This material is marketing communication.

Note that the information below describes the share class (I SEK), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class’ return. The information below regarding returns therefore differs from the returns in other share classes.

Before making any final investment decisions, please read the prospectus, its Annual Report, and the KID of the relevant Sub-Fund here.

AUGUST PERFORMANCE

The fund’s value decreased by 2.1% in August (share class I SEK), while the benchmark decreased by 0.5%. Since the change of the fund’s strategy in September 2023, the fund’s value has increased by 26.3% compared to an increase of the benchmark by 21.1%.

Source: Coeli European

* Adjusted for spin-off of Rejuveron

** Includes September 1 (strategy change to long-only implemented September 4 2023)

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

EQUITY MARKETS / MACRO ENVIRONMENT

The broad European index rose by 0.7% in August compared to the S&P500 which rose by 1.9%. Measured in euros, the S&P500 fell by 0.5%.

After four strong months for small and mid-caps, performance was weaker in August with MSCI small caps posting a -0.8% return (-1.7% in SEK). The fund had a weak month, but without any major drama, and returned -2.1%. Performance was surprising to us amid strong company reports, but we believe that it will reverse in the future. Best contributors in August were Scandic, Rotork and Traton. Worst contributors were Bonesupport, Volution and Hiab. The Swedish krona appreciation contributed to the SEK class with a 1.1% loss (in isolation) and for the full year that corresponding figure is -3.5%. In August, the fund sold all shares in HBX, Bureau Veritas, Vallourec and Commerzbank.

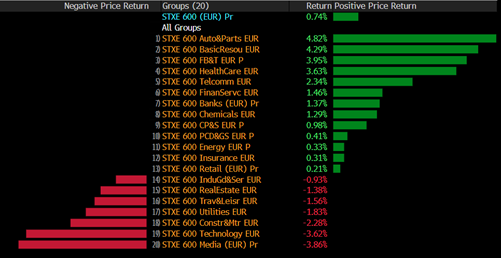

Below is sector development in August.

Source: Bloomberg

August began with a clear drop as President Trump imposed extensive tariffs on several countries. In addition, we received US data showing weak job growth for July, which contributed to the selling pressure on world stock markets. This start to the month was at least better than last year when Tokyo fell 12% in a single day. On that specific day last year, the author was hit by a bus on route to the office. At the same time as the bus hit my car, I spoke to my insurance company, who decided to withdraw its promise to replace my air heat pump for 300,000 kronor (which had been destroyed due to a lightning strike a few weeks earlier). So, compared to last year, August started off great.

Undoubtedly the month's biggest event was President Trump's meeting in Alaska with the wanted war criminal Putin. As expected, it was a real stomach-churning experience. The red carpet was rolled out and Trump stood and applauded. In a short time, Putin had bamboozled Trump and was able to return home content without more sanctions from the US and with more time to continue his disgusting attacks on the Ukrainian people. The flop was topped the next day when Trump called on Ukraine to surrender to Russian supremacy on the grounds that Ukraine is a small country and Russia is a big one. Okay?! To quote Olof Ehrenkrona in Svenska Dagbladet: "Trump has prolonged the war through his incompetence and boundless self-absorption. The United States is being humiliated and treated like a plaything by Soviet ghosts." Despite this, the atmosphere was harmonious when seven European leaders met to support Zelensky in Washington the following Monday.

Defense stocks came under heavy pressure in connection with the above events as investors naively believed in some kind of end to the war. Russia’s chain-smoking Foreign Minister, Lavrov, who showed up in Alaska wearing a CCCP shirt, shortly thereafter dismissed a meeting between Putin and Zelensky. Trump explained to the world that the reason there would be no meeting between Zelensky and Putin was that Putin didn’t like Zelensky. “He doesn’t like him. “I have people I don’t like; I don’t like to meet with them.” Defense stocks then began to rise again. Our own holdings in defense-related Babcock, for example, first fell 10% and then rose 9%.

