This material is marketing communication.

Note that the information below describes the share class (I USD), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class return. The information below regarding returns therefore differs from the returns in other share classes.

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

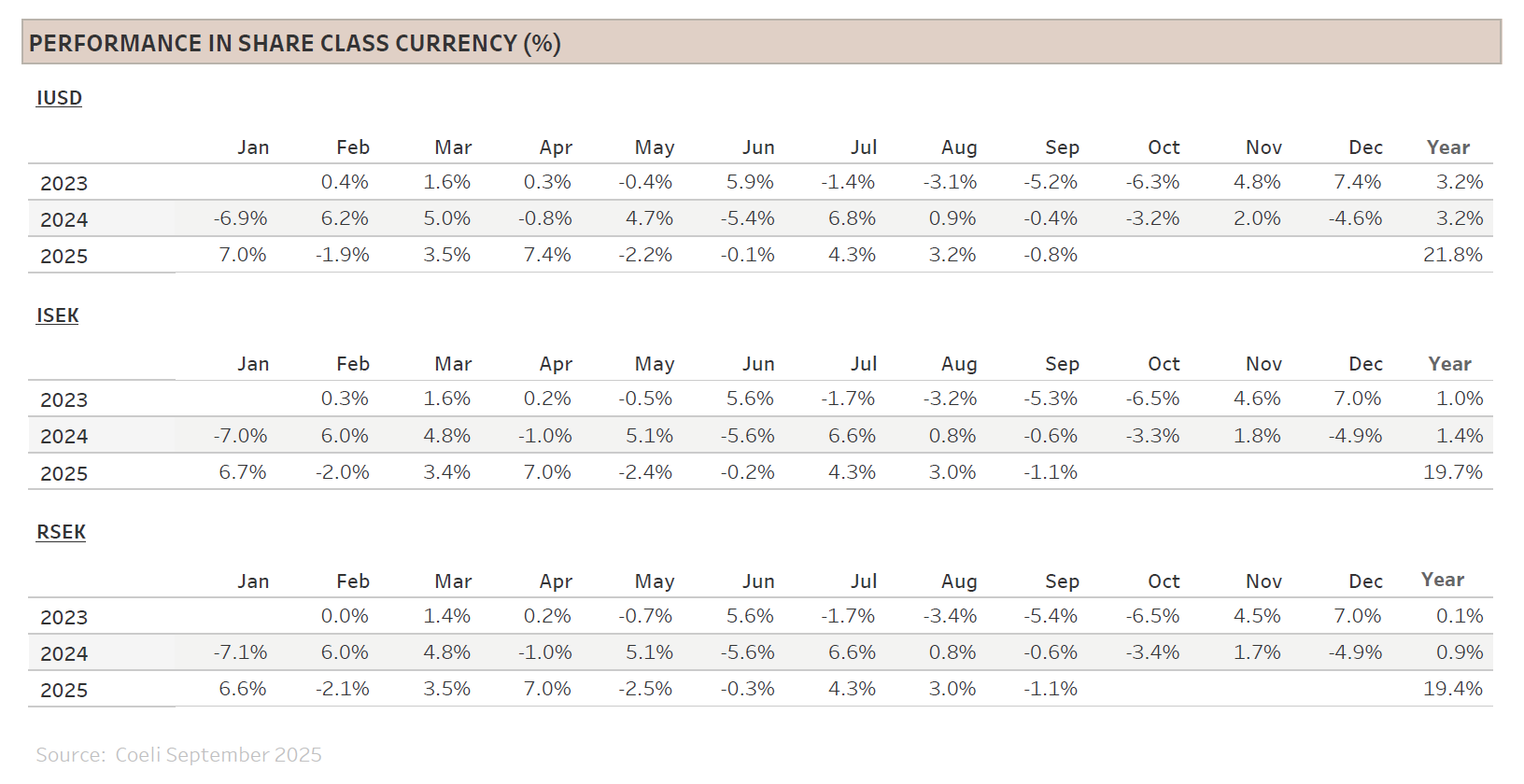

1) Share Class I USD

Performance for other share classes towards the end of the report.

