This material is marketing communication.

Note that the information below describes the share class (I SEK), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class’ return. The information below regarding returns therefore differs from the returns in other share classes.

Before making any final investment decisions, please read the prospectus, its Annual Report, and the KID of the relevant Sub-Fund here.

JANUARY PERFORMANCE

The fund’s value decreased by 0.2% in January (share class I SEK), while the benchmark increased by 0.4%. Since the change of the fund’s strategy at the beginning of September last year, the fund’s value has increased by 26.3% compared to an increase of the benchmark by 24.8%.

Source: Coeli European

* Adjusted for spin-off of Rejuveron

** Includes September 1 (strategy change to long-only implemented September 4 2023)

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

EQUITY MARKETS / MACRO ENVIRONMENT

What a month and what a start to the year! Most of it has revolved around President Trump and the US administration, where we have witnessed several unimaginable events. At the same time, the reporting period for the fourth quarter of 2025 has begun.

Source: X

Despite major events in the world, volatility in the stock market was surprisingly low overall. For individual stocks, however, we experienced high volatility and the start of the reporting season has in several cases offered significant share price movements even for large companies. For example, Microsoft fell 10% on the reporting day, which was the second largest decline ever in a single day. German SAP fell 16%, French LVMH by 8% while Meta rose by 10%.

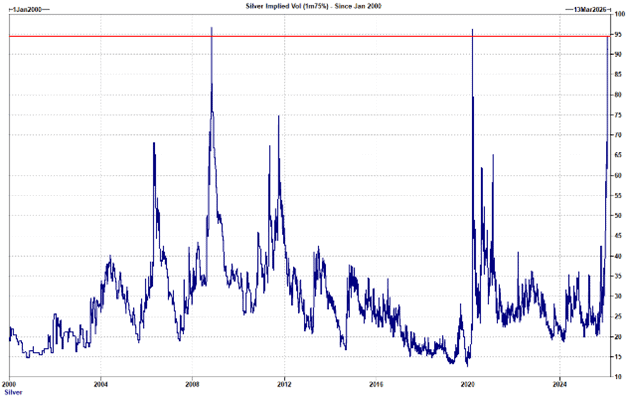

However, this was nothing compared to precious metals where gold rose by 13% in January, which includes a decline on the last day of the month by 9%. The corresponding development for silver was +19%despite the decline on the last day of January being a full 26%. Extreme movements in other words and with a volatility that was at the same level as during the financial crisis, see image below. The declines continued on Monday, February 2.

Source: Goldman Sachs

The price of bitcoin was also unusually volatile and under significant price pressure. Since the high in January, the price has fallen by 20% and since the high in October by a full 40%.

In this environment, the fund declined 0.2%. A continued strengthening of the Swedish krona affected the fund's return in January by -2.3%. The fund's return was slightly the benchmark, which rose by 0.4%.

The best contributors to the fund during the first month of the year were British Babcock (+15%), Danish FLSmidth (+22%) and Plejd (+19%). The worst were Beijer Ref (-15%), Danish Alm. Brand (-8%) and Lindab (-10%).

We had an unusually high number of company meetings in January, which was liberating and rewarding during a month dominated by macro news. In total, we had 35 company meetings, most of which took place in Copenhagen at SEB's large seminar (which I have attended since 2003) and in Frankfurt with Kepler Cheuvreux.

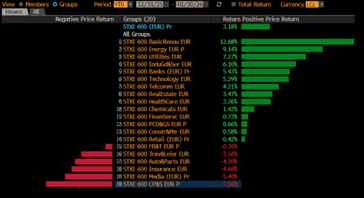

The spread in development for different sectors in Europe was unusually large. Mining companies were clear winners after the sharp increases in metals, but oil companies also rose sharply after the oil price rose by a full 14%, the sharpest increase in many years. The events in Venezuela and Iran contributed to this.

Source: Bloomberg

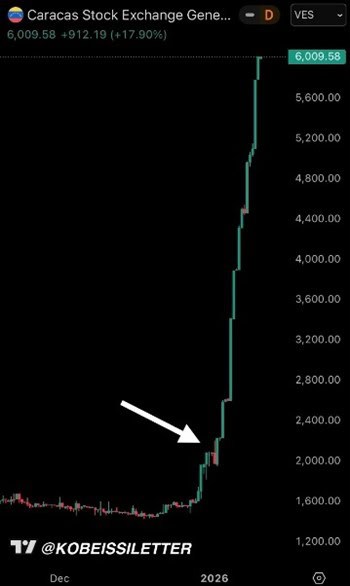

On January 3rd, the US military captured Maduro, the dictator of Venezuela, in a spectacular manner to say the least. Afterwards, Venezuelans around the world celebrated in great style. So did investors who were long Venezuelan stocks, as the index rose 200% in a few days!