The summation of all the efforts above and presented by the world’s most powerful man can be seen in this video. You must watch it as my vocabulary is too limited to describe the scene. Link to video.

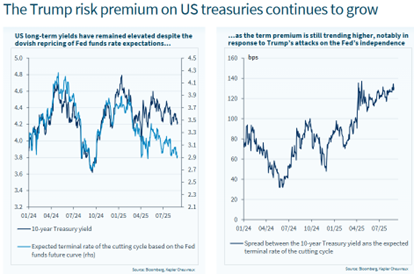

In connection with the annual meeting in Jackson Hole, Jerome Powell (Fed Chairman) communicated to the market that they were now more open to a reduction of the key interest rate. That was not enough for the great leader and with his usual bombastic style, Fed member Lisa Cook was dismissed with reference to her previous falsification of mortgage documents. This is of course a sharp escalation of the aggression against the US central bank by the US administration. Lisa Cook immediately denied the accusation and the Democrats claimed that it was an authoritarian exercise of power that flagrantly violates the Federal Reserve Act. On August 28, Lisa Cook sued the US president. Stay tuned for more.

It is extremely difficult to understand what Trump is thinking when attacks on an independent Fed are likely to drive up interest rates and inflation, pressuring the dollar and thereby further increasing the budget deficit. But as usual, there is no point in thinking rationally about irrational behavior.

Source: Kepler Cheuvreux

In April, it took a week for the president's wealthy friends to nervously point out that the stock and bond markets were in an uncontrolled spin, followed by capitulation. So far, the stock market is unaffected while the bond market is under some pressure. The difference between the American 30-year-old and the 5-year-old has risen sharply in the past week and has not been this large since 2021.

While Trump was attacking Lisa Cook, it was revealed that the FBI had raided the home of John Bolton, Donald Trump's former national security adviser and now one of his most public critics. The phrase "USA: The country of freedom" doesn't feel fitting anymore. One positive piece of news from Trump was when he suddenly announced that pharmaceuticals and semiconductors imported from the EU countries would suddenly have their tariffs lowered from 250 (!) to 15%.

A report from MIT sent the tech-heavy Nasdaq plummeting for a few days as it found that 95% of new AI pilot projects have not generated any measurable return for companies. It is a bit reminiscent of the telecom hysteria around the turn of the millennium. Paul Krugman, economist and Nobel laureate, notes that when you look back at what was said 25 years ago, it turned out to be mostly as predicted. The problem was that performance did not come quickly enough, which created enormous losses for the industry and affected development and investment for many years afterwards, with rising unemployment. The same happened in Europe, where they paid enormous sums for airspace. There may be a risk that it will be the same development this time, but there is no doubt that AI will have a very big impact on all of us in the future. Below is the development of American unemployment around the turn of the millennium.

Where will all the electricity come from? Elon Musk’s AI project Grok, with the company behind xAI, runs its data center “Colossus” with large gas-powered turbines. They were granted permission to use 15 turbines, but after inspection it was found that there were 35. This have led to significant environmental and public health problems including air pollution, respiratory problems among the population, high energy consumption and dangerous use of water. One wonders what the development and investment rate in AI will look like in Europe, given the disastrous decisions made in energy policy over the last 10–15 years which have led to higher energy costs and lower growth.

Data centers currently consume 1–2% of global electricity production, but according to MIT, this could increase to 21% by 2030. In the United States, data centers currently account for 4% of the country's electricity consumption but could rise to 12–15% by 2030. In Europe, data centers account for 2% of all energy consumption and are expected to rise to 5% by 2030. In Ireland, it is already over 20%! Back home in Sweden, electricity prices are currently at record levels due to the lack of wind and the fact that many nuclear power plants are down for repairs. How will we be able to keep up with AI developments in the future? The politicians who phased out nuclear power a few years ago have cost Sweden (especially the southern parts) enormous sums, but they continue to deny the problem and their involvement.

