This material is marketing communication.

Note that the information below describes the share class (I SEK), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class’ return. The information below regarding returns therefore differs from the returns in other share classes.

Before making any final investment decisions, please read the prospectus, its Annual Report, and the KID of the relevant Sub-Fund here.

OCTOBER PERFORMANCE

The fund’s value increased by 1.3% in October (share class I SEK), while the benchmark increased by 1.1%. Since the change of the fund’s strategy at the beginning of September 2023, the fund’s value has increased by 26.1% compared to an increase of the benchmark by 22.7%.

Source: Coeli European

* Adjusted for spin-off of Rejuveron

** Includes September 1 (strategy change to long-only implemented September 4 2023)

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

EQUITY MARKETS / MACRO ENVIRONMENT

History did not repeat itself in the sense that October is usually a weak stock market month. While the month saw one of the worst stock market days since April, it was an unusually eventful month that featured renewed political turbulence in France, US threats of sharply higher tariffs on China (which were withdrawn a day later), a sort of banking panic in the US which spilled over to Europe when smaller regional banks suddenly plunged on the US stock market, Fed interest rate cut, ceasefire in Gaza, first meeting since 2019 between the presidents of China and the USA and to top it off a slew of company reports that on the whole have been unexpectedly strong so far.

By the end of the month, the broad European index had risen by 2.5% compared to the S&P500, which rose by 2.3%. For the year, the SXXP600 has risen by 12.7% compared to the S&P500, which rose by 16.3%. Europe has had a significantly stronger year measured in dollars as the SXXP600 has risen by a whopping 24.9%. For smaller companies, the MSCI European Small Cap rose by 1.9%.

After a weak start with constrained market liquidity, the fund began to perform as reports rolled in. So far, 67 % of our companies, measured in capital, have reported and the outcome has been in line or better on 13 out of 17 occasions. The fund rose by 1.3% in October compared to the benchmark, which rose by 1.1 %, and we are generally satisfied with our performance and that of our companies.

We were active ahead of Verisure's IPO on October 8th and the fund received a good allocation. In the first hour we had already built up a new core holding for the fund and it is a good example of where (we think) our strong and quick analytical capacity can give us an edge over the broad market. Asker was a similar example this spring. The strongest contributors in October were Konecranes, Continental and Lindab. The weakest contributors were Bonesupport, Babcock and Viscofan.

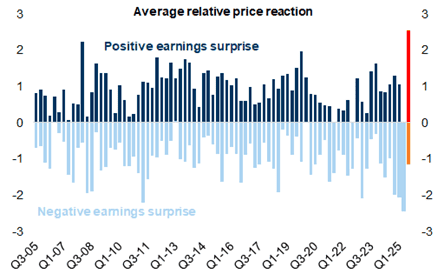

The market has been unusually generous; rewarding companies that beat expectations with positive share price developments.

Source: Goldman Sachs

Results in Europe compared to expectations.

Source: Goldman Sachs

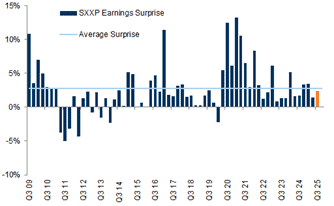

Downward revisions to earnings estimates in Europe have stabilized in tandem with EUR/USD.

Source: Goldman Sachs

There is a large difference in profit adjustments between companies with a high proportion of domestic sales (dark blue) and companies with high exposure to the US (light blue).

Source: Goldman Sachs

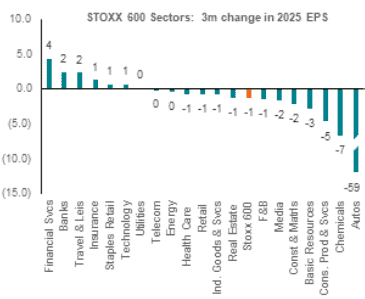

Profit expectations in Europe have fallen marginally, but European automakers are having a tough time, to say the least.

Source: BNP Paribas

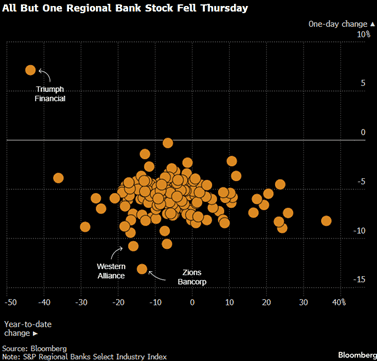

The rapidly emerging American banking crisis put considerable pressure on the share prices of regional banks for a short period of time, see the picture below. This spread to European bank shares and our holding in Austrian Bawag fell at most 8% on Friday, October 17. We took the opportunity to buy more shares.

Source: Bloomberg

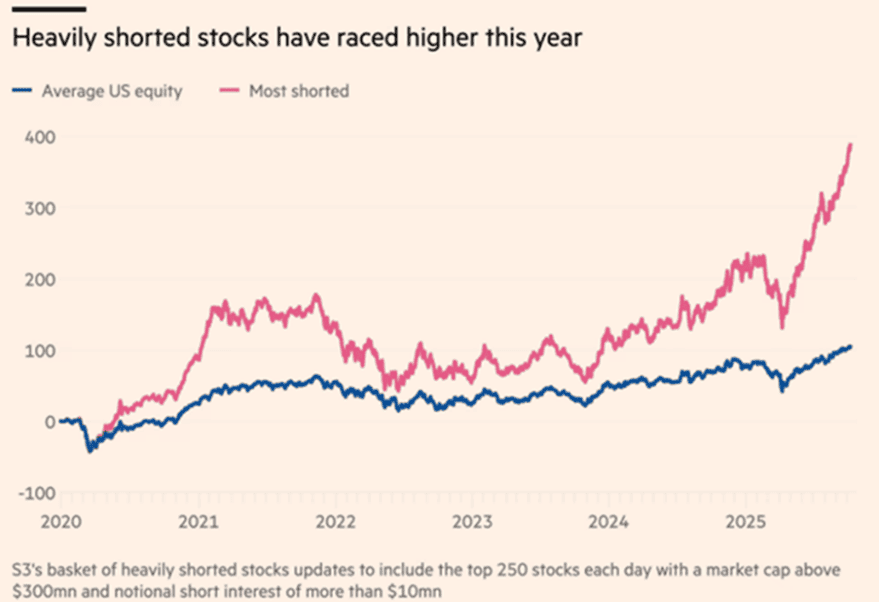

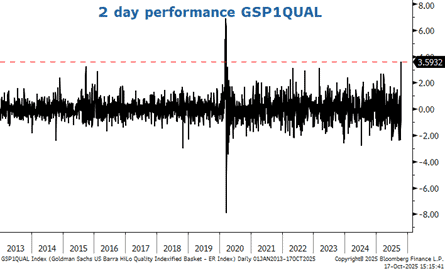

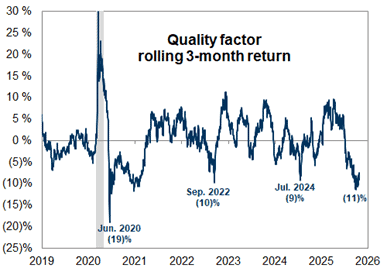

A clear trend during the year, and especially since this summer, is that quality companies have performed worse than riskier investments with lower quality. This is also something the fund has felt markedly in recent months and may be due to investors' hopes that a quick macroeconomic recovery will benefit companies with the highest leverage. We are convinced that this will correct itself.

