Note that the information below describes the share class (I SEK), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class' return. The information below regarding returns therefore differs from the returns in other share classes.

Monthly Newsletter Coeli Absolute European Equity October 2021

October performance

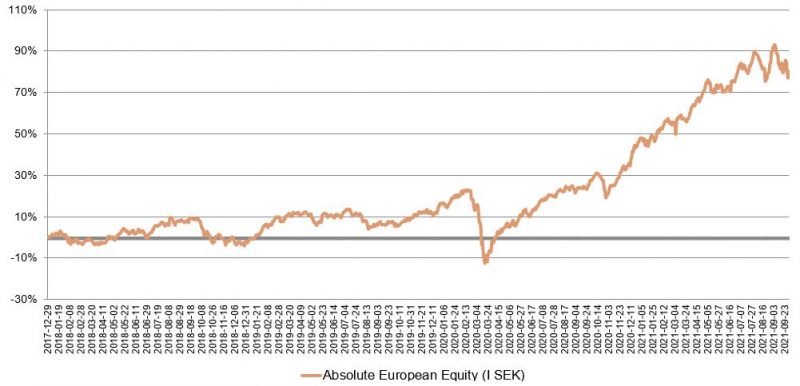

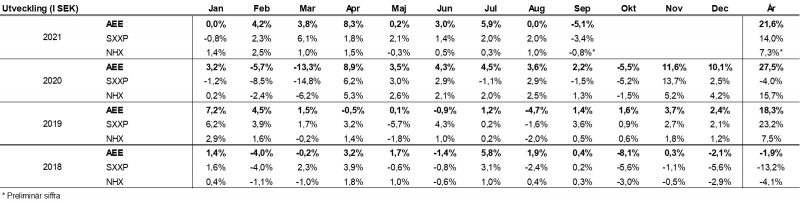

Fondens värde sjönk -5,1 procent i september (andelsklass I SEK). Stoxx600 (brett Europaindex) sjönk under samma period med -3,4 procent och HedgeNordics NHX Equities sjönk preliminärt -0,8 procent. Motsvarande siffror för 2021 är en ökning om +21,6 procent för fonden, +14,0 procent för Stoxx600 och +7,3 procent för NHX Equities.

Aktiemarknader/Makro

October has again, as many previous years, shown that it has an undeservedly bad reputation in terms of returns. The broad European index returned a positive 4.6 percent while the S&P500 rose by 6.9 percent. It was thus the second-best month for Europe and best month for the U.S. so far. The fund's return landed at x percent where the concentration of contributions, both positive and negative, was unusually high. Truecaller had the highest positive attribution by far, more about that later.

However, volatility has historically been at its highest in October. That was not the case this year if you look at the large broad indices. On the other hand, stock-level movements were very high in several places. Below is the volatility index for S&P500 which are now at pre-pandemic levels.

Source: Bloomberg

In other words, a limited number of large companies have recently driven the broad indices. Among the medium-sized and smaller companies, there has in many cases been a substantial correction since August when the market changed direction. For the SXXP600 and the S&P500, the decline during this period was at its most 6 percent. Here are some examples of return distributions of our holdings from the highest to lowest during roughly a month’s time: Photocure -32 percent, Lindab

-12 percent, Victoria -16 percent. The sharp turnaround at the end of the month resulted in +18 percent, +27 percent (!) and +14 percent respectively.

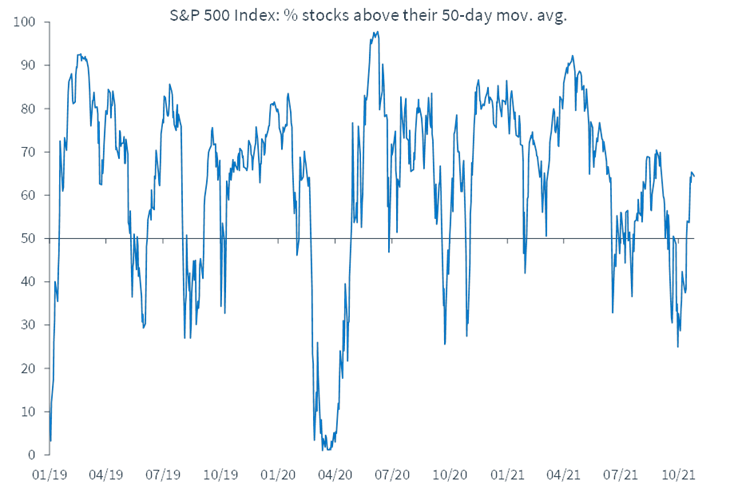

The picture below shows that only 150 of a total of 500 companies were traded above their 50-day moving average at the beginning of the month. It apparently indicated an oversold market and the rebound also came entirely as a classic textbook scenario. Now, two weeks later, the corresponding figure is just over 60 percent.