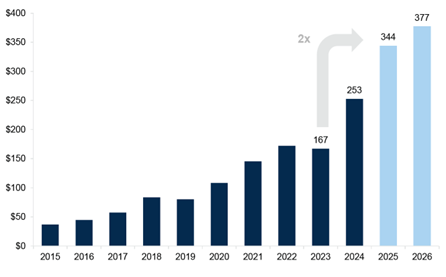

The image below shows the Mag7 companies' investments in billions of USD. The sharp increase is largely driven by increased AI investments. In 2025–2026, these seven companies will invest as much as the entire GDP of Sweden. The oldest company is Microsoft (1975) and the youngest is Meta (2003), a bit difficult to digest.

Source: Goldman Sachs

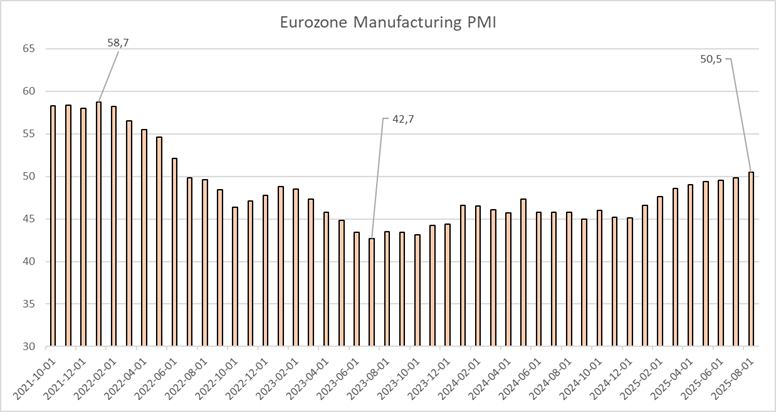

Unlike the US, inflation in the Eurozone seems to be more under control. Further encouraging news is that the PMI (activity index) is ticking up month by month, tax breaks will have an impact next year in several countries and the largest infrastructure and defense investments since World War II will soon start to appear in the statistics. In some countries, consumer confidence is now starting to rise cautiously from low levels.

Source: Coeli European, Bloomberg

Just when things were starting to brighten a bit in Europe, French Prime Minister Bayrou called for a vote of confidence. This triggered broad stock market falls in Paris and, in addition, a sharp rise in French interest rates. Our own holding in Trigano fell by 5% on the same day the news broke and has not yet recovered. Compared to the German 10-year yield, the spread is now a high 70-80 basis points which clearly reflects the increased political risk in the country.

In a country that has not had a budget surplus in the last 50 years, with a national debt of 114% and with growth that is modest even by European standards, one might think that politicians and the population could be a little humbler. But no. If things don't go their way in France, there will be fertilizers and tractors on the streets of Paris (agricultural policy) or rotten fish outside the Elysée Palace (fishing quotas) or yellow vests and complete chaos (higher retirement age). We wish the French people luck as government bondholders start to raise their voices. It's not as if France doesn't need to borrow more capital from bond investors.

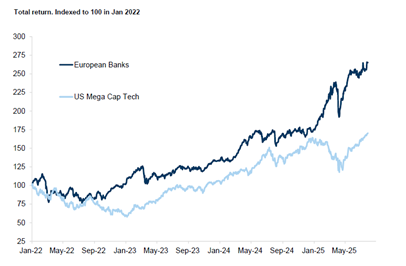

European banks continue to perform strongly, although there was some profit-taking at the end of the month.