We are grateful that we are no longer taking short positions, see image below.

Source: Financial Times

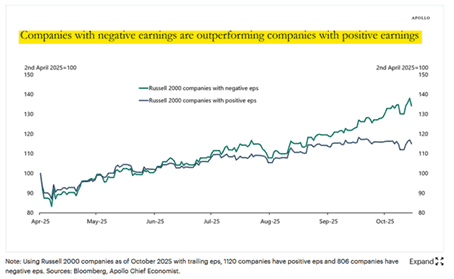

Below is the development for profitable American small companies compared to those that have no earnings. Unprofitable companies have clearly been rewarded since late summer.

As mentioned at the beginning, the fund's performance was weaker during the start of the month. It is noticeable that the fund's performance fluctuated around Thursday, October 16, when quality companies had the second strongest single-day return measured since 2013, compared to lower-quality companies.

Source: Bloomberg, Godman Sachs

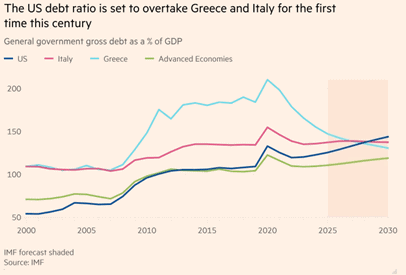

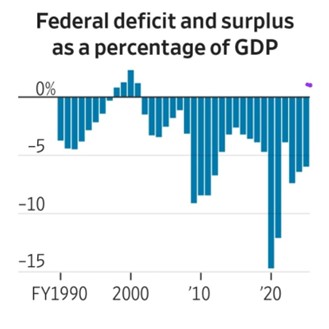

There is much to complain about in Europe, with its slowness, regulations and poor budgetary discipline. However, in the latter area, the US is well on its way to becoming a new “champion” and there is little to suggest that the current administration will become more restrained.

Source: Financial Times, IMF

The US has not had a positive budget surplus since 2001.

Source: X

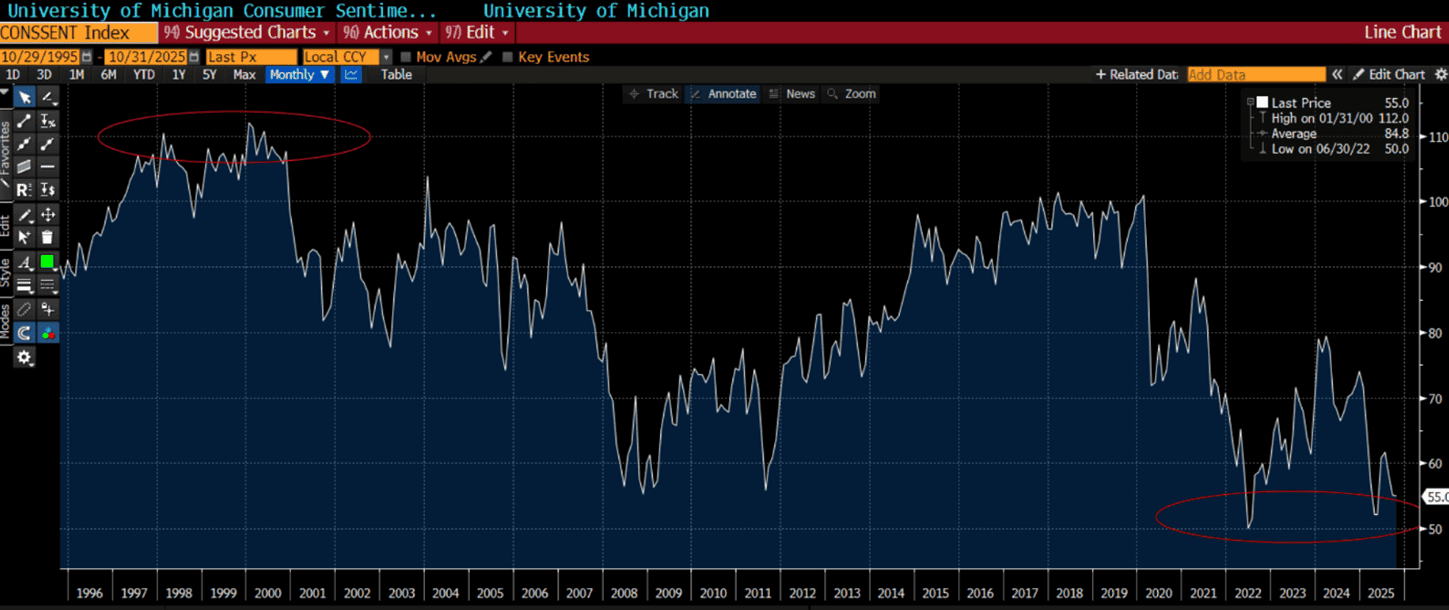

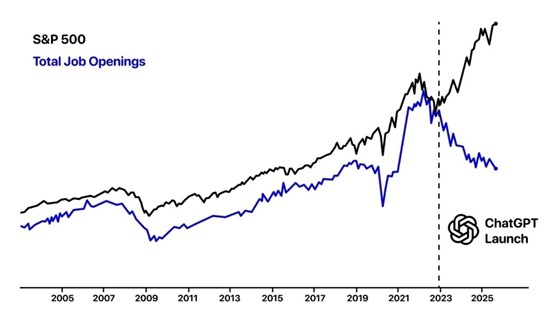

Below is an interesting graph showing the development of the US consumer sentiment index over the past 30 years (probably the same in Europe). The mood was at its peak during the internet hysteria around the turn of the millennium, while today, despite three years into a strong stock market, it is considerably gloomier. This is probably because the differences in society have increased dramatically and those at the top of the wealth ladder are doing just fine while those at the bottom experience the opposite as they are unable to join the party.

Source: Bloomberg

An interesting, if somewhat gloomy picture.