Source: X

President Trump, high on happiness after the successful capture, continued his offensive and made it clear to his allies that Greenland must be owned by the United States for security reasons. The world was on edge when he appeared in Davos, and you could almost hear a sigh of relief from everyone and everything when he promised not to take Greenland by military force. The stock market began to rise and that's where we are now. The world was relieved that the United States would not attack one of its most loyal allies, Denmark.

Late one night, Trump sent out this AI-composed image. It was the same night that he announced new punitive tariffs against Sweden, among others, for sending troops to Greenland.

Source: Truth Social

Trump was unusually active during the month and sent a letter to Norwegian Prime Minister Støre, stating that he no longer feels any responsibility to prioritise peace since he was not awarded the Nobel Peace Prize. The comment about the boat below makes one think of another boat that arrived in 1492.

Source: X

President Trump's new punitive tariffs on countries that have sent troops to Greenland led to the biggest drop in the US stock market since April 2nd of last year. For once, the EU started flexing its muscles on countermeasures and things calmed down, at least temporarily. TACO!

Much more enjoyable was the EU agreeing with India on a new trade deal that is likely to prove valuable for both parties and affect 1.9 billion people. The EU also reached an agreement on a free trade agreement with Mercosur, which consists of Argentina, Brazil, Paraguay and Uruguay and together affects 700 million people. Unfortunately, it looks like the unrealistic and anti-growth Left Wing Party and the Green Party, as well as their sisters and brothers in the EU Parliament, may put a damper on it and delay it by up to two years. Good job… (a personal reflection from the author).

At the same time, the UK was in China for the first time in 8 years agreeing to reduce tariffs on certain goods. Canada did the same with China, and both countries immediately received, what could be construed as threatening, comments from President Trump. Slowly but gradually, the US is becoming increasingly isolated, investors are rebalancing and reducing their US exposure and the dollar is falling further (although Trump just said that it was doing very well!?).

The US Federal Reserve chairman was also under heavy attack from Trump, which led to something that has never happened before, a joint statement from the world's central bankers to show solidarity with Jerome Powell. The importance of monetary policy independence is not something that the US administration seems to appreciate. The developments in (other) authoritarian regimes such as Zimbabwe, North Korea, Russia and Venezuela one would think is proof that it is not working.

Source: X

The summary of everything that happened in January makes one wonder if the great leader has lost his mind. That’s without factoring in the joyous scene when he received the Nobel Peace Prize from last year’s Nobel laureate Machado. One of Trump’s (and Putin’s) biggest European supporters, Slovakian Prime Minister Robert Fico, was clearly concerned about Trump’s mental health after visiting him at Mar-a-Lago on January 17th and afterwards describing him as “dangerous”. All this according to Politico magazine. Fico has since denied the whole story. Link to article: "European leader spoke of shoke at Trump's state of mind after Mar-a-Lago meeting".

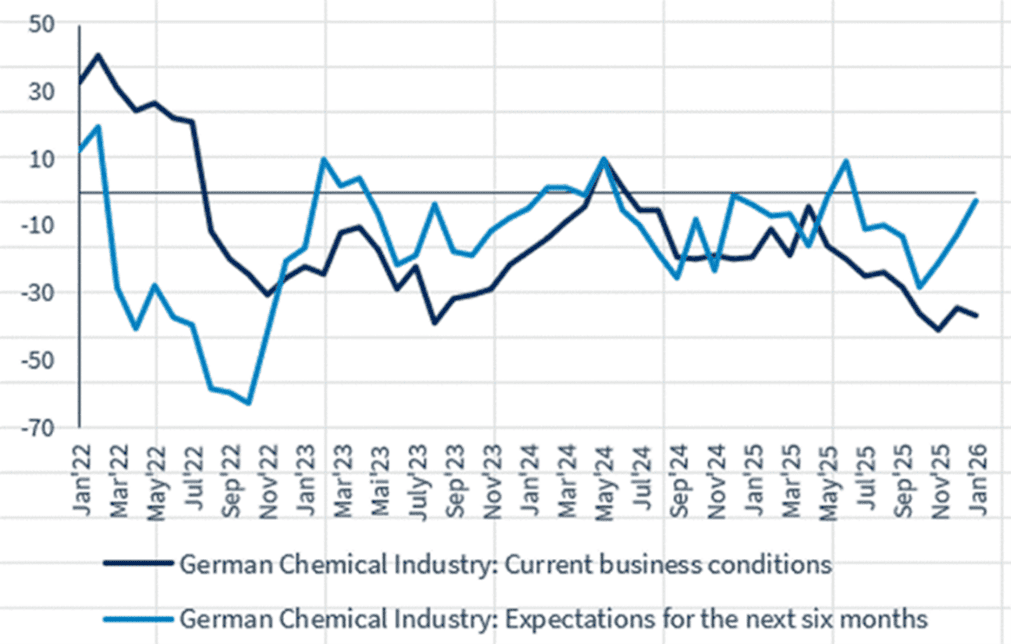

Now some comments on more traditional and refreshing macro events after having endured the above reading. The German IFO index for chemical companies fell slightly in December but showed a clear uptrend for the coming six months, see light blue line. Is this when we see activity increasing in Germany due to the huge infrastructure projects being launched?

