June was another news-packed month that began with an epic argument between two of the world's biggest alpha males in the form of President Trump and Elon Musk over the budget proposal, which includes major US tax cuts. Elon Musk was unusually clear that it will have significant negative consequences for the American economy.

Source: X

The argument ended with Musk having to apologize and straighten out his lines. It went well, and at the end of June he once again began to criticize the proposal, which is expected to be approved by the Senate before July 4th. To be continued.

The world held its breath for a few days while the effects and consequences of Operation Midnight Hammer were evaluated. Much remains shrouded in mystery about how much damage the US actually caused to Iran, but here and now it now looks like a major victory for President Trump as the war ended after 12 days. This is to the great joy of the entire free world, where Iran is now greatly weakened, including all its proxy warriors.

For the second month in a row, the US stock market developed stronger than the European one, even adjusted for the very weak dollar. Not since 1973 has the US dollar had a weaker first half of the year. The fund cruised through the heavy news flow and had a strong development of 4.6% compared to 2.3% for the benchmark. The weakened Swedish krona had a positive contribution of 2.4% for the fund in June. The corresponding contribution for the first half of the year is -2.8%. The fund's three strongest contributors were Babcock, Kalmar and SLP. The fund's worst contributors in June were Lindab, Traton and Volution.

When we summarize the first half of the year, Europe continues to be in a clear lead over the US. YTD, the Stoxx600 has returned 6.6% in local currency compared to the S&P500 of 5.5%. Measured in Euros, the S&P500 has fallen by 7.1%. Or to put it another way, for American investors, who measure in USD, the Stoxx600 has risen by 21% and the DAX by a whopping 36%. We guess that Germany, measured in USD, has never had a stronger start to a stock market year.

Unlike previous months this year, we received several positive news in June.

- The war between Iran and Israel began and ended with a clear victory for the free world. Let's hope things calm down there now.

- The price of oil shot up but retracted just as quickly.

- The ECB lowered interest rates further (as did the Riksbank, Swedish Central Bank).

- NATO agreed on new goals and the fight with President Trump did not occur.

- The proposal for the "revenge tax", section 899, which targets foreign investments in the United States, looks like it will be scrapped before it gets going.

US long-term interest rates fell, industrial metals rose, and we saw new highs in Europe. The US stock markets, which have been under more pressure than the European ones, have had a very strong recovery. In four months, Nasdaq has offered a movement of about 55%, where the index first fell by just over 20% and then rose by almost 35% and then reached a new high. Unbelievable.

