This material is marketing communication.

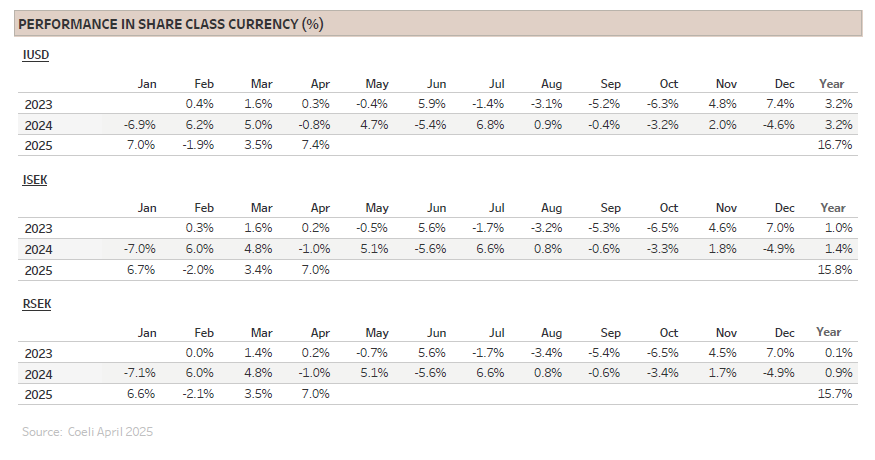

Note that the information below describes the share class (I USD), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class return. The information below regarding returns therefore differs from the returns in other share classes.

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

1) Share Class I USD

Performance for other share classes towards the end of the report.

FUND MANAGER COMMENTARY

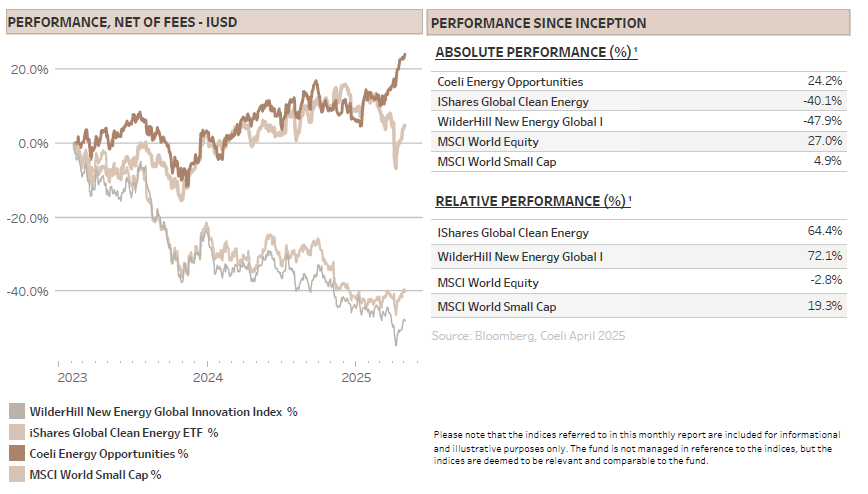

The Coeli Energy Opportunities fund gained 7.4% net of fees and expenses in April (I USD share class). Year-to-date, the fund is up 16.7% and it has gained 24.2% since inception in February 2023.

The fund outperformed the most comparable indices, the Wilderhill New Energy Global index (NEX) and the iShares Global Clean Energy (ICLN) by 4.0% and 4.3%, respectively. The year-to-date outperformance is 23% and 13%, and since inception the fund is ahead by 72% and 64%, respectively.

In the last monthly letter, we warned that market volatility would remain elevated following President Trump’s announcement of sweeping tariffs on ‘Liberation Day’. At the same time, we anticipated a de-escalation, noting how reciprocal tariffs were unlikely to be permanent as they were haphazardly pegged to last year’s trade deficit, and would inflict too much harm on the US economy and Trump’s popularity. Both forecasts proved accurate: volatility persisted in the immediate aftermath, with global markets experiencing sharp declines, but renewed optimism around possible trade negotiations helped drive a strong market recovery into month end. As a result, disciplined trading and effective stock picking enabled the fund to achieve one of its best months on both an absolute and a relative basis.