Source: Goldman Sachs

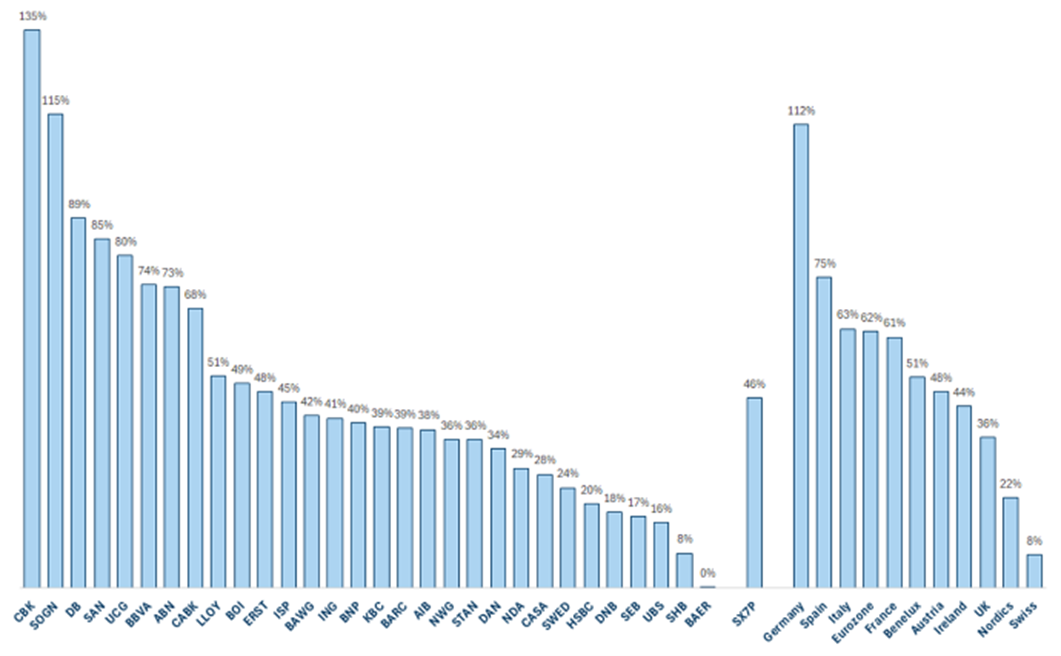

Below is the price development for the various European banks this year. Commerzbank at the top this year and we are grateful for having sold our shares during the month. We still have Austrian Bawag, + 46% as of the end of August. Also note the very strong and stable Nordic bank shares that are not at all following the sector rally.

Source: Goldman Sachs

PORTFOLIO COMPANIES

Rotork

The British manufacturer of special electric actuators delivered a half-year result that was well received by the market and us. Operating profit grew by 10% on an organic basis. Order intake stood out as strong with a growth of 6%. This in a climate where many of Rotork’s industry peers have had a tough time.

The conference call regarding the half-year report provided even more positive data points:

- Order intake in July remained strong, building on a strong finish to the first half of the year. The company has also started taking orders in data centers – a new but fast-growing area for Rotork.

- Within the company’s more traditional end-markets, Rotork has become a preferred supplier to Saudi Aramco, which is apparently difficult to achieve and represents a significant barrier to entry. This could prove to be an important parameter for Rotork’s order intake in the Middle East in the coming years.

- It has also entered a partnership with automation giant Rockwell, where Rockwell has the right to distribute Rotork’s electric actuators. Rotork is the sole supplier of electric actuators in Rockwell’s portfolio.

- Rotork is now returning to start taking orders in nuclear power, an area that Rotork essentially left completely in the years after Fukushima. Management has clearly had a rethink and now sees the nuclear market as a growth area. We, of course, hope they are right.

Rotork has a return on capital employed (adjusted for goodwill) of around 50%. The company should manage to grow by 5–10% over the long term while gradually improving margins. At a time when many industrial companies have experienced declining order intake, Rotork has managed to maintain its order intake growth. Despite this, the share is trading at a significant discount to its own history, while we believe that the company is in perhaps its best shape ever.

Rotork shares rose 6% in August and had risen, at that point, 10% for 2025.

Sampo

Sampo delivered another good report in August. Revenues were marginally higher than expected which, together with good cost control, resulted in an insurance result that was 3% higher than expected. The report was essentially free of worries (maybe that is a worry in itself?). The weather has been beneficial for the Nordic insurance companies from April to June and Sampo had no huge individual payouts in the quarter.

