This material is marketing communication.

Note that the information below describes the share class (I USD), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class return. The information below regarding returns therefore differs from the returns in other share classes.

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

1) Share Class I USD

Performance for other share classes towards the end of the report.

FUND MANAGER COMMENTARY

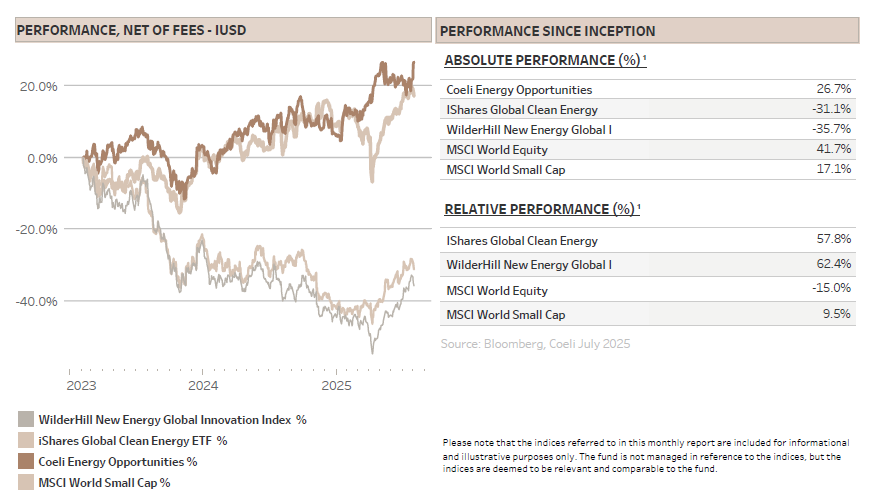

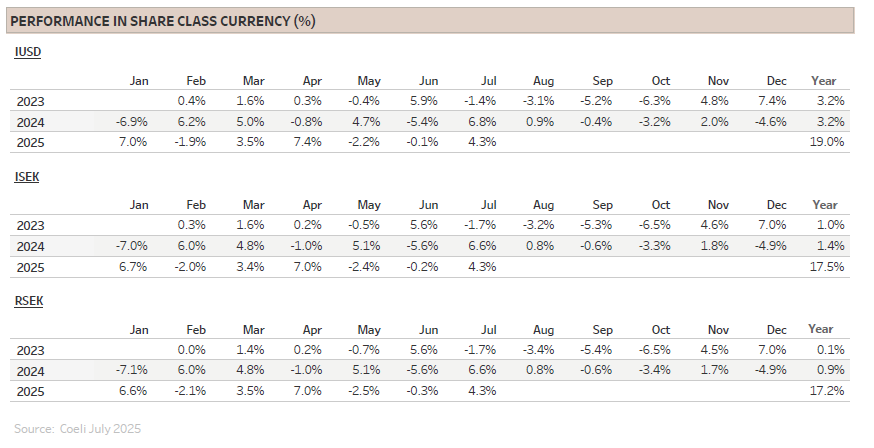

The Coeli Energy Opportunities fund gained 4.3% net of fees and expenses in July (I USD share class). Year-to-date, the fund is up 19.0% and it has gained 26.7% since inception in February 2023.

Compared to the two most comparable indices, the Wilderhill New Energy Global index (NEX) and the iShares Global Clean Energy (ICLN), the fund underperformed NEX by 1.9% and outperformed ICLN by 2.0%. Year-to-date the fund has outperformed NEX by 3.1% and underperformed ICLN by 0.1%. Since inception the fund is ahead by 62% and 58%, respectively.

July was a volatile month for the fund. Long positions did well, contributing 8.7% to NAV, driven in part by “powering AI” themes like ‘Grid Equipment’ and ‘Grid Services’, combined adding 2.9% to the monthly performance. There are no indications yet that hyperscalers will reduce their capital expenditure on AI chips, infrastructure, or power. On the contrary, AI momentum appears to be strengthening, with META and Microsoft (MSFT) reporting rising revenues and returns from their AI businesses. Spending on AI and its expected returns remains one of the most important drivers for the stock market, outweighing concerns about a potential tariff-induced slowdown.

