This material is marketing communication.

Note that the information below describes the share class (I USD), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class return. The information below regarding returns therefore differs from the returns in other share classes.

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

1) Share Class I USD

Performance for other share classes towards the end of the report.

FUND MANAGER COMMENTARY

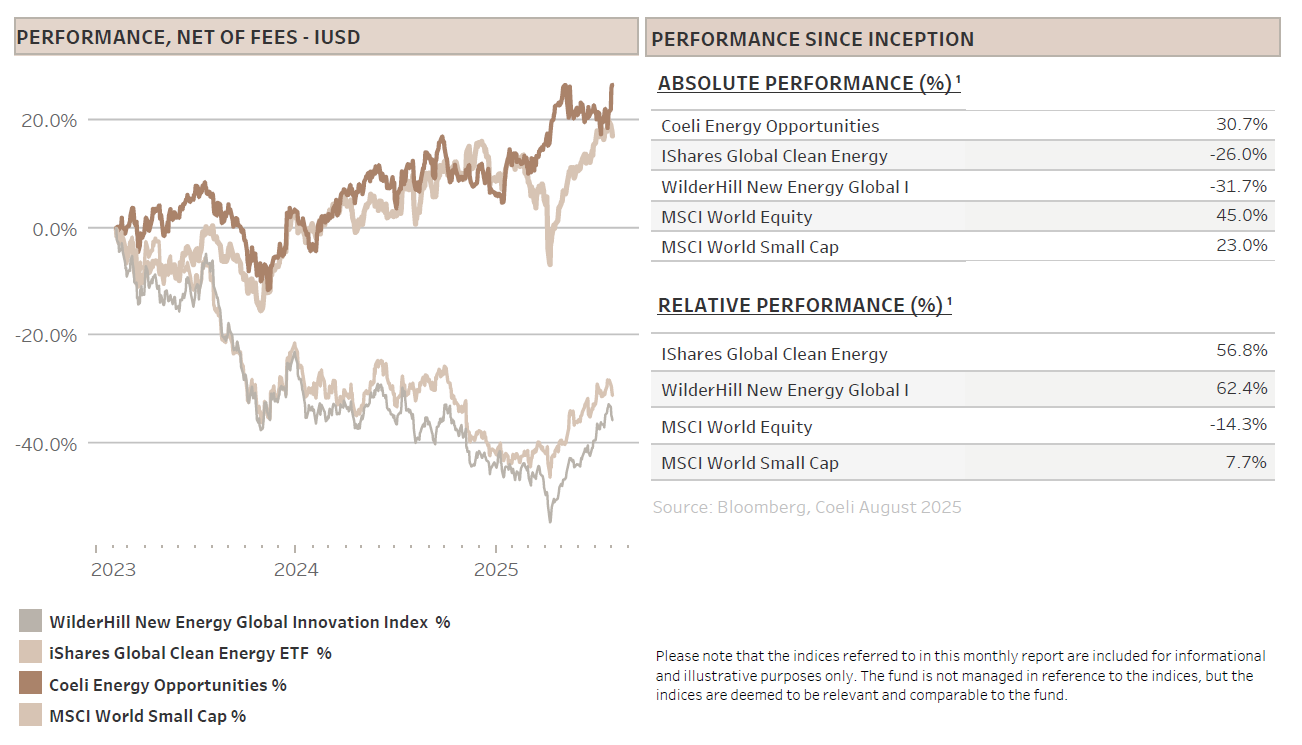

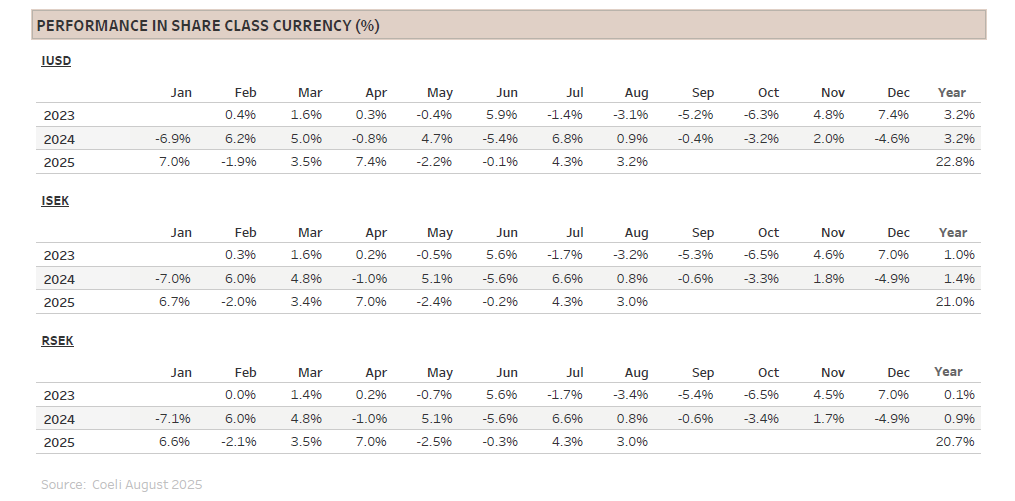

The Coeli Energy Opportunities fund gained 3.2% net of fees and expenses in August (I USD share class). Year-to-date, the fund is up 22.8% and it has gained 30.7% since inception in February 2023.

The fund underperformed the most comparable indices, the Wilderhill New Energy Global index (NEX) and the iShares Global Clean Energy (ICLN) by 3.0% and 4.1% in August. Year-to-date the fund is underperforming the NEX by 0.3% and ICLN by 5.0%. Since inception the fund is ahead by 62% and 57%, respectively.

The fund’s performance in August was solid overall. About 70% of the investment themes contributed positively to NAV, with profits generated on both the long and the short side. The best-performing theme, ‘EU Renewable Development’, added 1.6% to NAV, driven