Source: X

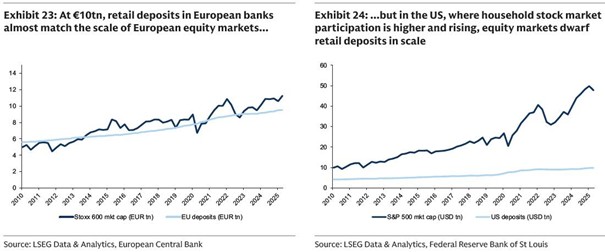

The equity culture in the US is on a different level compared to Europe where the combined assets of private individuals in tired bank accounts equal the value of the European stock markets. In the US the difference is 6-7x greater in favour of the stock market. That says a lot about a lot.

Source: Goldman Sachs

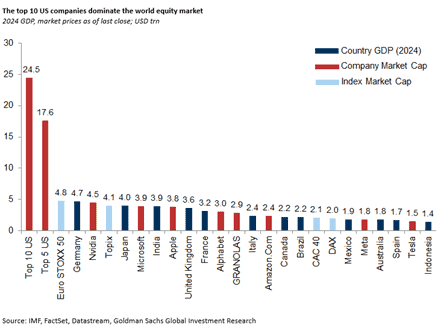

The strong American equity culture has contributed to the following development. The 10 largest American companies account for a quarter of the value of all the world's stock markets. Breathtaking and almost dizzying when you study the picture.

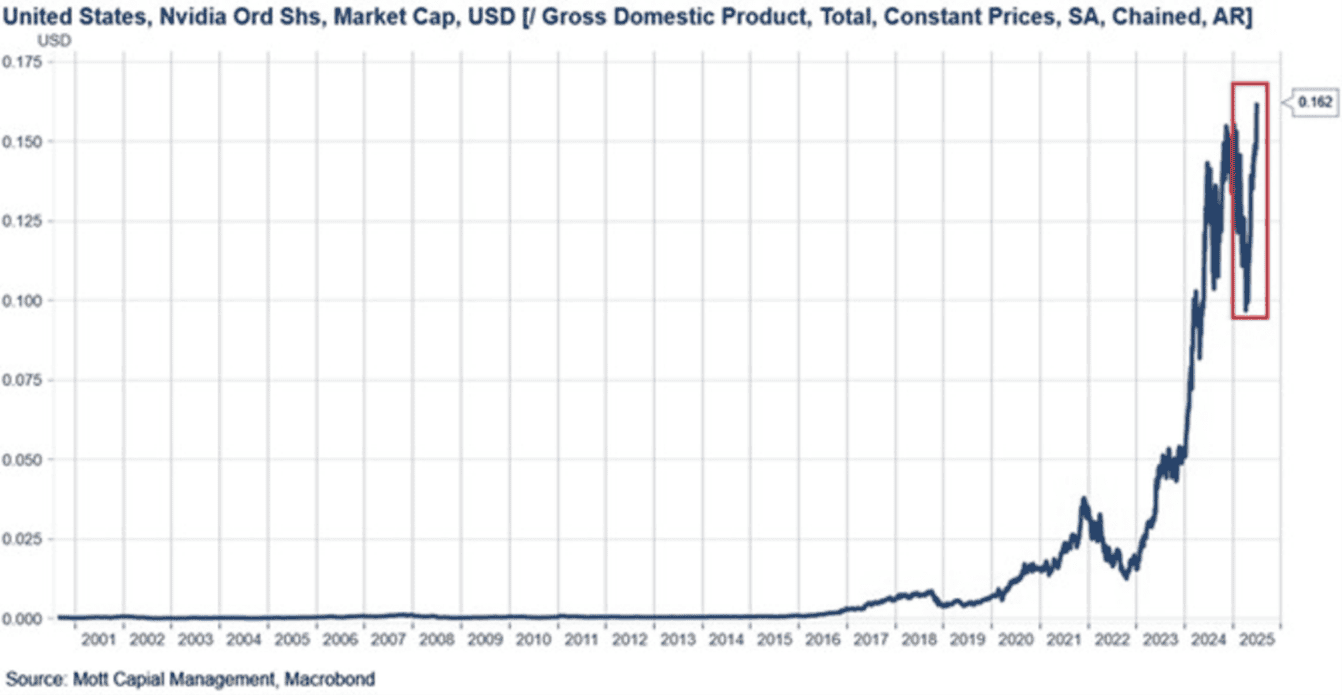

An even more breathtaking picture, if possible. Nvidia's current market capitalization of approximately USD 5 trillion now corresponds to 16 % of US GDP...

Source: Bloomberg

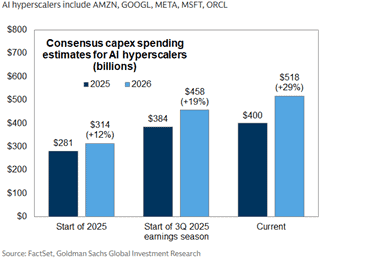

AI investments for major US tech companies are skyrocketing, see image below including timeline. No one wants to be left out, but many companies will likely get burned in terms of return on their investments.

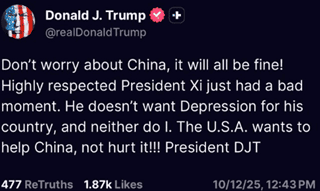

After scaring the world's investors on a Friday afternoon in the middle of the month, sending stock prices plummeting, President Trump managed to calm the masses over the weekend. By Monday, everyone was happy again, and more than half of the decline had been reversed.

Source: Truth Social

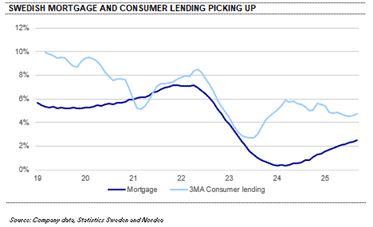

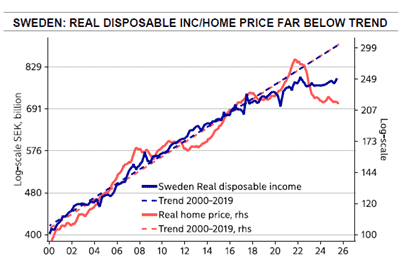

In Sweden, which looks to be among the first European countries to emerge from the recession, consumers are now increasing their housing and consumer loans.

Tax cuts on income and food, and lower interest rates, are a nice lubricant for the Swedish consumer, who has experienced an extremely bleak and rare development of disposable income in recent years. It was also pleasing to see that Swedish GDP grew by 2.4 % in the third quarter, where expectations were 1.6 %.

Source: Nordea

The Nobel Peace Prize went to Venezuelan opposition leader Maria Corina Machado.