This quarter was the last for CEO, Torbjörn Magnusson, who was instrumental in transforming Sampo from a disjointed conglomerate into a leading player in non-life insurance. He is being replaced by Morten Thorsrud, who has been with the company for over 23 years and was most recently CEO of If.

Sampo shares rose 4% in August and had risen, at that point, 25% in 2025.

Asmodee

Asmodee released a report that far exceeded expectations, with operating profit beating consensus by almost 40%.

However, the share price did not rise. There are probably several reasons for this. First, a strong report was probably expected by the market (there are plenty of public sources to try to discern how Asmodee's games are doing between quarters). Second, it was mainly the company's distribution business that beat expectations - a business with lower margins than Asmodee-owned games. Finally, Asmodee management was relatively cautious/conservative during the company's conference call, which is not unusual for management that is new to the public market.

A few days after the report, a large placement of shares was announced from, among others, the main owner Lars Wingefors. This put further pressure on the share, which fell 7% in August.

We have a medium-sized holding after adding to our position during the month. We believe upcoming reports will be good, while a restarted acquisition program would likely please the stock market (and multiples) over time.

Van Lanschot Kempen

The Dutch private banking company has been a good holding for us during the year. A well-functioning private banking business is quite lucrative over time: Customers are typically loyal, and an aging population speaks for more inheritance and generational changes, which is positive for the industry. We believe that Van Lanschot can deliver inflows corresponding to around 5% of their managed assets on average in the coming years. If customer portfolios grow by around 5% per year, the company's managed assets could increase by 10% per year. In all its simplicity, costs should increase at a much lower rate than that, which means that profit growth should exceed 10% per year.

In addition to private banking, Van Lanschot has some income from a smaller loan book, a smaller investment banking business, and a fund business. None of these revenue streams are particularly attractive compared to the private banking business. When Van Lanschot released its report for the first half of the year in August, all deals except the fund deal were in line with our estimates. After a strong price increase during the year, the Van Lanschot share fell 9% in August, which meant that the share had risen by 20% for the full year.

Scandic

Scandic was a good contributor to the fund during August. In last month's newsletter we speculated that some of the ownership list will be replaced as the investment profile changes somewhat. Scandic is moving from being a distinct dividend stock to a growth stock, which we believe has contributed to August's rise after a relatively weak July. We took advantage of the situation that arose in July to buy more shares and believe that the details of the acquisition will become clear during the second half of the year. The share rose by almost 8%.

Bonesupport

Bonesupport was one of the fund's weaker stocks. This may have to do with short-term profit-taking after a strong July. August offered a positive news flow in our opinion. During the month it became clear that Cerament G will be granted NTAP (New Technology Add-on Payment) for open fractures. NTAP is a program within CMS (Centers for Medicare & Medicaid Services) with the aim of providing hospitals with increased reimbursement when they use new and innovative medical technologies.

The extended reimbursement is valid for three years from the first approval, which means that Cerament G for bone infections is no longer valid. This caused the market to jump, but the fact is that NTAP did not have as big an impact on the company's Cerament G sales as they initially thought. Approximately 17% of the US population is covered by Medicare insurance. Of these 17%, NTAP becomes available to about half of the patients. So, you can say that approximately 8-9% of the US population had access to NTAP. It is also unlikely that surgeons who have started using Cerament G will go back to old methods because the product is far superior. In addition, the health economic calculation for Cerament G is better than older methods, even without NTAP. Having said that there is an argument for penetration being somewhat slower.

The takeaway is that NTAP for open fractures is probably more important than for bone infections as all procedures carry a risk of infection. A surgeon no longer needs to assess whether the patient should receive antibiotics or not as the decision no longer has a financial impact on the hospitals. What we can also look forward to in the autumn is the possibility for Cerament G for bone infections to receive a permanently higher reimbursement level with new DRG codes. Odds are looking good for that. The share fell 6% during the month.