by gains from short positions in offshore wind. ‘Diversified Renewables’ also performed well, contributing 1.3% to NAV thanks to bitcoin miners and Bloom Energy (BE), a fuel cell provider benefiting from the AI-driven demand for power. Other powering-AI related themes delivered mixed results. While ‘Electrical Components’ and ‘Grid Services’ combined detracted 0.7% from NAV, this was offset by positive returns in ‘Grid Equipment’. Although we remain strong believers in the AI investment theme, we continue to reduce and hedge some of our long exposure to AI enablers providing infrastructure and power.

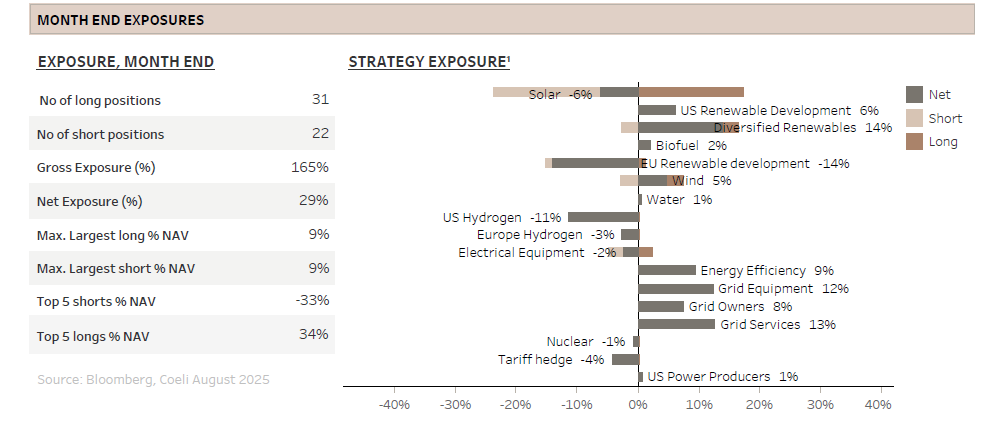

The weakest performer in August was the ‘US Hydrogen’ theme, which detracted 0.6% from NAV. This pure short theme is composed only of small-cap names that have recently benefited from expectations of another Fed cutting cycle and retail investors’ enthusiasm for “meme-like” stocks. While we share the bond market’s optimism for rate cuts in September, we do not believe this materially improves the commercial prospects of hydrogen business models. As fund AUM has grown, we have increased hydrogen short positions to maintain consistent net exposure. By month-end, overall net and gross exposures stood at 29% and 165%, respectively.