Source: X

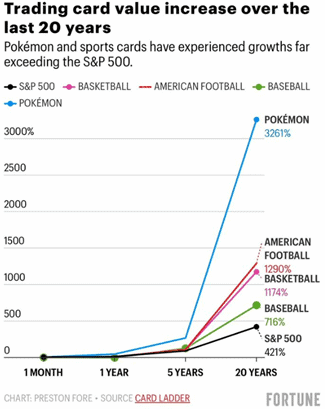

One should have taken a long position in Pokémon cards instead of sitting and analysing companies. Having said that, a little spills over onto us as the fund has a large position in Asmodee, which distributes Pokémon cards in certain markets.

Congratulations Javier Milei! From chaos to a budget surplus in Argentina for the first time in many years and great success in bringing down extremely high inflation. However, much remains to be done.

Source: Financial Times

PORTFOLIO COMPANIES

Beijer Ref

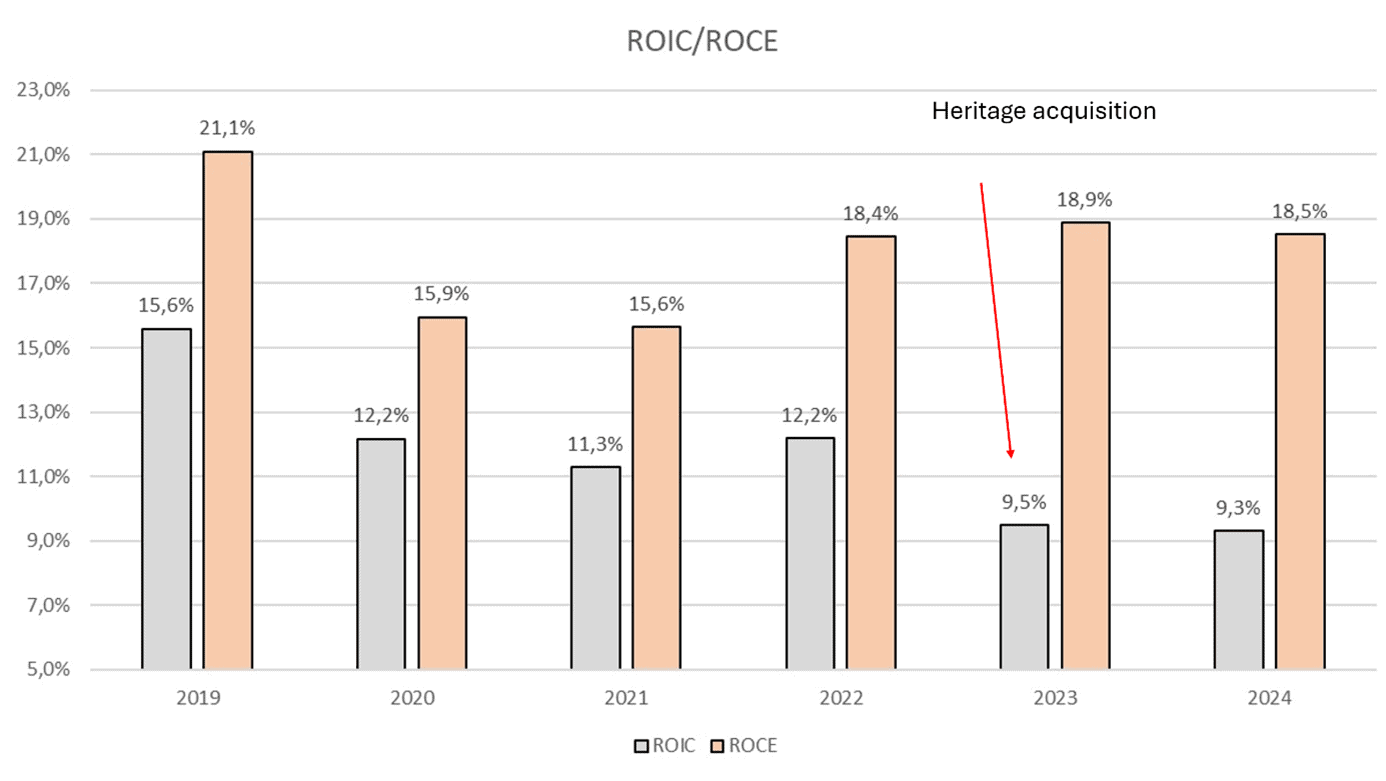

Since the summer, the fund has gradually built up a larger position in the Swedish HVAC and refrigeration distributor Beijer Ref. The Beijer Ref share has long been a favorite among Swedish fund managers. The structural drivers are easy to understand: regulatory tailwinds should drive good organic growth in the refrigeration segment, while increasingly higher temperatures should drive the HVAC leg. On top of this, there is a well-motivated and well-thought-out acquisition strategy. Good organic growth and an active acquisition leg have meant that Beijer Ref now has a long history of double-digit profit growth, which has of course been appreciated by the market.

In recent years, however, we have watched Beijer Ref's development from the sidelines. The valuation has, for the most part, looked high. Acquisition activity, an important factor for profit growth and thus the future share price, has been low from a historical perspective for a period. Meanwhile, we have seen how the company's return on capital has had a downward trend, primarily driven by the company tying up more and more working capital. We now see an improvement in all these areas.

Although Beijer Ref had improved its operating margins from 8–9% to 10–11% from 2019 to 2024, the return on capital employed had not improved according to our calculations. The main reason was Beijer Ref's tying up of working capital. From 2019 to 2024, working capital as a percentage of sales had risen from 27% to 40%. In 2023, a major platform acquisition was also completed in the US, Heritage, which negatively affected the return on invested capital (including goodwill).

Source: Beijer Ref, Coeli European

The high level of tied up working capital was largely driven by supply disruptions caused by the pandemic and the war in Ukraine. In other words, factors outside Beijer Ref's control. But our impression has also been that tied up working capital has not been a major priority historically for Beijer Ref as a company. We believe that this has changed now with Christopher Norbye as CEO. In 2025, we have seen clear improvements in inventory management and the number of days that the company's accounts receivable is outstanding has also decreased. This should result in improved return on capital employed in the future. This year, cash flow has strengthened significantly. During the first 9 months, we estimate that free cash flow has increased by more than 50% compared to 2024.

Source: Beijer Ref, Coeli European

Beijer Ref is seen as a serial acquirer that has historically created significant value by acquiring smaller distributors and then extracting synergies in special purchasing. Since the summer of 2024, however, the acquisition pace has been low from a historical perspective. Serial acquirers that lose pace tend to underperform in the stock market. However, we now sense a change in that regard. During the month, an acquisition was announced in the Baltics and during the conference call for the third quarter, management was clear that they expected significantly higher activity, even as soon as in the fourth quarter.