SUMMARY

We are now moving into the least popular month among the world's equity investors. Given that the summer has been relatively carefree so far, one should probably be prepared for some turbulence in the coming weeks. However, the underlying tone in the market remains positive, especially in Europe. Below is performance so far this year, the penultimate column to the right shows the performance in local currency and the last column to the right measured in USD. Note the strong excess return that several European equity markets have had compared to the US (see yellow). It is no wonder that global investors are reducing their historical overexposure to the US and increasing it in Europe.

Source: Bloomberg

Data points worth mentioning are that the sovereign wealth fund with the strongest historical returns, New Zealand, came out at the end of the month saying it would increase its weighting towards Europe. Another data point showed that the world’s global hedge fund investors would also increase their weighting in Europe at the expense of the US. The chart below shows US investors increasing exposure to the UK, Western Europe’s lowest-valued stock market.

Source: US Treasury

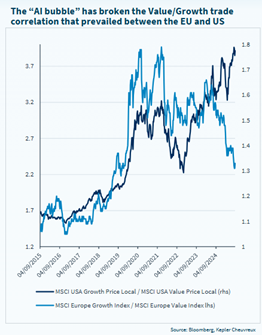

Historical relationships between the US and Europe have changed with AI. In the US, growth stocks have had the strongest performance this year, while in Europe, it has been value stocks.

Source: Bloomberg, Kepler Cheuvreux

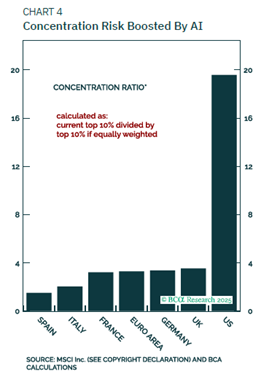

When investing in US indices, you should be aware of the concentration risk, both in the form of companies (which is at a record high) and in relation to AI, see image below. Microsoft and Nvidia are behind almost half of the S&P500's return. In Europe, the rise is significantly broader.