MARKET COMMENT – ALL EYES ON THE FED

The S&P 500 rose 1.9% in August, driven by the MAG7 and other large-cap technology stocks, while the equal-weighted S&P 500 declined by 1.5%. The European STOXX 600 once again lagged the S&P, gaining only 0.7% in local currency terms, although it remains ahead by 23% year-to-date in dollar terms. The Russell 2000, representing US small caps, outperformed strongly with a 7% rise, its best month since November last year, bringing its year-to-date return to +6% versus +10% for the S&P 500.

A key driver of small-caps’ outperformance in recent months has been growing expectations of a new Fed rate-cutting cycle beginning in mid-September. This view was cemented by a weak employment report in early August with significant negative revisions, followed by mixed but relatively benign inflation readings, and finally by Fed Chairman Powell at Jackson Hole, where he emphasized increasing risks of labour market weakness and suggested that recent price increases may largely reflect one-off tariff effects.

As most investors know, Fed rate cuts are typically supportive for equities provided economic weakness does not deteriorate into a recession, which few economists currently foresee. Still, several uncertainties justify caution. First, the full impact of tariffs has yet to be seen. Second, equity valuations remain elevated, fuelled by expectations that large AI investments will deliver substantial productivity gains. As we have noted in previous monthly reports, any cracks in these assumptions could lead to meaningful downside for the stock market. Third, President Trump has openly threatened the Fed’s independence and amid increasing talk of financial repression, long-term rates could rise even as the Fed cuts at the short end. While equities might initially benefit as an inflation hedge, rising long-term rates and diminished confidence in US financial and economic policies could weigh heavily on markets over time. Finally, September is historically the weakest month of the year for the stock market, and with the first FED cut already priced in by bond markets, we remain cautiously positioned for now.

POWER WITHOUT WIRES: WHY THE GRID IS THE REAL BOTTLENECK

As we discussed in last month’s report “Trump’s War on Wind and Solar Continues”, President Trump has made no secret of his hostility toward renewable energy. Yet even he has acknowledged that the US cannot win the global AI race against China without vastly more electricity. Training and running advanced AI models consumes staggering amounts of power, however, the real constraint is not wind turbines or solar panels, but rather the ability to connect new power generation to data centres via the grid. Much of America’s transmission system, built decades ago, is already buckling under growing load. Some analysts warn that to keep pace with demand, the grid will need to double or even triple in capacity over the next twenty years.

Europe finds itself in much the same situation, though with one critical difference: most governments remain committed to decarbonisation targets and continue to expand renewable capacity. That makes the grid bottleneck even more visible. This spring provided two sharp reminders of its severity. In late April, Spain and Portugal suffered a rare system-wide blackout caused by what ENTSO-E, the European transmission association, termed a “complex chain of technical and operational factors.” A few months later, Scotland reported record wind curtailments with 4 terawatt-hours lost in the first half of 2025, enough to power every household in Scotland for six months. These are not isolated events but symptoms of a systemic mismatch between the pace of renewable deployment and the far slower expansion of grid infrastructure.

Four Drivers Behind the Grid Super-Cycle

First, demand is rising again. Electrification of heating, transport, and industry, combined with the rapid growth of data centres, is pushing power loads steadily higher.

Second, the grid geography is changing. Where once a handful of large power plants dominated, today the system is increasingly decentralized. Also, the best renewable resources are often located far from demand centres. North Sea wind must reach German factories in the south, French nuclear must flow east, and Iberian solar must travel north. That requires long-distance, high-capacity power highways: HVDC (High Voltage Direct Current) lines capable of transmitting power efficiently over hundreds of kilometres, complemented by 400 kV+ (kilovolt) backbones that function as the highways of national networks.

Third, the grid is ageing. The bulk of the European power networks were built between 1920-1960. Although they were constantly upgraded, they have not kept pace with rising demand or the shift toward intermittent and distributed generation.

Fourth, operational reality bites. In 2024, wholesale European electricity prices cleared at zero or negative for about 4% of all hours, double the share of 2023. This was not because renewables were “worthless”, but because the system could not absorb, transport, or store the surpluses.

Hence, the paradox is that Europe does not lack power, but rather connection. Spain often generates more solar than it can move to cities. Scotland routinely curtails abundant northern wind which forces expensive gas-fired plants in the south to pick up the slack. Sweden sees cheap or negative prices in the north, but due to inadequate transmission, the south pays power prices closer to Continental Europe. In each of the three cases, the problem is not power generation, but the wires to carry it.

