This material is marketing communication.

Note that the information below describes the share class (I USD), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class return. The information below regarding returns therefore differs from the returns in other share classes.

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

1) Share Class I USD

Performance for other share classes towards the end of the report.

FUND MANAGER COMMENTARY

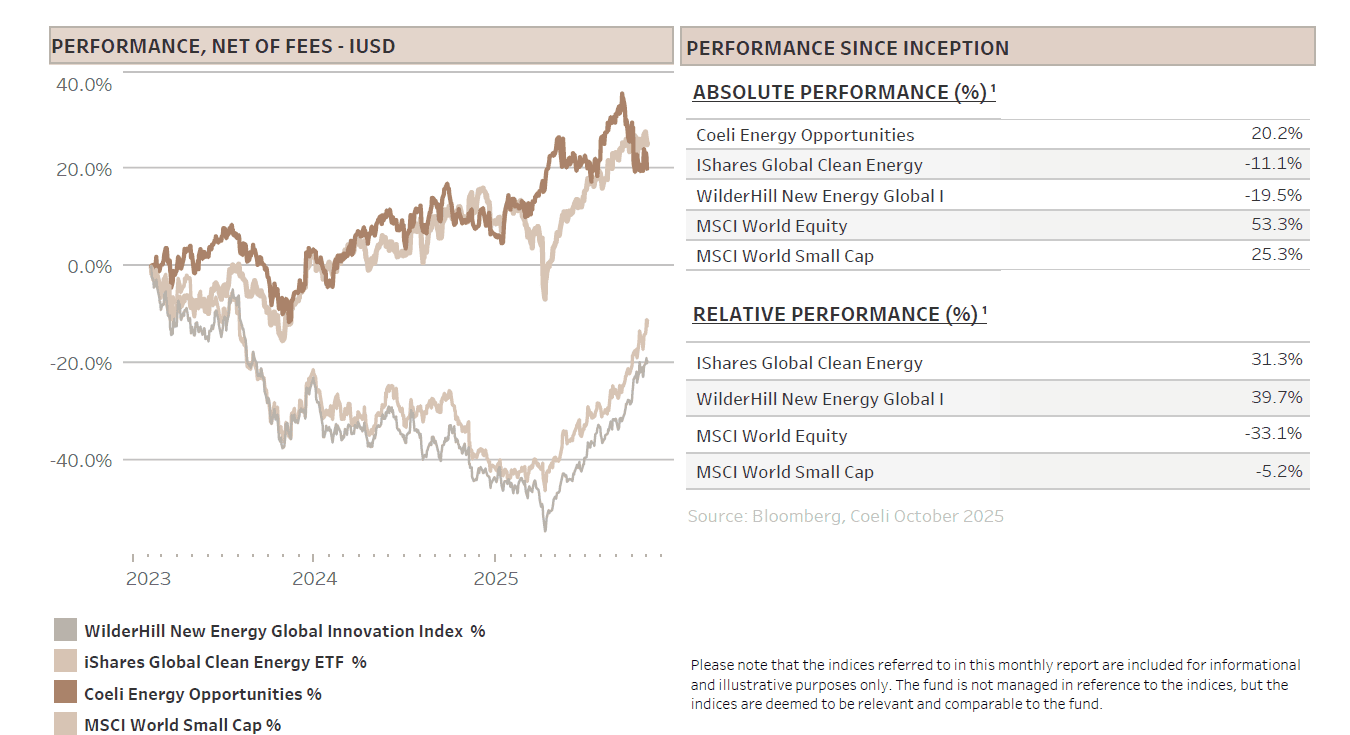

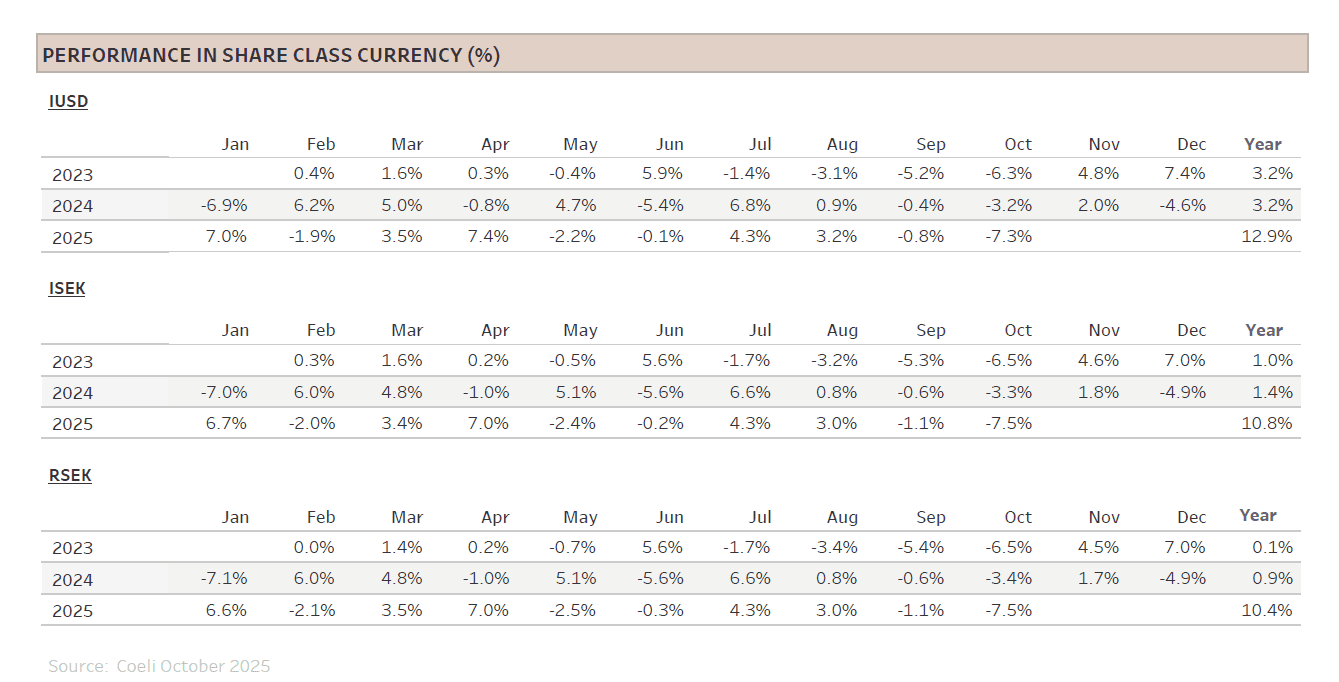

The Coeli Energy Opportunities fund lost 7.3% net of fees and expenses in October (I USD share class). Year-to-date, the fund is up 12.9% and it has gained 20.2% since inception in February 2023.

The fund underperformed its most comparable indices, the Wilderhill New Energy Global index (NEX) and the iShares Global Clean Energy (ICLN) by 18% and 19%, respectively, in October. Year-to-date the fund is underperforming the NEX by 32% and ICLN by 40%, while since inception the fund remains ahead by 40% and 31%, respectively.

October saw a continuation of September's challenges. The meme rally accelerated into early October and while hydrogen stocks, which caused significant losses in September and early October, peaked and began to deflate, other stocks with weak fundamentals and high short interest became sudden retail favourites. The fund lost 18.5% on shorts in October, roughly two-thirds of which were linked to hydrogen stocks, though shorts in solar and other renewable sectors were also squeezed. At the same time, the powering AI themes continued to do well. Two-thirds of the fund’s themes were up for the month, and long contribution was 11.2%. The best performing theme was ‘Diversified Renewables’, which added 3.9%, led by gains in a couple of bitcoin miners and Bloom Energy (BE), the best positioned fuel cell company. BE rose another 56% in October, extending its year-to-date gain to 495%.