Source: X

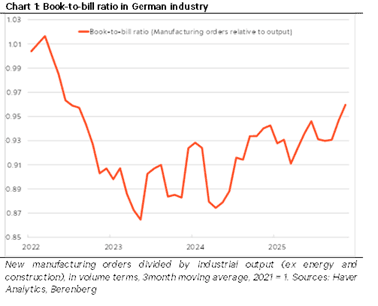

Book-to-bill (orders received in relation to sales) in German industry is approaching 1.0 after three years of zero growth in German GDP.

The construction materials trade in Sweden breaks a four-year decline and finally showed growth in 2025. During the fourth quarter, sales increased by 7.4%, with the largest part accounted for in December. Many of us hope that the construction industry will finally turn around, as it is a major engine for the Swedish economy.

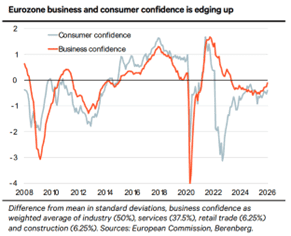

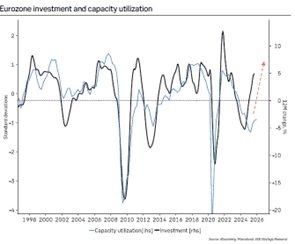

Optimism in the European economy is slowly turning around.

Rising investments indicate that capacity utilization in European industry is on the rise, which means rising profits and growth.

Source: Bloomberg, Macrobond, SEB Strategy Research

The picture below shows the development of the US dollar in relation to the euro since 2008. If we are going back to old lows (which we don’t know) we are not even halfway through the weakening of the US dollar. Remember that as recently as 2014, one dollar cost just over 6 Swedish kronor.

Source: Bloomberg

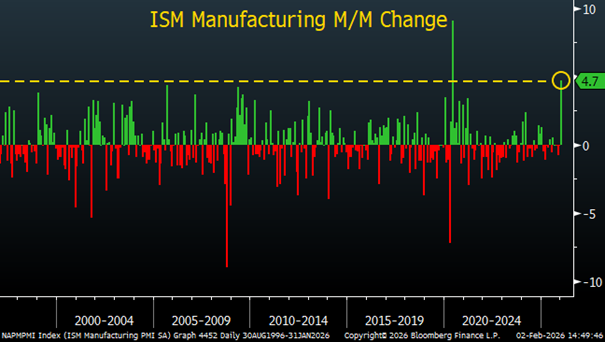

On Monday, February 2, the US manufacturing purchasing managers index was released. It showed the second largest month-over-month increase in the past 30 years. This has contributed to a strong start for cyclical companies in February and, if it holds, should be a significant ingredient for a stronger dollar.

Source: X

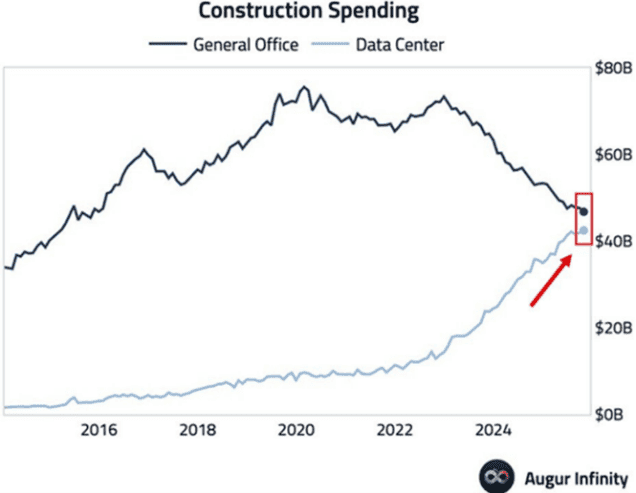

The expansion of data centres in the US continues unabated and is now on par with investments in office buildings.

Congratulations!

Source: X, BBC News

PORTFOLIO COMPANIES

Babcock

The news flow was dominated by several (above-mentioned) geopolitical conflicts, which caused defence-related stocks to rise during the month. Babcock was no exception. The stock rose by 15% during the month. In addition, the company released a financial update that was in line with expectations. In addition, a CEO change was announced from the esteemed David Lockwood, who has successfully implemented Babcock's restructuring in recent years. Lockwood is set to retire and hand over the baton to an internal candidate at the end of 2026.

FLSmidth

The mining equipment company's stock had a strong month. A couple of good reports from industry peers, Sandvik and Epiroc, did their part to fuel an already strong sentiment in January as gold and copper prices rose. Copper prices rose 5% in January and gold by 13%, despite declines of 3 and 9% respectively on the last day of the month. FLSmidth shares rose 22% in January. We took advantage of the situation and reduced our position.

