This material is marketing communication.

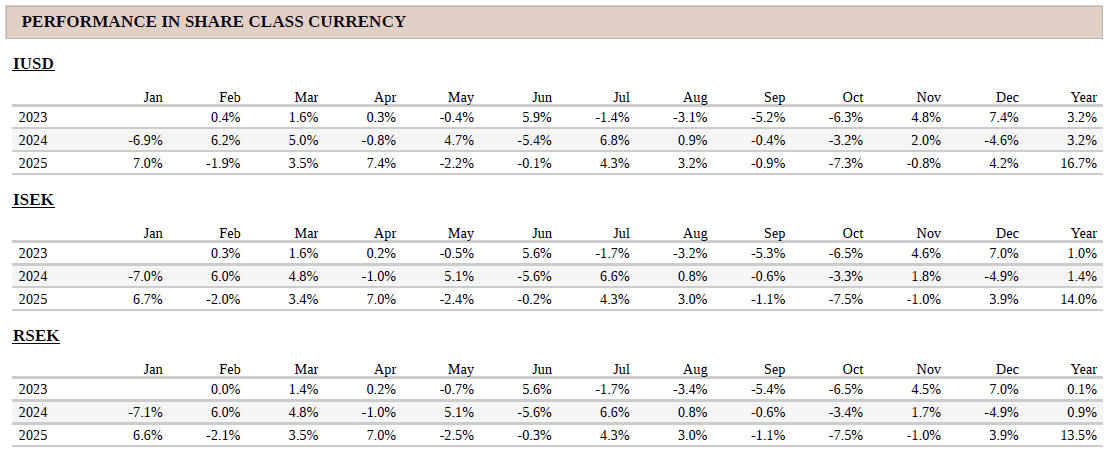

Note that the information below describes the share class (I USD), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class return. The information below regarding returns therefore differs from the returns in other share classes.

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

1) Share Class I USD

Performance for other share classes towards the end of the report.

FUND MANAGER COMMENTARY

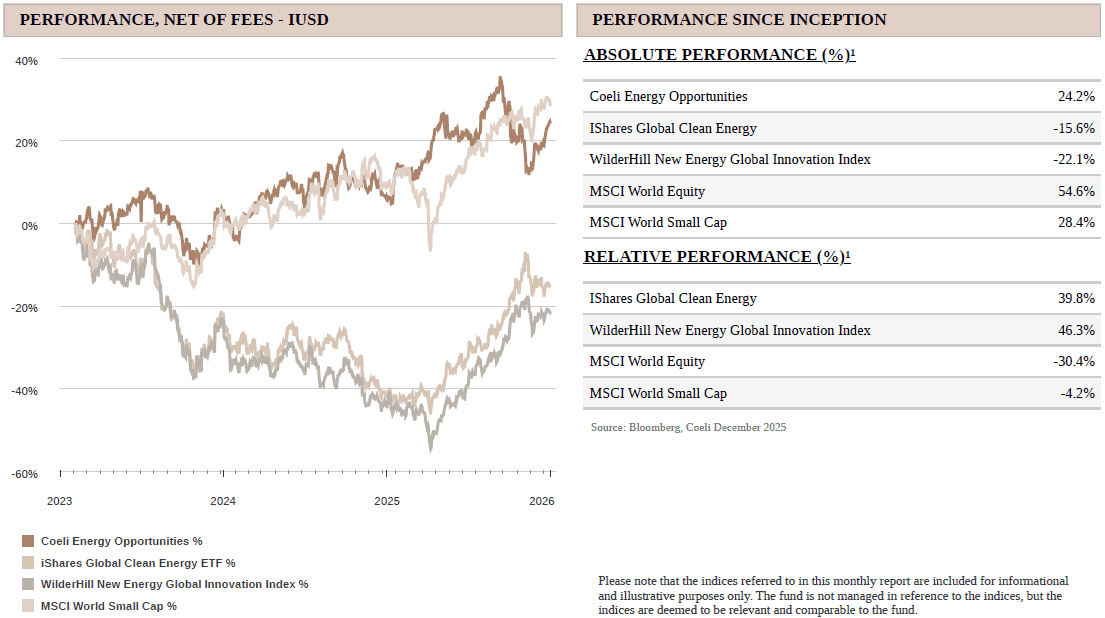

The Coeli Energy Opportunities fund rose 4.2% net of fees and expenses in December (I USD share class). It gained 16.7% during the year and has returned 24.2% since inception in February 2023.