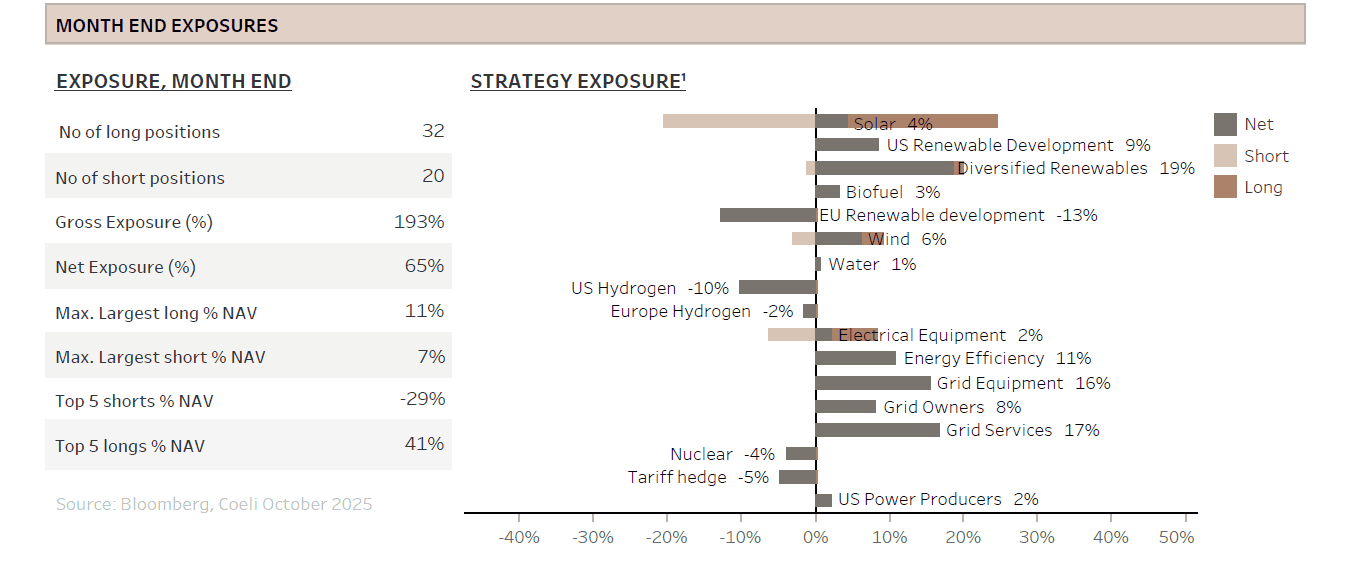

The fund increased its net exposure during the month by significantly reducing hydrogen shorts at the start of October and cutting other squeezy shorts by month-end as the meme rally shifted to new names. The fund also added to some longs in AI-related themes as hyperscalers showed no signs of slowing, with deal activity and capex only accelerating. At month-end, overall net and gross exposures stood at 65% and 193%, respectively.

Our year-to-date underperformance against the most comparable indices is considerable. We have reviewed the constituents in the indices and note that many of the stocks had a good year in terms of stock price performance up until mid-September when prices went vertical. However, reviewing earnings expectations for the same stocks, they are mostly down or unchanged. The meteoric rise is largely due to multiple expansion. The fund’s performance reflects this pattern as it held up well from ‘Liberation Day’, despite the relentless rally in shorted names, until around mid-September when the shorts accelerated at an unprecedented rate. Unfortunately, we underestimated the scale and the duration of the optimism in these mostly unprofitable companies. Price dislocations however create opportunities for patient investors.

MARKET COMMENT – IS IT ALL ABOUT AI?

The S&P 500 rose 2.3% in October, its sixth consecutive month of gains. Nasdaq climbed 5%, with the rally again led by the Mag 7 and large-cap tech riding the AI wave. However, the S&P 500 equal weight index declined by 1%, underscoring deteriorating market breadth. Indeed, as the index surges and the 10 largest companies now account for 40% of its value, it is striking that more stocks are hitting 52-week lows than highs.

While the frequency of earnings beats in Q3 was unprecedented outside the Covid years, the next day’s reward for surpassing estimates averaged only a third of the typical boost. This suggests the bar is high and that macro uncertainty and positioning are weighing on the market. Still, aggregate earnings forecasts are being revised upwards.

The macro-outlook remains mixed. Though the Fed cut rates in October, Chair Powell signalled that further reductions in December are not a foregone conclusion. However, with no new labour market statistics following the longest US government shutdown in history, the bond market still prices another rate cut as more likely than not.