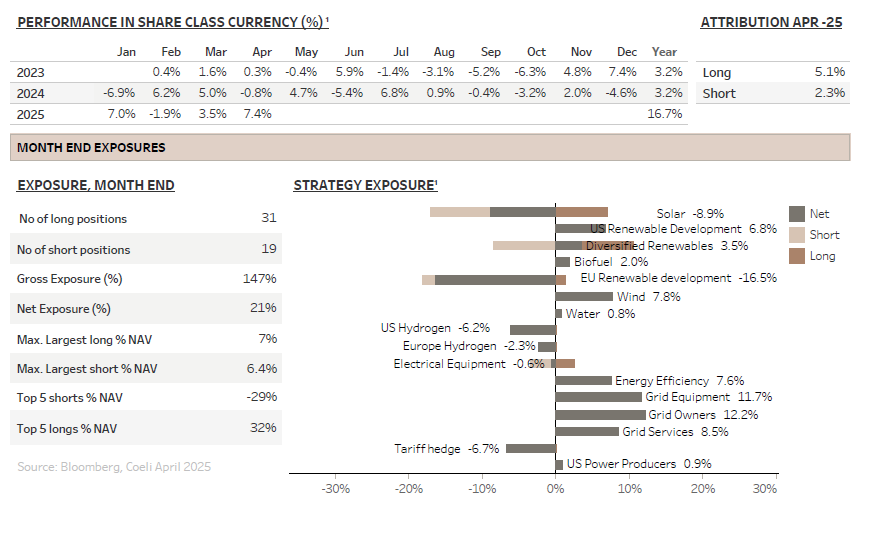

For the second consecutive month, more than 70% of the themes generated profits, and we are pleased that both the long and the short side contributed positively, adding 5.1% and 2.3%, respectively. The best performing thematic was the four grid related themes, which combined contributed 3.5% to NAV. Both ‘Grid Services’ and ‘Grid Equipment’ benefited from robust first-quarter earnings and positive guidance with limited impact from tariffs, at least so far. These stocks also rallied into month end, helped by renewed momentum in AI-related stocks as hyperscalers maintained their capex forecasts.

The only theme losing more than 1% of NAV was ‘Tariff hedge’, which was added at the beginning of the month as a precaution against potential escalation in trade tensions. The theme, which consists of short positions in transportation stocks vulnerable to a prolonged trade war, lost 1.1% of NAV in April.

Although markets have regained all their April losses and volatility has subsided, we remain concerned that investors are underestimating the economic damage caused by ongoing tariff uncertainty. The longer this uncertainty persists, the greater its negative impact on both consumer spending and corporate investment decisions, factors that will ultimately slow economic growth and erode future corporate profits. Reflecting our cautious outlook, we lowered our net exposure to 21% at month end, while gross exposure closed at 147%.

MARKET COMMENT – TARIFFS CAUSING EXTRAORDINARY VOLATILITY

The S&P 500 declined by only 0.8% in April, but this modest loss concealed a period of extraordinary volatility. At one point, the index was down by more than 14%, making April the fifth most volatile month in 85 years. The last time volatility reached such levels was in March 2020, when the Covid-19 shutdown triggered a market crash, which was subsequently countered by unprecedented fiscal and monetary stimulus.

While President Trump’s misguided tariff polices caused the sell-off, the recovery was triggered by the financial markets’ which sent bond yields surging and equity markets plunging forcing Trump’s hand. Only 13 hours after the reciprocal tariffs were introduced, the Trump administration introduced a 90 days pause on all countries except China. Soon after, the administration also eased tariffs on China by exempting various electronics, pharmaceuticals, certain energy/mineral products and many other products. Trump blinked, and he blinked more than once.

This was not a big surprise. We have long argued that Trump’s main priority is political self-preservation. Prolonged economic weakness would risk Republican control of Congress in next year’s midterms and make Trump a lame-duck president for the rest of his term. As a result, we expect further de-escalation and anticipate that the unsustainably high tariffs on China will start to come down sooner rather than later.

Nevertheless, as we argued in last month’s report, the 10% universal tariff is likely to remain for revenue generation purposes and sectoral tariffs will persist for national security reasons. Only reciprocal tariffs are likely to be negotiated away for most countries, with China being a notable exception. Still, timing is everything and as most trade agreements take years to negotiate, making even informal trade deals with over 100 countries in a matter of months is nearly impossible.

Even if the Trump administration manages to secure such agreements, we believe the economy is already damaged and it will only get worse the longer uncertainty persists. Although not yet visible in the hard, but backward-looking, macro data, forward-looking consumer confidence indicators are already flashing red. Expectations of business conditions and job availability have reached their lowest levels since the global financial crisis, and the average expected inflation rate in 12 months has soured to 7%. This complicates the Federal Reserve’s ability to cut rates aggressively to support equity markets. The bond market currently expects three rate cuts this year, similarly to its expectation the day before ‘Liberation Day’.

