This material is marketing communication.

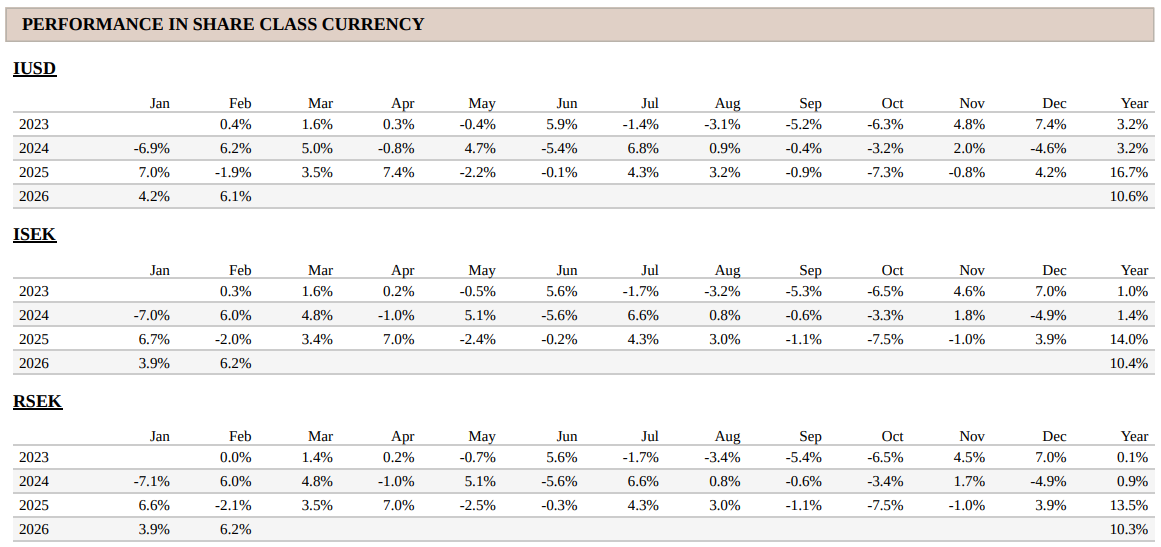

Note that the information below describes the share class (I USD), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class return. The information below regarding returns therefore differs from the returns in other share classes.

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

1) Share Class I USD

Performance for other share classes towards the end of the report.