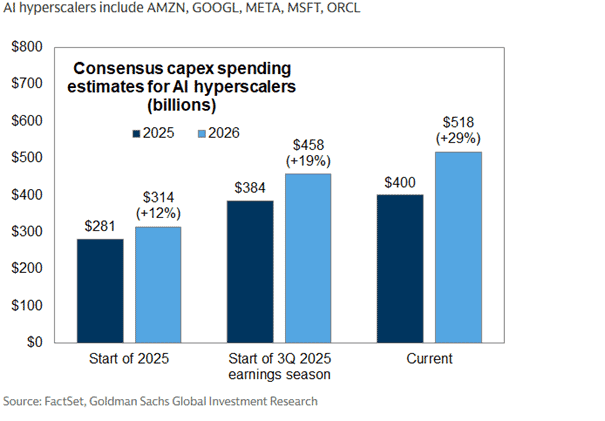

Although many argue, us included, that equities screen expensive, bull markets rarely end with rising earnings and FED rate cuts; a trigger is usually required. Will AI be the trigger? As discussed in last month’s report, ‘Are we in an AI bubble?’, AI is now the dominant macro driver for equity markets, with most economic growth and stock market returns tied to AI investment and its anticipated returns. As it is too early for the market to discern the returns on AI investments, market focus remains instead firmly on investment levels. However, as can be seen from the graph below, hyperscalers’ spending continues to surprise to the upside in both absolute dollars and expected growth.

While at the start of 2025, AI investments for 2026 were expected to grow by 12% to USD 312bn, the latest post-Q3 forecast is for 29% growth to as much as USD 518bn, a 65% increase over the original estimate. The 2025 forecast has also increased by a staggering 85%, to USD 400bn versus expectation at the start of the year.

AI investments are not slowing; they are accelerating rapidly. Peak investment levels are clearly not the trigger for a market correction, at least not yet.

BRING YOUR OWN POWER – HOW THE DATA CENTER IS REWIRING THE GRID

A recurring topic in our monthly reports is the growing strain on electricity grids driven by the emergence of huge AI data centers. As discussed above, spending is accelerating, not slowing down, at least not yet. While growth will eventually moderate, in the meantime, multiple sub-cycles within the sector are being disrupted by technological and structural shifts in demand. Some cycles will fade due to declining hype, and others will become oversupplied before demand inevitably falls. We will examine several of these trends as new data centers are increasingly forced to secure their own power supply.

In our March-24 report “Roadblocks on the AI highway”, we explained that the greatest challenge to expanding data center capacity is access to power and grid connections. Our November-24 report, “The urgency to secure power”, explored future data center power options such as renewables, nuclear, natural gas, fuel cells and repurposing industrial sites or bitcoin mining facilities. Since then, most stocks in these categories have surged as urgency around AI-driven power demand has increased alongside hyperscaler investments projections.

The market is, however, ingenious. Nearly every company with any resemblance to a power-generating asset is offering their services. Hyperscalers are eager to sign contracts, often with expansion options, to secure supply in a tight market, but likely also to set up for a potential oversupply in the future. Recently, several oilfield service and equipment companies have announced fleet expansions of small gas turbines and reciprocating engines, essentially modular combustion units mounted on trailers. Gone are the days when tech companies tried to obscure their consumption of fossil fuels.

Yet, how efficient is it to run trailers with diesel and natural-gas engines to power data centers? Not very. In fact, it is incredibly inefficient, but it serves its purpose: it creates rapid supply, more optionality, and allow hyperscalers to keep building. Ultimately, we believe this is nothing more than a stopgap solution for data centers awaiting grid connection or more efficient alternatives.

From Stopgaps to Structured Power

Renewables such as solar and wind, along with large combined cycle gas turbines (CCGTs) are vital for data center buildout. Renewables offer relatively cheap and rapid power to the grid, while gas turbines provide resilience via their “spinning mass”, supporting the alternating current (AC) waveform required for grid stability.

Nevertheless, it is increasingly a requirement for data centers to “bring your own power”, but neither renewables nor large CCGTs are optimal for direct connection to a large load like a data center. However, fuel cells are well suited for this purpose: they are small, modular, and if one unit fails or need maintenance, the power supply is only marginally impacted. Fuel cells also deliver high electrical efficiency, operate quietly, and do not emit particulates. They do, however, require regular maintenance as stack efficiency declines over time, a risk that could limit their potential to serve as a permanent solution unless maintenance costs fall in line with those for renewables and gas turbines.

Bloom Energy (BE), a fund holding, is the clear market leader in solid-oxide fuel cells (SOFC), having supplied “servers” to smaller data centers for a decade. Given the acute power shortfall in parts of the US, limited viable alternatives, and the need to bring your own power, Bloom has started receiving orders from hyperscalers this year, propelling the stock nearly 500% YTD. The valuation is now clearly rich. As mentioned in last month’s report, other companies are trying to address the SOFC market, but the real challenge will be scaling in time to seize this opportunity. MOUs (memorandums of understanding) for future contracts from new entrants may materialize, but the most likely scenario is further contracts to Bloom, given its track record and expanding manufacturing base.