Source: Kepler Cheuvreux

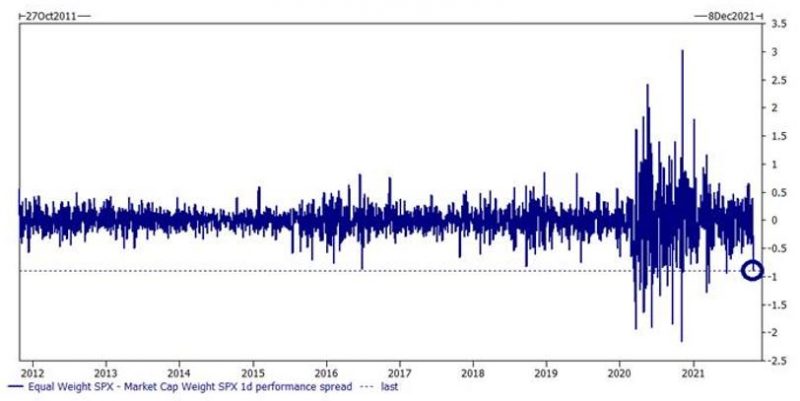

During the last week of October, market concentration was at extremely high levels. On Wednesday, October 27, we experienced the lowest breadth sessions in the market in almost a decade. Breadth is defined as equal weighted S&P500 versus market cap weighted S&P500.

Source: Goldman Sachs

Why did the market change character after the summer? During the first half of the year, we were all in the best of worlds with maximum acceleration of earnings, upward revisions of profit estimates every week and with inflation that remained low. Interest rate increases could not be discerned. Now we have a (temporarily?) sharply rising inflation and rising interest rates, even though interest rate is from extremely low levels. We can now anticipate the end of an unprecedented party where the host couple consisted partly of world central banks and partly of panicked politicians who invested huge sums to mitigate the effects of the pandemic. The hangover will come, but it is many monthly letters away (we think). Below is the quarterly profit development for American companies. The rate of acceleration decreases but is still very good.

Source: Goldman Sachs

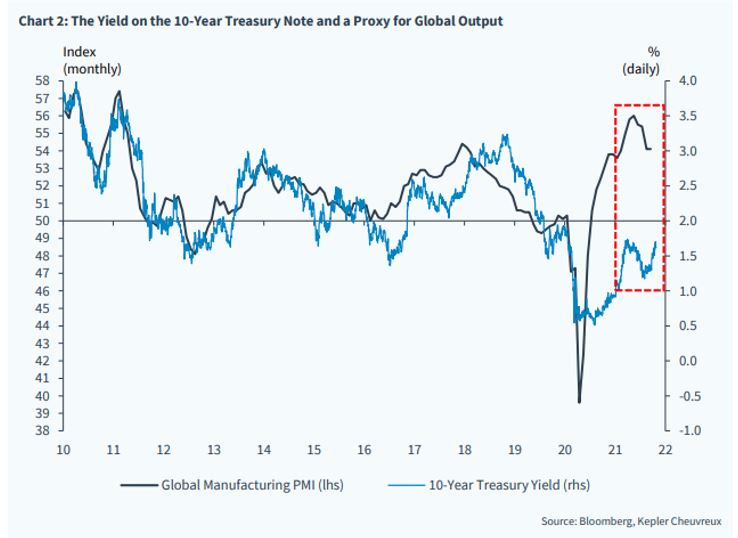

The historical correlation between the world's total manufacturing industry and the US 10-year interest rate has been completely decoupled since the outbreak of the pandemic, although it is now beginning to contract. That the interest rate will continue to rise slightly next year feels reasonable. That activity in the world's manufacturing industry is declining somewhat also feels reasonable, given that we come from very high levels. The correlation is likely to increase next year (and thus the imbalances will decrease).

Source: Kepler Cheuvreux

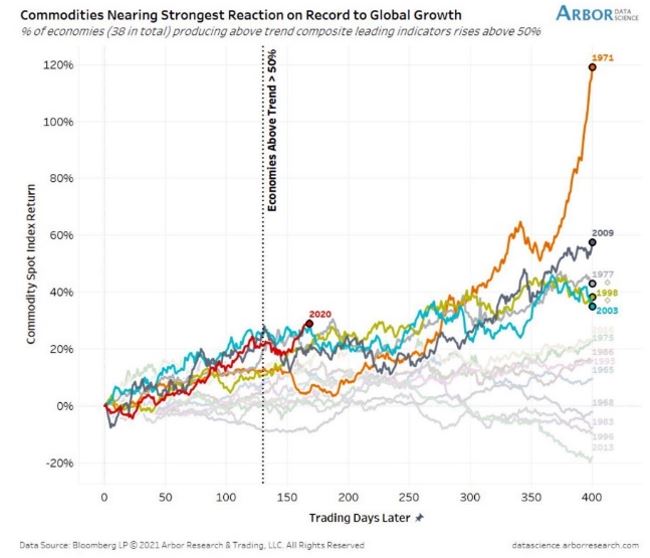

Raw materials, including oil, petrol and natural gas, have been the largest contributors to inflationary pressures. Inflation is expected to reach its maximum soon and then fall. At present, inflation is expected to peak in December with a 6 percent increase in the United States and 4 percent in Europe. We neither believe nor hope that the development for raw materials will continue on the same track as in 1971, see picture below.