The Beijer Ref share has largely been trading sideways since mid-2021. In 2021, earnings per share were SEK 2.34 and for 2025, analysts expect earnings per share of SEK 4.78. When valuations were at their wildest towards the end of 2021, the Beijer Ref share was valued at around EV/EBIT 40-45x on a one-year forward-looking estimate. Today, the share is more likely valued at around EV/EBIT 21x. It may not be a bargain in absolute terms, but in our opinion, it is appealing for what we see as a quality company that should be able to grow its profits by double digits for many years to come. The valuation also does not consider future acquisitions, which are not included in the estimates.

In October, Beijer Ref released a Q3 report that was marginally better than expected in terms of results. A deep dive reveals that there was much to be happy about. The organic growth of 5% was higher than expected. In particular, the organic growth of 6% in the US was better than many had feared, after a few OEM players in the HVAC industry reported weak reports. In addition, the free cash flow was strong and, as mentioned, we received positive comments regarding upcoming acquisitions.

Despite what we see as a fine report, the share has not really performed during the month. Many seem to be on the sidelines waiting for a placement from EQT, who owns 8% of the shares in the company. We have no idea when and how a placement will take place, but once it does, we guess that the share will do well.

The Beijer Ref share rose 3% during the month and is down 8% for the year.

Konecranes

Konecranes delivered a fantastic Q3 report. Order intake beat expectations by just over 20%, while operating profit was 16% better than expected. All business areas contributed nicely. The market has previously been concerned that next year will lack growth considering the order book having fallen slightly at the end of the first half of the year. After this report, it has instead expanded by 6% compared to the end of 2024.

The order book suggests that 2026 will be another year of growth for Konecranes, which has improved significantly as a company in recent years. Return on capital employed has improved from around 15% 10 years ago to 35–40% today, according to our calculations. The company's service business, which accounts for 60–70% of operating profit, is growing at a rapid pace and should contribute to the group's profitability improving over time. In the quarter, Konecranes took large orders from the defense industry, nuclear power industry and aerospace industry – in short, hot markets that we do not believe will lose momentum in the coming years.

Source: Konecranes, Coeli European

Our thesis is that tariffs will ultimately have a positive impact on Konecranes, as changing logistics chains should increase demand for Konecranes' products. Recently, the US has also imposed 100% tariffs on Chinese ship-to-shore cranes, which will benefit Konecranes' competitive position in a segment with significant Chinese dominance. In addition, there are proposals for tariffs equivalent to 150% on several other port-related cranes where Konecranes could potentially benefit.

Konecranes' main listed competitor in the industrial segment, Columbus McKinnon, reported recently. The company raised its guidance for the year, which together with better-than-expected results sent the share up 15% on the reporting day. McKinnon mentioned, among other things, that the cycle in the US is now looking better. Order intake in the US rose by 11% for McKinnon.

Our estimates are that the company is trading at around EV/EBITA 9x in 2026. That is hardly expensive. In our opinion, Konecranes should be rewarded with multiples that are closer to quality Swedish industrial companies which are more likely to trade around 15x operating profits.

The share price rose 22% in October and is up 40% this year.

Lindab

Lindab delivered an operating profit that was a few percent better than expected. We are now probably sensing better end markets, especially for the important ventilation segment. Lindab had positive organic growth in several markets in Europe. However, things are still slow in Sweden and Germany. If those markets turn around while the rest of the ship remains intact, we could probably see fairly good organic growth next year. After several years of cost cuts, volume growth can provide very nice incremental margins.

The Lindab share rose 15% in October and is down 1% for the full year.

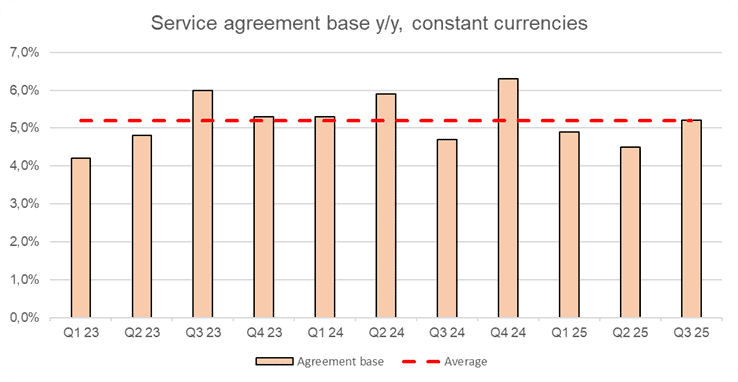

Volution

During the month, our largest holding released its financial statements for the financial year ending in July, after previously announcing preliminary figures. The group's organic growth was 6% (from previously mentioning a little over 5 %), of which volume growth was five percent. The UK market has been especially strong for Volution, where regulatory tailwinds have provided good growth in an otherwise weak construction market. Several markets in continental Europe are also showing signs of improvement.

Volution shares rose 4 % in October and were thus up 17 % for the full year.

Continental

Continental is a German industrial company active in automotive components and tire production. We analyzed the company during the summer when it became known that it would spin off its automotive components division, Aumovio, which happened in September. In 2026, the company is expected to sell its other division, ContiTech, leaving the golden egg Continental Tires. Continental has long traded at a discount to comparable companies and has been considered a complex conglomerate with different business models and financial profiles. When the company initiated the split, a sum-of-the-parts valuation became highly relevant, and there was a clear discrepancy with how similar companies are valued.

When Continental manages to sell ContiTech, the business will consist of the highly profitable, stable and cash-generating tire division. The company will be less capital-intensive, have higher margins and be less volatile since approximately 75% of sales consist of replacement sales (replacement of car tires). The margin is expected to increase from 6–7% to 13–14% and the return on capital from 6–7% to 25%. The new Continental will therefore be a completely different type of business.

The market capitalization is currently 13 billion euros, and we estimate that ContiTech will be sold for 4 billion euros, which means that 9 billion remains in market capitalization. The Tires division is expected to generate 2.7 billion euros in operating profit before depreciation, and adjusted for debt, the remaining Continental is trading at 4.6x EV/EBITDA. The dividend yield is a high 6% and when the sale of ContiTech is completed, the proceeds will predominantly be distributed to shareholders. The implied dividend yield is 20% for 2027e. The valuation is too low considering the stability that Continental offers, and we believe that the valuation will be adjusted upwards when the sale is completed next year.

It was a turbulent month for tire companies. First, Michelin lowered expectations in a so-called pre-silent call and then issued a full-year profit warning a week later. At that time, Continental’s share price had been pushed down by about 10% and we then significantly increased our position. Three days later, Continental issued a reverse profit warning, with results expected to be over 20% better than consensus. The stock rose almost 17% during October and a full 23% from its lows, making it a strong contributor to the fund.