Trigano

The French motorhome manufacturer released a sales update for the period covering September to November (broken financial year). Organic growth came in at 5%, which is an increase from the previous quarter (-5%), albeit below preliminary estimates. Pure motorhome sales rose by 7% in the quarter, while Trigano's more volatile holiday home segment saw sales decline by just over -20%. European distributors have for some time chipped away at a large stock that was built up in the years following Russia's invasion of Ukraine, which caused major supply disruptions. That stock has now almost normalized, which has resulted in Trigano gradually increasing its production again. This should mean clearly better profitability in the coming year.

Over time, Trigano may be able to use its market-leading position to negotiate lower prices with its suppliers. These cost savings are partly passed on to customers in the form of lower prices, which in turn should lead to even higher market shares. We note how the company has been gaining market share for many years and over the past 10 years the operating margin has risen from 6% in 2015 to our estimate of almost 11% in 2026. This is a very cyclical business, but since 2007, the average organic growth has been around 4% per year (CAGR). Since 2015, it has been close to 7% per year (CAGR), driven by the pandemic and an aging population. The share is valued at around P/E 10-11x on our estimates for the financial year ending August 2026.

The Trigano share was an outperformer for the fund in 2025, and we had reduced our position ahead of the report. During the month, the share fell by -4%.

Beijer Ref

The Beijer Ref share has not been a highlight for the fund since we started building a position in the summer of 2025. The company's strong Q3 report was followed by a softer Q4 report that showed marginally negative organic growth. Operating profit was a couple of percent below expectations. Management pointed to difficult comparison quarters and fewer working days (which we knew in advance). Profitability, adjusted for acquisition costs, improved in a good way, while the company generated a nice cash flow. The share fell -5% on the report day and fell -15% for the month as a whole. Outflows from Swedish small-cap funds and the "overhang" from EQT have not helped the share.

Although we had hoped for a better report, our investment thesis (read more from our monthly letter in October) has not changed significantly: Over the next 12–18 months, Beijer Ref should be able to return to organic growth of 4–6%. In addition, acquisitions are contributing positively to profit growth as the company digs up synergies in special purchasing. The acquisition rate has increased recently, which we see as positive. Cash flows have improved during the year, and the return on capital is heading in the right direction. The valuation of the share is lower than it has been in for a long time and since this summer we have seen several insider purchases. We have chosen to exploit the weakness by buying additional shares.

De’Longhi

The coffee machine manufacturer released preliminary figures for the fourth quarter of 2025. Sales were slightly better than expected. Organic growth was around 8%, a couple of percentage points better than we and others had expected. One of the most important drivers behind the development was once again the Professional Coffee segment, which sells coffee machines to cafes, bars, hotels and restaurants under the La Marzocco and Eversys brands. The segment's sales increased by a full 40% during the quarter.

De'Longhi's management has raised the possibility of a spin-off/stock exchange listing of the Professional Coffee segment. This is a business that should be able to grow double-digits for many years with operating margins exceeding 25% at the EBITDA level. We estimate that De'Longhi's share in the deal could be worth close to 1.5 billion euros, which would then value the remaining business at around 7x EV/EBITDA. It appears cheap for a business that should generate at least five percent growth per year with rising margins.

We are not big supporters of sum of the parts valuations unless there are clear indications that management is willing to make structural changes. We have such indications in De’Longhi, and we believe and hope that a spin-off will be announced in the next 12 months. De’Longhi shares rose by 2% in January.

Bonesupport

Due to the uncertainty and question marks that have been in the stock market regarding Bonesupport's sales development, the company chose to communicate preliminary figures for sales and its expected sales growth for 2026. Growth for the full year 2025 amounted to approximately 40% organically, which is in line with what the company communicated a year ago. This includes some headwinds that have arisen outside the company's control, including reprioritizations within the NHS in the UK, which continues to struggle with long waiting lists after the pandemic. Development in Germany has also been sluggish, where a pressured hospital system has led to extensive cost savings.

The most important component for the company and the investment case is the development of Cerement G in the US, which appears to have continued strong growth during the fourth quarter. For 2026, the company expects growth of over 35% in constant currency, which was just above analysts' forecasts. Bonesupport has recently been affected by downward revisions, mainly linked to a weaker dollar, but the underlying business continues to develop at a good pace. The share rose almost 4% in January.

WDP

Warehouses de Pauw is a new and smaller holding in the fund. Simply put, it is a Belgian logistics real estate company with operations in Belgium, the Netherlands, France, Germany and Romania. In January, WDP presented its fourth quarter report, which was fully in line with expectations. The forecast for 2026 also corresponded to market estimates. The report was well received and likely mainly driven by new financial targets extending until 2030, where the company expects to increase earnings per share by just over 6% per year. This, together with positive comments that customers have started to expand again after a Covid-related hangover, contributed to the share rising 3% on the report day and 8% during January.

