This material is marketing communication.

Note that the information below describes the share class (I USD), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class return. The information below regarding returns therefore differs from the returns in other share classes.

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

1) Share Class I USD

Performance for other share classes towards the end of the report.

FUND MANAGER COMMENTARY

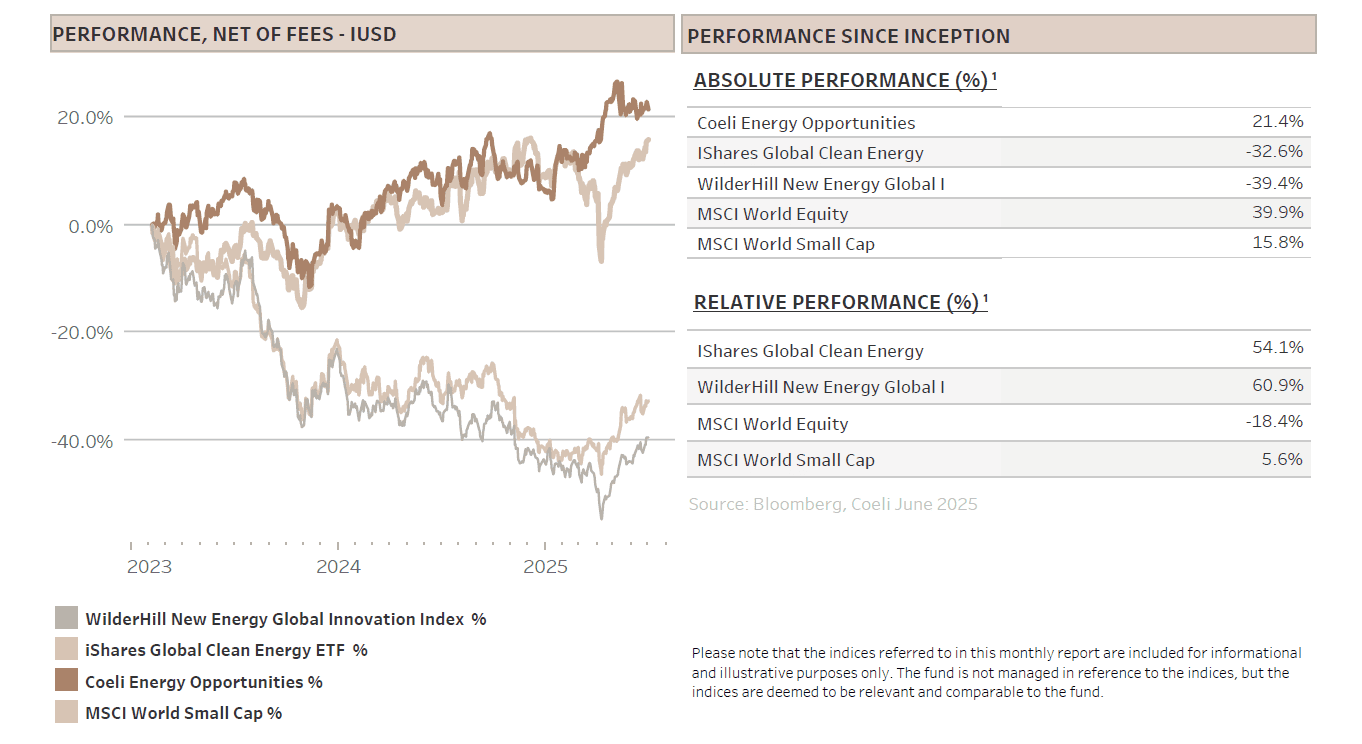

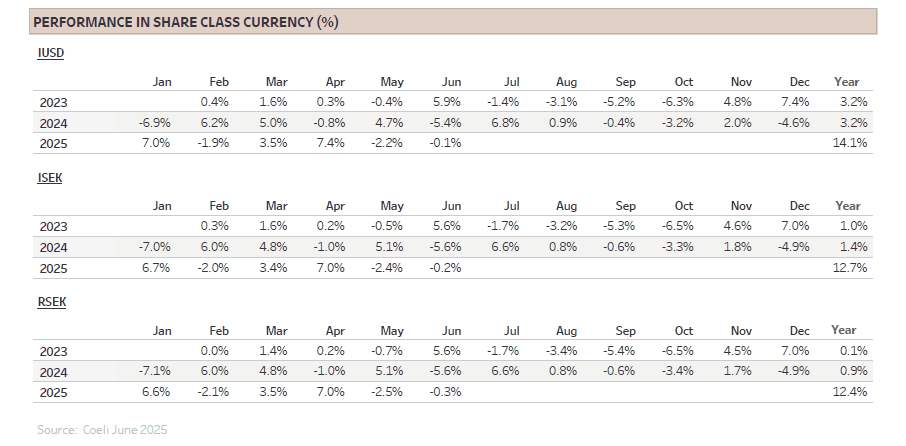

The Coeli Energy Opportunities fund lost 0.1% net of fees and expenses in June (I USD share class). Year-to-date, the fund is up 14.1% and it has gained 21.4% since inception in February 2023.

The fund underperformed the most comparable indices, the Wilderhill New Energy Global index (NEX) and the iShares Global Clean Energy (ICLN) by 8.0% and 4.6% in June. Year-to-date the fund is outperforming the NEX by 4.9% and underperforming ICLN by 2.4%. Since inception the fund is ahead by 61% and 54%, respectively.

President Trump’s recent policy wins have boosted market sentiment and helped drive US equities to new highs. The market has largely priced out uncertainty surrounding trade policy and geopolitical risk after the bombing of nuclear facilities in Iran. Trump also got a significant victory by signing the ‘One Big Beautiful Bill Act’ (OBBBA) in early July.

The fund’s long positions, especially those related to AI and the power grid, tracked the broader market and gained 5.6% over the month. However, the short positions lost 5.7% mainly due to losses in the ‘US Hydrogen’ (-2.6%) and ‘Solar’ (-1.5%) themes, both impacted by the legislation of the OBBBA. US hydrogen stocks received unexpected relief when the final Senate bill extended tax credits for a couple of more years than initially anticipated. However, the intention of the republicans is not at all to aid green hydrogen producers, but rather to help oil and gas companies producing blue hydrogen, a competitor of green hydrogen.

In the ‘Solar’ theme, the fund was again blindsided by literally last-minutes changes to the Senate bill that gave reprieve to some of our short positions. Navigating the bill’s progression and trading renewable energy stocks during the OBBBA legislation has been a true rollercoaster. Although the new law is far worse for renewable energy sectors like wind and solar than the original Inflation Reduction Act, the final outcome is better than feared. The bill’s signing marks a clearing event for stocks, allowing both the market and us to refocus on companies’ fundamentals. We discuss the act in more detail in the Fund Performance part.