Verisure

During the month, we participated in Europe's largest IPO in three years: Verisure. Most people are probably familiar with the company, which sells and monitors home alarms with a 24/7 connected alarm center that detects, verifies and manages burglaries, fires and other threats in the home.

One of Verisure's biggest success factors is its ability to filter out 99% of all false alarms. Because the company can almost always verify if an alarm is real, it has been able to build effective partnerships with police and security companies. This is what customers pay for, not just the detection itself, but the security that someone will act quickly. Many companies can sell sensors that detect smoke or movement, but the difficult part is being able to verify what is actually happening.

Verisure is far superior to its competitors in Europe and is the market leader in 13 of the 15 countries where the company operates. At the same time, the company is capturing 70% of market growth and extending its lead. The company has 90% of its revenues in Europe, where penetration is a low 4% – compared to 23% in the US. In markets where Verisure has been present for a long time, such as the Iberian Peninsula and the Nordics, penetration is close to 30% of the addressable market (adjusted for housing type, affordability, etc.). Verisure spends just over 7% of its turnover on marketing because grassroot sales do not scale sufficiently. This has led to over half of all sales being made via inbound demand.

The company has a long growth journey ahead and will use around 50% of its free cash flow to invest in new customers. A customer can be acquired at around 3.6x EBITDA and stays for an average of 15 years. The annual customer churn rate is a low 7%, which is among the lowest globally among subscription-based business models. ARPU (average revenue per user) has grown by an average of two percent per year over the past ten years, while the cost of retaining customers has remained flat. The remaining cash flow will be used to pay dividends and strengthen the balance sheet.

We estimate that the company can grow by around 10% per year and with continued margin expansion from today's healthy 24%. In mature markets, the margin is over 40%. This gives an expected profit growth of around 15–20% per year in 2026-2028e and for that you pay around 18x EV/EBIT for 2027e. The share is up 21% since its introduction on the Stockholm Stock Exchange on October 8.

SLP

SLP delivered another solid report and was bang on in line with expectations. The company continues to impress, and the management result is up 46 % compared to last year. This year alone, the earning capacity has increased by 25%, while the loan-to-value ratio is a low 48%. Interest rates have come down while the yield requirements have not moved, which has a positive effect on the result. The company is trading below 15x earnings for 2027e. The share rose about 2% during October.

Kalmar

Kalmar released a mixed report. Order intake was 10% lower than expected, while profit was 6% better. Trade tensions and tariffs continue to create uncertainty, leading to varying developments between regions. Underlying capacity utilization remains high, and the company notes that the market appears to be more resilient than expected. So far this year, order intake is up 9% compared to the previous year, which was hard to believe given the macroeconomic signals earlier this year.

The focus remains on growing the service business, which has been neglected. Bad acquisitions (now divested) have meant that the company only has a 30% market share in spare parts, despite this being the most profitable business. CEO, Sami Niiranen, comes from Atlas Copco/Epiroc and is well-aware of the importance of service. The stock is trading around a low P/E of 12x with no debt. The stock rose almost 7% in October and is up 13% this year.

Scandic

Scandic delivered a report that was completely in line with expectations. What then drove the share up was the analysts' updates after the Dalata acquisition which was announced in the summer. According to our estimates, this contributes an additional 16 and 23% to earnings per share in 2026e and 2027e, respectively, which is also in line with what the company guided on the conference call. From 2027, Scandic will operate Dalata under a lease agreement, just like in the Nordics. Scandic is Pandox's largest leasing customer and we expect a similar arrangement in Ireland. The share is trading at a low P/E of 10.4 for 2027e. The share rose 4% in October. Since the turn of the year, Scandic has delivered a return of 34%, which is clearly better than other listed hotel companies in Europe. During the same period, Accor has lost just over 5%, Meliá 3% and Whitbread 2%. Scandic remained relatively undiscovered for a long time, due to high short selling, convertible debt and the fact that the company does not appear in conventional stock screens because IFRS 16 distorts key figures.

Hiab

Hiab reported a weak operating profit that was 28% below expectations, driven entirely by a weak US market. The operating margin for the third quarter was 11.4%, but the full-year guidance remains at 13.5%. The share had risen 5% the day before the report but then fell 13% on the day of the report. We took advantage of the opportunity and bought more shares. Our view is that sales in the US are now down to mere replacement levels, while the share decline priced in further deterioration. At the same time, Europe was strong with 26% growth in order intake, which is positive but not surprising given the low levels from where it comes.

Despite weaker margins, the company delivered a full 29% return on capital. It is difficult to understand why Hiab should be trading at a 30% discount to Nordic industrial companies given that the company is expected to increase sales by 7% per year, achieve margins of 16% and a return on capital of around 30%. We do not think this is reasonable and therefore retain Hiab as a large position in the fund. The business is short-cycle and early in the cycle. When things turn around, it tends to move quickly. The closest competitor, Palfinger, reported at the end of October that Europe will be the big driver next year, but also that the US is expected to contribute, which benefits Hiab. The company is trading at 10x EV/EBIT for 2027e with net cash, and we believe that an acquisition could take place before the end of the year. The share fell 3% in October and has fallen 3% this year.

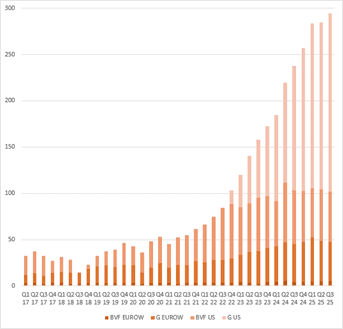

Bonesupport

Bonesupport delivered a slightly weaker report on the sales side, both in North America and Europe. We do not see any structural problem in the US, but in Europe there are challenges with rearranging priorities within the NHS in the UK and budget pressure in Germany. Bonesupport has had weak quarters before but never two in a row, and the company is adamant that they will reach the full-year guidance of at least 40% growth, which implies a strong fourth quarter. The share price is one thing, but the fact is that the main product, Cerament G, grew 59% during the quarter.

A new segment was recently opened for Bonesupport: revision arthroplasty, i.e. the replacement or adjustment of a previous joint prosthesis. It is often done due to wear, loosening, infection or complications with the original prosthesis. An estimated 300,000 such procedures are performed annually, of which 15–25% are infected.