Moreover, while first quarter earnings held up better than expected, partly influenced by front loading of demand before ‘Liberation Day’, analysts’ earnings downgrades are 2.5x times more frequent than upgrades, a historical outlier. This might reflect that while many companies have removed full-year guidance, others have simply repeated the previous guidance as the tariff uncertainty is too great to quantify. We believe this might prove too optimistic in aggregate and see downward pressure on earnings for 2025 and 2026.

RENEWABLE ENERGY – TILTING AT WINDMILLS

It is common knowledge that President Trump has a strong dislike of wind farms. This sentiment reportedly began almost 20 years ago when he fought-and-lost-against the construction of an offshore wind farm near his golf course in Scottland. That dispute sparked his ongoing campaign against wind power. His core arguments are that wind farms are ugly, harmful to people (cancer), damaging to wildlife (birds killed and whales stranded), and uneconomic (he claims they are the most expensive energy source in the world). All these arguments, except the subjective first one, have been refuted by most experts.

Trump also campaigned on shutting down the US wind industry if elected. It was thus not a huge surprise that he banned new offshore leases on inauguration day. Still, most pundits, including us, assumed that projects with all federal permits would be allowed to proceed. We believed it would be legally difficult and potentially expensive to halt already-permitted projects. Additionally, electricity from offshore wind along the US East Coast is sorely needed, and since Trump promised on the campaign trail to halve energy costs, we assumed he would not halt incremental electricity production at great cost to private enterprises.

Well, we were wrong. In April, the Trump administration halted the permit for Equinor’s 810 Megawatt (MW) Empire Wind project off the coast of New York. The Department of the Interior concluded, after a permit review, that the federal approval had been rushed through by the Biden administration and lacked sufficient analysis and consultation. Equinor (EQNR) was ordered to halt construction until further review is completed to address serious deficiencies.

Three weeks later, the project remains halted, and the government has not provided any further reasons for the stop order. EQNR views this as an “extraordinary, unprecedented, and unlawful act” and is considering appropriate legal action. The longer the development is halted, the more at risk is the projected capex of USD 7bn. Although only USD 2.5bn had been invested by the end of last year, offshore wind developers typically lock up most of the supply chain at FID (final investment decision). While some suppliers might be able to reduce their costs and use capacity on other projects, it is expected that EQNR, as the developer, must carry at least 50%, and likely much more, of the remaining capex. To make matters worse, even if the government allows construction to proceed within weeks, the project might have incurred a year’s delay at significant additional cost. The seasonal window for installing offshore wind turbines is short, and delays multiply quickly and are costly.

We will follow developments closely but believe this has negative implications for other US offshore wind developers and their supply chains.

First, the reasoning for the permit delay seems arbitrary as the permitting process for Empire Wind started in 2016 and is the second longest of all US offshore wind permit processes. This argument could therefore be used against all permitted projects under construction.

Second, there is little difference between this project and, for example, Orsted’s (ORSTED DC) 924 MW Sunrise Wind (100% owned) development north of Empire Wind. Both projects received permits within months of each other and are at the same stage of development, with onshore construction commenced but no offshore work yet. In addition, Orsted has another project, 704 MW Revolution Wind (50% owned) off Rhode Island and Connecticut, which is about six months ahead of Sunrise, with foundations already installed and expected start-up in late 2026. Total capex for these two developments is about DKK 65bn, with about half still to be invested.

Third, this is clearly negative for the supply chain, even though turbine manufacturers like Vestas (VWS), supplier to EQNR’s Empire Wind, and Siemens Gamesa, supplier to Orsted’s two projects, as well as cable manufacturers like Nexans(NEX) (supplier to all three projects), claim to be contractually well covered. We believe this is the case, but there are always indirect costs to rescheduling large orders, especially when manufacturing hundreds of turbines, each the size of the Eiffel Tower.

We are not involved in Vestas, but we own Siemens Energy (ENR), not because of its ownership in Siemens Gamesa, but because of its booming power and transmission businesses. The fund also owns Nexans (NEX), but see the US offshore wind risk as manageable as it constitutes less than 3% of its transmission backlog, a subset of the whole business. NEX has completed production of the Empire cables, and if the project is cancelled, the company claims it would receive termination fees to cover the remaining margin. Moreover, Nexans’ work on Revolution Wind is largely complete and was recognized in the first quarter, while Nexans claims the potential loss from a cancelled Sunrise is minimal. Overall, we are comfortable with NEX’s US offshore wind exposure, although it is suboptimal to have manufacturing capacity for subsea cables in the US if EU imposes tariffs on US imports.