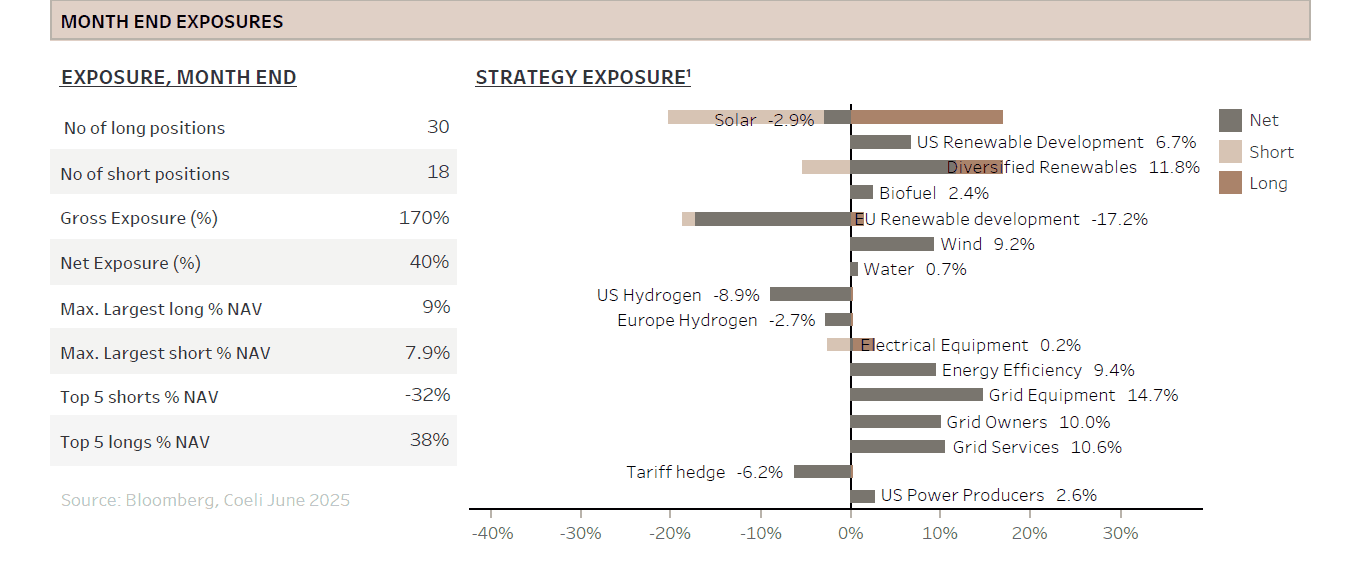

Amid the extreme volatility caused by the legislation of OBBBA, we maintained the fund’s net exposure in the low 40% range for most of the month, while gross exposure fluctuated between 155% and 170%. We ended the month at 39% and 167%, respectively.

MARKET COMMENT – DOES TARIFFS MATTER AT ALL?

The S&P rose 5% in June, reaching a new all-time high after its fastest recovery ever from a >15% sell-off. Europe lagged with the Stoxx 600 falling 1.3% as the market rotated back to US growth stocks, led by Mag-7 and including AI power stocks.

One of the key drivers of this strong performance is the market’s reduced fear of tariffs and Trump’s trade policies negatively impacting the US and the global economies. As we write this report, the reciprocal tariff deadline of 9th of July is fast approaching and after signing only two trade deals, not agreements, Trump has started sending countries dictates on ‘how much they have to pay’ to trade with the US. So far, the rates have been higher than most expected, but the market reaction has been measured, having grown accustomed to Trump’s negotiation tactics.

Considering the two announced deals with the UK and Vietnam, it should be clear that Trump’s plan is not to level the playing field by forcing all countries to eliminate tariffs. While Vietnamese exports face a minimum tariff of 20% entering the US, the rate is zero for US export to Vietnam. We have long argued this reflects the US need for tariff revenue and Trump’s genuine desire to onshore manufacturing to create blue-collars jobs for Americans.

As the world seems to have accepted a 10% base tariff as the minimum, with many countries expected to ‘willingly’ be paying more, tariff income for the US will be significant even as overall import levels gradually decline. This should be seen as a major win for Trump.

Although this income will not at all offset all federal taxes, as Trump suggested during his campaign, it is likely to cover most or all the increased deficit resulting from the tax cuts in the OBBBA. Essentially, President Trump and the Republicans are financing one tax cut with another, since tariffs are effectively a tax on imported goods.

Who will bear this tax? Contrary to Trump’s claim that it will be paid by foreigners, Goldman Sachs estimates that 70% will be borne by US consumers through higher prices, with the reminder split equally between US importers and the foreign exporters. If correct, this implies eventual margin pressure on both US and foreign companies.

We remain firmly in the camp that increased tariffs will eventually harm the US and the global economies. However, this may be offset by an AI-driven productivity boost, which could fuel medium-term earnings expectations and justify higher valuation multiples than in the past. Moreover, with likely reduced risk of a tit-for-tat tariff trade war, the inflationary impact of tariffs is more likely to be transitory than we and most pundits feared earlier this year. This means the FED could resume cutting interest rates later this year.

Finally, note that the tax cuts in OBBBA are short-term fiscally expansionary, as savings will accrue in future years while spending increases occur almost immediately. This means both the US and Europe face combined fiscal and monetary expansion over the next year. Combined with proposed and likely changes to US banks’ capital requirements and Europe’s work on a Savings & Investments Union to reform the European securitisation market to free up banks balance sheet for Europe’s investment needs, liquidity will be abundant. This is generally a positive signal for the stock market, even when it is trading at historically high valuation multiples.

NUCLEAR ENERGY – IS A BUBBLE BREWING?

Power demand in the US is surging, a consensus that crosses the political divide. However, while Republicans are curtailing tax incentives for wind and solar energy, they are boosting incentives for other forms of energy generation. One of their favourites is nuclear power, which under the OBBBA received an extension of tax credits by three years, now lasting until 2035. For a capital-intensive sector with long lead times, this is important, and it is one reason nuclear is once again prominent in the headlines. The question remains: can nuclear help close the US power supply gap, or is it just another hype cycle?