The company is expected to receive FDA approval for Cerament V soon, which would broaden the areas of use. In the fourth quarter of 2025, the company will also begin rolling out Cerament BVF in spine surgery. We do not have high expectations for volumes there, as competition is fierce, but it paves the way for Cerament G in the same area. The NTAP approval for Cerament G in trauma should support sales. When an orthopedist treats acute trauma, a trade-off is made between cost and risk. If the cost is covered by NTAP, it should be an obvious choice to use Cerament G. The share has developed weakly this year and is now trading at 30x EV/EBIT on 2026 operating profit, a year when profits are expected to double. The share price fell 24% in October and is down 43% this year.

The image below shows the sales trend per quarter since 2017.

Source: Coeli European

SUMMARY

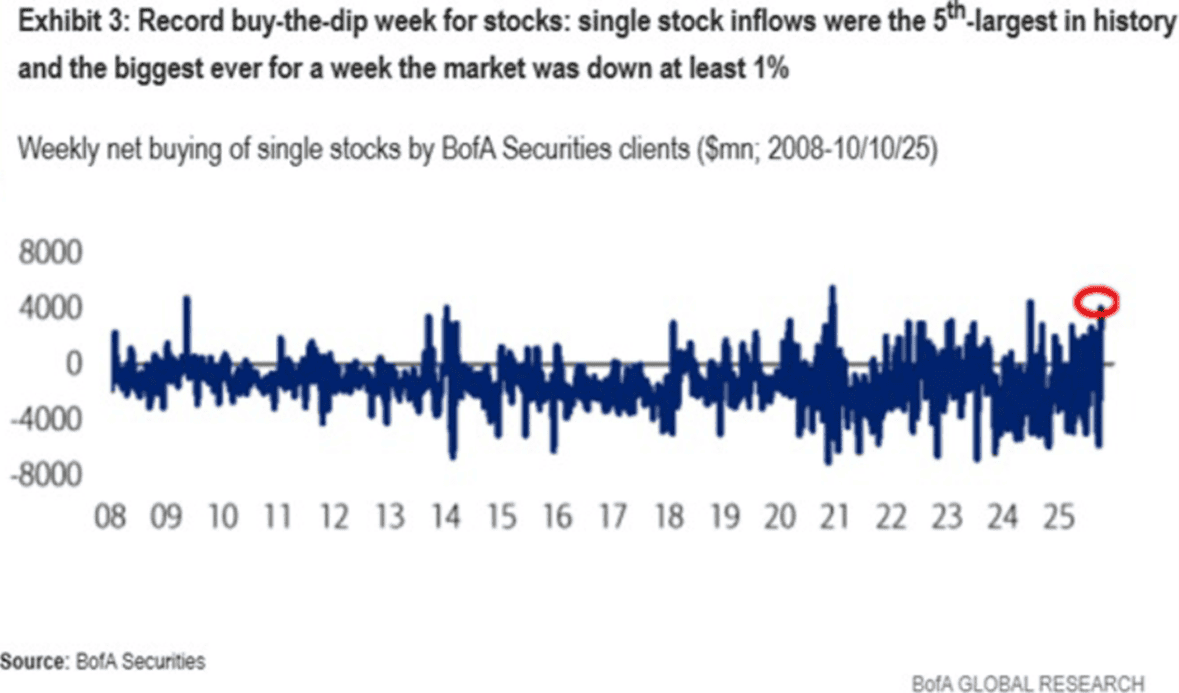

The conditions for the world's stock markets look unusually good at the moment. This view seems to be shared by private individuals, who, at the slightest dip, especially in the US, rush in with force to exploit temporary weaknesses. A sign of the times was when the stock market suddenly came under pressure in mid-October. Over the next five days, the US stock market received its fifth largest inflow ever.

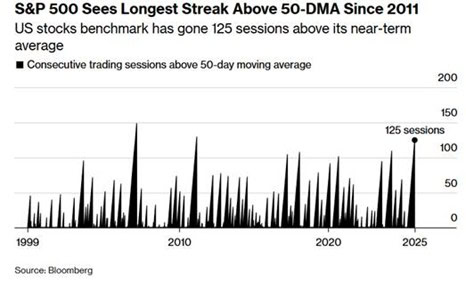

The graph below is a few weeks old, but it looks like it will soon be a new high for the number of days the S&P500 has traded above its 50-day moving average. October was the sixth consecutive month of positive markets in the US, while it was the fourth month for Europe.

As mentioned at the beginning, in a market with higher risk-taking than usual, lower quality companies tend to outperform quality companies. The difference in returns over the past 10 weeks is significant.

Source: Goldman Sachs

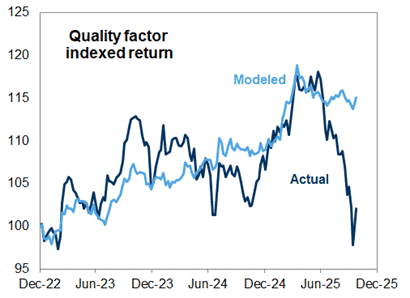

The rotation into lower quality companies has been brutal in many places and has also been faster than what economic development justifies (a model that includes growth and interest rates, among other things). The question is which of the two lines is currently more wrong?

Source: Goldman Sachs

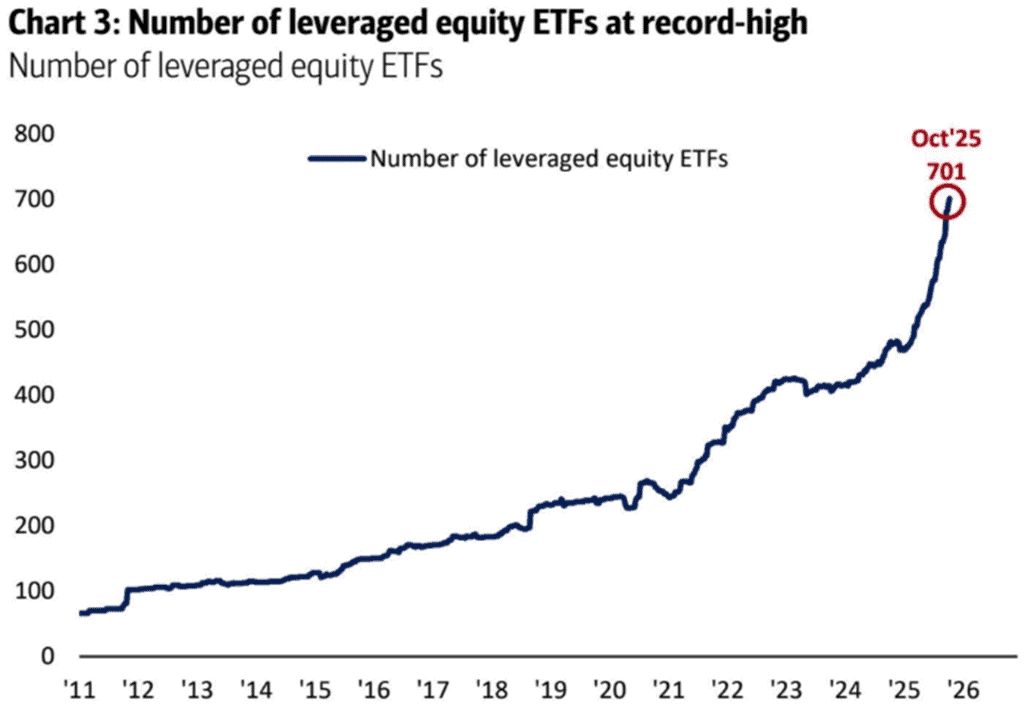

When savings are not enough, leverage yourself! The number of leveraged ETFs is breaking new records. Don't forget that the effect of market downturns with leverage becomes mathematically unpleasant.