Source: datascience.arborresearch.com

Europe is particularly vulnerable in terms of rising energy prices, as in a short time we have been made very dependent on the weather to produce enough energy. Sweden is perhaps the clearest example in Europe where we have for a long time had a well-thought-out, functioning and cost-effective electricity system that delivered safe electricity with small environmental consequences (hydropower and nuclear power). Politicians carry a very large responsibility for this disaster, and we now face great challenges to get the entire energy system into balance. It will most certainly take ten years. The gift and transfer union, EU, is busy printing checks to economically weak households so they can afford to pay for the heat to the home. It does not feel completely stable.

Below is a new proposal for this year's Christmas present:

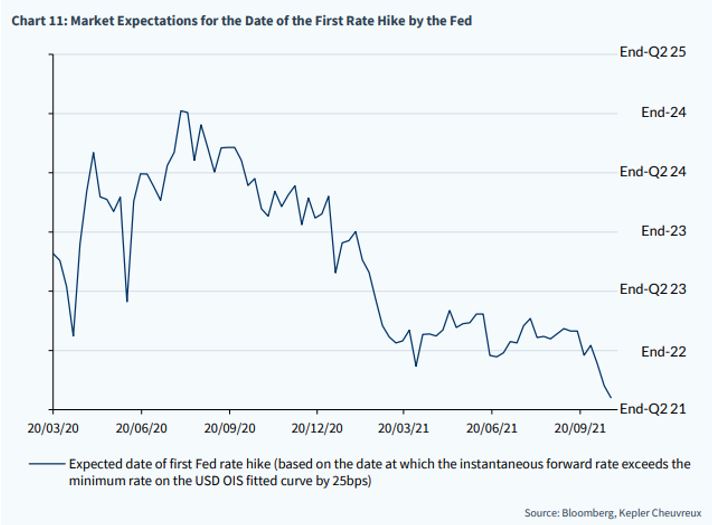

Inflationary pressures have meant that the market's expectations of the US Federal Reserve's first rate hike is going to be much sooner, see below.

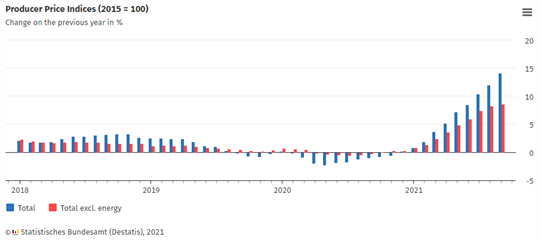

German producer prices rose by as much as 14.2 percent in September. The sharpest increase since October 1974!

Euro inflation usually correlates strongly with the German 10-year government bond. That’s no longer the case and may well be interpreted as the market is of the opinion that it is temporary, or that the central banks are destroying all price dynamics. "Cash is trash" applies. If capital is not put to work through various investments, valuations are quickly diminished.

Source: Bloomberg

Another indicator that clearly shows how production capacity lags demand and creates imbalances in the systems, the stock of cars in the American market has plummeted and is now at record low levels. These inventory levels will be rebuilt in the coming years to return to the levels five years ago.

Source: Bloomberg

Sharply rising corporate profits in combination with rising interest rates have made equities the clear winner over bonds. China is excluded, but it can probably be attributed to a state apparatus that has greatly affected the business community in the country.

Source: Kepler Cheuvreux

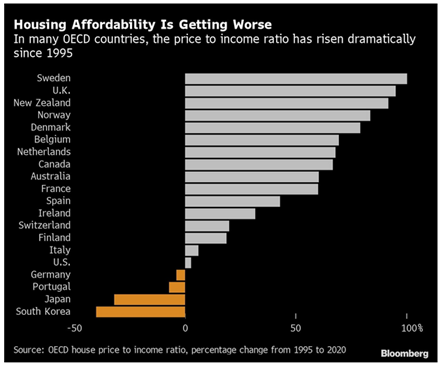

Asset inflation has exceeded wage inflation. It's not so strange considering that 20 percent of all US dollars available have been printed this year alone! The relationship between price and income has deteriorated drastically since 1995 in most OECD countries and particularly in Sweden. Note the difference between Sweden and Germany.