In December, the fund outperformed its most comparable indices, the Wilderhill New Energy Global index (NEX) and the iShares Global Clean Energy (ICLN) by 3.6% and 6.7%, respectively. For the full year, the fund underperformed the NEX by 24% and ICLN by 30%, while since inception it remains ahead by 46% and 39%, respectively.

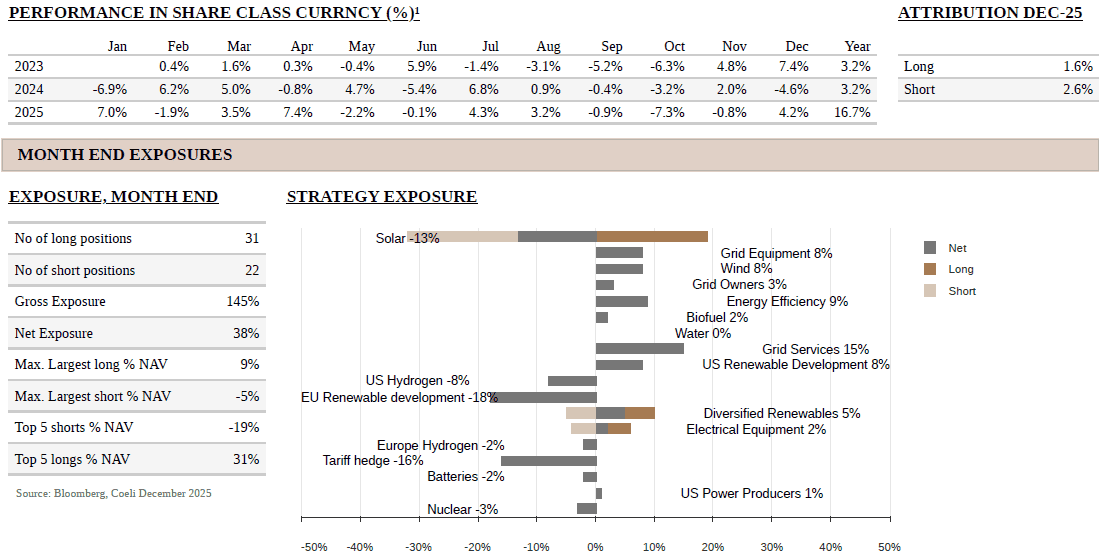

December was a solid month, with long positions contributing +1.6% and shorts adding +2.6% to performance. Although 8 of 18 themes posted losses, drawdowns were modest, all below 0.4% of NAV. The best performer was ‘Hydrogen’, where the two pure short themes contributed a combined 1.1%. Hydrogen stocks continued their deflation following the September–October meme rally, which caused the fund significant losses earlier in the year. Similarly, solar shorts, which had doubled and tripled during the meme phase, declined 15–25% in December, driving the ‘Solar’ theme to a +0.8% gain despite modest headwinds in long positions like First Solar (FSLR) and Sunrun (RUN).

The ‘Nuclear’ theme contributed +0.8% to NAV as elevated valuations of companies with negligible near and medium-term revenue prospects continued to normalize. AI and Grid-related themes combined for +1.0% in a relatively quiet month, with no standout winners or losers. At month-end, net and gross exposures stood at 40% and 143%, respectively. Absent inflows towards the end of the month, net exposure would have been approximately 45%.

MARKET COMMENT – THIRD CONSECUTIVE YEAR OF DOUBLE-DIGIT RETURNS

Despite setting its 39th all-time high for the year on Christmas Eve, the S&P 500 declined by 0.05% in December after a small sell-off into year end, ending a seven-month winning streak. The index still delivered a strong 16.3% return in 2025, marking its third consecutive year with double digit gains. The Nasdaq fell 0.5% in December but gained 20.2% for the year. Russel 2000, the small cap index, declined by 0.7% in December but gained 11.3% for the year, ending 1.6% above its 2021 peak. Since that peak, the S&P 500 has increased almost 50% while S&P 500 equal weight is 18% higher, indicating Mag 7 has outperformed the rest, and particularly small caps.

