This material is marketing communication.

Note that the information below describes the share class (I USD), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class return. The information below regarding returns therefore differs from the returns in other share classes.

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

1) Share Class I USD

Performance for other share classes towards the end of the report.

FUND MANAGER COMMENTARY

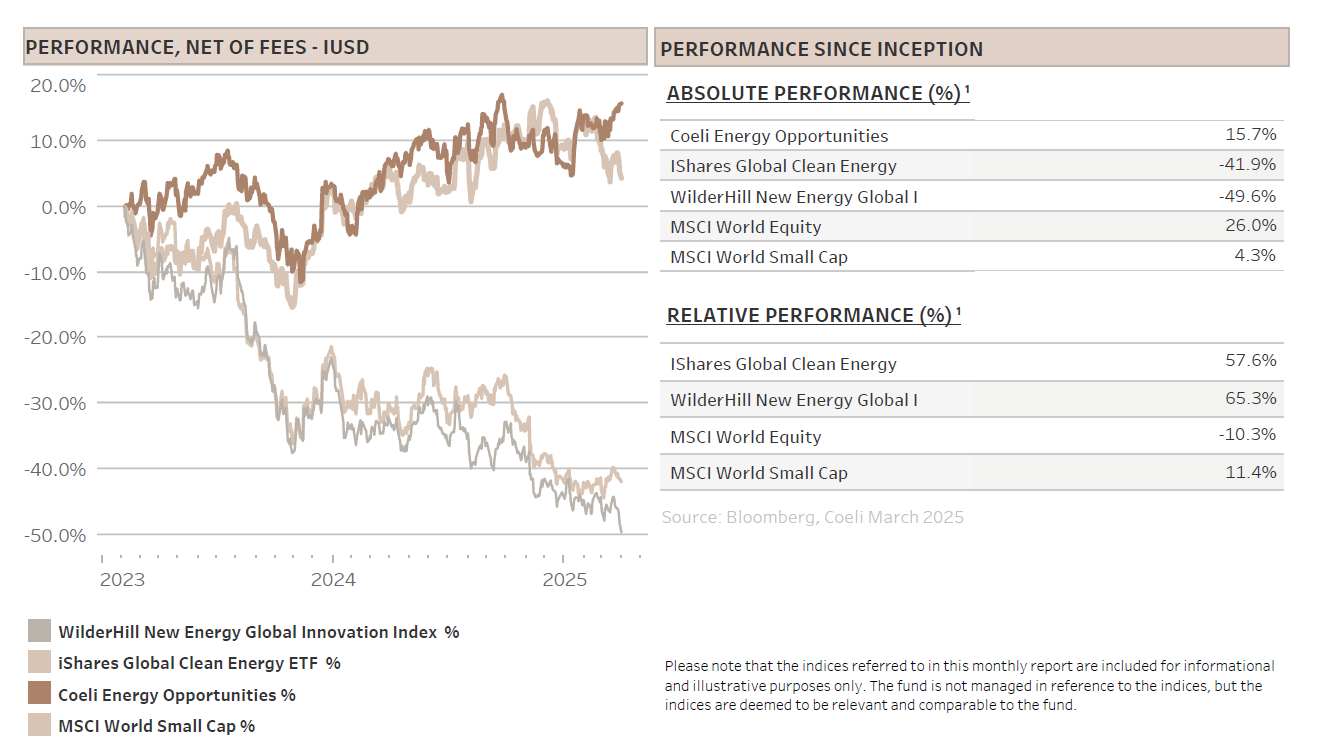

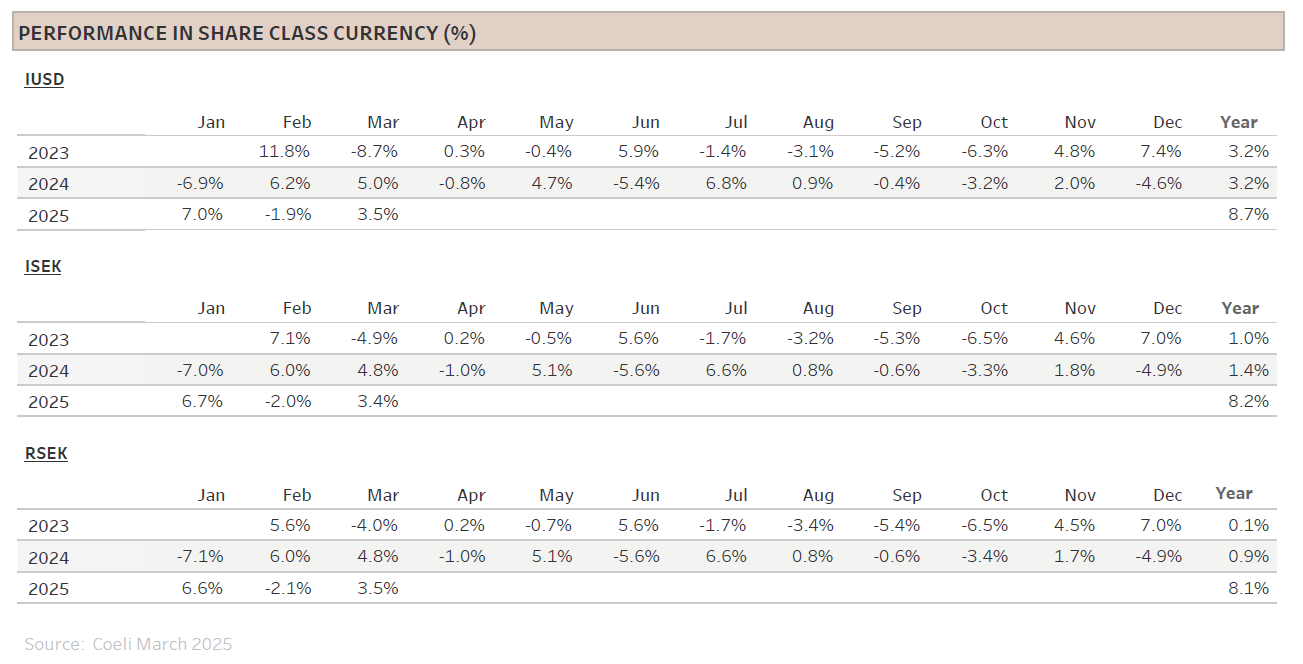

The Coeli Energy Opportunities fund gained 3.5% net of fees and expenses in March (I USD share class). Year-to-date, the fund is up 8.7% and since its inception in February 2023, it has gained 15.7%.

The fund outperformed the most comparable indices, the Wilderhill New Energy Global index (NEX) and the iShares Global Clean Energy (ICLN) by 9.5% and 0.5%, respectively. The year-to-date outperformance is 18% and 8%, and since inception the fund is ahead by 65% and 58%, respectively.

During the month, the fund changed its name to Coeli Energy Opportunities. There is however no change to the strategy, risk profile or management of the fund.

In our February investor letter, we highlighted that we viewed the near-term market outlook as challenging. Rising uncertainty, historically a poor omen for equites, weighted on the sentiment. The so-called ‘Trump trades’ which surged after the US election, had already started to deflate as expectations of stronger growth and inflation gave way to fears of recession and stagflation. European stocks on the other hand, had a strong start to the year amid hopes for a Ukraine peace deal and German fiscal stimulus. However, as we expected, with no immediate earnings boost and impending US tariffs, European stocks fell into month end.