Continental

Continental published preliminary figures for the fourth quarter in January. The ContiTech segment was slightly worse than expected, while the core Tires business was in line with forecasts. Continental plans to divest ContiTech in 2026, making the result of Tires by far the most important part of the report. The deviation in ContiTech does not significantly affect the sales process and the company states that interest from potential buyers remains high.

Analysts value ContiTech at between 2.5 and 7 billion euros, where our view is around 4–5 billion, which would correspond to a full 20–25 euros per share. Continental's tire business generates strong cash flows and around 75–80% of sales are replacements for worn-out tires, which is defensive in nature. According to our calculations, the company could distribute up to 80% of the sales proceeds in the form of an extra dividend (which it has announced it will do), which if we are right is at least 15 euros per share or a dividend yield of just over 20%. What then remains is a company that is currently valued at just over 7x P/E 2026e, where Michelin and Pirelli are valued at around 11x. At the same time, it has a return on capital well above the cost of capital and significantly above Michelin. There seems to be a disconnect and we could have almost 50% upside in the share after receiving 15 euros in extra dividend.

Traton

Traton announced its volume sales for the fourth quarter and full year 2025. The number of units delivered decreased by 8% compared to 2024. However, this had limited impact on the share as the company told the market the next day that free cash flow exceeded market expectations by a full 63%. The improvement came mainly from better working capital management and lower investments. During the month, both Paccar and Volvo presented strong reports and raised their forecasts for the number of units delivered in 2026 in both Europe and the US, which was received positively by the market. Traton rose 5% in January.

SUMMARY

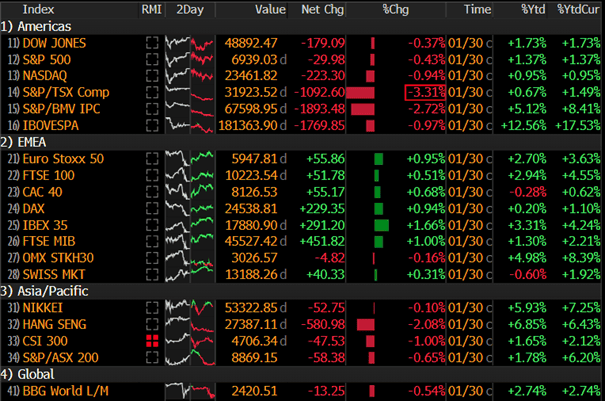

European stock markets continue to develop stronger than their American counterparts. Nasdaq was the weakest of the American indices and Mag7 has basically traded sideways since September last year. In addition, the strongest development in January was the Russell2000, which for 14 days in a row (!) had a stronger development than the S&P500, which is extremely unusual, and rose by 5.3%.

Below, performance in January measured in local currency in the penultimate right-hand column and in USD farthest to the right. Note that Sweden has started the year as one of the world's best stock markets.

Source: Bloomberg

Having said that, it is remarkable that Swedish small-caps, after a weak 2025, had a negative return of 4.2% in January. It is likely that outflows from smaller company funds are contributing to this, but in addition, there are major changes in the state AP funds whereby AP1 is divided equally between AP3 and AP4 while AP2 and AP6 are merged. This likely lead to major adjustments in positions.

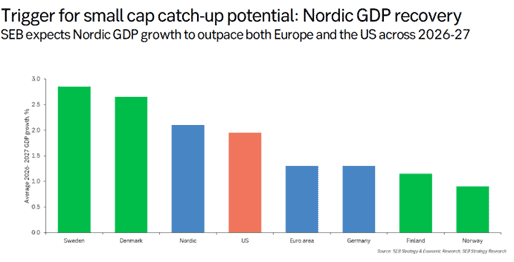

We note that the five largest negative contributions in January are Indutrade, Beijer Ref, Addtech, Trelleborg and Getinge, with the common denominator that they are larger companies and popular SMID stocks that can provide quick liquidity in the event of outflows. The other and positive side of the coin is that the weak start in combination with a record strong Swedish krona will likely attract more foreign investors and then things can reverse quickly. In addition, small companies typically develop stronger than larger companies when the domestic economy is growing. This may come back and bite us, but the outlook for this year looks unusually promising for Nordic small companies, see image below.

Source: SEB Strategy & Economic Research, SEB Strategy Research

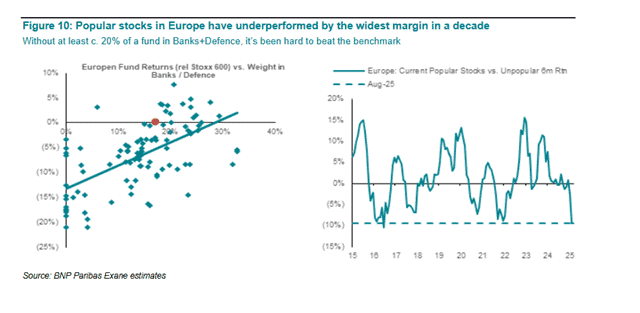

The trend of popular stocks underperforming the broader market also applies in Europe, where banking and defence stocks have been the outliers over the past year. The fund has just over 10% in these sectors in the form of Babcock and Bawag, which continued to perform strongly in January.