While US equity markets performed well in 2025, they were outpaced by most global equity markets when measured in USD terms. The Eurostoxx 600 rose 16.7% in local currencies but gained 32.3% in USD, nearly double the S&P 500's return. In fact, global equities just marked a three-year USD total return CAGR of 20.7%, the best return for global equities since the tech bubble in 1999. In many respects, the big story of the year was weakening USD or in fact all fiat currencies when measured against gold, which rose 65% against the USD in 2025.

REVIEW OF 2025 PERFORMANCE

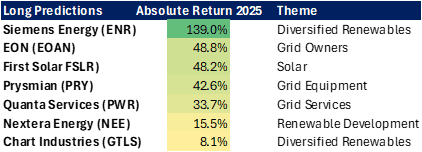

The fund delivered solid absolute returns of 17% in 2025 after fees and expenses, in what became another year of wide dispersion across the energy transition universe. Compared to 2024, absolute returns were higher, but relative returns, which were about 30% in 2024, were negative by nearly the same magnitude this year. Most of the themes we highlighted a year ago played out largely as expected, but a few did not and weighed on performance. Before discussing how the portfolio is positioned going into 2026, this section reviews what worked well and what did not in 2025. The table below shows 2025 absolute returns for all positions mentioned in last year’s outlook.

Positive contributors

Diversified Renewables

‘Diversified Renewables’ was the strongest theme for the year, with several of the largest contributors to absolute performance. In last year’s outlook, we highlighted Siemens Energy (ENR) as a top pick despite a 320% return in 2024 and a rich 70x 2025 P/E multiple. However, as we expected, consensus estimates were too low and during the year, 2025 earnings estimates were revised up by more than 100%, while 2026 and 2027 EPS estimates were increased by 68% and 74%, respectively. The share price appreciated 139% over the year, supported by well-deserved multiple expansion as 2028-2030 estimates were raised even further.

The second-largest contributor to the theme’s P&L was Bloom Energy (BE), the global leader in fuel cell manufacturing. The stock gained 291% during the year and was up 365% from the fund’s first purchase in May. The company secured several large orders in 2025, prompting the sell-side to revise 2028 EPS estimates up by 172%.

Chart Industries (GTLS), highlighted several times last year as one of the preferred energy transition names, was acquired at a 22% premium to Chart’s prior closing price. We had mixed feelings about the takeover as we had expected a stronger valuation.

‘Diversified Renewables’ also included trading in several bitcoin mining companies which all performed exceptionally well. Importantly, as we have pointed out many times, the key motivation for our positions were not bitcoin itself but the transition of these companies into high performance computing data centres.

Another strong contributor within the theme was Micron Technology (MU). MU is one of three major memory chip manufacturers supplying the DRAM and high-bandwidth memory (HBM) chips that are critical for data centres. Although memory manufacturers are not a typical focus area for the fund, the investment drew on insights from broader research into AI infrastructure and data centre demand. While we were not early to invest in MU, there still appeared to be substantial upside as the memory market is severely undersupplied, and we managed to enter the position early September, just before DRAM prices started going vertical. MU appreciated more than 90% from the fund’s first entry through the end of the year.

Grid

In the 2025 Outlook, we presented grid infrastructure as the most compelling structural theme entering the year. This proved correct, and the four grid themes were together were the largest positive contributors to performance in 2025.

In ‘Grid Equipment’, the strongest contributor was Prysmian (PRY), supported by continued strength in US low- and medium-voltage cables as well as strong growth and margins in the transmission division, Q3 transmission margins were already close to their FY 2028 target level. The stock appreciated 43% in 2025 driven by some upward revisions to 2026-2027 consensus earnings, alongside multiple expansion during the year.

‘Grid Services’ also performed well. As outlined in last year’s outlook, Quanta Services (PWR) is the closest thing to a compounder in this segment, delivering another year of consistent operational performance and meeting or exceeding earnings expectations. The stock rose 34% during the year, however we traded in and out of it actively during the year. In May, we made Mastec (MTZ) the largest grid-services position, as the stock was significantly cheaper and we believed there was, and still is more room for positive surprises especially from its leading natural gas pipeline business. This proved the correct decision as MTZ outperformed PWR by nearly 20% from that point and gained 60% for the full year.