It is common knowledge that Greenpeace and many environmental activists have a strong dislike of nuclear power. This sentiment emerged in the 1970s and was reinforced by disasters like Chernobyl and Fukushima. These events helped entrench a narrative that reactors are dangerous, the waste unmanageable, and the economics unworkable. Most of these claims, apart from the subjective fear of radiation, have since been challenged by experts. New reactor designs are inherently safer, waste volumes are modest and technically solvable, and nuclear provides something most renewables cannot: always-on, carbon-free electricity.

Nevertheless, nuclear power in the US has been dormant for decades. Until last year, no new reactors had entered commercial operation since the 1990s. Only the two long-delayed Vogtle units in Georgia were under construction, each more than seven years behind schedule with cost overruns of more than USD 20bn, 150% over the original budget. However, this is beginning to change as energy security, climate change, policy shifts and perhaps most importantly, rising power demand have pushed nuclear back onto the agenda. President Trump has singled out nuclear as a strategic priority, setting targets to have ten new reactors under construction by the end of this decade and to quadruple US nuclear capacity by 2050.

Although the ambition is notable, some observers, including us, have viewed it as more rhetorical than real. The US has limited experience and capacity in building nuclear plants and regulatory hurdles remain high. Still, since mid-2024, activity has picked up. In Tennessee, Kairos Power began construction of its Hermes test reactor, the first non-light-water reactor to break ground in the US in more than 50 years. The Department of Defence has also begun work on Project Pele, a portable 1–5 MWe microreactor designed to power remote military bases. Other projects are moving through permitting stages, often with strong federal backing. While these are small steps, in a slow-moving sector like nuclear, they are significant.

The US regulatory environment is undergoing its most substantial reshaping since the Atomic Energy Act of 1954. Trump’s executive orders have directed the Nuclear Regulatory Commission (NRC) to shift from a risk-averse to a “pro-innovation” stance. On paper, this sounds transformational and has excited investors. However, senior experts note that similar ambitions have been proposed by many administrations over the last 30 years. The fact is that the NRC’s processes are built on extensive institutional knowledge about reactor safety and licensing. While efficiency and innovation can be pursued, overriding safety protocols is extremely difficult, which explains why reforms rarely deliver the breakthroughs hoped for.

Nonetheless, improvements have been made in the review time for construction permits. A notable change finalized in 2024 allows emergency planning zones (EPZs) to be determined based on the potential size of a radiation release rather than fixed 10-mile zones designed for large, legacy reactors. For small reactors with very low fission inventories, especially microreactors, this could reduce the required safety buffer to just a few hundred meters. This change could enable reactors to be located closer to population centres and industrial facilities. However, it remains uncertain how many local communities, many of which have long resisted wind farms and transmission lines, will welcome nuclear plants in their “backyards”.

Another major NRC reform is the ongoing rollout of a new licensing framework that is performance-based, risk-informed, and in principle technology-neutral. It replaces the assumption that all new reactors must resemble pressurized water reactors from the 1980s. Combined with Department of Energy’s pilot programs and targeted funding, this provides microreactors and other advanced designs a clearer path to licensing than ever before.

Internationally, despite the disastrous cost overruns on recent European nuclear plants and Germany’s shutdown of its own nuclear capacity, political support for nuclear power is growing. For example, Sweden’s parliament recently approved a government-backed plan to finance 5GW of new nuclear capacity through subsidies or contracts for difference (CFDs). While history suggests Sweden may struggle to meet its 2.5GW target by 2035, increased European focus on rebuilding its nuclear industry could help it reach the 5GW target by 2045. Other European countries are exploring similar moves, reflecting a broader global reassessment of the role of nuclear power.

All in all, as reflected in the rising share prices of nuclear technology-related stocks, momentum is building. However, we remain cautious about extrapolating too much from these early signals. Most small modular reactors (SMR) and microreactor projects announced so far are small-scale demonstrations, not utility-scale deployments. Many are backed by federal grants or strategic customers, like the military, rather than competitive power markets. Moreover, despite regulatory improvements, building commercial reactors still takes years, not quarters. Even under the most optimistic assumptions, it is difficult to envision the US nuclear fleet adding more than a few hundred megawatts of capacity in the next five years. Given the expected power supply gap driven by AI data centre demand, this will not be sufficient. As we have long argued, solar and wind remain the only large-scale power generators capable of closing the supply gap over the next 3-4 years.