FUND MANAGER COMMENTARY

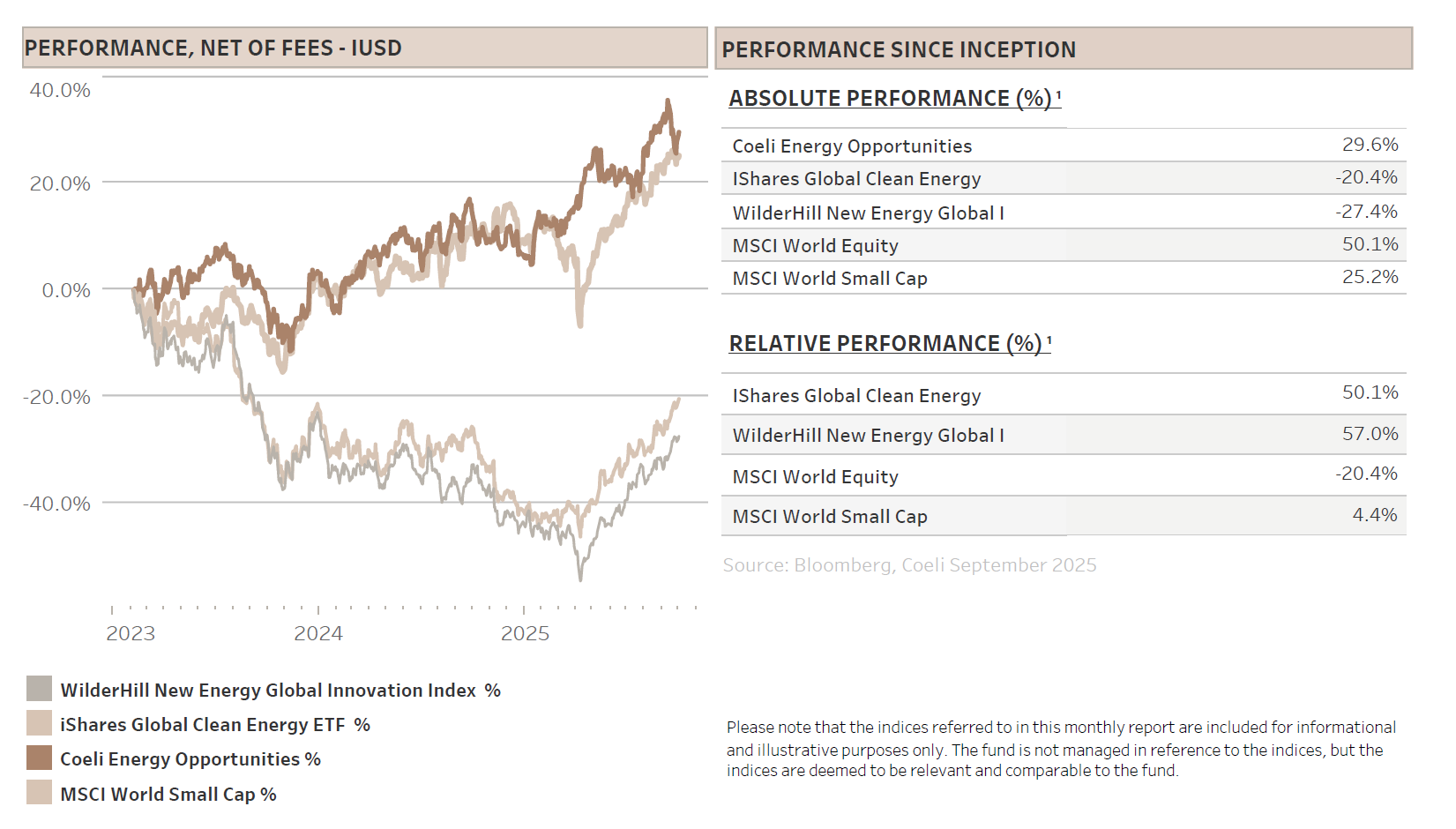

The Coeli Energy Opportunities fund lost 0.8% net of fees and expenses in September (I USD share class). Year-to-date, the fund is up 21.8% and it has gained 29.6% since inception in February 2023.