Hedges in ‘Electrical Equipment’ worked as intended. Two out of three shorts declined during the year and contributed positively, which we view as a good outcome given the broad strength across grid and power stocks.

The ‘Grid Owners’ theme also contributed strongly. EON (EOAN), the largest position, recovered from the weakness seen at the end of 2024 and appreciated 49%. Concerns around German political outcomes proved overstated, and regulatory developments supported the view that allowed returns would remain stable or improve. Elia (ELI), a smaller position, delivered even stronger performance, ending the year up 59%.

Solar

The key long position during the year, and the largest absolute contributor in the theme, was First Solar (FSLR). Last year it was described as the only conviction long in the space pending possible dismantling of the Inflation Reduction Act. The stock appreciated 48% during the year and 58% following the signing of the One Big Beautiful Bill Act (OBBBA), when it was made the fund’s largest position and kept close to the maximum size for the remainder of the year. Following OBBBA, the fund also scaled up NextPower (NXT), the leading solar tracking company as we perceived it to be another winner from the legislative outcome.

Despite these gains, the ‘Solar’ theme was one of the two themes that detracted significantly form performance in 2025, entirely due to shorts that appreciated significantly more than the longs. This is discussed further below.

Wind

The ‘Wind’ theme also performed strongly, led by Nordex (NDX1) the single largest positive contributor for the fund. As expected, the company’s margin improved steadily quarter by quarter as the company completed problematic projects won during Covid. Order intake grew nicely during the year, and earnings estimates for the coming years increased by 40-50%. Given that the stock screened inexpensively at the beginning of the year, the market rewarded it with a 138% price appreciation. For comparison, Vestas (VWS), its closest peer which we exited in late 2024, rose 78%, roughly half of which came in the last two months.

Negative contributors

The losses for the year came primarily from two themes, ‘US Hydrogen’ and ‘Solar’, which were either pure shorts or skewed short for most of 2025. Considering that renewable indices finally recovered, rising 40-50% after four consecutive down years, this outcome is not entirely surprising. Still, there are a couple of aspects with which there is clear dissatisfaction.

We had long argued that the finalization of the OBBBA would be a risk clearing event. However, once the law was finally signed, we placed too much emphasis on uncertain fundamentals as the Trump administration introduced new roadblocks for solar and wind developments, a topic covered in the July-25 monthly: “Trump’s war on wind and solar continues”. Although we deemed the legislative outcome favourably and added to quality names like NXT, FSLR and MTZ, we failed to fully recognize that “a rising tide would lift all boats”, that is, weaker names and heavily shorted stocks would also rally, regardless of fundamentals or future policy risks.

From the passing of OBBBA, the two most comparable renewable indices, the Wilderhill New Energy Global Index (NEX) and the iShares Global Clean Energy ETF (ICLN), rose 34–35% (versus full-year increases of 40% and 47%, respectively). Over the same period, earnings estimates for 2025–2027 declined relative to both the start of 2025 and post‑OBBBA levels, indicating that index performance was entirely driven by multiple expansion.

To make matters worse, when the FED restarted its cutting cycle in September, it fuelled a meme rally across many of the shorts, accelerating their ascent on little or no fundamental news. As detailed in the September and October report, this forced the fund to crystallise some losses, turning what had been shaping up to be a great year into merely a good one.

OUTLOOK FOR 2026

When we wrote last year's outlook for 2025, we highlighted elevated uncertainty stemming from Trump's unpredictability. The market was optimistic about tax cuts and deregulation but concerned that trade wars and mass deportations could trigger inflation and slower growth.

Today, with those risk factors largely in the rearview mirror, sentiment has shifted markedly. A broad consensus has emerged that equity markets will advance in 2026. The macro backdrop appears supportive: fiscal stimulus via tax cuts and higher deficit spending, combined with monetary accommodation from at least two additional rate cuts and the ending of quantitative tightening. Importantly, markets expect another year of strong, broad-based earnings growth, a departure from the 2024–2025 period, when gains were heavily concentrated in a handful of mega-cap technology stocks. The outlook appears bright.

Yet, the strong consensus is a bit worrying, particularly given that US equities are trading at valuations rarely seen outside of bubble environments. However, as we have noted repeatedly, equity markets do not crash as long as earnings remain robust and central banks cut rates. Even a meaningful correction, distinct from a crash, would require a material trigger.