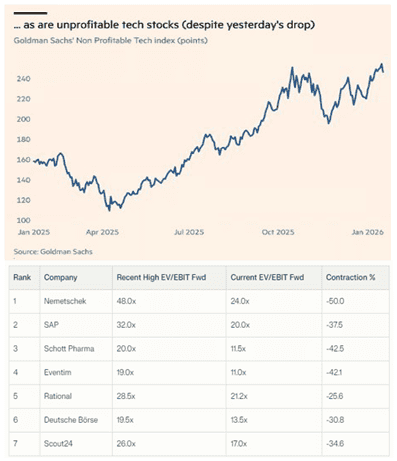

The Goldman Sachs index for unprofitable technology companies had a very strong performance last year while many manager favourites had the opposite, see image below. On that theme, German Rational, which can be seen in the image below, is a new holding for the fund and we will return to it in upcoming monthly letters.

Source: Financial Times, Goldman Sachs

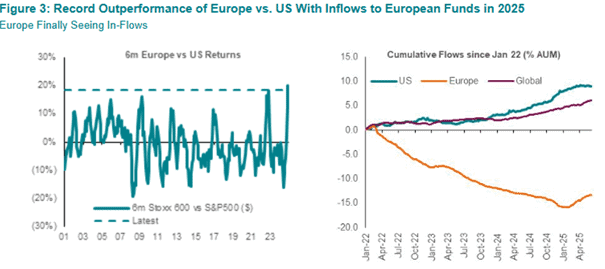

The image below on the left clearly shows the difference in returns between the SXXP600 and the S&P500 over the past six months and measured in USD. The image on the right shows that inflows to European equity markets increased last year while pure US equity funds decreased slightly. Global equity funds saw continued inflows.

Source: BNP Paribas Exane

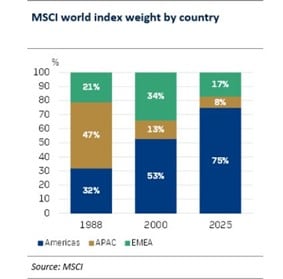

The image below shows an incredible development in the distribution of geographical regions in a world index. An indexed global fund is thus 75% American stocks, with Mag7 being closer to 40% of that. In 1988 it was 32%.

Source: MSCI, @BodenPJ

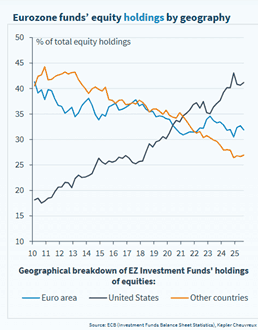

Since 2010, equity funds in Europe have increased their US exposure from just under 20% to just over 40%, while at the same time the European share has decreased from around 40% to around 30%. It is likely that the reversal that began in 2025 will continue this year, thereby contributing to a positive return in Europe.

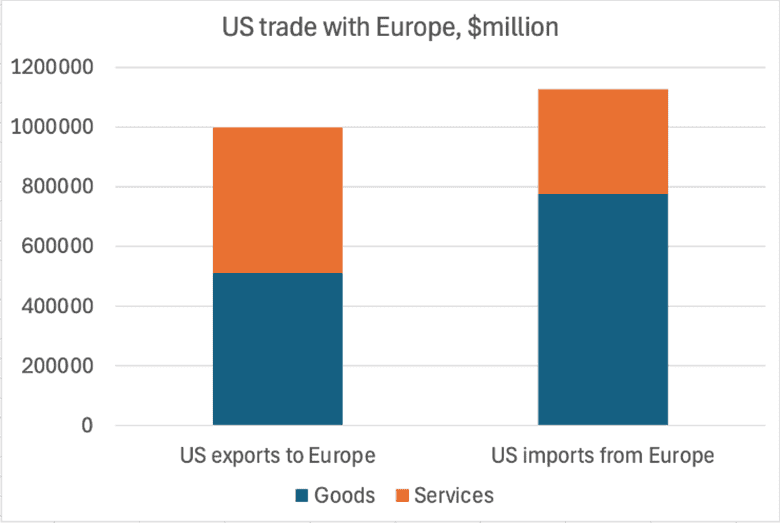

In the event of an escalation of tariffs and a possible trade war, the US will not go unnoticed. Below are US exports and imports with Europe.