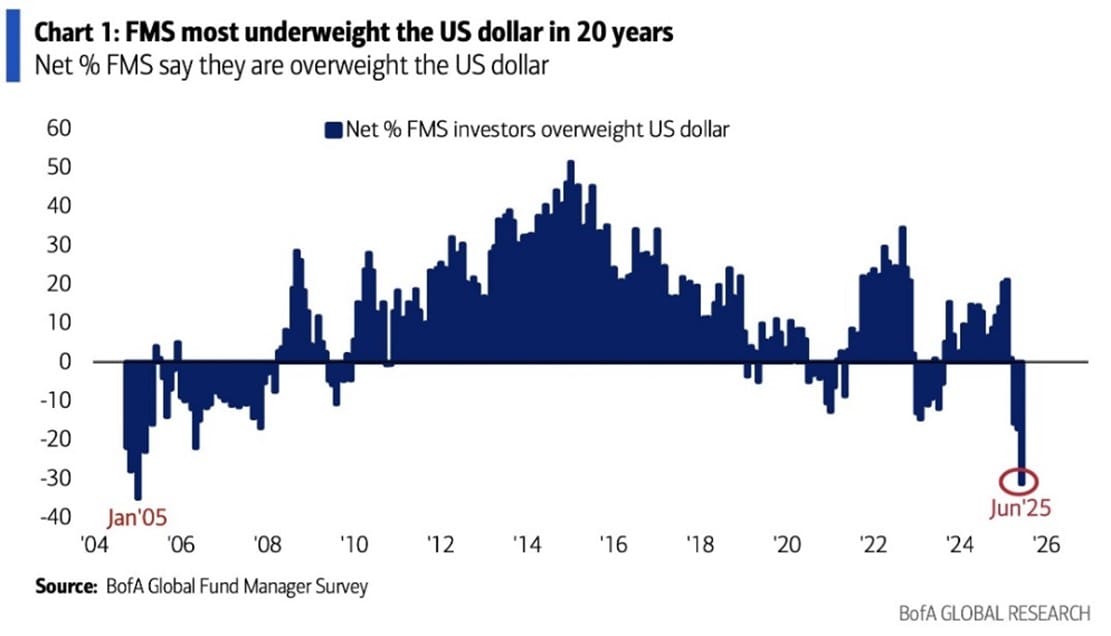

The picture shows that investors have sold large amounts of USD in recent months.

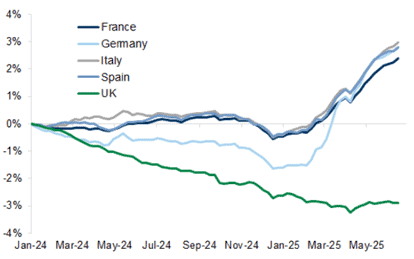

Inflows to European stock markets have been the strongest in many years. The UK is struggling, but at least the huge outflows there have slowed.

Source: Goldman Sachs

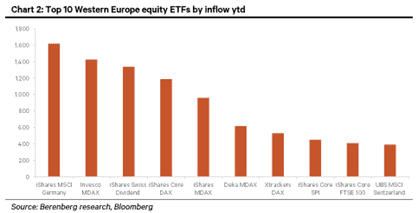

When it comes to inflows into European ETFs, the German stock market completely dominates.

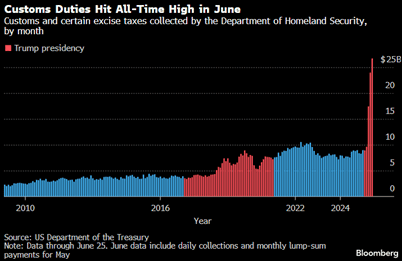

President Trump is probably pleased with the picture below.

Source: Bloomberg

The current account balance has also changed radically, likely due to a sharp decline in imports.

Source: Bloomberg

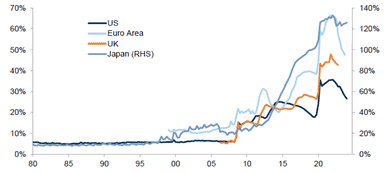

Study the image below showing the balance sheet of different countries' central banks in relation to the country's GDP. The difference compared to 20 years ago is enormous and with the Covid crisis the floodgates were fully opened.

Source: Goldman Sachs

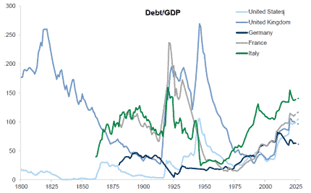

The image below shows the debt of different countries in relation to GDP. Note the peaks during the two world wars and the increase since 2000.

Source: Goldman Sachs

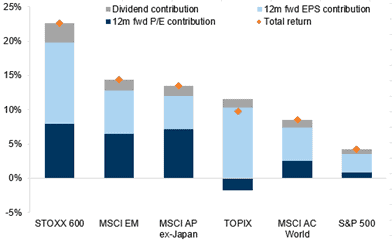

Despite all the uncertainty, the stock market has delivered a good return over the past 12 months. The figure below is measured in USD. Note in particular that we have had profit growth in all regions. Europe is a superior overall winner.

Source: Goldman Sachs

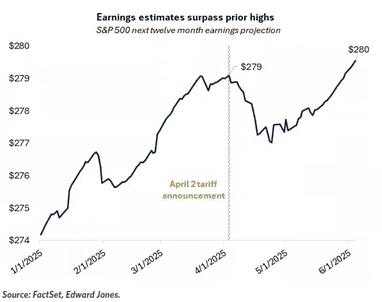

The image below shows the earnings growth for the S&P500 this year and is a good explanation for why the stock market is at new highs – because so are the earnings.