FUND MANAGER COMMENTARY

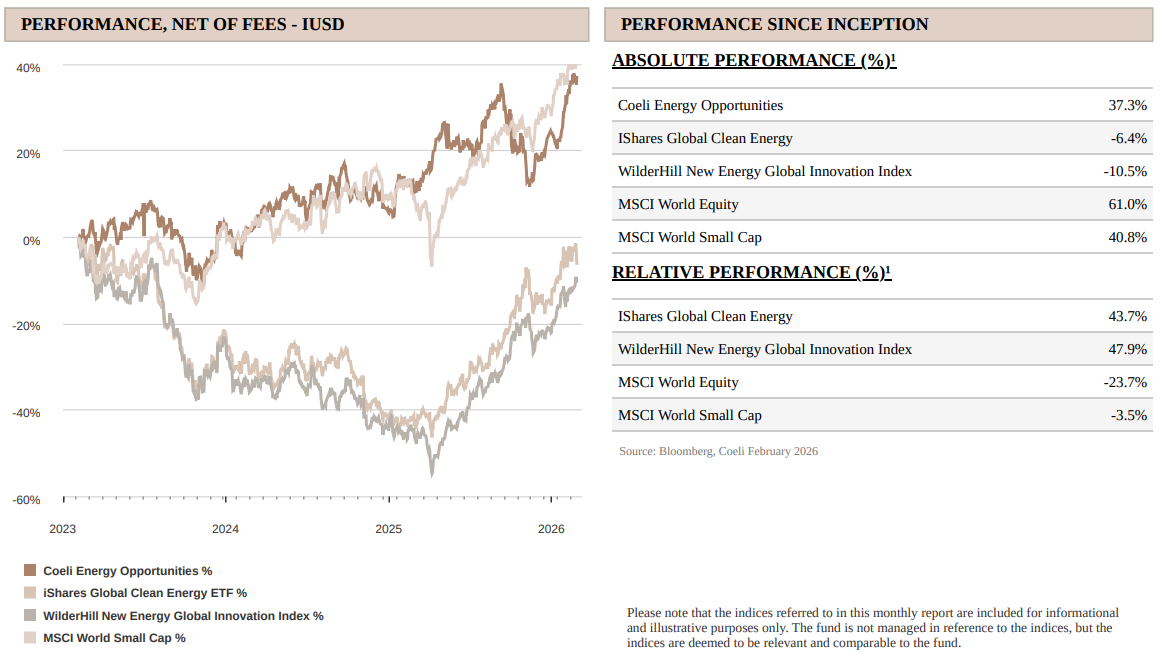

The Coeli Energy Opportunities fund gained 6.1% net of fees and expenses in February (I USD share class). Year-to-date, the fund is up 10.6% and it has gained 37.3% since inception in February 2023.

In February, the fund outperformed its most comparable indices, the Wilderhill New Energy Global index (NEX) and the iShares Global Clean Energy (ICLN) by 1.6% and 5.7%, respectively. Year to date, the fund has underperformed NEX by 4.2% and ICLN by 0.8%, while since inception it remains ahead by 48% and 43%, respectively.

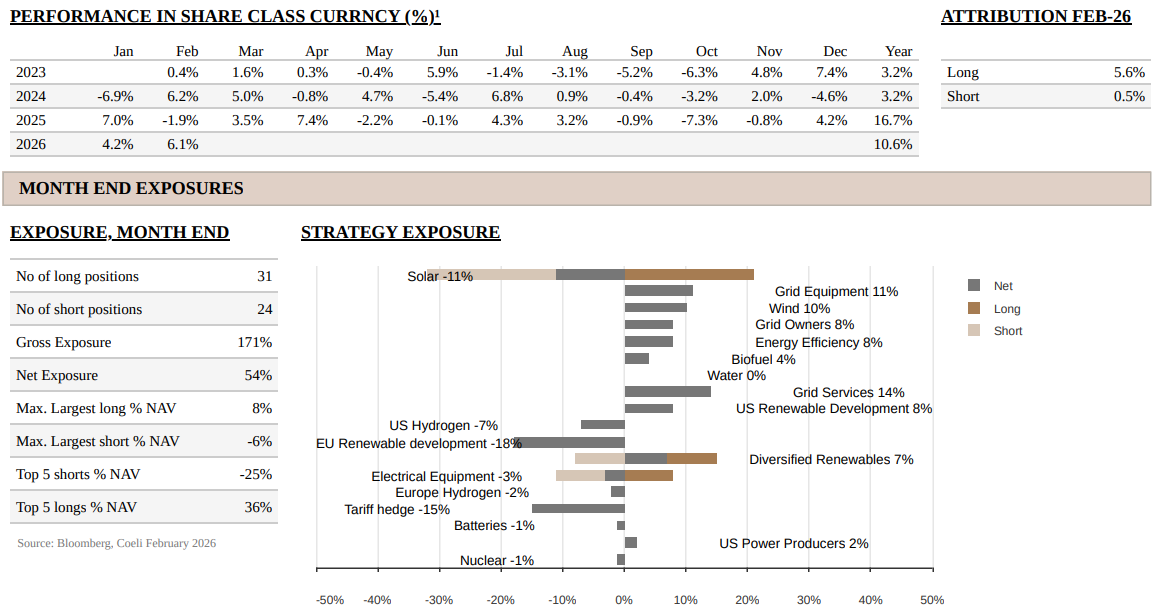

In a volatile month with significant dispersion between stocks and sub-sectors, the fund gained 5.6% on long positions, while shorts added 0.5%. More than two thirds of the themes delivered positive returns, led by ‘powering AI’ related themes, where two of our largest positions, Siemens Energy (ENR) and Mastec (MTZ), both rose on strong earnings. The ‘Wind’ theme also performed well, adding 1.7% to NAV, as Nordex (NDX1) rose 28% in February following solid results and raised guidance.