What could trigger a market correction?

Reflation represents one such trigger. If economic momentum accelerates beyond expectations, the Fed could shift from rate cuts to hikes. Few market participants currently price this scenario, but surging commodity prices and accelerating AI capex pose inflation risks if labour markets are not as soft as expected.

Geopolitical risk is another concern. President Trump campaigned on reducing America's global policing role, yet the US has already conducted strikes in 7 countries during his first year in office. So far so good, you could argue, but an overconfident administration could miscalculate and trigger a geopolitical shock with economic consequences.

However, we believe the most probable trigger is a bursting of the AI stock market bubble. As detailed extensively in our September 2025 report, "Are We in an AI Bubble?", we identified strong bubble indicators while noting that a meaningful decline may not materialize until market focus shifts from accelerating AI capex to realized returns on those investments. Last month, we noted early signs of this transition with credit markets tightening for AI infrastructure companies lacking near-term cash generation. Yet we acknowledge that markets may allow several additional quarters before demanding proof of returns on AI investments. Any correction could thus unfold gradually rather than abruptly.

Still, we would not be surprised if the "easy money" in AI power and infrastructure equities has already been made. Going forward, we anticipate increased dispersion among companies providing power and infrastructure to AI data centers. While we see solid fundamental upside in our core long positions, we are concerned about rich near-term valuation multiples that will contract in any potential “burst”. To hedge this risk, we are increasing shorts in AI power and infrastructure companies facing capacity constraints or excessive competition, as well as those with optimistic business plans dependent on ample credit availability to sustain growth.

Grid

We remain bullish on grid investments in the western world. This segment sits at the heart of the energy transition and is the key enabler for new sources of power demand, like AI data centres. Yet, as described above, many stocks screen expensive on near-term multiples. Still, given the structural growth cycle and strong competitive positions of selected companies, rich valuations are largely justified for those with pricing power and high margins for years to come.

In line with our investment process and its strong focus on supply–demand dynamics, we closely monitor the supply response; sooner or later, supply overwhelms demand even in the most attractive sub-sectors. On the demand side, expectations have been lifted by the advent of AI data centres. However, as highlighted in previous monthly reports (March 2024 – “Roadblocks on the AI Highway” and November 2025 – “The Urgency to Secure Power”), there is significant uncertainty around potential improvements in chip and infrastructure efficiency. Any downward adjustment to power and data centre demand expectations is likely to impact trading multiples and share prices, as seen briefly during the “DeepSeek scare” in January 2025. It will not matter that near-term fundamentals are unchanged or that, for many grid companies, AI is only the “icing on the cake” for growth.

Against this backdrop, we continue to add short positions in sub-sectors where we see supply and demand moving from clearly undersupplied to more balanced. Many companies are operating at peak production capacity with historically high gross margins and are starting to face greater price competition. When earnings growth stalls, premium valuation multiples tend to normalize quickly.

Grid Services

We remain optimistic about the fundamentals of our ‘Grid Services’ companies. The largest position, as mentioned above, is Mastec (MTZ), an Engineering, Construction and Procurement (EPC) company focused on grid, renewable energy and gas infrastructure. We are positive to all its end markets but what distinguishes MTZ from its peers is its relatively stronger position in natural gas, where we expect growth to exceed current consensus expectations. MTZ executed 2025 well, raising full year earnings guidance three times.

We also continue to own Quanta Services (PWR), but given its richer valuation, the position is sized smaller than MTZ. In Europe, the fund owns SPIE which is broadly the French equivalent of PWR and MTZ. SPIE appears cheaper than both MTZ and PWR on near-term multiples, but adjusting for earnings growth, MTZ remains the most attractively valued of the three.

Grid Equipment

We still own all three European cable manufacturers: Prysmian (PRY), NKT and Nexans (NEX). As in 2025, we favour PRY, driven by its scale, diversified product portfolio and strong positioning in US low- and medium-voltage cables. NKT, which was our largest position of the three in 2023 and into 2024, remains a significant holding and may be scaled up again as its expansion projects are completed and the new capacity starts to generate returns.