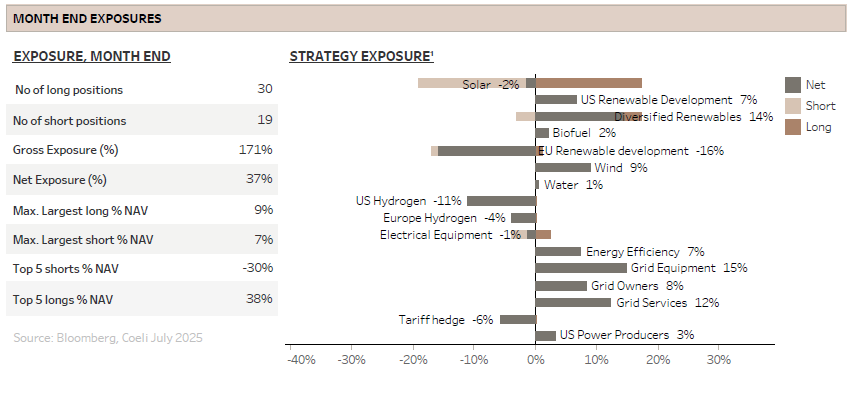

Short positions detracted 4.4% in July, partly due to the ongoing ‘meme’ stock rally affecting some of our conviction shorts. Goldman Sach’s ‘meme’ basket is now the best performing group of stocks for the year, up 37%. Additionally, our cautious positioning with net exposure below 40% for much of the month also had a net negative impact. With valuations in the AI enabler segment back to the pre-DeepSeek highs of late January, we increased certain shorts to hedge our significant exposure to the powering-AI theme. By month-end, net and gross exposures stood at 37% and 171%, respectively.

MARKET COMMENT – TRUMP WINNING THE TRADE WAR?

The S&P 500 rose 2.2% in July, notching nine new daily all-time highs and, unusually, did not experience a single trading day with a move of 1% or more in either direction. The STOXX Europe 600 lagged once again, returning just 0.9% for the month and it is now trailing the S&P 500 year-to-date in local currency terms. However, when measured in US dollars, the European index is up more than 20% this year, compared to less than 8% for the S&P 500.

Europe’s underperformance relative to the US can largely be attributed to a comparatively weak earnings season, while US companies delivered significant upside surprises. With approximately 75% of S&P 500 constituents having reported, this quarter ranks among the highest for positive earnings surprises in the last 25 years. So far, aggregate earnings for the quarter have risen 9% year-over-year, far exceeding the 4% growth forecast at the start of reporting season. It is worth noting, however, that results are only slightly above estimates from just before 'Liberation Day' in early April and below expectations set at the beginning of the year. Furthermore, considering the front-loading of demand ahead of tariff deadlines and the boost from stronger-than-expected AI-related revenues and profits from the 'Magnificent 7', we caution against assuming these results are indicative of a negligible impact from tariffs.

We remain firmly convinced that most tariffs will ultimately be borne by US consumers and importers, leading to higher prices, slower growth and compressed profit margins for several sectors. In contrast, some domestic manufacturers may benefit from expanded market share and higher margins as international competitors are forced out. While the net effect of tariffs is negative for the broader economy, it is important to remember the adage: “the stock market is not the economy.” Lower corporate taxes, indirectly funded by increased tariff revenues, along with gains from the deployment of AI and productivity enhancements, might more than offset the drag from tariffs and continue to support the stock market.

Moreover, it is encouraging that the new tariff regime has so far proved more disruptive than outright destructive. President Trump has succeeded in pressuring much of the world to accept a 15% baseline tariff rate, the new 'cost of doing business with the US'. In parallel, he has through ‘diplomatic shakedowns’ secured promises of large-scale direct investment and commitments to purchase US-made goods worth hundreds of billions of dollars. Given the sheer size and, in many cases, unattainable nature of these commitments, we interpret them as largely symbolic ‘wins’ leveraged by Trump for political advantage.

A striking example is the EU's pledge to buy USD 750bn worth of US oil, gas, and nuclear technologies over the next three years, approximately USD 250bn per year. That sum is more than triple the volume of EU’s energy imports from the US in 2024 and represents 75% of total US energy exports in the prior year. Realistically, it is unclear how the EU will persuade mostly private-sector buyers to commit to US supplies at that scale, or why US exporters would forgo other markets without significant incentives. Notably, the EU’s own climate ambitions to reduce fossil fuel use were conveniently left out of the agreement. And as we noted last month in ‘Nuclear Energy – Is a Bubble Brewing?’, commercially available small modular nuclear reactors are unlikely to launch within the agreed timeframe.