While earnings season was mostly supportive for the fund, the ‘Solar’ theme suffered from two large drawdowns in First Solar (FSLR) and Sunrun (RUN), making ‘Solar’ the only major losing theme, detracting 2.2% from NAV. FSLR and RUN operate in different sub-sectors, but both were hit by weaker-than-expected volume guidance. We discuss this in more detail in the fund performance section. At month‑end, overall net and gross exposures stood at 54% and 171%, respectively.

MARKET COMMENT – AI DISRUPTION CAUSES HISTORICAL HIGH DISPERSION

S&P 500 fell 0.9% in February as the rotation out of “Mag 7” and large-cap technology continued for the third consecutive month. While Nasdaq declined 3%, weighed down by AI-disrupted software stocks, the S&P Equal Weight Index (SPW) rose 3.4% and the Russel 2000 (RTY) gained 0.7%. Europe’s Stoxx 600 increased 3.9%, its eight consecutive monthly gain, as investors continued to rotate out of US assets, the dollar and mega-cap technology. The standout region, however, was Asia, led by the Korean Kospi index which rose as much as 25%.

Although hyperscalers’ higher capex guidance at the end of January preserved the underlying AI trade, the market intensified its search for clear AI winners and losers. Which companies and sectors have tangible, defensible moats, and which are vulnerable as AI automation disrupts their core businesses? Because this is difficult to assess, the market has effectively “shot first and asked questions later,” questioning the terminal value of many companies and driving significant multiple compression.

This intense focus on winners versus losers has produced record dispersion beneath relatively benign index volatility. The S&P 500 has traded in a range of just 2.7% in 2026, while the average constituent has moved within a band roughly seven times larger. This ratio is the highest since at least 1994 and represents an ideal backdrop for long–short hedge fund strategies.

Unfortunately, this attractive market backdrop changed abruptly on the final day of the month, as the US and Israel initiated military action against Iran.

IRAN WAR - IMPACT ON RENEWABLE ENERGY

While the attack on Iran was well telegraphed, we initially viewed it as another market wobble worth looking through rather than the start of a more durable risk-off move. In our almost 30 years in the capital markets, we have learned the hard way that geopolitical risk events should be bought. The facts also pointed to a short war: both sides have limited missile stockpiles, implying a natural cap on escalation; regime change did not appear to be an explicit US objective but more of a potential “bonus”; and most experts agree regime change is unlikely through air power alone. Once the narrow goals of degrading Iran’s nuclear and ballistic capabilities are achieved, a ceasefire is the most logical outcome, especially as any prolonged disruption of the Strait of Hormuz would push energy prices sharply higher, reviving inflation and slowing economic growth. With US mid‑terms only eight months away, it is hard to see why President Trump would want this war to drag on for more than a few weeks. If Republicans lose both the House and the Senate, impeachment is likely, effectively turning Trump into a lame duck for the rest of his term.

Our initial view was clearly not unique. The S&P 500 fell only 2% in the first week after the attack. Oil and gas spot prices moved sharply higher, but the forward curves shifted mainly in the front end, signalling that markets expect energy flows through Hormuz to normalise relatively soon.

This makes us uncomfortable. While we still believe self‑preservation is the dominant incentive for the US president and that he may soon declare “a great victory,” the disruption risk to the Strait of Hormuz, and the attacks on neighbouring Gulf countries’ energy infrastructure has been more severe than we initially expected. In other words, what first looked like another contained geopolitical scare has evolved into something with a more meaningful tail risk. There is no guarantee that fighting will end quickly or that flows through Hormuz will normalize without disruption. Iran knows it cannot win the war militarily, but its effective control over the strait has re‑confirmed its leverage and the economic pain it can inflict. Crucially, Iran has learned it does not need to mine the strait or attack every vessel; the threat alone may be enough to deter or at least reduce traffic in the future. Even if Hormuz volumes recover to average 70% of normal for a sustained period, nearly 2% of global oil supply would be interrupted, after accounting for diverting flows through pipelines. This seemingly small impact would keep upward pressure on oil prices and importantly make the global oil markets much more sensitive to any disruptions.