Nevertheless, a wave of private-sector activity is underway, with over 100 start-ups pursuing SMRs or microreactors. This is encouraging and demonstrates genuine innovation, but it raises a fundamental question: which utilities or governments will truly place their bets on one of these companies? Especially since major industry players like GE-Hitachi, Westinghouse and Rolls Royce, with more than 60 years of experience, have conducted research on small reactors for decades and offer their own SMR commercial solutions. As the incumbents begin winning contracts, we believe most start-ups will ultimately struggle to attract customers, secure regulatory approval and raise additional capital.

On the fuel side, spot uranium price rose fivefold to over USD 100 per pound in 2024 before settling below USD 80. The move was driven by structural supply tightness as well as political developments. Importantly, the Biden administration passed a law banning Russian uranium imports from 2028, with a waiver period through 2027. Since Russia supplies around 20–25% of enriched uranium used in US reactors, this caused significant optimism among both established and start-up uranium miners. There is renewed focus on domestic enrichment and conversion capacity, with mothballed mines restarting and new greenfield mining projects attracting capital.

However, there is probably not yet a speculative bubble in uranium. The supply side has been underinvested for years, and shifting away from Russian supply will require a meaningful rebuilding of US capacity. That said, much of the anticipated uranium demand growth assumes a significant ramp-up in reactor construction that has yet to materialize. Also, Trump tend to be his favourite sectors’ worst enemy at times, and it is easy to imagine a future reversal of the Russian uranium ban as part of a future trade agreement with Russia.

All in all, we believe the nuclear sector is in the early stages of a structural, albeit uncertain, shift. The tailwinds are real: bipartisan political support, generous tax credits, a friendlier regulatory regime, and a clear case for firm, carbon-free power. However, enthusiasm has outpaced construction timelines. The only two public SMR providers (excluding the SPAC pipeline), Nuscale Power and Oklo Inc are trading at 19x and 362x EV/Sales in 2028, respectively, demanding valuations that require flawless execution and continued regulatory and customer success. The broader investment community needs to distinguish between long-term opportunity and near-term hype.

For now, we remain on the sidelines and expect incumbents to be the ultimate winners rather than the start-ups. We anticipate ample opportunities to short the hype, much like in other similar cycles. We are monitoring permitting pipelines, construction starts, and domestic fuel policy more closely than headlines or stock price movements. When it comes to nuclear, progress is measured in poured concrete, not press releases.

FUND PERFORMANCE – ROLLERCOASTER IN LEGISLATING THE OBBBA

The fund’s flat performance in June was primarily due to overly cautious positioning both entering and during the month, combined with difficulties trading the sharp back-and-forth between the House and the Senate during the passage of the OBBBA.

In the ‘Solar’ theme, which was the second-worst performer of the month, the fund lost 1.5% of NAV. This was largely driven by a last-minute change to the Senate bill that included tax incentives for residential solar while removing legislation that would have taxed the use of components linked to Chinese manufacturers. We were short both thematics and consequently incurred losses. Earlier in the month, the initial Senate bill contained language suggesting that our largest long position, First Solar (FSLR), would only be eligible for about 40% of the expected manufacturing tax credits. The stock tanked but recovered as this was, thankfully, clarified in the final Senate bill, which also included improvements for solar power developers and utility-scale solar manufacturers.

We were quite surprised that the fiscal hawks in the House of Representatives accepted the final Senate bill without a fight. It is also concerning that they claim President Trump allegedly promised strict enforcement of and/or changes to the rules for solar and wind tax credits. Normally, we would be comfortable with the executive power following newly enacted laws, but Trump’s unpredictability and disregard for norms add an extra layer of uncertainty.

Nonetheless, we remain comfortable with our long position in utility-scale solar, as we believe solar will be the go-to power solution over the next few years. When the tax credits expire, we expect the value of time-to-power for the hyperscalers building AI data centres to sustain demand at higher price points, thus maintaining margins for the developers. Our long positions include developers such as NextEra (NEE) as well as manufacturers like First Solar (FSLR) and Nextracker (NXT). On the short side, we continue to believe Chinese manufacturers will struggle to obtain tax incentives and operate profitably in the US. Additionally, Chinese solar panel demand, which accounts for about half of global demand, is expected to plummet in the second half of 2025 due to new regulations in China. Given that global nameplate capacity is already almost double current demand, we see slim chances of prices increasing in the near term.