Grid operators are responding. Germany’s network development plan foresees 4,800 km of new high-voltage lines and €200bn of investments by 2037, including a series of “electricity autobahns” to move wind power from the north to factories in the south. France’s RTE has mapped out a €100bn plan to replace aging lines and build connections for offshore wind. The UK’s Ofgem has approved an initial spending plan of £10bn, the first steps in what is likely to become an £80bn+ expansion of the electrical grid into the 2030s. In Italy, Terna plans to invest more than €23bn in its “Hypergrid” of submarine and underground cables to double north–south transfer capacity, while Spain is pressing ahead with new interconnectors to France, Portugal and Morocco.

This investment super-cycle has clear beneficiaries in which the fund is involved. Global cable manufacturers like NKT, Prysmian (PRY), and Nexans (NEX) are seeing record order books. Engineering and installation specialists like SPIE and component providers such as Schneider Electric (SU) and Siemens Energy (ENR) play essential roles in providing substations, switchgear, and control systems for these expanding grids. The fund is also invested in some of grid owners, like EON, National Grid (NG/) and Elia (ELI), which will see strong earnings growth from higher regulated return on soaring investments.

So, what exactly needs to be built? The requirements are, we believe, well understood by regulators and companies alike. Europe needs new “power highways”: HVDC links to move huge volumes of electricity efficiently from where it is produced to where it is consumed. It needs more cross-border interconnectors to allow neighbours to share surpluses and back each other up when the wind or sun fall short. At sea, it needs offshore hubs to consolidate wind output into shared platforms that serve multiple markets. At a local level, distribution grids must be modernised so rooftop solar, EVs, and heat pumps can be connected without overloading networks. By modernisation we mean tangible upgrades: thicker cables, new substations, and digitalized control systems that manage flows in real time. Alongside the wires, the system must build “buffers” like batteries, pumped hydro and flexible demand systems that can absorb peaks and provide stability. It is an enormous task.

For both investors and society, the message is clear: returns follow wires. Every euro invested in high-voltage lines or storage unlocks several euros of renewable value that would otherwise be stranded. UK’s Ofgem estimates average network costs will increase by £52 per customer annually but deliver savings of roughly £80 per year by 2031. Whether in America, where the AI race collides with an outdated grid, or in Europe, where decarbonisation is running ahead of infrastructure, the lesson is the same: building power generation without building connection is self-defeating. The next frontier is wiring up the transition by making renewables dispatchable, ensuring power flow smoothly, and securing the backbone of electrified societies.

We continue to view the grid as one of the most powerful and durable investment themes ahead. It sits at the interconnection of three mega-trends, the boom in AI data centres, the electrification of industry and society, and the transition to a less carbonised world. For us, it remains not just a bottleneck, but also a cornerstone opportunity.

FUND PERFORMANCE – SOLID MONTH ON MOST MEASURES

Compared to the previous three months, the fund’s P&L volatility declined in August. More than two-thirds of themes were profitable, and the largest loss-making theme detracted less than 1% from NAV. Long positions delivered a gain of 3.1% while shorts added 0.1%, despite continued momentum in “meme-like” stocks in the US.

The best-performing theme was ‘EU Renewable Development’, contributing 1.6% to NAV, driven by short positions in offshore wind. Our sceptical stance on the sector has been in place for some time, predating the election of President Trump, whose outspoken opposition to wind power has further worsened the industry’s risk-reward profile.

First, as noted above, incremental offshore wind capacity is expensive and unreliable if not accompanied by sufficient grid expansion. Second, while solar costs have continued to decline, offshore wind costs have risen, making it less competitive, particularly once grid costs are included. The fact that all three major Western wind turbine OEMs are loss-making in their offshore wind operations, with two of them, we would argue, reluctant participants, underscores the industry’s structural challenges.

Third, utilities and oil majors that once touted large offshore wind ambitions have scaled back, cutting capex forecasts and deferring or cancelling projects. While the silver lining is that future projects’ IRRs may improve, the higher cost of capital offsets much of this benefit. Finally, Trump’s refusal to greenlight new offshore wind projects, and the risk that even nearly finished projects may be blocked, raises risks further. As we highlighted in our April 2025 report “Tilting at Windmills”, developers risk absorbing most of the remaining capex if projects are halted. Lawsuits will follow, but these could take years and although the developers have a good case for compensation, the US government can offset this by having avoided paying out billions of dollars in investment tax credits (worth 30–40% of total investment costs).