Source: BCα Research

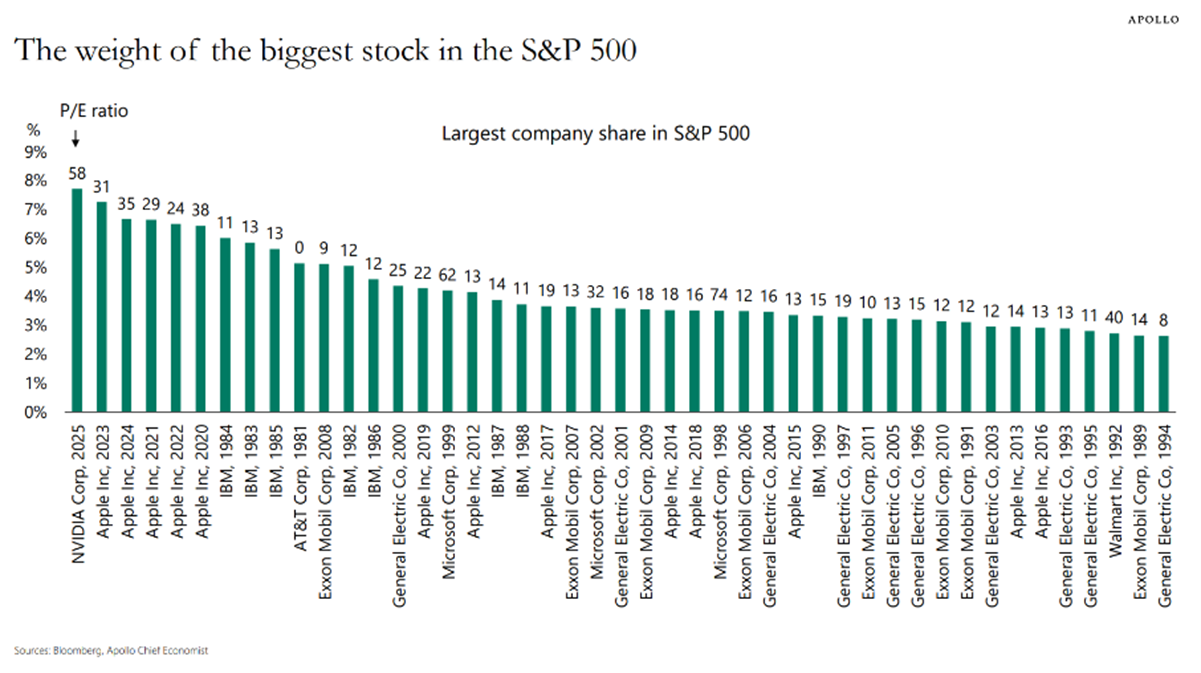

The image below illustrates which companies have historically had the largest weight in the S&P500 and what the P/E ratio has been. Never has the weight for an individual company been greater and never has the valuation of the largest company been higher. The room for margins of error is thus limited and it differs significantly from Europe, which has significantly more valuation protection in the event of a market correction.

Source: Bloomberg, Apollo Chief Economist

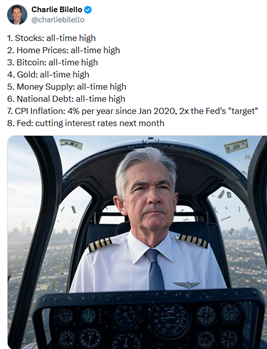

President Trump points out every day how well the American economy is doing. It is a bit contradictory that he is simultaneously attacking the Federal Reserve for lowering interest rates.

Source: X, Charlie Bilello

The Wall Street Journal recently reported strong indications that inflation in the US is starting to accelerate. We wouldn't be surprised if the Fed disappoints the market in September and leaves the key rate unchanged. The market currently sees an 87% chance of a rate cut in September.

Source: Wall Street Journal

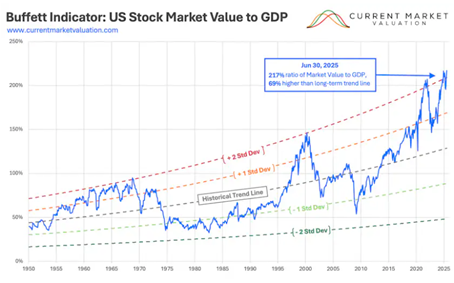

There's starting to be a shortage of oxygen up there. It's important for the American economy to develop well from here.

Source: Currentmarketvaluation.com

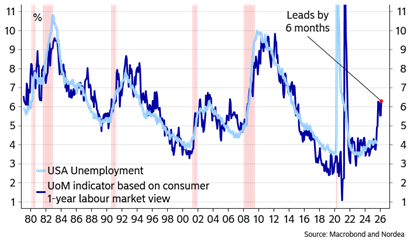

Leading indicators show that US unemployment will rise in the coming months.

Source: Macrobond and Nordea

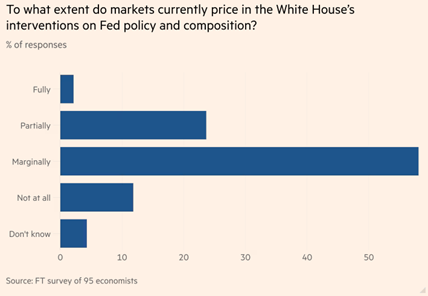

President Trump's attacks on the US Federal Reserve do not seem to have caused any major fear in the market so far (which is surprising). The Financial Times recently published a survey that showed the following:

On the topic of why no one seems to care about the valuation of the American stock market, someone quoted John Maynard Keynes and his book “General Theory of Employment, Interest and Money”. Few market participants really care about what their company is worth but instead are most concerned about what the price will be in a few months. It feels a bit like that now when it comes to the American market.