Source: FactSet, Edward Jones

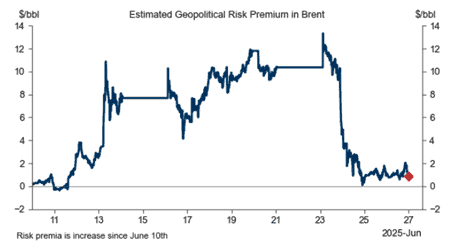

The geopolitical risk premium for oil has dropped from around $15 to below $1 in a few days.

Source: Goldman Sachs

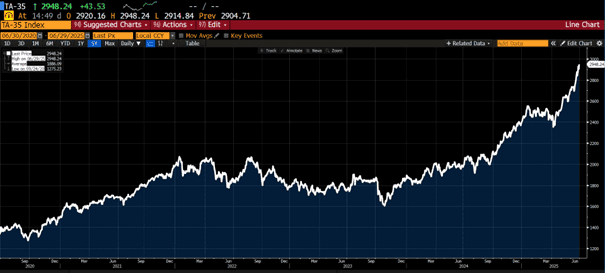

We note that the Tel Aviv stock market continues to rise to new heights. It spontaneously feels somewhat contradictory, but war is (unfortunately) also business.

Source: Bloomberg

Portfolio Companies

Babcock

We wrote about British Babcock last month when it was both a new holding and one of the fund's best contributors for May. After rising by 16% in May, the share price accelerated further and rose by 23% in June, thus becoming the best contributor of the month. The increase since the beginning of the year is now a full 129% and compared to our purchase value, the share has risen by 42%.

The reason for the strong development was to some extent that it reported earnings that were slightly above expectations. But what made the market trade the share up 11% that day was:

- Upgrade of short-term targets for 2026. It now expects at least an 8% operating margin as early as next year, which is a year earlier than planned.

- Upgrade of medium-term targets. It expects at least a 9% margin in 2028, which is 80 basis points better than what the market expected. This increases operating profit by 10%, all else being equal.

- The dividend was increased by 30%.

- A buyback program of 4% of outstanding shares will be implemented. This is the first time Babcock has ever bought back shares.

A very good delivery, simply!

Lindab

The worst contributor in June was Lindab, whose share price fell 9%. The explanation can be attributed to a number of analysts who adjusted their profit estimates down slightly. The quarterly report in July will probably not show a turnaround, but with each passing month we get closer to an acceleration in operations. Lindab is in its third year with negative organic growth, which is significant. In addition, it should be noted that Lindab is late-cyclical in the construction economy.

The reason for owning the share now is a strong management team and market position, but above all, operational leverage will make a big impact when growth returns.

Bonesupport

Bonesupport was one of the top contributors to the fund in June without any specific news. As we mentioned earlier, the share has been pressured by currency headwinds and increased short selling. We have taken advantage of the weakness and increased our position by 20% in the past month. On July 15th, it is time for Bonesupport to show its true colours. The market is expected to be well aware of the consequences of the weak dollar, and we believe that the underlying business is continuing at the same positive pace as before. The share rose just over 10% in June but has fallen by a full 28% this year.

SLP

SLP continues to acquire properties at a level that few other companies can match. During the first half of the year, it has purchased and agreed on acquisitions for an additional SEK 3 billion, which corresponds to approximately 20% of the existing portfolio. During the quarter, SLP refinanced a third of the loan portfolio, which resulted in the average margin on the entire loan portfolio being reduced by 8 basis points. If we assume a multiple of 15x, this corresponds to just over SEK 100 million, approximately 1% of the market value. SLP reports on July 10th and we believe the company can continue its unbeaten streak of exceeding market expectations. The share rose just over 10% in June and has risen by 9% this year.

Kalmar

Since the low in April, Kalmar shares have risen by almost 50%. In addition to a low valuation, several large, announced orders during the quarter have fueled the share price rise. The valuation remains attractive and, after rising by 16% in June, the company is valued at a low 10x operating profit in 2026e. The company will present its quarterly report at the end of July. During the first half of the year, the share has risen by 13%.

Hiab

Hiab also had a strong price development in June with a positive 8% and since the lowest level in April the share has risen 45%. No major news has been announced recently, but our clear impression is that interest in Hiab has increased recently, with the latest quarterly report, with a delivered operating margin of 16%, likely being a catalyst. The company's exposure to a growing defense industry combined with an attractive valuation has also driven the price development. During the first half of the year the share has risen by 1%.