The second-best performing theme, ‘Diversified Energy’, added 1.3% to NAV despite a notable 11% decline in Siemens Energy (ENR), the largest position in the theme. This loss was more than offset by strong gains in relatively smaller positions, including bitcoin miners and Bloom Energy (BE), a fuel-cell company. As discussed in our November 2024 report “The Urgency to Secure Power”, both benefit from being able to deliver relatively clean and immediate power to utilities and hyperscalers. In hindsight, we took profit too early in the bitcoin miners and sized Bloom too conservatively at the outset. However, the stock has nearly tripled since our purchase less than six months ago. We continue to actively seek out similar opportunities.

The only theme that detracted more than 0.5% in August was ‘US Hydrogen’, now down four consecutive months but still with a solid positive return for the year. Hydrogen stocks have recently benefited from expectations of Fed rate cuts, which tend to fuel speculative small-cap and unprofitable tech rallies. While we acknowledge this risk, the financing environment does not change the core problem: green hydrogen remains too expensive globally and in the US.

As we argued in our June 2025 report, hydrogen was a relative winner from the One Big Beautiful Bill Act (OBBBA). However, although the law extended eligibility for tax credits from 2025 to 2027, this remains far less favourable than the Inflation Reduction Act’s original 2032 extension. The two extra years of runway is unlikely to change the economic case, especially as blue hydrogen, produced from natural gas with carbon capture, has become comparatively more attractive. Moreover, changes in tax credits for fuel cells now allow natural gas-fed fuel cells to qualify, a shift designed to benefit fossil fuel producers. This does little to improve the competitiveness of hydrogen fuel cells in mobility, and we remain firmly negative on the segment.

Looking ahead, we remain cautiously positioned with net exposure in the low 30s. While additional Fed cuts could provide short-term support for equity markets, we believe the first cut is largely priced in and the timing of subsequent cuts is uncertain. Valuations remain elevated, underpinned largely by strong investor conviction in the AI investment cycle. Should cracks emerge in this theme, the downside could be significant. For now, we prefer to stay patient, carefully monitor developments, and maintain dry powder, hoping to selectively increase exposure into year-end as market conditions evolve.

Thank you for your continued trust, and we look forward to updating you again next month.

Sincerely

Vidar Kalvoy & Joel Etzler

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

- Portfolio Manager and Founder of the Coeli Energy Opportunities Fund.

- Over 15 years of investment experience spanning both public markets and private equity.

- Managed the Coeli Energy Transition Fund from 2019 to 2023.

- Spent six years at Horizon Asset in London, a market-neutral hedge fund.

- Started working with Vidar Kalvoy in 2012.

- Five years in Private Equity at Morgan Stanley.

- Began his investment career in the technology sector at Swedbank Robur in Stockholm in 2006.

- Holds an MSc in Engineering from the Royal Institute of Technology (KTH), Stockholm.

- Portfolio Manager and Founder of the Coeli Energy Opportunities Fund.

- Has managed energy equities since 2006 and brings more than 20 years of experience in portfolio management and equity research.

- Managed the Coeli Energy Transition Fund from 2019 to 2023.

- Head of Energy Investments at Horizon Asset in London for nine years, a market-neutral hedge fund.

- Experience from energy investments at MKM Longboat in London and equity research in the technology sector in Frankfurt and Oslo.

- Holds an MBA from IESE in Barcelona and a Master’s in Business and Economics from the Norwegian School of Economics (NHH).

- Before entering finance, he served as a lieutenant in the Royal Norwegian Navy.

IMPORTANT INFORMATION. This is a marketing communication.

Before making any final investment decisions, please refer to the prospectus of Coeli SICAV II, its Annual Report, and the KID of the relevant Sub-Fund. Relevant information documents are available in English at coeli.com. A summary of investor rights will be available at https://coeli.com/financial-and-legal-information/.

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

Please note that the management company of the fund may decide to terminate the arrangements made for the marketing of the fund in one or multiple jurisdictions in which there exists arrangements for marketing.