Source: Goldman Sachs

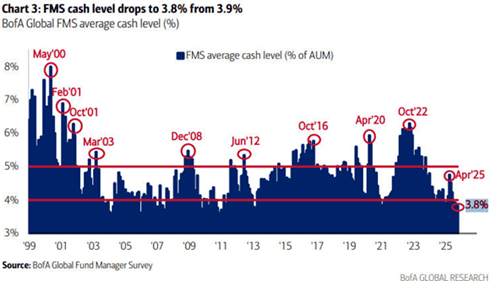

Cash levels are at lower levels than the historical average.

Source: Goldman Sachs

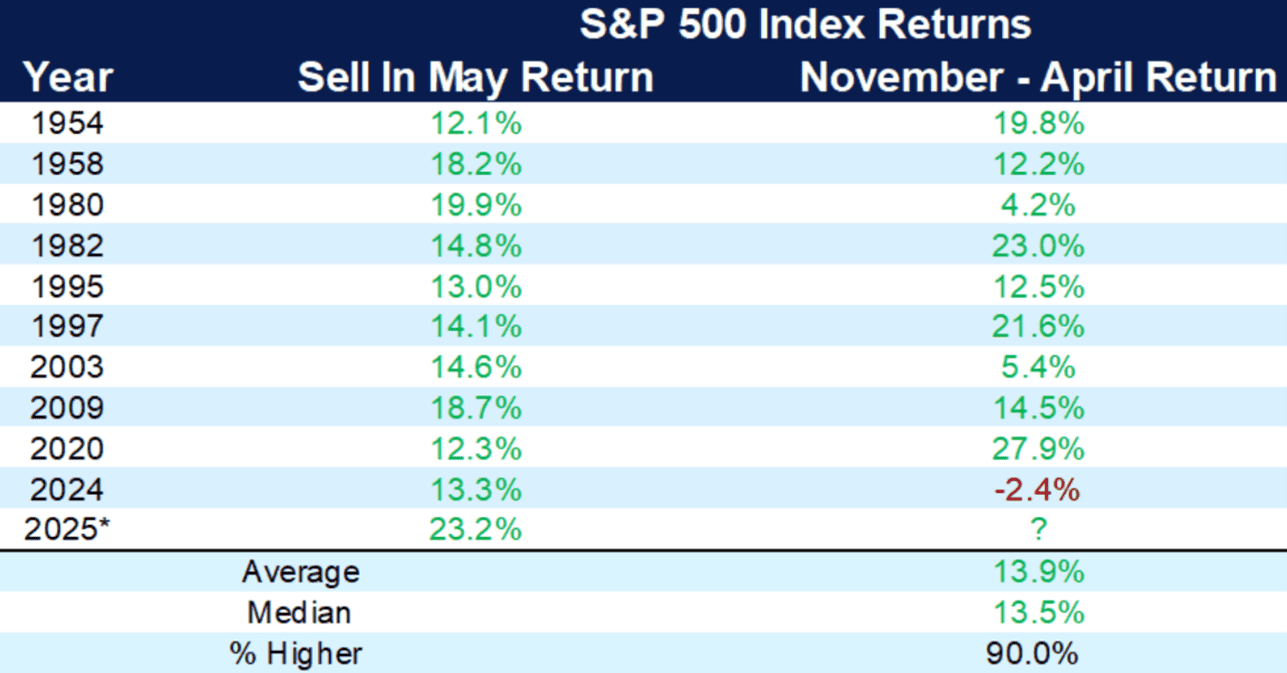

Historically May to November has been the weakest period seasonally; however, this time it looks different.

Source: X

We are now rolling into the, historically, strongest period for stocks and the image below shows the development up to the turn of the year.

Source: Goldman Sachs

In summary, things are looking unusually bright on the world's stock markets right now. European interest rates have fallen sharply and are on their way down in the US. Most central banks are also in full swing of lowering key interest rates and inflation is under control. Manufacturing PMI in Europe was below 50 (indicating reduced activity) from the summer of 2022 to August this year when the figure was 50.7 (increased activity). Oil prices are low and technological successes with AI are slowly starting to trickle down to cost savings for companies. A huge amount will happen in the coming years.

The tariffs have been handled surprisingly well so far. To quote our own Kalmar, which reported on the last day of the month: "The market seems to be more resilient than we previously anticipated".

For the first time since 2019, a summit took place between President Trump and China's Xi Jinping. A visit that Trump rated a 12 on a 10-point scale. The meeting led to what the parties called a “hard-won consensus.” It should be seen as a framework for a one-year ceasefire in the trade conflict, which is a good start towards a better development than what was the case this year.

Huge infrastructure and defense investments in Europe will most likely drive growth for many years to come. As an added bonus, Europe is now also getting some help from Nvidia CEO, Jensen Huang, who thinks things are going too slowly here (many of us agree) and is therefore making investments in various European companies. The most recent was Nokia, where it invested 1 billion euros and became the owner of 2.9% of the company. In addition, Nvidia has recently announced collaborations with Mistral AI, Schneider Electric, Siemens, BMW, Mercedes, Orange, Swisscom, Telefonica and ABB, to name a few. Clearly positive!

For the fund 67% of the companies have reported and it has been predominantly positive, although many humbly note an unusually high level of uncertainty in their forecasts.

We thank you for your interest and wish you a fruitful November.

Mikael & Team

Malmö, 6th of November 2025

IMPORTANT INFORMATION. This is a marketing communication. Before making any final investment decisions, please refer to the prospectus of Coeli SICAV II, its Annual Report, and the KID of the relevant Sub-Fund. Relevant information documents are available in English at coeli.com. A summary of investor rights will be available at https://coeli.com/financial-and-legal-information/.

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested. Please note that the management company of the fund may decide to terminate the arrangements made for the marketing of the fund in one or multiple jurisdictions in which there exists arrangements for marketing.