Not all fuel cells are the same though. There is a widespread misconception on social media that proton-exchange membrane (PEM) fuel cells, like those produced by Plug Power (PLUG) or Ballard Power (BLDP), are suitable for data centers. PEM fuel cells require externally sourced, high-purity hydrogen. As we have explained many times, producing electricity from hydrogen is incredibly inefficient, but to make it worse, there is no viable infrastructure for delivering the enormous volumes required to run a data center. Supplying even a single hyperscale site would mean thousands of tanker-truck deliveries per day, obviously physically and economically impossible. In our view, PEM systems will not play a role in suppling data centers with electricity, but despite these facts, stocks in this sector have rallied hundreds of percents on hype, which will eventually end one day.

Batteries represent another key technology as data centers increasingly require onsite power and redundancy. While China still dominates the supply chain, US domestic battery supply is expanding, and battery storage was a notable beneficiary of the One Big Beautiful Bill Act (OBBBA). In previous monthly reports, we have covered the potential to scale Virtual Power Plants (VPPs) using aggregated batteries, a trend we expect to continue gaining importance.

Demand for power is developing so fast that both utilities and data center operators are applying an “all of the above” approach to power supply. Similarly, for on-site power generation of data centers, we believe a hybrid power stack is most likely: grid connection, medium sized gas turbines or SOFCs providing continuous on-site power, combined with batteries and supercapacitors to absorb or deliver power in milliseconds as workloads fluctuate. In effect, each site becomes a miniature utility - generating, storing, and stabilizing its own supply.

The Architectural Leap

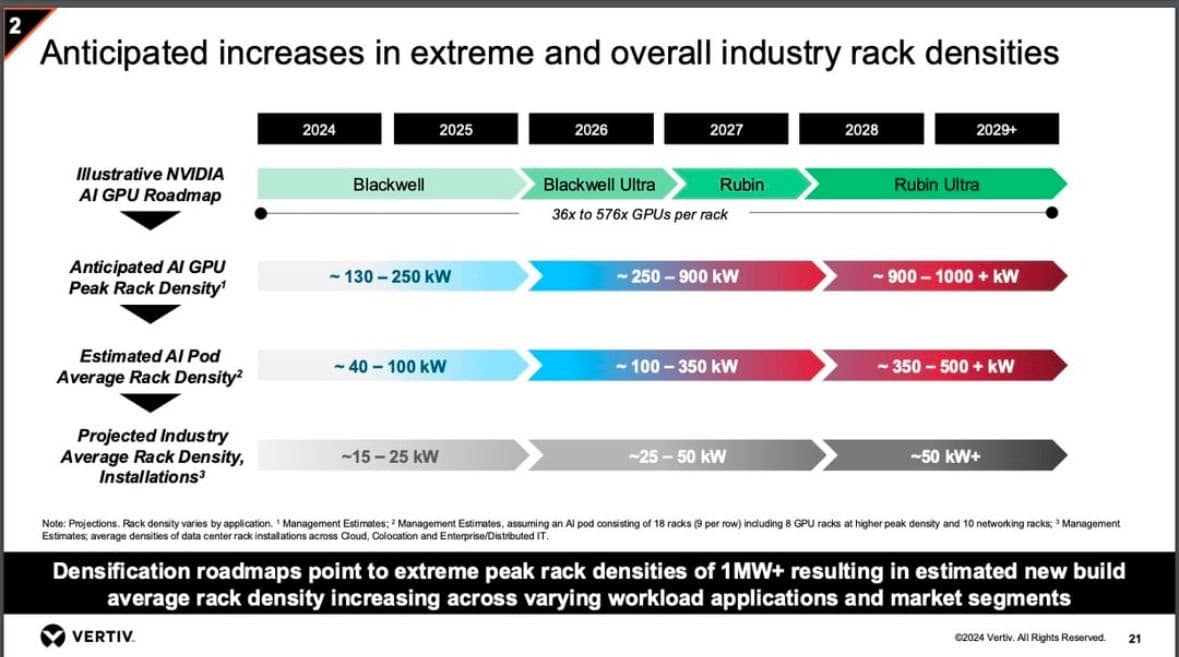

The next shift happens inside the perimeter of the data center. NVIDIA’s recent “Data Center of the Future” whitepaper outlines an electrical redesign centered on an 800-volt direct current (DC) architecture. The traditional alternating-current (AC) hierarchy: high-voltage grid connection → step-down transformer → switchgear → UPS → server-level conversion, involves numerous conversions, each adding inefficiency and heat. Moreover, with Nvidia’s future GPUs demanding immense power, using lower-voltage AC would require power cables so thick they could not fit inside the racks of data chips.