Summary

June ended on a high note with several major positive macro news. The next major macro event is likely already completed by the time this is published - "the one big and beautiful bill". If it goes according to plan, it will mean significant tax breaks, which will likely have a positive impact on the stock market. We suspect that investors (and Republicans) are putting the budget deficit issues ahead of them.

The deadline for negotiations on tariffs with the EU expires on July 9th. We note that the market is optimistic that it will land well and, in general, there is significantly less focus on this issue among investors now than compared to 10 weeks ago. In two weeks, we will know significantly more.

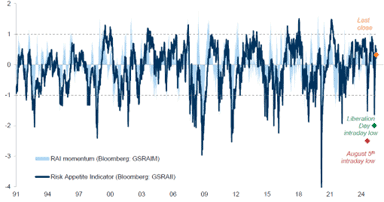

Risk appetite in the market is currently at a normal level. The green dot in the image below was when Trump announced tariffs on April 2nd. The rebound in risk appetite that followed was just as strong as the decline had been.

Source: Goldman Sachs

A major reason for the sharp rebound in the stock market was that liquidity in the financial systems rose significantly. Below is the Goldman Sachs Financial Conditions index, which is now at its lowest level this year. Note the sharp difference compared to 10 weeks ago. The index is a weighted combination of the policy rate, the long-term risk-free rate, the spread in corporate bonds, stock valuations and currencies. A low level is of course positive for an asset class like stocks.

Source: Bloomberg

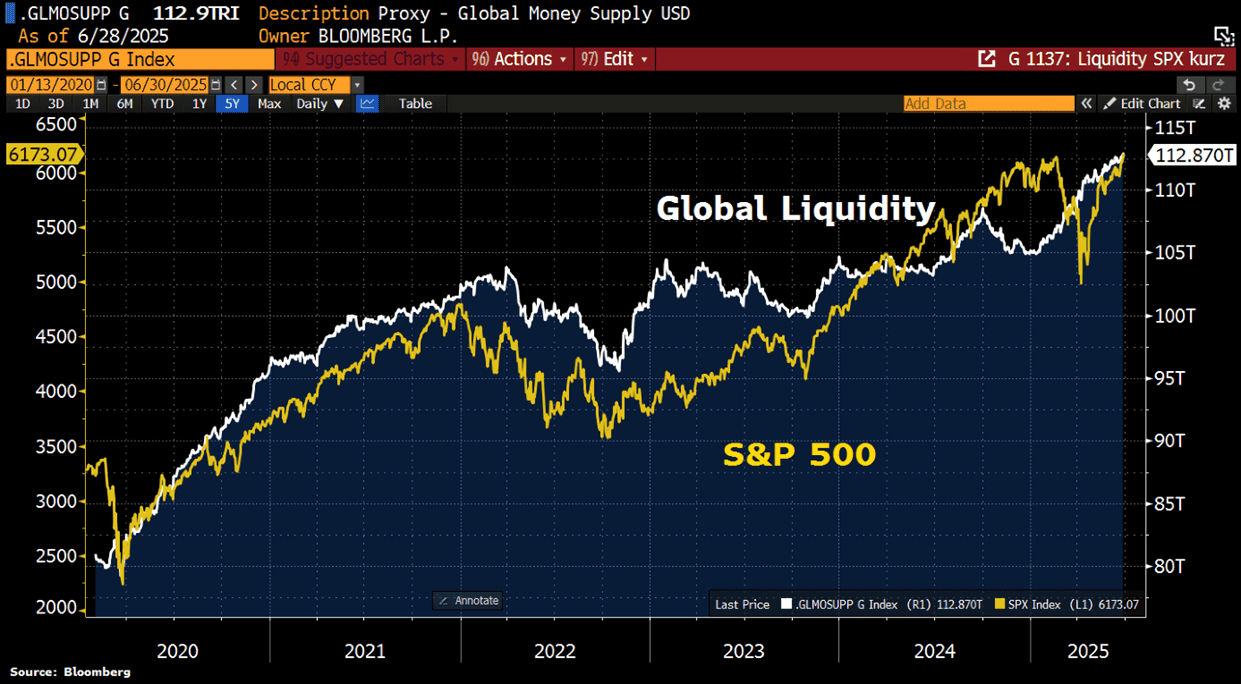

On the same theme: The correlation between global liquidity and the S&P500 is high.