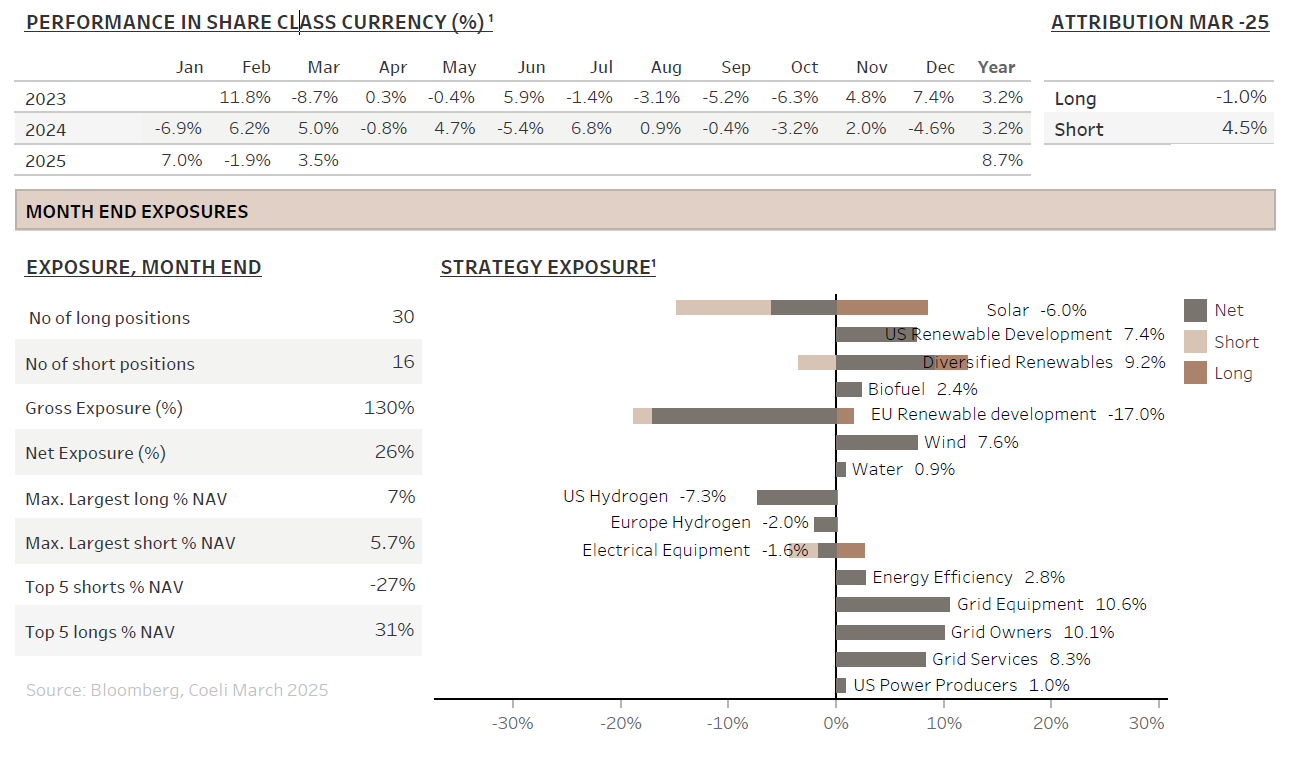

The fund delivered strong performance in March, with over 70% of the themes generating profits. Short positions contributed 4.5% to NAV, while longs in aggregate lost 1%. The best performing theme was ‘Solar’, contributing 2.1% and benefitting from short positions in tariff exposed Chinese and European solar equipment companies. The second-best theme was ‘Grid Owners’, adding 1.7% to NAV, aided by declining long-term rates and a flight to safety during the market sell-off. The worst performer was ‘Diversified Energy’ where one of our largest long positions, Chart Industries (GTLS), accounted for most of the loss as the stock declined by 25% during the month on no company specific news. More details on fund performance in the dedicated section below.

As noted last month, President Trump’s policy approach and unconventional leadership style has increased market volatility, creating attractive trading opportunities within our investment universe. We expect this volatility to stay elevated in the near term and while we maintained gross exposure unchanged at about 130% into month end, we have during the first three trading days of April lowered it to 115%. Net exposure at month end was only 26%, well below our sweet spot of 40-80%, an indication of our cautious view on the markets into April. However, three days into the new month, it is at 20% after having dipped even lower during the sell-off post the tariff announcement.

MARKET COMMENT – WAITING FOR ‘LIBERATION DAY’

The S&P 500 fell by 5.8% in March, its worst monthly performance since December 2022. Europe’s Stoxx 600 declined by 4.2% but extended its quarterly outperformance against the S&P 500 to 12%. The S&P 500 decreased by 5.2% in the first quarter, dragged down by the MAG 7 stocks, which lost 15% compared to the nearly flat performance of the equal weight S&P 500 (SPW). Later in this report, we will discuss whether the US tech sector has peaked, at least relative to the broader market, and more importantly, whether US tech dominance is under threat.

Last month, we warned that ‘recession risk is likely lurking around the corner’ in the US. That risk only intensified in March as many companies in the US told us that activity has slowed down and projects are paused awaiting clarity on tariff policy. This was supposed to happen on "Liberation Day" on April 2, when Trump was expected to unveil his team’s detailed work on reciprocal tariffs on countries and industries. Many pundits believed, or hoped, that this would serve as an invitation to negotiate lower tariffs on both US imports and exports, acting as a clearing event for risk and boost to trade and economic growth.