The fund underperformed the most comparable indices, the Wilderhill New Energy Global index (NEX) and the iShares Global Clean Energy (ICLN) by 7.1% and 8.4% in September. Year-to-date the fund is underperforming the NEX by 9% and ICLN by 16%. Since inception the fund is ahead by 57% and 50%, respectively.

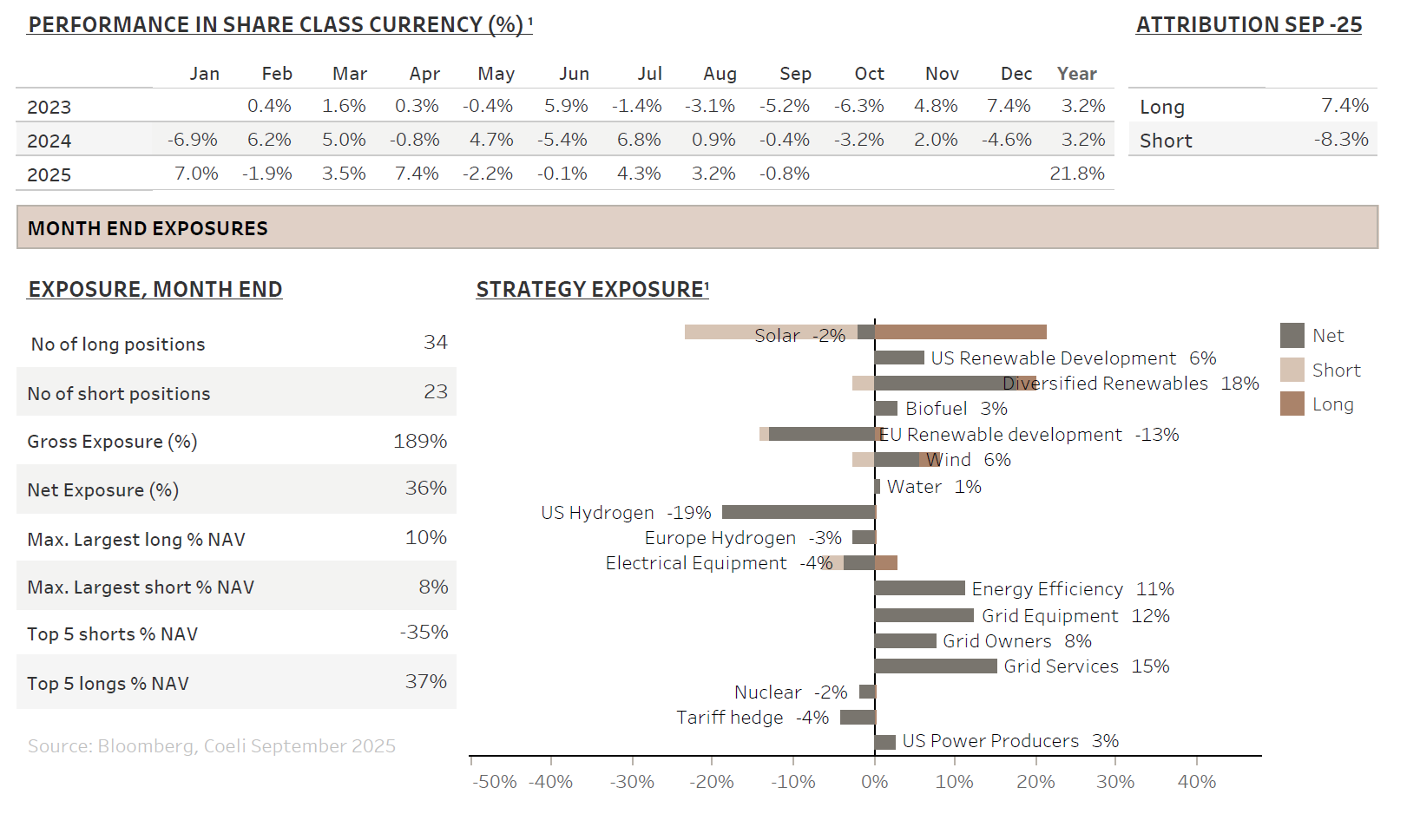

September was a challenging month for the fund. While long positions added 7.4%, benefitting from continued optimism around AI infrastructure and powering AI, the shorts lost 8.3% due to short squeezes in unprofitable small caps, especially hydrogen stocks. The initial trigger for the small cap-rally was in our view the expectation that a new FED cutting cycle has begun, but hydrogen stocks were also buoyed by the misguided narrative that hydrogen could play a role in powering AI data centres.

The two best performing themes were ‘Diversified Renewables’ and ‘Grid Services’, adding 3.0% and 1.5% to NAV, respectively. Both themes are benefitting from the continued enthusiasm around anything related to powering AI. The main contributor in ‘Diversified Renewables’ was Bloom Energy (BE), accounting for about two-thirds of the gain as the stock surged 60% in September alone, extending its year-to-date gains to nearly 300%. Bloom is the leading supplier of fuel cells and has already secured data centre contracts with a US utility and a hyperscaler.

However, Bloom’s staggering returns this year has prompted investors to search for companies with similar characteristics. Unfortunately, many retail investors appear to believe that Bloom’s former hydrogen-focused peer group from five years ago could be the next ‘AI Power’ plays. While it is true that Bloom’s fuel cells could generate electricity using green hydrogen, the datacentres will all be using natural gas. Some of these hydrogen stocks continued to soar into early October and as retail market exuberance has reached record levels, driven mainly by technicals rather than fundamentals, we have significantly reduced our exposure to the hydrogen theme. By month-end, overall net and gross exposures stood at 35% and 190%, respectively.

MARKET COMMENT – TRADING GOLDILOCKS AND ‘SILLY SEASON’?