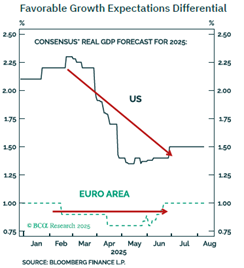

Further fuel for Europe to continue to develop stronger than the US is that the expected growth in the US has dropped significantly this year, while the opposite applies to Europe, albeit from significantly lower levels. Several years of strong growth in the US has come to a significant extent from an extremely expansionary policy with record-breaking budget deficits. This is now expected to slow down, while Europe is now starting to spend and invest for the first time in a long time.

Source: BCα Research, Bloomberg

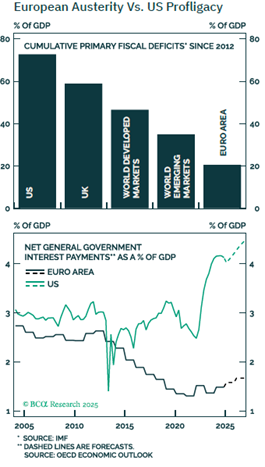

Since 2012, the US’s accumulated budget deficit is about 75%! The corresponding figure for the Eurozone is 20%. The image below shows what happens to interest expenses after such seemingly irresponsible economic policies.

Source: BCα Research, Bloomberg

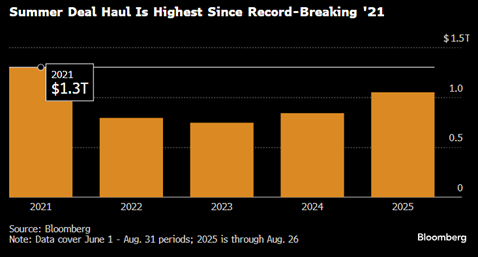

More positively, acquisitions are starting to increase and the summer offered the highest activity since the record year of 2021.

Source: Bloomberg

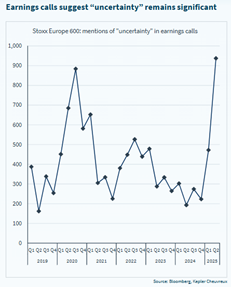

In conclusion, it can be stated that uncertainty among European companies remains high, but companies have continued to deliver.

Source: Bloomberg, Kepler Cheuvreux

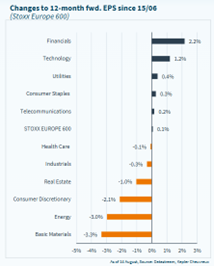

In Europe, it is banks that have had the highest upward revisions to profit estimates, while mining and steel companies have had the largest downward revisions.

Source: Datastream, Kepler Cheuvreux

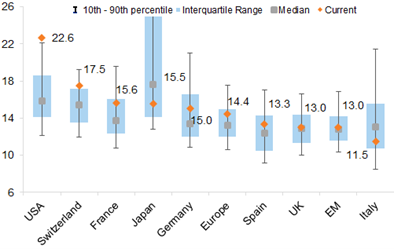

Valuation of several different stock markets. The US is valued just over 70% higher than a number of key European markets, with roughly the same expected earnings growth in 2026 (+12%).

Source: Goldman Sachs

As mentioned earlier, September is not a favorite month for the stock market, but it is rather pointless to try to forecast the development a few weeks ahead. Instead, we spend our time on company analysis, and we have meetings with many companies during September with trips to Paris and Munich booked. Below is the September return for the S&P500 over the past 30 years.

Source: Bloomberg

We thank you for your interest and wish you a continued nice late summer.

Mikael & Team

Malmö, 4th of September 2025

IMPORTANT INFORMATION. This is a marketing communication. Before making any final investment decisions, please refer to the prospectus of Coeli SICAV II, its Annual Report, and the KID of the relevant Sub-Fund. Relevant information documents are available in English at coeli.com. A summary of investor rights will be available at https://coeli.com/financial-and-legal-information/.

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested. Please note that the management company of the fund may decide to terminate the arrangements made for the marketing of the fund in one or multiple jurisdictions in which there exists arrangements for marketing.