Source: Bureau of Economic Analysis

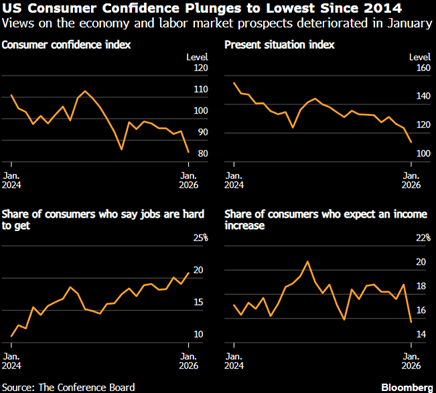

It is encouraging to see the US economy accelerating and the Fed now estimates GDP growth at over four percent. Link to article.

At the same time, the mood of US consumers is at unusually low levels, indicating a major dissonance between how ordinary people perceive the economy and industrial activity – a “K-economy”.

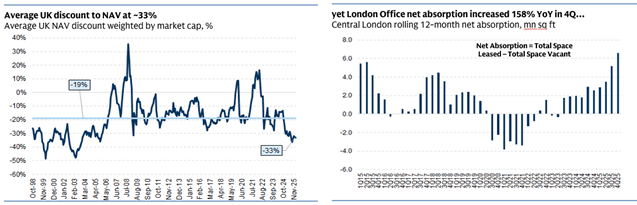

Many of us were disappointed with how European real estate stocks performed last year. British property stocks are now valued at around a 30% discount to NAV, which is historically high (low valuation). What is particularly interesting is that net office take-up relative to vacancy hit a new high for a quarter. We also note that two of the companies now have activist funds as owners. Are property stocks finally on the way? There is much to suggest so. The fact that the property bond market is red hot while the stocks are trading extremely modestly is a mystery to the undersigned. If anyone can explain why, feel free to get in touch. The fund has holdings in SLP and Belgian WDP, both of which are logistics companies.

Source: Berenberg

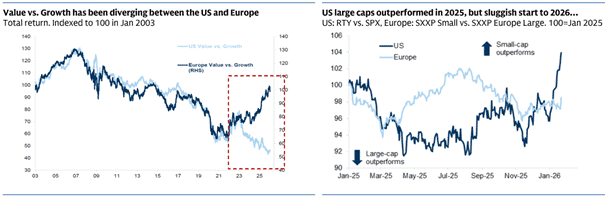

The difference between the performance of value and growth stocks in the US and Europe has been enormous over the past year, with value stocks performing significantly stronger than growth stocks and the opposite in the US. The image on the right shows the explosive start of US small-cap stocks in 2026, and we hope the trend will spread to this side of the Atlantic.

Source: Goldman Sachs

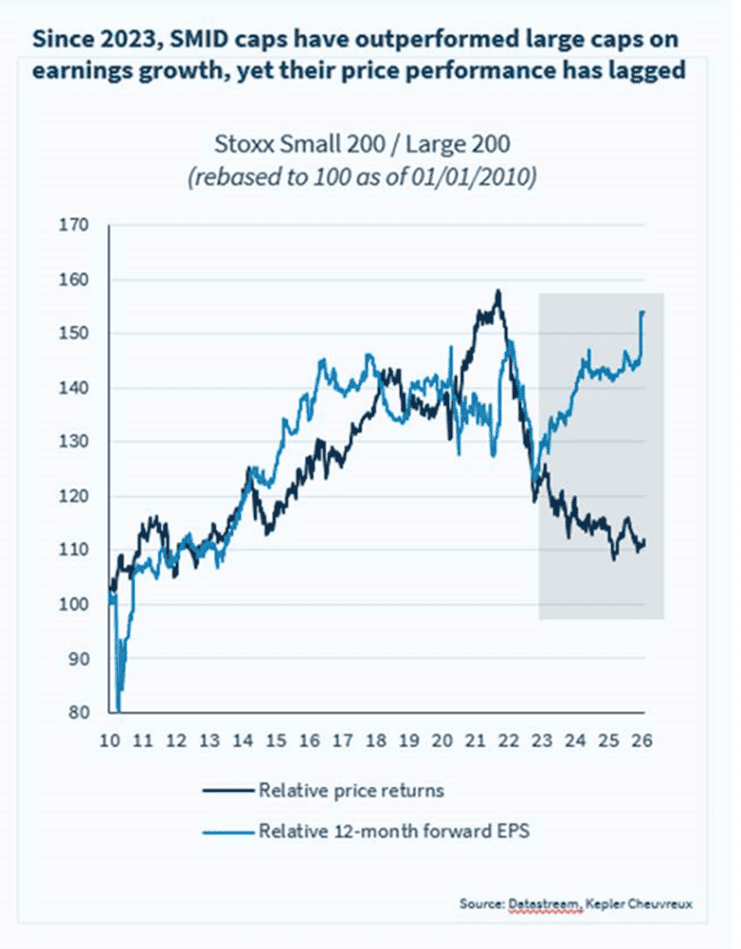

Despite significantly better profit development for smaller European companies compared to larger companies, this is not reflected in the price development. With this asset class, patience is a virtue, but when the trend turns, it can be quick.