We are also involved in Cadeler (CADLR), the leading installer of offshore wind turbines, which has exposure to the US through one vessel working currently on Orsted’s Revolution and contracted to work on Sunrise until at least the end of 2026. If Orsted is forced to cancel or delay one or both projects, CADLR is expected to receive termination fees covering nearly all the remaining EBITDA. Compared to the other suppliers’ US offshore wind exposure, this is the one position that concerns us the least.

All in all, we are comfortable with our limited exposure to the US offshore wind sector but see significant risk to developers like Orsted if projects are cancelled or delayed. It is too harsh to assume that the company will be on the hook for 100% of remaining capex of about DKK 30-35bn, but when Orsted cancelled its Ocean Wind project last autumn, it ended up having to cover 75% of the remaining capex. Assuming the same ratio for Sunrise and Revolution would mean DKK 22-24bn, or about 20% of the market value of the company.

In addition to the risk of higher capex, lower earnings and cash flow from the US operations, Orsted faces several issues. First, farming down Sunrise was likely part of Orsted’s ambitious but necessary plan to raise cash as the balance sheet is strained and committed capex is high. Second, Orsted will have to pay tariff on imports to the US with no chance of reimbursement from customers. Third, Orsted is budgeting with the Inflation Reduction Act (IRA) Investment Tax Credit (ITC) of 30% and a 10% bonus adder (‘energy community’). We have argued that the 30% tax credit should be safe, but the bonus adder has little support among Republican representatives, making it an easy target in budget reconciliation. This would mean another significant impairment. However, considering the Trump administration’s deliberate sabotage of EQNR’s offshore wind project, is the 30% ITC on already committed offshore wind capex safe?

We are concerned about the recent developments in the US. The Republican party, once known as the party of business and defender of the rule of law, has shifted direction. Under President Trump, longstanding rules and norms, respected by both Democratic and Republican governments for decades, are being challenged or disregarded. While this may aim to deregulate and streamline government, the resulting uncertainty discourages business investments, at least in the short term. This heightened risk also raises the risk premium on US equities, lowers valuation multiples and makes US stocks less attractive to investors.

FUND PERFORMANCE – STRONG ABSOLUTE AND RELATIVE PERFORMANCE

The fund delivered strong returns of 7.4% in April, outperforming Russel 2000 and MSCI World Small Cap index by 10.1% and 6.8%, respectively.

April largely continued the strong performance seen in March, driven by effective stock picking and active trading capitalizing on the high volatility. We maintained our negative exposure to tariffs while increasing positions in stocks benefitting from higher fiscal spending in Europe. Although we reduced our net exposure to the AI power thematic, we retained enough to benefit as AI momentum returned at the end of the month. We are also pleased that the fund generated positive P&L not only during the rally in the second half of the month, but also during the initial sell-off following ‘Liberation Day’.

Alpha generation remains strong, with positive active returns in 72% of months since inception, 85% of the months on the short side and 59% on the long side. Active returns are calculated by scaling both the long and short side to 100% and comparing them to the average of the two most comparable indices. We believe this is an effective way to assess the quality of the stock picking on both the long and the short side.

While the best performing thematic was the four grid themes, the leading theme in April was ‘US Hydrogen’ adding 1.8% to NAV. We have over the last years written extensively about our negative view on the viability of most green hydrogen businesses, a view that has only strengthened as funding evaporates and projects get cancelled.

‘Grid Owners’ was the second-best performing theme in April, contributing 1.6% to NAV. As mentioned last month, electricity grid owners generate regulated returns that grows with increasing investments in the electricity networks, making these stocks defensive compounders. Moreover, with rising power demand, after decades of no growth, and a growing consensus that more renewable energy generation requires a stronger grid, it is now widely accepted that grid investments must increase significantly over the next decade.

Our two largest holdings in ‘Grid Owners’, Eon (EOAN) and Elia (ELI), both performed well in April. Elia gained almost 20% as it continued to recover from the long-awaited capital increase in March. Eon rose 10%, despite a mid-month sell off following some sell-side downgrades after the stock reached their price targets. We remain positive on Eon, as we see upside risk to both capex and allowed returns when the new German government implements its stimulus package.

