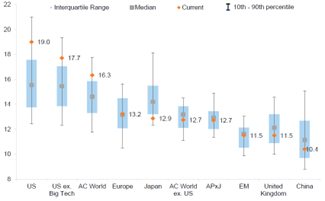

There is still a large difference in risk premium between the US and European stock markets. Moreover, interest rates and inflation are higher in the US and the political risk can safely be said to be higher in the US.

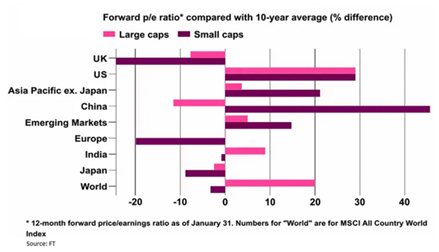

The US remains at its own level when it comes to valuations. The UK stands out in the other direction.

Source: Goldman Sachs

The valuation stands out, in particular, for UK small caps, which are trading at over a 20% discount to their 10-year average. The US is trading at a 30% premium. The initial risk/reward ratio is enormous.

Source: Financial Times

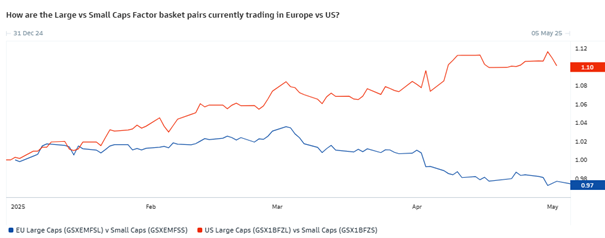

European small-caps have performed better than large-caps this year, while the opposite is true in the US.

Source: Goldman Sachs

So how do we summarize the situation and what are we doing?

There is no doubt that the European stock market has benefited on a relative basis from the turbulence in American politics. The conditions in the US have changed significantly and thus many years of overexposure to the US will be reduced through selloffs. That capital is now looking for a new safe haven where there is good liquidity and where there are markets with good ethics and transparency.

Although liquidity could be better, we believe that the flow of capital will continue to enter Europe. In addition to the political chaos, it currently looks like the US is in a mild recession. At the same time, the S&P500 has only fallen by 3% for the full year, with a valuation that is clearly higher than historical levels. Four months ago, growth in the US was expected to be 2.5% this year and the outcome for the first quarter was -0.2%. The US is cutting its public spending while Europe is increasing its for the first time in many years. We are slightly biased, but it does not feel attractive. In addition, you have a dollar that Trump is trying hard to make fall further.

Source: Goldman Sachs

We are entering the summer months which are typically weak, but it feels like other things are driving the stock market right now. Here and now, systematic funds are expected to be big buyers and at the same time, large buyback programs are getting underway again after the companies reported.

We note that small companies have developed better than larger companies recently, which feels reasonable given lower tariff risk, valuation difference compared to larger companies and that interest rates in Europe have continued to fall, which is especially positive for the smaller companies. Since Liberation Day, smaller companies have performed about 3% better than large companies.

Source: Kepler Cheauvreux

Our reporting season so far has been unusually good and we hope and believe that this will continue over the next two weeks. Looking at the last five quarters, four out of five reporting seasons have been good or very good and only the fourth quarter of last year was weak.

Have a wonderful May!

Mikael & Team

Malmö May 7, 2025

IMPORTANT INFORMATION. This is a marketing communication. Before making any final investment decisions, please refer to the prospectus of Coeli SICAV II, its Annual Report, and the KID of the relevant Sub-Fund. Relevant information documents are available in English at coeli.com. A summary of investor rights will be available at https://coeli.com/financial-and-legal-information/.

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested. Please note that the management company of the fund may decide to terminate the arrangements made for the marketing of the fund in one or multiple jurisdictions in which there exists arrangements for marketing.