Grid Owners

We continue to view the theme a long-term compounder. Yet, after the strong performance last year, the near-term upside is more limited as a greater share of future growth is now priced in. The largest position is EON whose share price has compounded by roughly 24% over the last three years, including a 49% increase in 2025. It trades at a premium to its Regulated Asset Base (RAB), but so do its peers. We are comfortable with this premium because the RAB is expected to grow rapidly over the coming years, compensating for previous years of under investments. On earnings multiples, EON still trades at a discount to other regulated utilities. Elia is another name we are optimistic about. Its RAB growth and capex needs are even higher, but so is expected earnings growth.

Electrical Components

We will continue to use electrical components stocks as hedges for the grid themes. Many sub-sectors within this bucket are seeing increasing supply and competition. In many cases, capacity now matches demand, but in others rising competition is starting to erode margins. We continue to identify and add short positions that can be scaled up quickly if needed, in order to hedge the risk of an abrupt contraction in the valuation multiples across grid-related stocks.

Diversified Renewables

This theme comprises companies with broader exposure across the energy value chain, such as Siemens Energy (ENR), a major player in grid equipment, gas turbines and wind turbines. We remain optimistic to ENR for 2026. Despite the stock’s nearly 900% appreciation over the last two years, the valuation is not demanding relative to expected earnings growth and when compared with its closest peer, GE Vernova (GEV). Nevertheless, we remain vigilant about monitoring supply in the power markets, as strong share price performance alone becomes a risk if expectations soften.

We also continue to own Bloom Energy (BE) for its fuel cell solutions for powering data centres. While the valuation is rich, with demanding expectations for order growth, we strongly believe it will secure several additional contracts in the coming months and may announce further manufacturing expansion. This should provide multiple potential catalysts and help sustain or increase the market capitalization. Another reason for owning Bloom is that it functions as a hedge against our shorts in non‑profitable names. Short interest in BE is quite high, and it is a retail favourite often promoted on crypto-related platforms, even though it has of course nothing to do with crypto.

We also retain smaller positions in some bitcoin miners, although position sizes have been reduced significantly after several names generated returns of more than 200% since first being highlighted in the November 2024 monthly report. These positions correlate well with heavily shorted, non-profitable companies in risk-on rallies and, like Bloom, play a dual role in the portfolio.

While we do not discuss shorts in detail, we see an increasing number of attractive short opportunities in this ongoing AI gold rush. The AI investment boom has driven some valuations to extreme levels. In many of these names, we see highly asymmetric risk-reward, as expectations of ever-growing AI capex and flawless execution are priced in despite multiple potential bottlenecks that could slow data centre build out.

Solar

We are selectively optimistic on the solar space for 2026. Underlying power demand is growing, driving higher power prices and increasing urgency to add new supply. In regions with good solar resource and well-developed grids, solar remains by far the cheapest and fastest option for incremental power. Still, the Trump administration is not supportive and, as discussed in our July 2025 monthly “Trump’s War on Wind and Solar Continues”, can continue to create meaningful speed bumps and potential roadblocks.

For US utility-scale solar, market expectations are unusually wide, with forecasts ranging from a 20% decline to 10–15% growth. Our base case is that installations in 2026 are flat to slightly up versus 2025. Even in a scenario where stringent Foreign Entity of Concern (FEOC) rules are implemented, or punitive Section 232 polysilicon tariffs are introduced, we expect the main impact to fall on installations from 2027 onwards. The biggest near-term risk to our base case is the administration slow‑walking permits for projects with links to federal land.

In this context, we continue to favour First Solar (FSLR) and Nextracker (NXT). FSLR is the largest beneficiary of the Biden‑era tax credits that were preserved in OBBBA. Its US manufacturing footprint offers panels with no Chinese inputs, including polysilicon, eliminating the risk that developers using FSLR modules will fail to qualify for domestic‑content tax credits. FSLR is effectively sold out for domestically produced panels through 2027 and into 2028, and we expect the remainder of the decade to be contracted once there is clarity on polysilicon tariffs and FEOC rules. The average selling price is expected to rise by at least 10-20%, and potentially by 30–40%. Longer term, the market is likely to assign some value to an extension of manufacturing tax credits. Given that US panel prices are currently 3–4x global levels, an abrupt end to tax credits would effectively shut down the US solar industry. Since most utility‑scale solar plants are located in Republican‑leaning states, we would not be surprised to see sufficient political support for an extension.