The worst-performing theme of the month was ‘US Hydrogen,’ which detracted 2.6% from NAV. As mentioned, hydrogen was a relative winner in the OBBBA. Until the final Senate bill, hydrogen tax credits were expected to expire at the end of this year, but they were surprisingly extended to the end of 2027 after intense lobbying from the oil and gas industry. However, these companies want tax credits to produce blue hydrogen using natural gas as feedstock. Blue hydrogen competes with green hydrogen, which is produced by electrolysers that convert water and electricity into hydrogen. Although green hydrogen has a significantly lower carbon footprint, it comes with a much higher price tag. Moreover, many green hydrogen projects planned during the 2020–2023 hype under the Biden administration have struggled to find buyers and consequently to secure financing. We believe that extending the timeline by a couple of years to attract potential offtakers in the US is unlikely to make a difference as political support for green hydrogen has waned and rising power prices only reduce its competitiveness. We maintain our negative positioning in this segment and expect to recoup the losses over the last months.

The best performing thematic was again the grid-related themes, all linked to the increasing power demand in part driven by growth in AI data centres. The theme ‘Diversified Renewables,’ including Siemens Energy (ENR) and Bloom Energy (BE), added 1.7% to NAV, while ‘Grid Services’ and ‘Grid Equipment’ each contributed 0.9%. Optimism around AI-driven power demand has returned to pre-DeepSeek levels and AI-related stocks have hit new all-time highs. We remain uncertain about the extent to which AI will boost overall productivity and aggregate corporate earnings, but until clearer evidence emerges, this thematic is likely to continue to support share prices. Additionally, we are investing in AI indirectly through companies providing power and infrastructure to AI data centres, the “shovel companies”. These firms should benefit from increased power demand for several years, even if productivity gains are dispersed across the broader economy and do not immediately improve overall profitability.

Following the fastest recovery in S&P 500s history, the index ended the month at a new all-time high and is trading at a P/E ratio of 22x, placing it in the top 5% valuations over the past 30 years. To justify such a premium multiple, either earnings growth much accelerate, or risk levels need to decline further. Although improving liquidity, driven by deregulation of banks’ balance sheets and further interest rate cuts by the FED, will provide some support for current valuations, the most critical driver remains sustained earnings growth. While we continue to believe that tariffs act as a drag on the global economy by reducing corporate margins and earnings, the negative impact may be less severe than previously expected. Moreover, this could be more than offset by improved earnings growth fuelled by AI-driven productivity gains.

All in all, although our cautious positioning has proven incorrect over last past two months, we are not inclined to chase the market at this stage, especially given the potential for rising tariff issues as we approach the seasonally weaker stock-market months of August and September.

Thank you for your continued trust, and we look forward to updating you again next month.

Sincerely

Vidar Kalvoy & Joel Etzler

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

- Portfolio Manager and Founder of the Coeli Energy Opportunities Fund.

- Over 15 years of investment experience spanning both public markets and private equity.

- Managed the Coeli Energy Transition Fund from 2019 to 2023.

- Spent six years at Horizon Asset in London, a market-neutral hedge fund.

- Started working with Vidar Kalvoy in 2012.

- Five years in Private Equity at Morgan Stanley.

- Began his investment career in the technology sector at Swedbank Robur in Stockholm in 2006.

- Holds an MSc in Engineering from the Royal Institute of Technology (KTH), Stockholm.

- Portfolio Manager and Founder of the Coeli Energy Opportunities Fund.

- Has managed energy equities since 2006 and brings more than 20 years of experience in portfolio management and equity research.

- Managed the Coeli Energy Transition Fund from 2019 to 2023.

- Head of Energy Investments at Horizon Asset in London for nine years, a market-neutral hedge fund.

- Experience from energy investments at MKM Longboat in London and equity research in the technology sector in Frankfurt and Oslo.

- Holds an MBA from IESE in Barcelona and a Master’s in Business and Economics from the Norwegian School of Economics (NHH).

- Before entering finance, he served as a lieutenant in the Royal Norwegian Navy.

IMPORTANT INFORMATION. This is a marketing communication.

Before making any final investment decisions, please refer to the prospectus of Coeli SICAV II, its Annual Report, and the KID of the relevant Sub-Fund. Relevant information documents are available in English at coeli.com. A summary of investor rights will be available at https://coeli.com/financial-and-legal-information/.

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

Please note that the management company of the fund may decide to terminate the arrangements made for the marketing of the fund in one or multiple jurisdictions in which there exists arrangements for marketing.