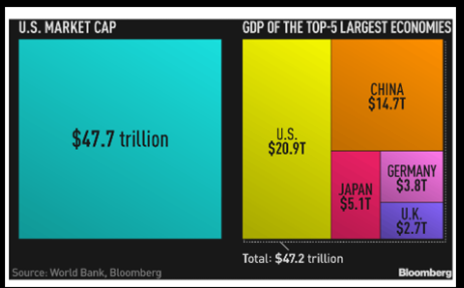

Speaking of asset inflation, the total market capitalization of the US stock exchange is now as large as the combined economy of the United States, Japan, Germany and the United Kingdom. When you take a stap back and grasp the size of the numbers it is astounding!

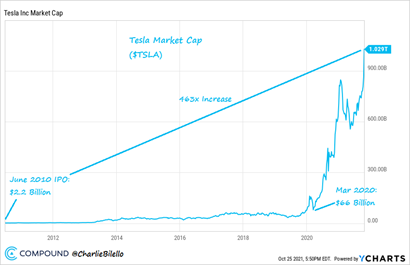

Tesla and Elon Musk are doing well now. Hertz placed a modest order for 100k cars from Tesla last week. The share price responded immediately and rose by 10 percent, thus exceeding the market capitalization of USD1000 billion. We'll take that one more time. Hertz, which has a market capitalization of $12 billion, placed an order with Tesla of $4 billion which caused Tesla's market capitalization to rise by $100 billion. We’re getting a vague feeling of euphoria. Elon Musk is in clear lead on Bloomberg's Rich List with a total fortune of USD302 billion, which corresponds to half of all goods and services sold in Sweden in one year. The only European is LVMH's founder Bernhard Arnault in an honourable third place. Elon has quickly climbed up the list. Just 18 months ago, he was not there at all.

Source: Bloomberg

Clearly the listing of Tesla 2010 has been successful (463x).

Source: Compound@CharlieBilello

In this regard, we cannot help but to past in the below tweet.

In conclusion and in the most absurd event since MFF (Malmö Football Team) left the Allsvenskan (Fotball League) in 1999. When the Norwegian police held a press conference about the recent tragic archery killings in Kongsberg, SVT (Swedish State Television) turned down the volume so that we would not hear what horrors had happened. We are undoubtedly the most anxious people in the world, but should we not at least be able to listen to the Norwegian police?

Source: Steget Efter

Long positions

Truecaller

In our previous monthly newsletter, we told you that we were an anchor investor in the upcoming IPO of Truecaller. Based on a range of SEK44 to 56, the listing price was finally set at SEK52 which meant a market capitalization of approximately SEK19.4 billion. The first trading day occurred on October 8th and we must, honestly, say that we were surprised by the trade. Many shares are listed on a stock exchange at a discount against a realistically estimated valuation and we thought that SEK 52 was an attractive entry price. The discount often gives a nice price development during the first trading day. That was not the case this time and the stock closed unchanged on the first day of trading.

We were frustrated and surprised by the price development, but we were all the happier when the management announced a few days later that the third quarter report would be brought forward from November 12th to October 27th. We could not interpret this as anything other than very positive and within a few minutes of the announcement we increased our already large position and increased it to the largest holding in the portfolio. Clearly aggressive given it was a new company in the portfolio, but we had a strong conviction that the market had not understood the power of the company's earning capacity. Despite this very positive news the share continued to hover strictly around SEK52, which was difficult to understand. As an anchor investor we had done a lot of analytical work of the company. Our sister fund, European Opportunities, has also owned shares (unlisted) since last spring, so we were well-informed, already, at the beginning of the listing process.

The fact of the matter is that at least one million shares had been lent out and thus sooner or later had to be bought back into the market. Of the 72 million shares invested on the day of listing, we estimated that up to 45 million were in relatively firm hands. That left a real free float of a modest 27 million shares. Since less than one million shares were traded on some of the days, we realized that a good report could make it difficult for short sellers who would need to cover their positions. This was additional motivation for us to buy more shares after the listing, as we thought that a potential short squeeze could give an extra boost to the share price once the report was out.

Then came the report day on October 27th. The figures were exceptionally strong, beating the analyst estimates we received by 22 and 68 percent respectively on sales and operating profit (before depreciation) and they were also better than our own high expectations. We acted quickly to buy more shares at the opening when the share price was only up 6-7 percent. Then began a spectacular price movement because of a spectacular report. The share price picked up speed and by the end of the day the share had risen by as much as 34 percent. As if that were not enough, the increase continued the next day with as much as 23 percent and the market value had then increased from about 20 billion to about 32 billion in two days. On the third day, the share was consolidated at high levels with a decline of around 5 percent.

We sold some shares the next day as we breached certain limits due to the extreme increase in the share price (it was our largest holding). We sold at high levels and that corresponded roughly to the number of shares we bought in the market after the IPO. That the market did not understand that bringing forward the reporting date was in practice a reverse profit warning is a mystery to us. That some players also went short at SEK52 is even more strange. For us, it strengthens our view that in-house analysis and hard work are the only ways to generate excess returns over time (if you ignore luck, but that is not a great strategy to rely on).