Uncertainty could therefore linger. A higher risk premium in oil and gas is likely, and refilling European gas inventories will be materially more expensive than expected following the loss of a month or more of Qatari LNG. The key question is how much this uncertainty and higher energy cost will dent global growth and corporate earnings. With the risk of a prolonged semi‑closure of Hormuz, weakening US labour data, emerging liquidity issues in private credit, and equity indices still only a few percentage points below all‑time highs, we do not find the broad equity market risk/reward particularly attractive.

On the other hand, we believe the risk/reward in our energy transition universe has improved. In general, higher energy prices support alternative energy producers and energy infrastructure providers, granted a deep recession is not triggered. The closest analogue is the invasion of Ukraine in February 2022, when renewable energy stocks significantly outperformed as energy prices rose on the expectation that Russian oil and gas would be shut in. Russian oil production ultimately fell only marginally, but gas output dropped sharply, and European gas prices have never returned to pre‑war levels. This has benefitted renewable energy developers and the broader electrification industry.

There is, however, one crucial difference this time. In 2022, even though markets initially expected a short war, it was immediately obvious that Europe had to wean itself off Russian energy and become less dependent on external suppliers. Higher spending plans on renewables, permitting reforms and subsidy schemes improved the long‑term outlook for alternative energy in Europe and the US. Stock prices reacted accordingly, rising despite aggressive rate hikes as central banks battled inflation.

This time, the closure of Hormuz is widely seen as temporary, which is unlikely to trigger the same level of “call to arms” on energy security. Moreover, Europe benefits from the higher wind and solar capacity built the last years and from the fact that baseline demand has never recovered as power prices shifted to a higher level. Also important, policy rates are not near zero as they were in 2022. Even if a months‑long closure of Hormuz sends gas prices soaring and reignites inflation, the rate environment is unlikely to deteriorate as dramatically as in 2022, when the ECB and Fed hiked four and seven times, respectively.

Against this backdrop, we expect renewable‑energy related equities to perform relatively well as the focus on energy independence and new generation capacity increases. We are hopeful that grid infrastructure will receive at least as much attention as additional solar and wind capacity. The marginal value of new renewable generation is waning without parallel investment in the transmission and distribution grids. In addition, new AI‑driven tools are likely to push demand management and grid utilisation further up the agenda as power prices rise. Overall, we continue to prefer companies that build and own grid infrastructure to pure‑play wind and solar developers, many of which lack durable competitive moats and may soon end up on the receiving end of political interference to cap retail electricity bills.

Although power generators are the obvious beneficiaries of higher gas and power prices, we are somewhat sceptical. First, many have hedged a large share of near‑term production, and gas and power forward curves beyond 2027 have not moved dramatically, limiting the earnings uplift. Second, if power prices stay elevated, European governments will almost certainly intervene by capping household utility bills, as they did in 2022, triggering a multiple derating.

Third, several European governments want to revisit carbon taxes imposed on European power production. A sharp spike in power prices this year may provide the political cover needed to slow or partially reverse pre‑set carbon price increases into the 2030s. While we support carbon pricing in principle, we question the wisdom of rigidly pre‑programmed hikes irrespective of the competitive backdrop. Can Europe afford to have 50% higher power prices than the US and Asia?

Fourth, affordability was on the agenda in Europe even before the war started, and if power prices remain elevated for an extended period, the current merit‑order system for paying power producers may come under further scrutiny. Under this model, the marginal MWh needed to meet demand sets the clearing price, so low‑cost generators (hydro, nuclear, solar, wind) receive the same price as expensive peaking plants. A shift towards a pay‑as‑bid system would be negative for low marginal‑cost producers and for flexible traders who benefit from the volatility that the merit‑order system creates.

Finally, many utilities and renewable developers had acquired an “AI premium”, as investors assumed they would earn excess returns selling power to price‑insensitive data centre operators. We have always questioned how far European governments would allow retail power prices to rise purely to boost margins for some of the world’s most profitable technology companies. With power now likely to be scarcer in Europe over at least the next year, the opportunity to lock in very attractive long‑term data centre contracts is diminished.