The S&P 500 rose 3.5% in September, its strongest September in 15 years, defying its reputation as the weakest month of the year. Gains were again led by the MAG7 and other large-cap technology stocks, while the equal-weighted S&P 500 increased less than 1%. Market concentration reached new highs, with the ten largest companies now representing 39% of total market capitalization. Still, small caps also caught a bid as the Russel 2000 index gained 3.0% and set a new all-time-high for the first time since 2021.

The market currently finds itself in a classic ‘Goldilocks’ scenario: inflation appears to be under control while the labour market is soft enough to justify additional FED cuts but not weak enough to slow down the economy. Not too hot, not too cold – Goldilocks. Tariffs and government shut down are not issues the market worry about right now.

Meanwhile, the AI investment boom continues to accelerate. Expected hyperscaler capex is roughly 30% higher than at the start of the year and the capex only from the five largest companies accounts for more than 1% of US GDP or about 7% of investments in 2025. We will delve deeper into this theme later, but this wave of AI-driven capex is acting as a significant economic stimulus and will likely be the key macro factor to monitor for the rest of 2025 and into 2026. Any potential “crack” in AI optimism seems more likely to materialize in 2026 than this year, though.

Moreover, despite inflation remaining above FED’s target and unemployment below historical averages, the bond market anticipates at least four more FED cuts over the next 12 months. Combined with front-loaded fiscal stimulus from record-high government deficit and surging AI investments, there is a growing risk monetary easing could overheat the economy. We are already witnessing froth in equity markets as retail participation in early October reached all-time highs and retail traders now dominate the options market with zero-day-to-expiration call options. Furthermore, most major indices sit at record levels while many unprofitable stock laggards have risen several hundred percent in weeks despite no improvement in fundamentals. In many ways it is starting to resemble the meme-rally in late 2020/2021.

Meme-rallies always end in tears, but timing the conclusion of the current ‘silly season’ remains challenging and difficult. As many of the largest risks on the horizon are rather 2026 events, we believe conditions are favourable for a continued rally into year-end. Accordingly, we have significantly reduced shorts and increased net exposure in early October.