Source: Bloomberg, Holger Zschaepitz

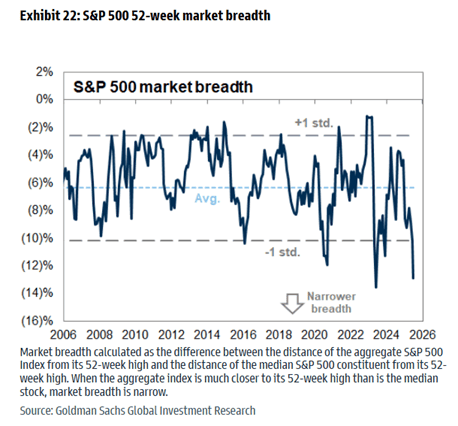

The world's largest company, Mag7, continues to deliver strong reports. Their strong recovery in the stock market has caused the breadth of the US market to drop significantly. The recovery is of a "lower quality".

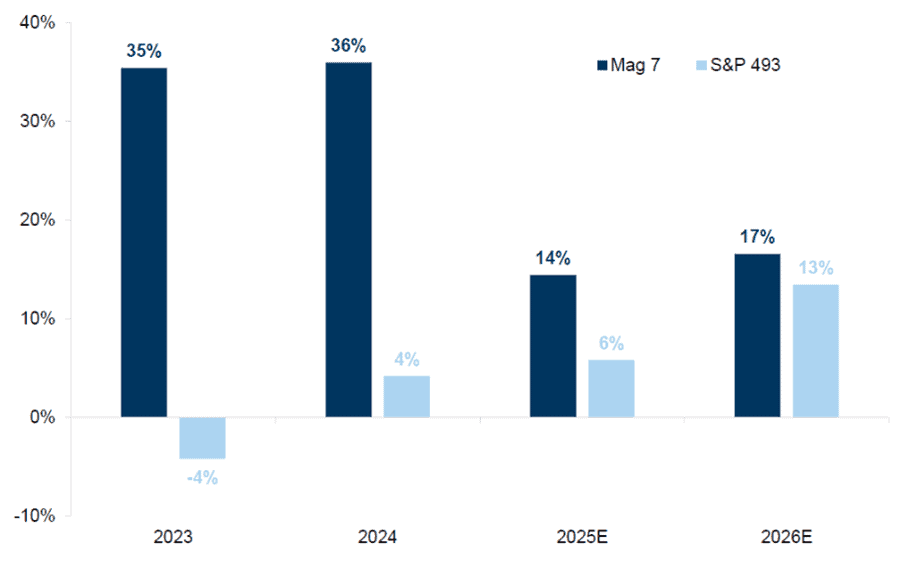

After two phenomenal years for the big tech companies, things are now starting to level out a bit in terms of expected profit growth.

Source: Goldman Sachs

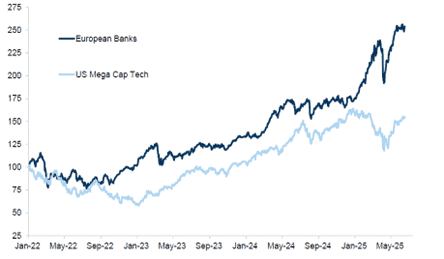

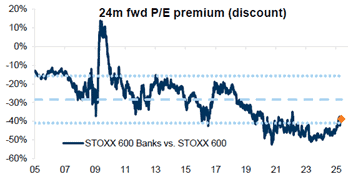

Despite a very strong return for Mag7, it pales in comparison to the European banking index. European banks have been the best sector for four years in a row and so far this year, it is again at the top with a positive return of 29%. The fund has two positions in the form of Austria's Bawag and Germany's Commerzbank, which have risen by 41 and 74% respectively. In addition, Bawag in particular has paid a substantial dividend.

Source: Goldman Sachs

Despite a very strong price trend, European banks are valued at a near-record discount to the Stoxx600.