By contrast, we see more attractive opportunities among US power producers. AI‑driven demand growth for data centres is far more pronounced in the US, with ample scope for opportunistic companies to offer behind‑the‑meter solutions and help hyperscalers “bring their own power.” If global power prices stay elevated and weigh on growth, the US is relatively better insulated as its gas and power markets are not directly tied to Hormuz’ energy flows, and as a net energy exporter, the US economy ultimately benefits from higher oil and gas prices. The downside is that higher gasoline prices imply a wealth transfer from consumers to producers, politically sensitive in an election year, and something President Trump is unlikely to welcome. Since the outbreak of the war, we have shifted more of our net exposure towards the US.

All told, while we hope the war ends quickly, we fear that higher energy costs will persist for some time. That is bad news for the global economy but should accelerate investment toward electrification and grid infrastructure, particularly in Europe, as governments seek to reduce external dependence. For our investable universe, this is clearly positive: the energy transition is no longer just about climate, it is about security, competitiveness, affordability and growth.

FUND PERFORMANCE - ANOTHER STRONG MONTH DESPITE ISSUES IN SOLAR

February was another good month for the fund, with a return of 6.1%. In addition to a broadly positive earnings season, performance benefited from being on the right side of a market that increasingly focused on separating AI winners from losers. While the moats of many software and service companies are being questioned as AI disrupts their business models, our infrastructure‑ and power‑focused holdings are backed by tangible assets and growing order books as hyperscalers continue to lift capex budgets.

The best performing theme within the “Powering AI” complex was “Grid Services”, adding 2.2% to NAV in February. As we have written in previous reports, we continue to like this theme because it sits at the intersection of several powerful tailwinds: accelerating grid investment, rising power demand from AI and data centres, growing utility capex and a tightening contractor market where scale, execution capability and labour availability matter more than ever. All three long positions rose during the month, but Mastec (MTZ) stood out. We highlighted MTZ as one of our top picks for the year in our 2025 year- end review, and the company again exceeded expectations in February, advancing 24% after already gaining 11% in January.

The immediate driver was a very strong Q4 report. Group order intake was excellent, with a book-to-bill of 1.6x, Q1 adjusted EBITDA guidance came in 11% ahead of consensus and full-year EBITDA guidance around 5% above, which already looks conservative in our view given backlog coverage and the margin outlook in Pipeline Infrastructure. Free cash flow was somewhat weaker than expected, but this was mainly due to growth and timing, and management guided to solid conversion in 2026. The one softer element in the quarter was the pipeline business itself, where results came in slightly below expectations and backlog declined. Even there, however, guidance was strong and, in our view, still conservative. We continue to prefer MTZ among the US EPCs given its unique exposure to natural gas pipelines, where we believe fundamentals remain attractive and returns should be solid over the next several years.

“Diversified Renewables”, another “Powering-AI”-linked theme, added 1.0% to NAV in February and has contributed roughly one‑third of the fund’s year‑to‑date performance. The key contributor was once again Siemens Energy (ENR), which reported strong quarterly results with particularly robust order intake and free‑cash‑flow generation. The stock rose 16% in February and is up 39% year to date. Short positions in “neo‑cloud” names also contributed positively against longs in bitcoin miners. Finally, active trading around the very volatile Bloom Energy (BE) added to returns. The fund currently has no position in BE.

The second-best performing theme was “Wind”, adding 1.7% to NAV as Nordex (NDX1) advanced 28% following strong quarterly results, new medium term EBITDA targets and the initiation of capital returns to shareholders. Importantly, the results triggered meaningful upgrades, with consensus earnings estimates for 2026 and 2027 increasing by roughly 20% in both years. What stood out to us was that the improving outlook appears increasingly structural, demand is no longer just a Germany story but is supported by broader electrification needs across key markets, including a more constructive backdrop in the US. Management was also notably confident on execution, margins and free cash flow, and we continue to believe consensus may still underestimate the earnings potential. NDX1 remains the largest contributor to the fund’s P&L so far this year, despite us trimming the position several times.

The “Solar” theme, by contrast, performed poorly in February, driven mainly by weak quarterly reports from First Solar (FSLR), the leading US panel manufacturer, and Sunrun (RUN), the largest lease player in the residential rooftop market.