Ultimately, the EU’s commitment is unrealistic but may have been necessary to secure the deal. However, these outsized promises provide Trump with leverage to demand further concessions, ensuring tariff uncertainty will likely persist throughout his term.

Trump has also amplified policy uncertainty by increasing the pressure for FED chairman Powell to resign or slash interest rates, and by firing the head of the Bureau of Labor Statistics (BLS) following an unfavourable employment report. Both moves have the potential to undermine confidence in US economic stewardship, likely resulting in higher long-term interest rates and increased market volatility.

Ironically, the soft July jobs report and significant downward revisions to earlier months have made it politically easier for Powell and the FOMC to lower rates. The bond market is now treating a September rate reduction as nearly inevitable. Equity markets generally like rate cuts, and the prospect of a new easing cycle could sustain the ongoing market rally. Of course, this enthusiasm somewhat overlooks the fact that the catalyst for these rate cuts is a weakening economy.

SOLAR ENERGY – TRUMP’S WAR ON WIND AND SOLAR CONTINUES

It is well known that President Trump strongly dislikes wind energy. While he has historically been less critical of the solar industry, we believed after last month’s signing of the One Big Beautiful Bill Act (OBBBA) that that solar stocks would finally be investable again. It turns out, not yet. The Trump administration continues to create speed bumps and possible roadblocks for the industry.

Just days after signing the OBBBA, Trump issued an Executive Order (EO) instructing the Treasury to review guidance regarding ‘safe harbouring’ for wind and solar energy projects. Of the three actions required by Treasury by August 18, one is the issuance of new guidelines clarifying what constitutes the ‘beginning of construction’ for projects seeking tax credits after those credits expire. Notably, only wind and solar projects are subject to these new rules; other forms of energy generation remain unaffected.

Under the current, admittedly lenient standards established in 2013 during the Obama administration, construction is deemed to have started when a project passes either a physical work test or has incurred at least 5% of its total costs. Once qualified, developers have four years to complete the project. For large-scale solar initiatives costing hundreds of millions, passing the physical work test can be as simple as acquiring and storing transformers worth a few hundred thousand dollars. A straightforward hurdle for well-capitalized companies with strong project management. Developers like Nextera (NEE) and AES, both long holdings in the fund, prudently ‘safe harboured’ four years’ worth of projects at the end of last year.

There is strong precedent in the US against retroactive tax law changes, so projects that qualify before the new guidelines are announced on August 18 should remain eligible for credits as long as completion occurs within four years. If correct, the practical effect may simply be to restrict safe harbouring for projects launched from 18th of August and early July next year when the tax credits expire, potentially dampening activity in 2029 and 2030.

Nonetheless, precedent may not deter the Trump administration from ‘unprecedented’ actions. Some observers fear the new rules could be made retroactive to the EO’s early July announcement or even further back to the start of the year. Either way, uncertainty prevails, which seems to be the administration’s chosen tactic for impeding progress in wind and solar.

Alongside the EO tightening safe harbour rules, Treasury is also instructed to rapidly implement the new Foreign Entity of Concern (FEOC) restrictions included in the OBBBA. Originally designed to limit Chinese-linked companies from accessing US tax credits, FEOC has been broadened to limit and gradually exclude Chinese components from the US solar supply chain. As the law is new, bureaucratic interpretation leaves room for regulatory ‘creativity,’ and many believe that, with enough bad intent, the new framework could drastically limit equipment supply and block numerous solar projects. First Solar (FSLR), the fund’s largest holding and the only major domestic producer relying on non-Chinese technology, would be the main and maybe only beneficiary. The biggest losers will likely be Chinese solar firms and countless smaller developers whose projects rely on Chinese components.

Further, the administration is also going after the Chinese by launching a ‘Section 232’ investigation into imports of polysilicon, a key input for all solar modules except those from FSLR. Section 232 is meant for cases where imports are seen as a threat to national security, which is ironic, considering the government’s efforts to halt the solar industry’s growth. Should the investigation confirm such a threat, and few doubt the outcome, the President will have broad authority to impose tariffs, quotas or other trade restrictions. A decision is expected by year-end, most likely giving President Trump another stick to wield against the industry.