Source: Goldman Sachs

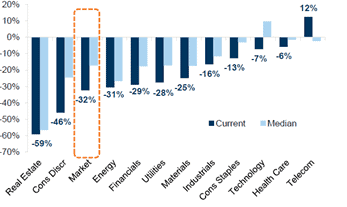

Compared to the past 20 years, most sectors in Europe are valued at an unusually large discount to the US market. There are various reasons for this, but the question is whether the difference should be this large? The sector that is perhaps most notable is energy. It is the same commodity and about the same return on capital, but a 30% difference in valuation.

Source: Goldman Sachs

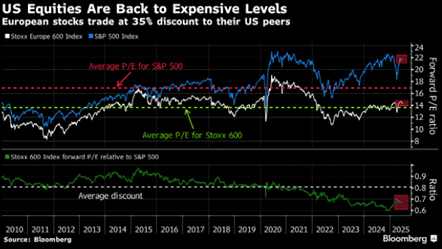

American stocks are once again at historically high valuation levels.

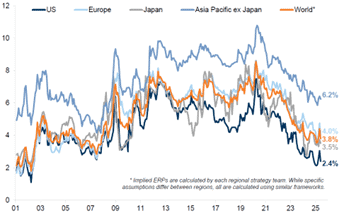

The risk premium for Europe remains clearly the highest compared to other important regions.

Source: Goldman Sachs

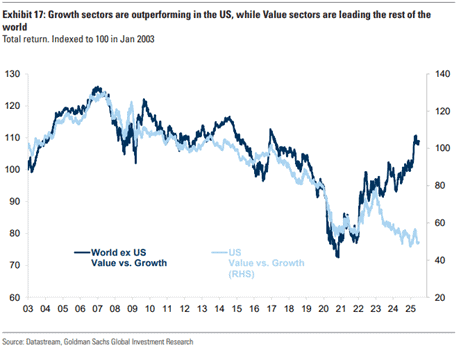

In the US, growth companies continue to dominate, while value stocks are performing significantly better in the rest of the world. This may be partly due to the fact that the world's most powerful tech companies are American.

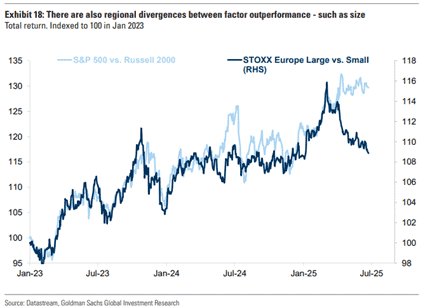

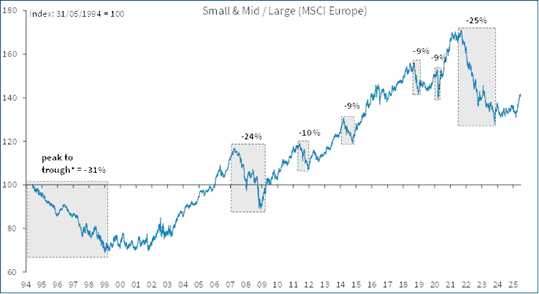

Large American companies have performed better than small American companies this year. The opposite is true in Europe, where small companies, SMIDs, have finally started to outperform the larger companies. We suspect that the falling interest rate level is the single largest explanatory variable.

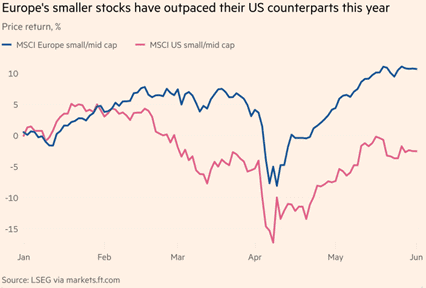

European SMIDs have also performed significantly better than American SMIDs so far this year.

Source: Financial Times

Can you see Europe's excess return vs. the US? There is some catching up to do.

Source: Berenberg

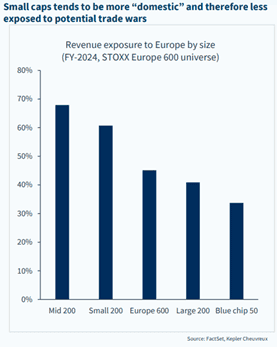

Smaller companies have a larger proportion of domestic sales and thus a lower tariff risk.