The third-best performer was ‘Wind’, which added 1.0% to NAV. Our largest position is in wind turbine manufacturer Nordex (NDX1), which gained 15% during the month. Nordex is benefitting from both strong order intake in Germany and improving margins as low margin legacy projects are in the rear-view mirror. The company’s exposure to the onshore US wind market is insignificant which is positive considering Trump’s negative view on the industry. Nordex is also not involved in offshore wind, which we see as another positive. We have been invested in the stock for over a year but made it a sizeable position after the all-too-late exit from Vestas (VWS) in October. Nordex has since outperformed Vestas by more than 50%.

The ‘Grid Services’ and ‘Grid Equipment’ themes also performed well, contributing 1.0% and 0.8% to NAV, respectively. While robust first quarter earnings played a role, the main driver was renewed momentum in the powering AI trade, which had suffered after Deepseek was announced in January. The hyperscalers are not showing any sign of reducing capex, in fact, META increased full-year capex guidance by 9%. Most importantly, Microsoft denied outright cancelling data centre lease agreements and expressed optimism about improved return on AI investments. As we wrote in the March-25 investor letter “IS US TECHNOLOGY DOMINANCE UNDER THREAT?”, the hyperscalers need to see improved operating cash flows from AI sooner rather than later to sustain the current elevated capex levels. Microsoft addressed this concern, at least for now.

As mentioned earlier, we introduced a new theme at the beginning of April called ‘Tariff hedge’. The idea is to hedge out some of the risk that the trade war escalates post the 90-day pause on reciprocal tariffs or that it takes longer than anticipated for US-China tariffs to come down to a level well below 50%. The theme lost 1.1% of NAV in April, indicating it should provide protection if tariff risk rise again. We look to increase and broaden this theme over the next months.

The equity market has rebounded since financial markets stood up to Trump and forced him to blink on reciprocal tariffs. However, we worry the recovery has gone too far, too quickly. The next positive tariff news, the inevitable de-escalation between the US and China, appears to be almost fully priced into equities and could trigger a ‘sell-the news’ reaction. While tariffs will likely fall from current irrationally high levels, full trade agreements could take years to negotiate, and, in the meantime, uncertainty will persist. Moreover, the equity market has already priced out the risk of Trump re-introducing reciprocal tariffs on the rest of the world post the 90-day pause ending in early July. While we lean towards that view, we doubt Trump will relinquish this leverage before the end of the tariff pause, which could mean increased volatility in June and into July.

Overall, we remain cautious in the coming months and aim to continue trading the expected high volatility.

Thank you for your trust, and we look forward to updating you again next month.

Sincerely

Vidar Kalvoy & Joel Etzler

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

- Portfolio Manager and Founder of the Coeli Energy Opportunities Fund.

- Over 15 years of investment experience spanning both public markets and private equity.

- Managed the Coeli Energy Transition Fund from 2019 to 2023.

- Spent six years at Horizon Asset in London, a market-neutral hedge fund.

- Started working with Vidar Kalvoy in 2012.

- Five years in Private Equity at Morgan Stanley.

- Began his investment career in the technology sector at Swedbank Robur in Stockholm in 2006.

- Holds an MSc in Engineering from the Royal Institute of Technology (KTH), Stockholm.

- Portfolio Manager and Founder of the Coeli Energy Opportunities Fund.

- Has managed energy equities since 2006 and brings more than 20 years of experience in portfolio management and equity research.

- Managed the Coeli Energy Transition Fund from 2019 to 2023.

- Head of Energy Investments at Horizon Asset in London for nine years, a market-neutral hedge fund.

- Experience from energy investments at MKM Longboat in London and equity research in the technology sector in Frankfurt and Oslo.

- Holds an MBA from IESE in Barcelona and a Master’s in Business and Economics from the Norwegian School of Economics (NHH).

- Before entering finance, he served as a lieutenant in the Royal Norwegian Navy.

IMPORTANT INFORMATION. This is a marketing communication.

Before making any final investment decisions, please refer to the prospectus of Coeli SICAV II, its Annual Report, and the KID of the relevant Sub-Fund. Relevant information documents are available in English at coeli.com. A summary of investor rights will be available at https://coeli.com/financial-and-legal-information/.

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

Please note that the management company of the fund may decide to terminate the arrangements made for the marketing of the fund in one or multiple jurisdictions in which there exists arrangements for marketing.