If that was not enough, Trump has also ordered that all solar and wind developments on federal land require personal approval from the Interior Secretary, who will only endorse projects meeting strict ‘capacity density’ (energy generation per acre) criteria. Solar projects are by definition land-intensive, and many will likely be disqualified automatically by this standard. While just under 5% of planned solar projects are on federal land, many developments on private or state land need federal permission for transmission lines or water crossings. Compounding these challenges, informational websites detailing applications and permit status have been deleted or rendered nonfunctional. We could go on with further examples of how the Trump administration tries to hamper the solar and wind industry, but the intent should already be unmistakably clear.

Why such aggressive obstruction? After all, Trump campaigned on reducing energy costs and claims the nation is locked in a power-hungry AI race against China. Power prices are set to increase with the rising power demand, why then undermine the development of alternative energy sources?

Speculation abounds. Many suggest it is partly retributive, a response to what Trump perceives as the Biden administration’s unfair targeting of fossil fuels and excessive support for renewables. Disregarding CO₂ emissions, which Trump has instructed his administration to ignore, this view has some merit. The substantial subsidies for renewables in the Inflation Reduction Act (IRA) are only defensible if climate change objectives are prioritized.

More perplexing is the risk of running short on power just as demand from AI data centres surges. As noted in our March 2024 report “Roadblocks on the AI Highway” and November 2024 “The Urgency to Secure Power”, access to energy is a key constraint in AI infrastructure deployment. The administration believes that natural gas and nuclear power will be the solutions, but the order backlog for gas turbines is record long and large turbines now come with a 4–5-year delivery time. The cost has also more than doubled over the last year. Moreover, for nuclear power, scaling nuclear will take a decade or more and come with prohibitive costs and a track record of decades of cost overruns.

Even leaving costs aside, the US faces a power supply gap over the next 3-4 years that solar and wind could help bridge. Rather than embracing these sources, Trump prefers to extend, or even reopen, coal plants. The climate impact aside, we question the economics of such extensions if substantial investments are required. It is conceivable that the political winds will shift after the next election, and a future Democrat-led administration would likely retaliate against polluting energy producers. This risk should also worry investors in gas-powered plants with start dates well into the next presidential term.

Overall, uncertainty in the solar sector remains high. Even if the new ‘safe harbouring’ rules are not retroactively applied and FEOC enforcement is not overly punitive, government hostility is likely to keep the industry under a cloud by intentionally restricting its growth to avoid paying out tax incentives.

At present, our fund is net short in the ‘Solar’ theme. We favour utility-scale solar over residential, as the former remains competitive even without tax credits whereas the latter would struggle. As noted in previous monthly reports, utility-scale solar is already cost-competitive with gas power without incentives. Moreover, power purchase agreement (PPAs) prices are trending higher in response to rising demand. According to UBS, the six largest hyperscalers account for nearly 20% of projected US electricity demand growth and given their substantial profit margins and urgent need for power, we are confident in their willingness to accept higher power prices. In effect, the current investment tax credits (ITC/PTC), which keep solar PPAs artificially low, are as much a subsidy for the hyperscalers as for the developers. Considering the hyperscalers financial strength and profitability, reduced tax incentives make sense.

FUND PERFORMANCE – VOLATILITY DRIVEN BY ‘MEME’ STOCK RALLY

Despite strong absolute performance, half of the fund’s themes posted losses during this volatile month, even as the main stock indices trended steadily upward. The primary source of P/L volatility was the ongoing ‘meme’ stock rally, which slowed and reversed towards month end. Although none of our short positions are true meme stocks, several are quite crowded and non-profitable. Many were also retail favourites during the renewable bubble and have been swept up in the current hype.