The picture clearly shows that there is significant value to be found among European small companies.

Source: Datastream, Kepler Cheuvreux

On the last day of the month, we received data on Europe's GDP for the fourth quarter, which showed 0.3% growth compared to the expected 0.2. This is clearly lower than the corresponding data for the American economy, but on the other hand, it is doped with 7-8% annual budget deficits that have dramatically increased debt. Soon, the US national debt will be 125% of GDP and the IMF's latest forecast shows that it will reach 143% as early as 2030. The corresponding debt in the Eurozone is 90%. The US interest costs are already enormous and in practice one must borrow to pay them.

The constant deficits have been covered by capital inflows from the outside world, not least Europe. Accelerating indebtedness will place great demands on the US's borrowing capacity. Interestingly the US is currently pursuing geopolitical blackmail against Europe at the same time as China has gradually reduced its purchases of US government bonds. The consequence of this, at some point in the future, is likely to be that the US will need to drastically tighten fiscal policy, and/or raise interest rates to attract global investors or force the Fed to buy large volumes of government bonds as it did during the corona crisis, which in turn led to a sharp rise in inflation. We can only hope that American politicians will start cutting their coats according to their cloths, but right now there are no signs of that, quite the opposite.

Source: X

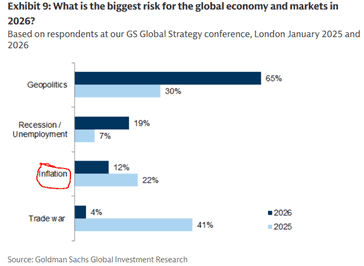

Goldman Sachs asked investors in January about the biggest risks for them as investors. Geopolitics emerged as the biggest risk compared to trade wars last year. We note that Polymarket puts a 39% probability that the US will strike Iran in February and a full 61% probability in the first half of the year.

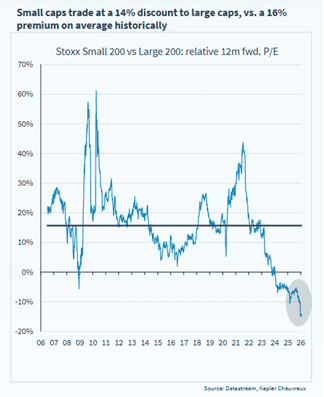

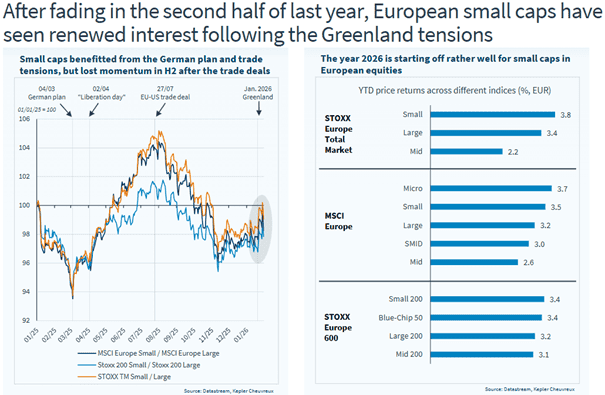

The turbulence with Greenland contributed to European small companies developing more strongly than larger companies.

Source: Datastream, Kepler Cheuvreux

In conclusion, European stocks, except for Sweden, have had a strong start to the year. If the dollar continues to weaken this year, it will have negative effects on profits, which will then be a continued headwind for the larger global companies in particular, so a stabilization of the dollar is desirable.

In the US, it seems that some doubt has arisen regarding the profitability of the gigantic AI investments being made and we suspect that this will be a recurring theme during the year.

The reporting season is in full swing, and the general impression is that margins are somewhat weaker than expected and currency effects are significant, especially Swedish ones that are denominated in last year's strongest currency. The fund has already had 11 companies announce sales and/or results, which corresponds to a full 44% of the portfolio. With the exception of Beijer Ref, which came on the last day of the month and was slightly below expectations, the fund's reporting season has started well.

If you still have the interest to hear more from the undersigned, you can listen to a podcast here.

A big thank you to Sofia Hårdänge at Placera for letting me be part of it!

Thank you for your interest and we will continue to plough through reports during February.

Mikael & Team

Malmö, February 4th, 2026

IMPORTANT INFORMATION. This is a marketing communication. Before making any final investment decisions, please refer to the prospectus of Coeli SICAV II, its Annual Report, and the KID of the relevant Sub-Fund. Relevant information documents are available in English at coeli.com. A summary of investor rights will be available at https://coeli.com/financial-and-legal-information/.

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested. Please note that the management company of the fund may decide to terminate the arrangements made for the marketing of the fund in one or multiple jurisdictions in which there exists arrangements for marketing.