Nextpower (NXT) is the global leader in solar trackers, which enable panels to follow the sun. Around 70% of its sales are generated in the US, and it holds a dominant market share both domestically and in most markets outside China. NXT is arguably the highest‑quality listed solar company. Since its 2023 IPO, management has raised guidance roughly every second quarter, and full‑year results in FY 2024 and FY 2025 exceeded initial guidance by 132% and 40%, respectively. The company is expanding into steel frames, EBOS, inverters and software, aiming to become more of a one‑stop supplier for large EPCs and developers. We believe this strategy is likely to broadly succeed and expect the 2030 targets presented at its capital markets day late last year to prove conservative and to be revised higher multiple times before 2030.

The US residential solar market is likely to decline meaningfully in 2026 as tax credits for cash and loan purchases of residential systems expired at the end of 2025. However, tax credits for leased residential systems remain in place, and we expect this segment to grow as rising power prices across much of the US make rooftop solar more attractive. Residential solar leasing is capital‑intensive, so rate cuts are also a major tailwind. Following the bankruptcies of SunPower (SPWR) and Sunnova (NOVA), the competitive set‑up is favourable for Sunrun (RUN), the market leader in leasing. Emerging competitors will likely grow, but it will take time for them to reach scale.

We remain skeptical of Chinese panel manufacturers. Global production capacity is roughly twice current demand, making competition intense and any sustained price increases unlikely. In recent years, many of these companies have generated most of their profits in the US market, which will become increasingly difficult as FEOC rules and tariffs are rolled out and tightened in the coming years.

Summary

In summary, while we remain constructive on the fundamental outlook for our key end markets, we enter 2026 with a more balanced view than a year ago. The structural growth in power demand, reinforced by AI and continued electrification, supports a favourable backdrop for many of our core holdings, yet we are mindful that rich near-term valuations will be vulnerable if expectations adjust. We therefore maintain a combination of high conviction long positions with strong visibility, complemented by an increasing number of shorts where we see stretched assumptions, rising competition or emerging supply responses. Although uncertainty around policy, inflation and data centre buildout remains, we believe the portfolio is well positioned for a range of outcomes. As always, our focus will be on identifying mispriced fundamentals, adjusting risk when the facts change and maintaining discipline should volatility rise during the year.

Thank you for your continued trust and confidence. We look forward to updating you on our progress throughout 2026.

Sincerely

Vidar Kalvoy & Joel Etzler

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

- Portfolio Manager and Founder of the Coeli Energy Opportunities Fund.

- Over 15 years of investment experience spanning both public markets and private equity.

- Managed the Coeli Energy Transition Fund from 2019 to 2023.

- Spent six years at Horizon Asset in London, a market-neutral hedge fund.

- Started working with Vidar Kalvoy in 2012.

- Five years in Private Equity at Morgan Stanley.

- Began his investment career in the technology sector at Swedbank Robur in Stockholm in 2006.

- Holds an MSc in Engineering from the Royal Institute of Technology (KTH), Stockholm.

- Portfolio Manager and Founder of the Coeli Energy Opportunities Fund.

- Has managed energy equities since 2006 and brings more than 20 years of experience in portfolio management and equity research.

- Managed the Coeli Energy Transition Fund from 2019 to 2023.

- Head of Energy Investments at Horizon Asset in London for nine years, a market-neutral hedge fund.

- Experience from energy investments at MKM Longboat in London and equity research in the technology sector in Frankfurt and Oslo.

- Holds an MBA from IESE in Barcelona and a Master’s in Business and Economics from the Norwegian School of Economics (NHH).

- Before entering finance, he served as a lieutenant in the Royal Norwegian Navy.

IMPORTANT INFORMATION. This is a marketing communication.

Before making any final investment decisions, please refer to the prospectus of Coeli SICAV II, its Annual Report, and the KID of the relevant Sub-Fund. Relevant information documents are available in English at coeli.com. A summary of investor rights will be available at https://coeli.com/financial-and-legal-information/.

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

Please note that the management company of the fund may decide to terminate the arrangements made for the marketing of the fund in one or multiple jurisdictions in which there exists arrangements for marketing.