ARE WE IN AN AI BUBBLE?

“It feels like a bubble to me.” - Jeff Bezos, September 2025

To be clear, Jeff Bezos is not claiming that AI technology lacks substance or long-term value. In fact, he believes AI is authentic, ‘going to change every industry’, and will deliver ‘gigantic benefits’ to society over time. However, he argues that AI is experiencing an ‘industrial bubble’ driven by investor exuberance and draws parallels to the investment frenzy of the IT-bubble.

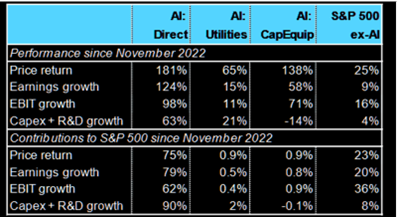

Let’s examine the facts. J.P. Morgan reports that since the launch of ChatGPT in late 2022, AI related stocks have contributed roughly 75% of S&P 500 returns, 80% of earnings growth, and 90% of capital spending.

Comparison to the IT-bubble

AI is undeniably a major force in the stock market, but is the comparison to the IT bubble justified? Possibly.

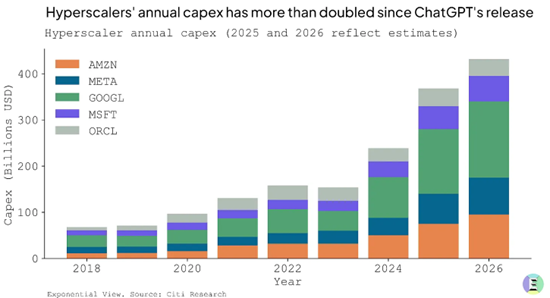

First, a key metric to monitor is hyperscaler capital expenditures. The five largest technology companies are set to spend nearly USD 400bn on AI data centres in 2025, representing an increase of approximately 60% over last year. Strikingly, according to Harvard economist Jason Furman, US GDP growth would have been just 0.1% in the first half of 2025 without investment in “information processing equipment and software”. This segment alone, where hyperscalers account for a large share, was responsible for 92% of GDP growth during that period. Forecasts for the top five tech companies’ capex indicate an additional 15-20% growth in 2026. Since previous projections have consistently underestimated spending, and with data centre announcements accelerating in recent months, these figures could ultimately be even higher.

Is this level of spending excessive? It is uncertain, but unlike during the IT bubble, the investments today are financed by the world’s largest and best-capitalized corporations. These companies can literally ‘afford’ to burn some hundreds of billions of dollars in the pursuit of Artificial General Intelligence (AGI).

Second, can it truly be a bubble when demand for compute power vastly exceeds supply? During the fibre optic build-out of the late 1990s and early 2000s, only a fraction of the installed capacity was utilized after the bubble burst in 2000-2001. Today, data centres cannot be built quickly enough to meet demand. For example, Oracle (ORCL) recently reported Remaining Performance Obligations (RPOs), i.e. revenue booked but not yet recognized, of USD 455bn, up 359% year-on-year, a staggering acceleration compared to 41% growth in the previous quarter. Supply simply cannot keep up with demand, at least not yet. Importantly, the limiting factor is not just computer chips but increasingly long-term access to power, as highlighted in our March-24 report “Roadblocks on the AI highway” and reiterated this summer by former Google CEO Eric Schmidt. Given the time and complexity involved in generating large amounts of new energy, compute power may remain in short supply for some time.

There are other distinct differences from the IT bubble. Hyperscalers now bear a large portion of the investment burden, boasting robust balance sheets, solid earnings and strong cash flows. While their market capitalizations are in the trillions, their valuations are generally reasonable considering projected earnings growth.

Concentration risk is excessive

However, the concentration risk for equity investors is greater than ever. The ten largest stocks, which are all technology companies, now comprise 39% of the S&P 500, which itself represents over half of global equity markets, meaning these ten tech companies account for roughly 20% of total global market capitalization. This concentration is striking and clearly amplifies systemic risk, making any weakness in AI a risk to investment portfolios worldwide.