Comment: The Truecaller share was trading weakly up until the reporting day. After that it rose 56% in three days.

Source: Bloomberg

A central part of our investment thesis is that Truecaller has only scratched the surface when it comes to making money from a user base which now consists of just over 290 million people. The company has focused on building a good product and with a focus on acquiring users. From now on follows probably several years of low-hanging fruit where Truecaller can optimize its advertising business to drive sales. In addition, Truecaller is continuing its development of Truecaller for Business where the management sees a lot of potential.

The share rose by 59 percent from the listing price to the last trading day in October. Even with today's prices, we do not think that the valuation around 20x EBIT 2024e is particularly strained.

Lindab

We mentioned in last month's letter that the large number of inside purchases in Lindab prior to the report was going to bode well. This turned out to be true when Lindab (again) beat the analyst estimates by almost 15 percent - this on pre-expectations that we felt were high. We bow once again to the management of Lindab who has made an incredibly impressive quality improvement of the company. The share rose 26 percent in October and has risen by as much as 63 percent this year.

ArcticZymes

It is an advantage to have the ability to keep your cool when Norwegian ArcticZymes announces its quarterly reports. The enzyme company usually shows a large variation in sales and results between individual quarters. (We think that ArcticZymes should be assessed on a 12-month basis.) A large variation on a quarterly basis in combination with a typical volatile Norwegian stock market can cause strong price reactions. It was therefore a little extra gratifying that ArcticZymes this time was able to release good numbers and maintain its forecast for the full year. The share price rose 12 percent on the reporting day and 2 percent for the month.

Sedana Medical

One of the losers of the month was Sedana Medical. The price drop is due to the commercial manager (and former interim CEO), Jens Lindberg, accepting an offer as CEO of the healthcare company Medivir. Admittedly, it is sad that a commercial manager is leaving Sedana in the current launch phase, but as we understand it, there is no other underlying reason behind Lindberg's decision other than that he was interested in a CEO assignment. The share price reaction is, as we see it, a real overreaction and we have therefore increased our position by about 30 percent. The share price fell 16 percent in October. The company will present its interim report on the 4th of November.

Photocure, Victoria and ISS

A couple of our larger holdings, Photocure and Victoria, have had a relatively weak share price development in the last few months. In October, that trend reversed. Photocure rose 16 percent, while Victoria retaliated with a 14 percent increase. ISS is another one of our holdings that performed weakly over a period and did not follow Photocure and Victoria in October. Hopefully, this trend will reverse in November when ISS reports on developments in the third quarter. In connection with this, we believe that the company will update its forecast on profitability for the full year. We have increased our position in ISS over the past week.

Short positions

Exposure

Summary

During the first weeks of October stock prices fell and volatility increased. On October 15th, the PBOC (People's Bank of China) broke the silence about the real estate company Evergrande with the message that the financial risks are "controllable" and are unlikely to have any spill over effects. It was appreciated by the world's investors and a significant element of short covering contributed to the rise in equities (buy to close short positions). When the quarterly reports began to roll in, it provided additional fuel for the market to recover. The broad European index rose by 5.5 percent since the low level at the beginning of the month and the volatility index fell by about 35 percent.

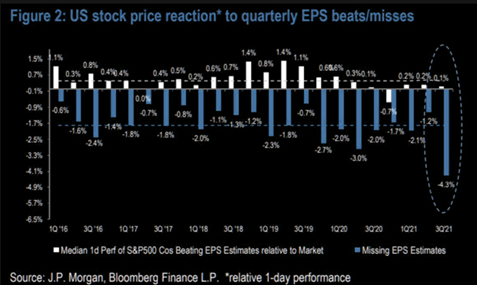

Companies that did not deliver, on the other hand, were severely punished and price movements for various shares were sometimes very high, see picture below.

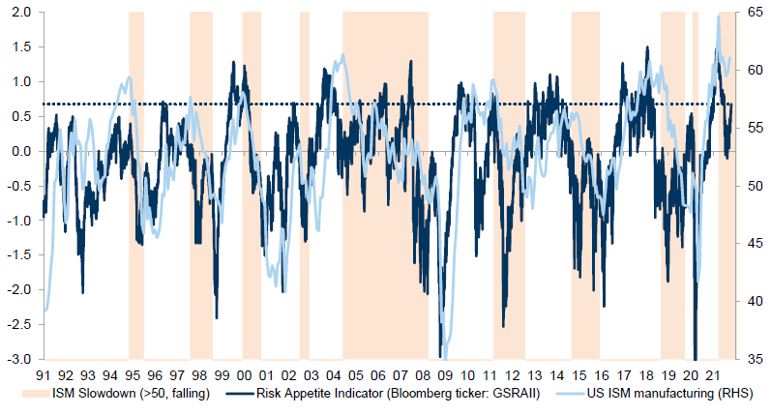

The picture below shows how risk appetite in the market has moved over the past 30 years. Falling ISM figures caused the risk appetite to fall after the summer, and then to rebound upwards in mid-October.