The main disappointment in First Solar’s quarter was not order intake or warranty costs, but weaker-than-expected 2026 revenue and, more importantly, gross margin guidance. Management’s explanation was reasonable, reflecting under absorption, a higher tariff burden as Trump’s IEEPA tariffs hurt their India and Southeast Asia and transition cost as production is moved from Asia to the US. It is now clear that 2026 is likely to be a transition year, but we continue to own the stock because several potentially important catalysts still lie ahead; including Section 232 tariffs, new anti-dumping and countervailing (AD/CVD) measures and final Foreign Entity of Concern (FEOC) rules, all of which could materially strengthen First Solar’s competitive position. After the recent sell-off, about half the current market cap is secured manufacturing tax credits, and we view the risk/reward as attractive.

Sunrun (RUN) shares some similarities with FSLR’s situation, but there are also important differences. RUN’s reported results were broadly in line with expectations, but 2026 new‑customer guidance was weaker than we, and the market, had anticipated. Our prior base case, shared by many, was that the leasing segment in which RUN is the clear market leader would grow in 2026 as tax credits for cash/loan purchases of residential systems expired. Instead, RUN guided to a low single‑digit decline in customer additions, emphasising cash generation and value creation over growth. The guidance likely also reflects a much tighter equity tax‑financing market until FEOC rules are clarified later this year.

Our view is that if RUN, as the leading leasing provider, expects a flat‑to‑declining market, that is significantly more problematic for smaller players supplying this market whose forecasts embed high growth. From a portfolio‑construction perspective, the position can therefore be hedged effectively. We added to our RUN position after earnings.

It has been a volatile start to March, with the Iran war briefly displacing AI as the main market focus. While we hope the conflict moves into the background in the coming weeks, we fear that its second‑order effects, most notably a higher energy‑risk premium, will linger and weigh on growth and risk assets. Even so, the main story of the year, at least for us, remains AI and hyperscaler capex. The key question is whether investment will continue to accelerate, or whether the negative equity‑market reaction to the latest capex upgrades will force a slowdown, at least in the growth rate.

We will watch developments closely. Until we see clearer signs of a shift in investment behaviour, we intend to maintain our high‑conviction long positions in power and infrastructure companies with durable competitive advantages, while continuing to build and adjust hedges and short positions to prepare for the next leg of this trade.

Thank you for your continued trust and confidence. We look forward to updating you again next month.

Sincerely

Vidar Kalvoy & Joel Etzler

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

- Portfolio Manager and Founder of the Coeli Energy Opportunities Fund.

- Over 15 years of investment experience spanning both public markets and private equity.

- Managed the Coeli Energy Transition Fund from 2019 to 2023.

- Spent six years at Horizon Asset in London, a market-neutral hedge fund.

- Started working with Vidar Kalvoy in 2012.

- Five years in Private Equity at Morgan Stanley.

- Began his investment career in the technology sector at Swedbank Robur in Stockholm in 2006.

- Holds an MSc in Engineering from the Royal Institute of Technology (KTH), Stockholm.

- Portfolio Manager and Founder of the Coeli Energy Opportunities Fund.

- Has managed energy equities since 2006 and brings more than 20 years of experience in portfolio management and equity research.

- Managed the Coeli Energy Transition Fund from 2019 to 2023.

- Head of Energy Investments at Horizon Asset in London for nine years, a market-neutral hedge fund.

- Experience from energy investments at MKM Longboat in London and equity research in the technology sector in Frankfurt and Oslo.

- Holds an MBA from IESE in Barcelona and a Master’s in Business and Economics from the Norwegian School of Economics (NHH).

- Before entering finance, he served as a lieutenant in the Royal Norwegian Navy.

IMPORTANT INFORMATION. This is a marketing communication.

Before making any final investment decisions, please refer to the prospectus of Coeli SICAV II, its Annual Report, and the KID of the relevant Sub-Fund. Relevant information documents are available in English at coeli.com. A summary of investor rights will be available at https://coeli.com/financial-and-legal-information/.

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

Please note that the management company of the fund may decide to terminate the arrangements made for the marketing of the fund in one or multiple jurisdictions in which there exists arrangements for marketing.