Is a bubble brewing?

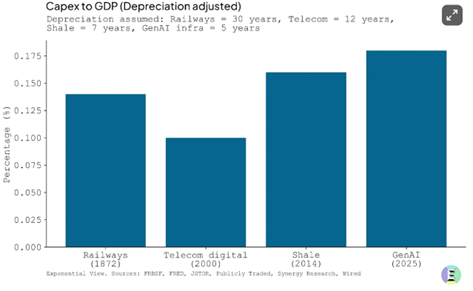

What is the likelihood that spending on AI data centres is excessive, blowing up a bubble? The odds are not insignificant. Comparing the current AI build-out to historical booms like the railway mania of the 1800s and the IT-bubble of the 1990s, AI capital expenditures relative to GDP already surpass those earlier booms.

Overbuilt infrastructure is historically rather a feature, not a bug of transformative infrastructure spending cycles. Despite severe investor losses in past booms, society reaped lasting benefits. One concern, though, is that most AI investment flows into data centres, where about 60% of the costs consist of fast-depreciating GPUs. This implies that much of the invested capital dissipates quickly, unlike railways and fibre networks, which continued to benefit society long after the initial bust.

Signs of financial engineering are emerging. While not yet matching the scale seen during the IT-bubble, these developments are nonetheless noteworthy. First, hyperscalers have quietly extended GPU depreciation schedules, from 3–4 years in 2020–21 to 5–6 years now, stretching costs over a longer period and boosting reported earnings. This adjustment has played a significant role in their consistent earnings beats. Hyperscalers justify the change by claiming that, as we transition into the age of inference, the useful life of GPUs is extended as these depreciated advanced GPUs for learning models can be repurposed for inference. However, this rationale remains highly uncertain, especially as Nvidia moves to near-annual upgrade cycles, rendering such accounting adjustments increasingly questionable amid a heightened investment boom.

Second, innovative off-balance-sheet financing is being used to fund data centres. For example, Meta’s latest data centre (USD 29bn) is leased from a Special Purpose Vehicle (SPV) owned by private credit infrastructure funds charging 200–300 basis points more than Meta could have secured with traditional on-balance-sheet debt. While this structure keeps liabilities off Meta’s balance sheet, it also disperses risks beyond the company itself, potentially to society at large.

Third, vendor financing is back. Nvidia’s recent pledge to invest USD 100bn in OpenAI through a vendor-financing arrangement is reminiscent of late-1990s telecom excesses. OpenAI has even confirmed that much of the funds will return to Nvidia. Maybe more concerning is OpenAI partnership with AMD to deploy chips for up to USD 100bn paid for by AMD granting OpenAI warrants that can be monetized as milestones are reached. Such circular financing did not end well a quarter-century ago when the IT- bubble burst.

Ultimately, these are only signs of a potential bubble. As with the IT-bubble, the crucial test for AI investments will be their returns. The internet bubble burst when market focus shifted from spending to realized profits. For AI, equity markets are still in the “easy” phase: the more spending is promised, the higher revenues and profits are extrapolated, driving share prices upward. However, attention will soon turn to actual AI revenues and ROI, and disappointing results could abruptly end the rally.

AI is the key macro driver

AI is now the most important macro driver for equity markets. While AI is poised to have a transformative impact and improve productivity, it remains uncertain whether the returns will benefit investors broadly or be socialized, as in many previous investment booms. Regardless, like all asset booms, there will be winners and many losers, providing abundant opportunities for long-short hedge funds that can ride the winners and also profit from a potential decline when ‘there is nowhere else to hide’.

FUND PERFORMANCE – IMPACTED BY ‘MEME’ SHORT SQUEEZE

September was marked by a dramatic intensification of speculative trading in US ‘meme-like’ stocks, a trend that accelerated sharply in the second half of the month and into October. US stocks experienced the largest notional retail buying on record, with social media behaviour mirroring the GameStop short squeeze of early 2021.