Source: Goldman Sachs

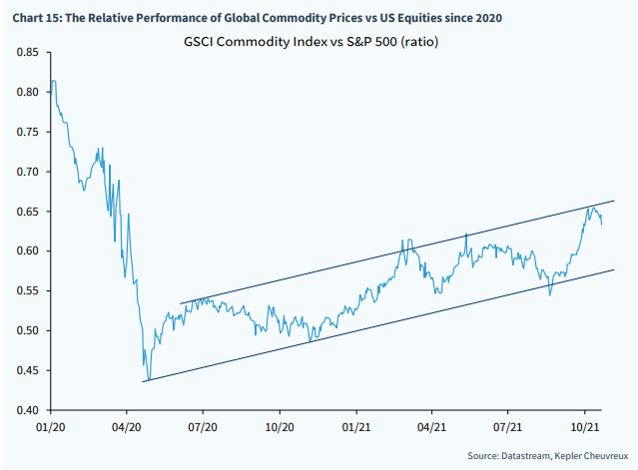

The central banks continue to light the inflation fire. A clear barometer is the price development for various commodities which has been very strong this year and which, together with cryptocurrencies, are the big winners so far. Below is the price development of raw materials compared with the stock market.

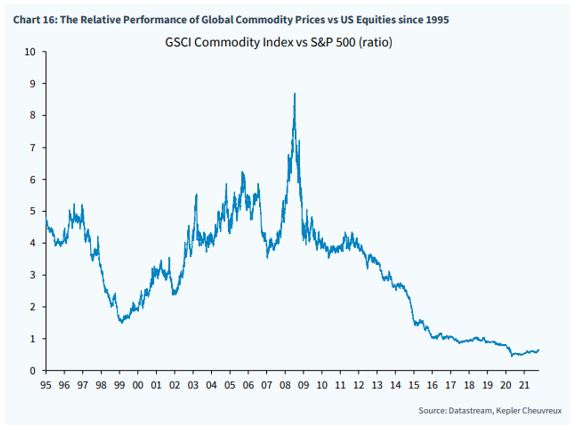

If you zoom out, the image becomes different. The peak in 2008 coincided with maximum growth in China. If you did not own a steel company during that period, you had problems with the portfolio.

The cryptocurrency victory marches continue as central banks reduce the value of money. Below is Bitcoin's price development over the last two years. Our unlisted holding in Bullish in which we invested in almost a year ago has likely developed well and will continue to do so.

Source: Bloomberg

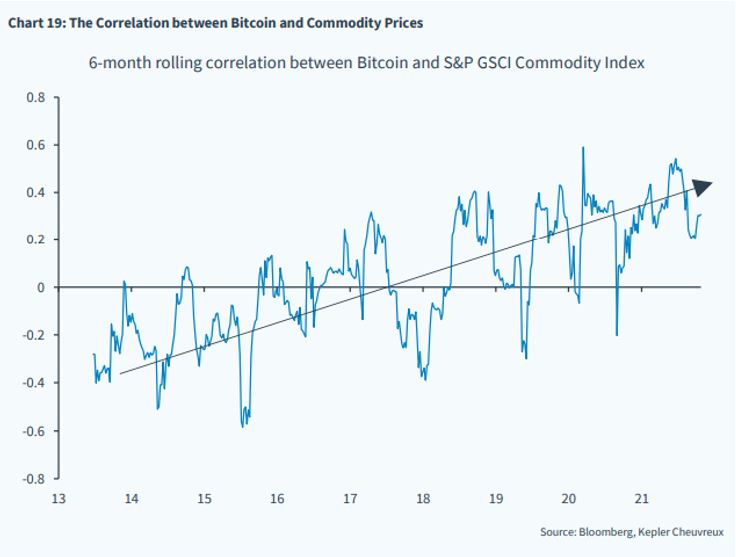

Interesting and clear pattern below. The correlation between Bitcoin and commodity prices. In general, rule number one for the next ten years is to own fixed assets. Rule number two and from a stock market perspective, allocate capital to companies that have pricing power and that are not pressured by rising costs. The companies that do not have that opportunity are structural and long-term losers which will be revalued at low multiples as a result.

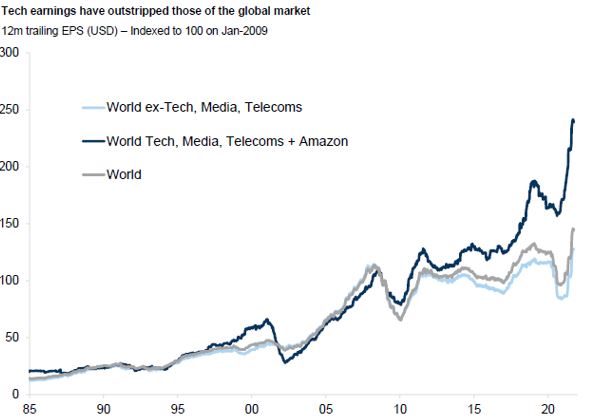

The valuation of the world's most important stock market, the US, has declined during the year for the five major technology giants. The other 495 companies have seen a slightly rising valuation.