The 800-volt DC model streamlines this architecture: power supplied by on-site fuel cells, batteries or rectifiers could feed directly into a high-voltage DC bus distributing electricity across racks to the chip level. Fewer conversions mean lower losses, smaller footprints, and greater control. These advantages are critical as rack power densities approach one megawatt as demanded by Nvidia’s upcoming Rubin Ultra GPUs.

Source: Vertiv 2024

Equally important, a DC backbone integrates seamlessly with new local power assets: fuel cells, batteries, and even solar, all inherently DC devices. The data center becomes a tightly coupled microgrid with more limited demand from the grid.

Although “bring your own power” was viewed largely as an inconvenience until now, it is becoming a necessity as data centers expand and shift toward DC electrical architecture. On-site SOFCs could have a slight advantage since they produce DC power directly, while gas turbines are inherently producing AC power. Batteries, supplying DC power, will likely become more important too, rapidly responding to the wild swings in power demand from the data centers which often can shift demand from nearly nothing to 100% in milliseconds. That load volatility is not something the grid alone can handle.

The shift to “the data center of the future” will create both winners and losers: the medium-voltage transformers, switchgear and rectifiers used to convert AC-DC and to step up and down voltage might see their roles diminished or rendered obsolete in data center applications. This is one instance where a technological shift, not hype nor excess supply, can end a cycle. AI is not just consuming electricity; it is redesigning the entire system that produces and delivers it. The data center of the future will probably look less like a tenant of the grid and more like a peer utility, complete with generation, storage, and control.

For our fund, this convergence of computing and power is a key investment theme. It reaches from semiconductors and cables to turbines, renewables, fuel cells, and batteries. The short-term scramble for megawatts will eventually subside, but the structural redesign of the power system is just beginning.

While grid investments continue to benefit the most from data center expansion, new opportunities are emerging as demand structure evolves. In this vertical, winners will build for a future in which data centers not only draw power from the grid—they become integral components of it.

FUND PERFORMANCE – RETAIL DRIVEN MEME-RALLY CONTINUES

October’s drawdown of 7.3% was the worst monthly performance since the fund's launch nearly three years ago. The primary driver was losses on a handful of short positions caught in the retail-driven meme rally, which triggered dramatic price spikes over just a few days. While long positions performed well in October, bolstered by powering AI themes and adding 11.2% to NAV, the fund’s net exposure at month-end was, in hindsight, too low, as we hedged out too much of our powering AI longs. We also underestimated other investors’ willingness to re-engage with renewable energy names and pay up for potential future growth.

The worst performing theme in October was ‘US Hydrogen’, which drew down 7.9% of NAV. As detailed in last month’s report, we realized losses early in October after irrational price moves made the size of our hydrogen positions too large for comfort. The two hydrogen themes lost nearly 10% of NAV overall in October.

Extreme moves in so-called meme stocks are mostly driven by retail investors, largely influenced by social media and buoyed by abundant liquidity, using short-term call options to chase heavily shorted stocks higher. This drives highly volatile price action as market makers (who sell the calls) rush to hedge by buying the underlying stock. The mechanism also works in reverse, and as short-dated options incur significant time losses as days pass, these rallies often end abruptly. Two of the three hydrogen stocks that caused losses in September and early October have since fallen 30–40% from their peaks but are still significantly overvalued in our view.

Unfortunately, retail investors have since moved on to other heavily shorted names, as call option activity continues to increase. According to Goldman Sachs, the volume of call options versus put options outstanding hit a new record last month, surpassing the prior peak seen during the meme rally in late 2020/early 2021. Timing an end to this “madness of crowds” is impossible, but we believe the set-up today differs substantially from the end of 2020, when Biden had just been elected President on expansive green deal promises, EU green investment targets were ambitious, and concept stocks could easily raise capital. Additionally, multiple covid vaccines had just been announced, and interest rates were at zero, fuelling abundant liquidity and risk tolerance.