Source: Kepler Cheuvreux

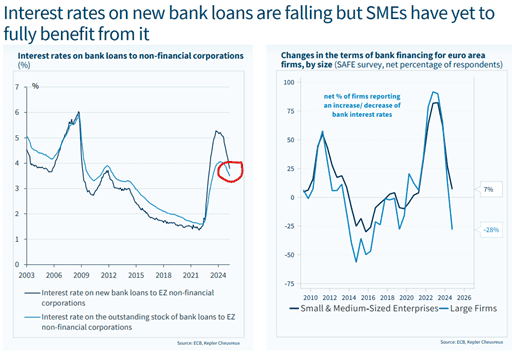

Smaller companies are more sensitive to interest rates than larger companies and thus falling interest rates will have a greater impact on smaller companies' earnings. This contributes to smaller companies' stronger profit growth (despite a currently lower valuation).

Source: Kepler Cheuvreux

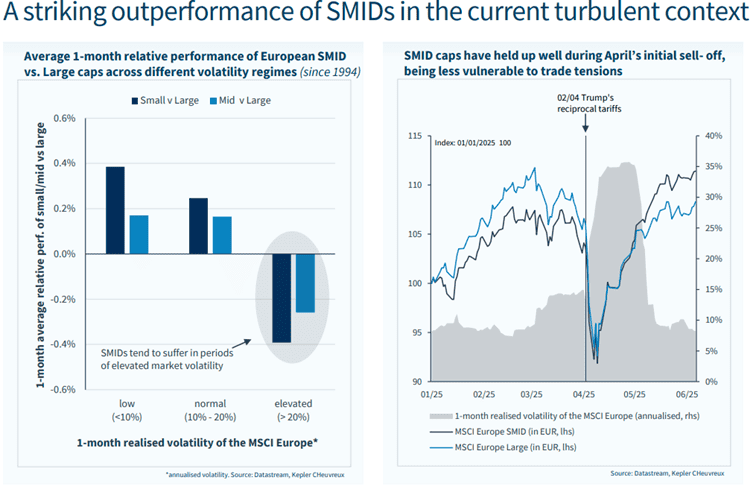

After a long and patient wait, it finally looks like European SMIDs are out of the starting blocks. The image below on the left shows the historical performance under different volatility scenarios. SMIDs perform significantly better in low or normal market volatility (as in May and June). The image on the right shows that larger companies were a clear winner in the first quarter, but the opposite was true in the second quarter. The rebound after April 2 with Trump and the tariffs has been significantly stronger for smaller companies.

Source: Kepler Cheuvreux

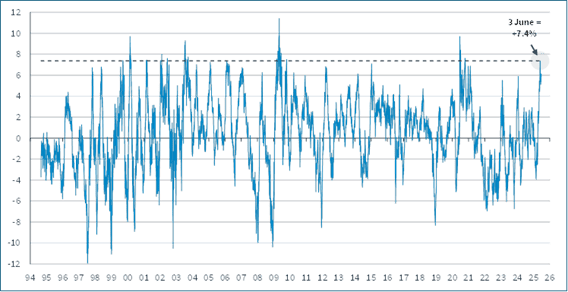

Picture of the month! The last three-month period is one of the strongest for European SMIDs measured over 30 years with just over 7% in excess return compared to larger companies. We think it shows clear evidence that SMIDs are now starting to perform strongly.

Source: Goldman Sachs

After a complete stock market crash in 2022 for SMIDs, which was then followed by two years of sideways development, we are now seeing a clear breakout upward for the smaller companies.