The difference in valuation between the technology companies and other companies is easy to explain when studying profit growth for the past ten years. Interesting that the profits went hand in hand for the previous 25 years.

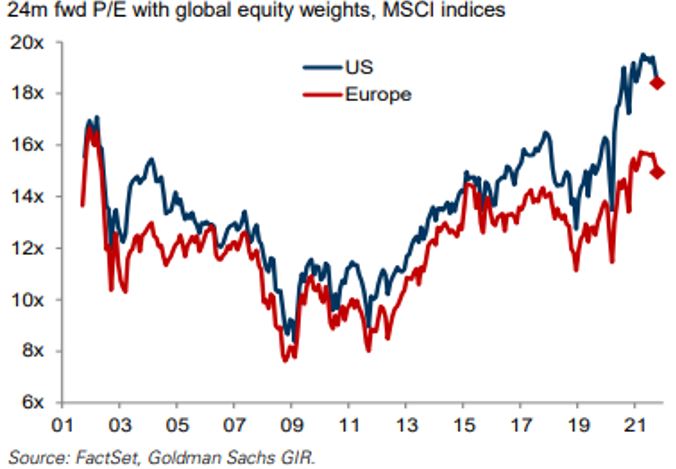

European values continue to be at significantly lower levels than American values. The fact that it has disintegrated in recent years is simply due to the unprecedented success of the major American technology giants both operationally and in the stock market.

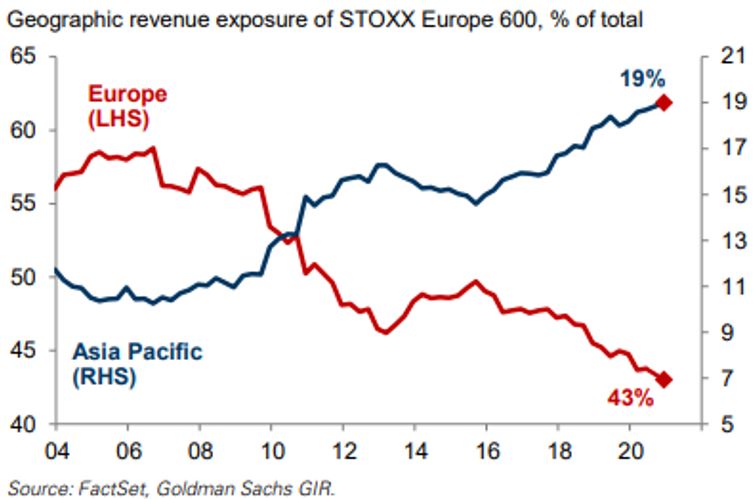

European companies are becoming increasingly global, which is clearly positive for the companies' earnings and their valuation.

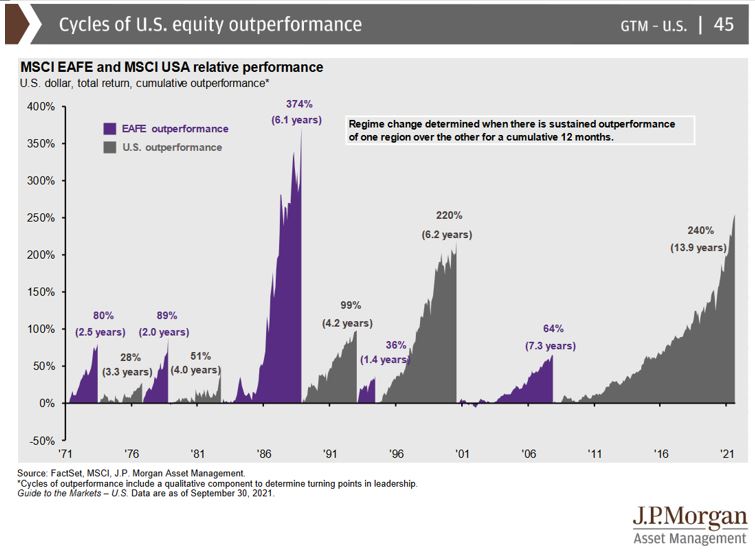

It has been around for a long time now, the US stock market's excess return compared to Europe's, Australia’s, and Asia's. There are several arguments as to why Europe could now break the trend:

- Low relative valuation

- Less exposure to low growth and more to global growth

- Europe has (after all) emerged from the pandemic better than many regions

- Diversification compared to the US with a high concentration of growth companies whose valuation is more affected by rising interest rates