Grid-related themes were again the best performers for the second consecutive month. ‘Grid Equipment’ contributed 1.7% to NAV, with top holdings Nexans (NEX) and Prysmian (PRY) rising 15% and 17%, respectively, after reporting strong Q2 results. A similar story unfolded in ‘Grid Services,’ which added 1.1% to NAV, primarily driven by Maztec (MTZ) and Quanta (PWR), up 11% and 7%, respectively. All four stocks are trading significantly above levels seen prior to the Deepseek-related sell-off in late January, an event that ultimately spurred further data centre expansion rather than contraction. It is worth noting, however, that only PWR has seen substantial earnings upgrades since January; the gains elsewhere are mostly attributable to multiple expansion. Given the rich valuations across the group, we are actively reviewing ways to hedge our AI-power exposure.

‘Diversified Renewables’ were the second-best performing theme. For once, it was not Siemens Energy (ENR) doing the heavy lifting but rather Chart industries (GTLS), a long held favourite energy transition company that in July received a takeover proposal from Baker Hughes (BKR) at a 22% premium to last close. The bid from BKR came even though GTLS was in a merger process with Flowserve (FLS). Although we valued stand-alone GTLS higher than the USD 210 bid from BKR, we are pleased to be taken out as the proposed merger with FLS diluted some of the most attractive parts of the GTLS.

The only major losing theme was ‘EU Renewables,’ which subtracted 0.9% from NAV in July. This theme is comprised primarily of short positions, both pure-play power generators and renewable developers with exposure to offshore wind. The power generators serve as effective funding stocks given their overvaluation based on forward power price curves that the companies gradually lock in through active hedging.

Our scepticism toward some pure-play renewable stocks stems from the poor risk-return profile of recent years’ offshore wind investments. We believe this view is supported by the fact that the industry has mostly slashed capex and recently abstained from bidding at several auctions. Moreover, farm-downs is a must to finance remaining capex, but has proved to be difficult or expensive as there are few potential buyers. Nevertheless, the fact that the industry has reduced number of bids and face less competition suggests that returns on current bids are more likely to meet return targets than those projects currently under development.

In last month’s report, we noted the S&P 500’s peak multiple, emphasizing that such a valuation requires either accelerating earnings growth or reduced risk. While we are still optimistic about the AI thematics that is driving the growth in stock markets, our focus is on the AI enablers that build infrastructure and power rather than the AI adopters. In our view, the AI enablers are clear beneficiaries of increased electrification and possess multiple structural advantages, not limited to data centers expansion alone. On the risk side, trade war fears have subsided, and anticipated Federal Reserve rate cuts into year-end should support higher valuation multiples. Nevertheless, with the two seasonally weakest months for equities ahead, we remain cautious and aim to increase net exposure later this year.

Thank you for your continued trust, and we look forward to updating you again next month.

Sincerely

Vidar Kalvoy & Joel Etzler

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

- Portfolio Manager and Founder of the Coeli Energy Opportunities Fund.

- Over 15 years of investment experience spanning both public markets and private equity.

- Managed the Coeli Energy Transition Fund from 2019 to 2023.

- Spent six years at Horizon Asset in London, a market-neutral hedge fund.

- Started working with Vidar Kalvoy in 2012.

- Five years in Private Equity at Morgan Stanley.

- Began his investment career in the technology sector at Swedbank Robur in Stockholm in 2006.

- Holds an MSc in Engineering from the Royal Institute of Technology (KTH), Stockholm.

- Portfolio Manager and Founder of the Coeli Energy Opportunities Fund.

- Has managed energy equities since 2006 and brings more than 20 years of experience in portfolio management and equity research.

- Managed the Coeli Energy Transition Fund from 2019 to 2023.

- Head of Energy Investments at Horizon Asset in London for nine years, a market-neutral hedge fund.

- Experience from energy investments at MKM Longboat in London and equity research in the technology sector in Frankfurt and Oslo.

- Holds an MBA from IESE in Barcelona and a Master’s in Business and Economics from the Norwegian School of Economics (NHH).

- Before entering finance, he served as a lieutenant in the Royal Norwegian Navy.

IMPORTANT INFORMATION. This is a marketing communication.

Before making any final investment decisions, please refer to the prospectus of Coeli SICAV II, its Annual Report, and the KID of the relevant Sub-Fund. Relevant information documents are available in English at coeli.com. A summary of investor rights will be available at https://coeli.com/financial-and-legal-information/.

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

Please note that the management company of the fund may decide to terminate the arrangements made for the marketing of the fund in one or multiple jurisdictions in which there exists arrangements for marketing.