Source: Kepler Cheuvreux

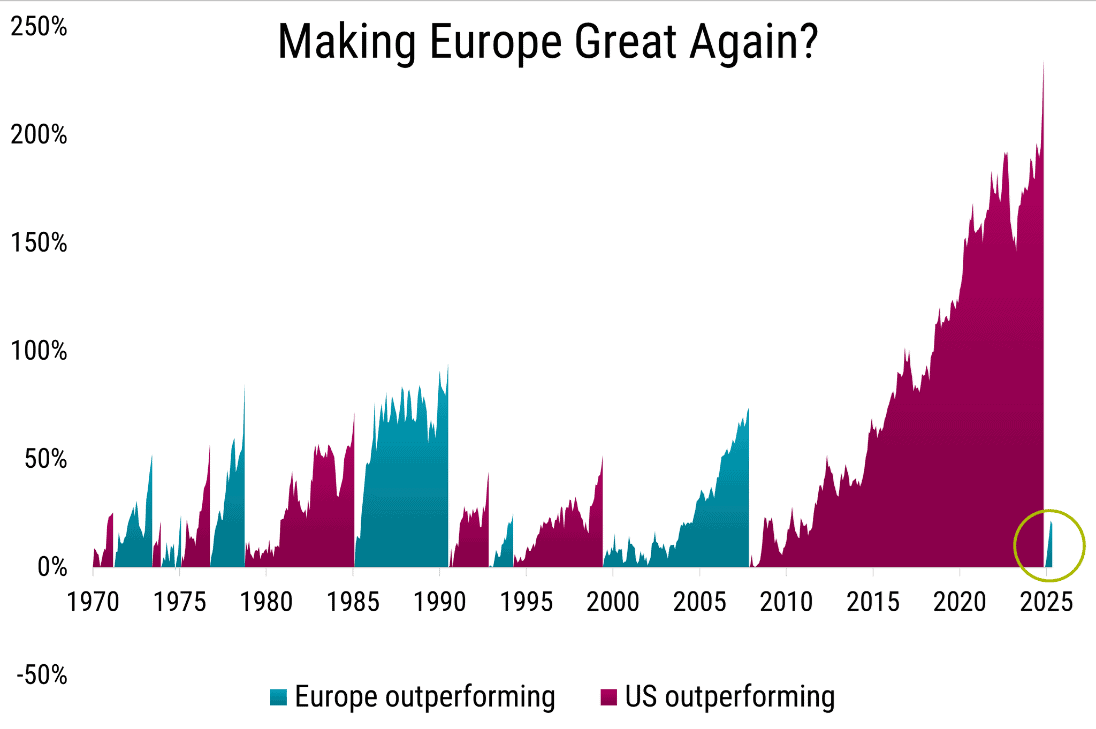

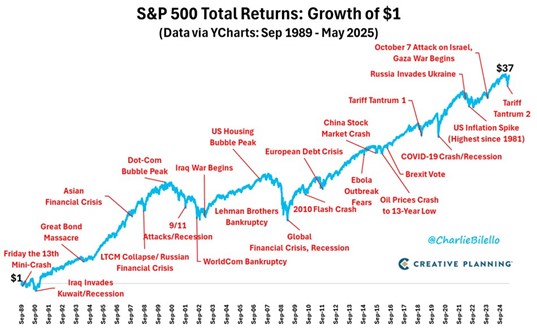

The last picture shows the importance of having a long-term perspective. There's been quite a lot of misery in the world over the last 35 years, but the fallout is pretty good, nonetheless.

Source: CREATIVE PLANNING, @CharlieBiello

In conclusion, we are pleased with the last two months as the fund regained momentum driven by analysis and stock picking. This type of market undoubtedly suits us well with decreasing macro noise, falling interest rates, falling inflation, capital inflows to Europe, and a greater focus on SMIDs. The conditions for European small and medium-sized companies are better than they have been in many years.

There is currently a clear “risk on” in the market and seasonally July is usually a strong stock market month. Of the last 15 July months, for example, Nasdaq has only had a negative return once. Since the start of 2018, the fund has only had one negative July month (2023). In two weeks, the new reporting season will start, and we are looking forward to it.

We wish you all a fantastic July with sun, swimming and relaxation with loved ones!

Mikael & Team

Malmö, 4th of July 2025

IMPORTANT INFORMATION. This is a marketing communication. Before making any final investment decisions, please refer to the prospectus of Coeli SICAV II, its Annual Report, and the KID of the relevant Sub-Fund. Relevant information documents are available in English at coeli.com. A summary of investor rights will be available at https://coeli.com/financial-and-legal-information/.

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested. Please note that the management company of the fund may decide to terminate the arrangements made for the marketing of the fund in one or multiple jurisdictions in which there exists arrangements for marketing.