- Mergers and acquisitions are heading for a record year in Europe

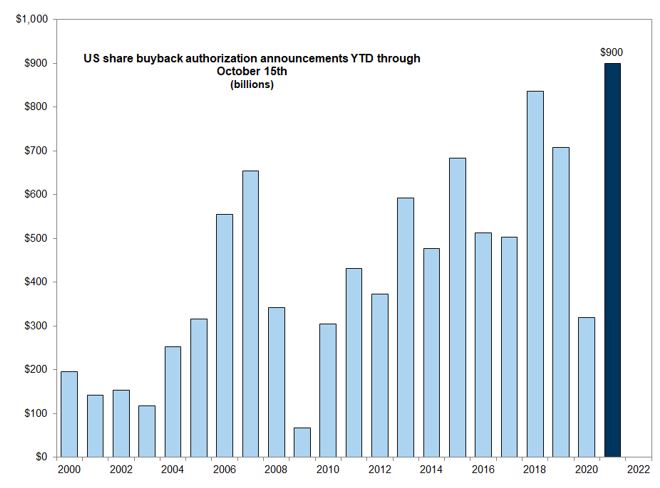

We are now rolling into the end of 2021, which as usual has been a very eventful year. We are certainly not in nirvana like at the beginning of the year when there were no clouds in the sky, but it still looks good (we think). After the reports, the share repurchases have begun to take place and will certainly have a positive effect on the share price in both the short and long term. Megatech companies Apple, Microsoft, Google and Facebook bought back shares for $55 billion in the third quarter and have a mandate to buy for another $250 billion (a lot of money). The four companies alone account for 18 percent of the S&P500 and 32 percent of the Nasdaq.

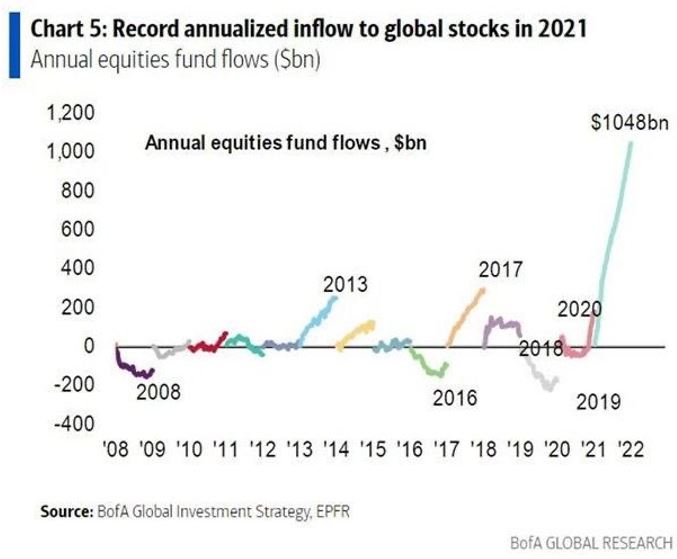

The inflows to the world's equity funds break all records and are off the charts. What to do when the central banks reduce the value of money, and you get around zero percent return on a bond when inflation is currently 4-5 percent?

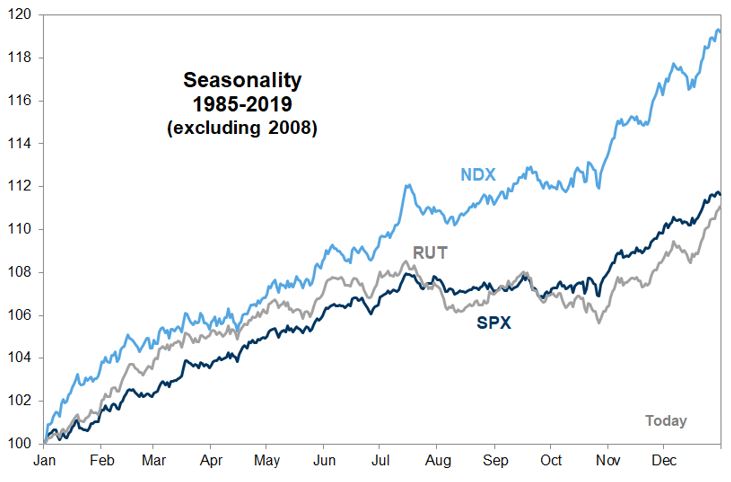

And the last picture for this time. With all the above said, we are now entering a period of historically strong returns and we believe that the same will happen this year as well. Profits continue to rise, repurchases start up after the reports, the options are few and who wants to buy bonds if interest rates rise, and you know you must pay to own them? Possibly we have a few weeks of minor turbulence, but then the path will continue again on its clear upward direction.

We round off with the following definition of a Bull Market:

Thank you for your trust and we are now changing gears for the final stretch!

Mikael & Team

Malmö November 3rd.