Approximately 60% of our investment themes delivered positive returns, led by ‘Diversified Renewables’, which added 2.8% to NAV. ‘Grid Services’ also performed well, contributing 1.2%, driven by Mastec (MTZ), which gained 17% over the month.

However, several of our long-held hydrogen short positions were targeted in the ‘meme-squeeze’, with both hydrogen-related themes detracting a combined 5.2% from monthly performance. While we expected that smaller companies and laggards might start catching up to broader AI driven market gains, the steep rallies in stocks entirely unrelated to AI took us by surprise. For example, Blink Charging (BLNK), an EV charging company in which the fund is not involved, is currently up 175% from its August lows.

Over our careers, we have experienced well over hundred short squeezes and generally avoid reducing exposure at the slightest hint of a squeeze. Locking in losses is rarely in the best long-term interest of investors. Indeed, the fund’s strategy is to tolerate somewhat higher volatility to generate higher returns over time. Nonetheless, while we believe last weeks’ price moves were irrational and not fundamentally anchored, the momentum in the squeeze was too strong and the exposure grew too quickly. As John Maynard Keynes famously stated, “The market can stay irrational longer than you can remain solvent”. Accordingly, we reduced our exposure and will revisit when fundamentals again matter.

Our position in Bloom Energy (BE), part of the ‘Diversified Renewables’ theme, helped offset some of the hydrogen related losses, as Bloom is also heavily shorted and benefitted from the meme-rally. Importantly, we do not consider Bloom to be a ‘meme- stock’ as it is genuinely one of the companies the most exposed to the ‘powering AI’ thematic. With several contracts already secured, the company offers a cleaner and more readily deployable alternative to gas turbines for data centres.

Additionally, Bloom is the market leader, currently facing limited competition in solid oxide fuel cells (SOFCs). Unlike Proton Exchange Membrane (PEM) technology, SOFCs can operate on natural gas, a requirement for data centre operators. Contrary to some suggestions circulating on Reddit and Twitter, hydrogen companies offering PEM fuel cells or electrolysers for green hydrogen production do not have relevant offerings for powering data centres.

Looking forward, we remain optimistic about grid infrastructure and power market segments, but continue to closely monitor for signs that the AI “bubble” could burst.

Thank you for your continued trust, and we look forward to updating you again next month.

Sincerely

Vidar Kalvoy & Joel Etzler

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

- Portfolio Manager and Founder of the Coeli Energy Opportunities Fund.

- Over 15 years of investment experience spanning both public markets and private equity.

- Managed the Coeli Energy Transition Fund from 2019 to 2023.

- Spent six years at Horizon Asset in London, a market-neutral hedge fund.

- Started working with Vidar Kalvoy in 2012.

- Five years in Private Equity at Morgan Stanley.

- Began his investment career in the technology sector at Swedbank Robur in Stockholm in 2006.

- Holds an MSc in Engineering from the Royal Institute of Technology (KTH), Stockholm.

- Portfolio Manager and Founder of the Coeli Energy Opportunities Fund.

- Has managed energy equities since 2006 and brings more than 20 years of experience in portfolio management and equity research.

- Managed the Coeli Energy Transition Fund from 2019 to 2023.

- Head of Energy Investments at Horizon Asset in London for nine years, a market-neutral hedge fund.

- Experience from energy investments at MKM Longboat in London and equity research in the technology sector in Frankfurt and Oslo.

- Holds an MBA from IESE in Barcelona and a Master’s in Business and Economics from the Norwegian School of Economics (NHH).

- Before entering finance, he served as a lieutenant in the Royal Norwegian Navy.

IMPORTANT INFORMATION. This is a marketing communication.

Before making any final investment decisions, please refer to the prospectus of Coeli SICAV II, its Annual Report, and the KID of the relevant Sub-Fund. Relevant information documents are available in English at coeli.com. A summary of investor rights will be available at https://coeli.com/financial-and-legal-information/.

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

Please note that the management company of the fund may decide to terminate the arrangements made for the marketing of the fund in one or multiple jurisdictions in which there exists arrangements for marketing.