Today, the liquidity backdrop is less favourable, and greater uncertainty surrounds the duration of the AI spending boom, which has supplanted the “green deal” as the key driver of optimism. Nevertheless, given the continued rally into November, we continue to reduce short exposure and will reassess these stocks when fundamentals again matter.

As discussed above, the best performing theme was ‘Diversified Renewables’, contributing 3.9% to NAV. The second-best performer was ‘Solar’, adding 1.3% to NAV. Our long-held favourite and largest solar position, First Solar (FSLR), rose 23% in October, while fellow favourite Nextracker (NXT) soared 36% on strong earnings and outlook. However, gains in the theme were largely offset by losses on shorts tied to Chinese solar stocks.

The global solar module market is currently more than twice oversupplied, with roughly 90% of capacity owned by Chinese firms. As losses mount, the Chinese government is working to force industry consolidation and trim capacity. These efforts have lifted polysilicon prices, a key solar module input, though unless module prices also rise, this is mainly squeezing manufacturers’ margins and is not something that should drive stocks higher. Furthermore, for Chinese companies with US manufacturing operations eligible for tax credits, we expect these to be significantly reduced next year under the Foreign Entity of Concern (FEOC) policy. For now, however, such issues are largely ignored by retail traders chasing the next meme stock.

The fund also lost 1.8% of NAV in the theme ‘EU Renewable Developments’ which is skewed short after paring back long positions in developers that had outperformed in recent quarters. This timing proved premature as we did not expect investors to pay up for future growth so soon, especially not for US-based expansion. Yet, optimism driven by AI data center power demand has overwhelmed concerns about possible Trump administration roadblocks and permitting delays. With sharp increases in US retail electricity prices, the issue is gaining political salience ahead of next year’s elections, and it is not unlikely that the administration will prioritize electoral incentives over impeding solar and wind developments.

The third-worst performing theme was ‘Energy Efficiency’, mostly comprised of long positions in European construction and insulation firms. The theme lost 1.0% of NAV in October, reflecting a stagnant European economy and delayed German fiscal stimulus. Yet, valuations remain attractive, fiscal stimulus is expected to impact order intake next year, and several companies have US and data center exposure. The prospect of peace and reconstruction in Ukraine would be the icing on the cake for patient investors.

Overall, October was exceptionally challenging. This has been the worst and longest short squeeze of our careers, but with AI sentiment robust and additional Fed cuts possible, predicting a meme rally’s end remains elusive. We are reducing exposure and conserving capital, so we can capitalize on the significant opportunity we expect after the meme rally subsides.

Thank you for your continued trust. We look forward to updating you again next month.

Sincerely

Vidar Kalvoy & Joel Etzler

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

- Portfolio Manager and Founder of the Coeli Energy Opportunities Fund.

- Over 15 years of investment experience spanning both public markets and private equity.

- Managed the Coeli Energy Transition Fund from 2019 to 2023.

- Spent six years at Horizon Asset in London, a market-neutral hedge fund.

- Started working with Vidar Kalvoy in 2012.

- Five years in Private Equity at Morgan Stanley.

- Began his investment career in the technology sector at Swedbank Robur in Stockholm in 2006.

- Holds an MSc in Engineering from the Royal Institute of Technology (KTH), Stockholm.

- Portfolio Manager and Founder of the Coeli Energy Opportunities Fund.

- Has managed energy equities since 2006 and brings more than 20 years of experience in portfolio management and equity research.

- Managed the Coeli Energy Transition Fund from 2019 to 2023.

- Head of Energy Investments at Horizon Asset in London for nine years, a market-neutral hedge fund.

- Experience from energy investments at MKM Longboat in London and equity research in the technology sector in Frankfurt and Oslo.

- Holds an MBA from IESE in Barcelona and a Master’s in Business and Economics from the Norwegian School of Economics (NHH).

- Before entering finance, he served as a lieutenant in the Royal Norwegian Navy.

IMPORTANT INFORMATION. This is a marketing communication.

Before making any final investment decisions, please refer to the prospectus of Coeli SICAV II, its Annual Report, and the KID of the relevant Sub-Fund. Relevant information documents are available in English at coeli.com. A summary of investor rights will be available at https://coeli.com/financial-and-legal-information/.

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

Please note that the management company of the fund may decide to terminate the arrangements made for the marketing of the fund in one or multiple jurisdictions in which there exists arrangements for marketing.