Instead, the outcome was far from reassuring. The reciprocal tariffs were not only higher than expected but were accompanied by a blanket 10% universal tariff on import, even from countries running trade deficits with the US and imposing no tariffs on American goods. Worse, the implementation timeline was aggressive; only two days for the universal tariff and a week for the reciprocal measures, leaving virtually no room for meaningful negotiations. Major economies facing high reciprocal tariffs, including the EU and China, have already retaliated or warned of retaliation. Considering Trump’s temper and combative focus on ‘winning’, a quiet retreat seems unlikely. The risk of a tit-for-tat trade war triggering a recession has risen sharply, and markets reacted with two days of steep declines, the worst since the Covid days.

We are not entirely surprised by the punitive tariffs as we have for some time argued that Trump’s agenda goes beyond simply renegotiating trade terms. Trump has long been deeply committed to reviving and expanding US manufacturing and for some reason, he is convinced that the economic value add from manufacturing of goods is more valuable than producing services.

More importantly, as we have noted in several previous reports, the Trump administration is scrambling to fund the extension of Trump’s first-term tax cuts, now estimated to cost about USD 4.6 trillion over the next decade. Although we expect most or even all reciprocal tariffs to be negotiated downward, the 10% universal tariff on all goods import seems to be a floor. Last year, assuming unchanged import volumes, this would have generated revenues of more than USD 300bn. Of course, import volumes will decline, but it looks increasingly likely that tariff revenue could be a big offset to the tax cut extension.

We expect the 10% universal tariff to remain for revenue generation purposes, while sectoral tariffs will stay for national security reasons. However, we continue to believe that reciprocal tariffs will be lowered for most countries. The fact that the tariffs are pegged to last year’s trade deficits, rather than existing tariffs on US export, suggest they are not designed to be permanent. However, uncertainty will linger, and the damage is no longer confined to investor sentiment. A widely watched CEO confidence index plunged, prior to the tariff announcement, to levels consistent with stagnant US growth. Post the announcement and a stock market crash, we can anticipate the outcome of the next CEO index update. Uncertainty will inevitably weigh on investment decisions, increase supply chain costs and curb hiring, among other effects. Earnings will face pressure and sell- side analysts will slash bottom-up estimates, further pressuring stock prices.

IS US TECHNOLOGY DOMINANCE UNDER THREAT?

After years of near-uninterrupted outperformance, cracks may be starting to form in the US tech sector. The “Magnificent Seven”, Apple, Microsoft, Alphabet, Amazon, Meta, Nvidia, and Tesla, are, as we pointed out above, down roughly 15% in the first quarter, while the remaining 493 stocks in the S&P 500 were broadly flat. Whether this marks a temporary pause or something more structural remains unclear, but the relative weakness has become difficult to ignore.

Over the past five years, the S&P 500 Technology sector has accounted for more than a third of MSCI World’s returns and one of the key drivers has been excitement around artificial intelligence. While we are not tech investors, AI-driven capex from the large US tech companies has become a central driver of global power demand, and by extension, demand for electrical equipment and infrastructure. Developments in this space are now closely tied to our investment universe, which means we follow the hyperscalers and their investment plans closely.

The five largest US tech companies are expected to spend over USD 300 billion in capex this year, primarily on data centre infrastructure. For context, five years ago, the combined capex was less than USD 100bn. Using Microsoft as an example, in 2020 it spent about a quarter of its operating cash flow on capex, while it last year invested four times more than in 2020 as capex consumed almost 50% of operating cash flow. This year, capex is set to grow to above USD 80bn and consume about two thirds of expected operating cash flow. Obviously, this trend must turn at one point and investors are rightly asking whether these AI-driven investments will generate attractive returns, and to whom the value will accrue.

One emerging concern is software commoditization. With the rapid democratization of generative AI, it is not hard to imagine someone building alternatives to Microsoft Word or Adobe Photoshop with minimal resources. If this dynamic take hold, even companies with strong historical moats could see their pricing power eroded. Rapidly changing competition could even challenge large software ecosystems.

Another risk, which is somewhat interlinked, comes from Chinese competition. Tesla, long viewed as a frontrunner in EVs, is already overtaken by Chinese competitors on quality and price, and Apple is losing share in China to domestic brands like Huawei and Xiaomi. While these trends are most visible in consumer hardware, China’s ambitions go much further. The country is actively investing in semiconductors, quantum computing, and AI, areas where it has historically lagged.

Even before the recent introduction of higher tariffs on China, the last three US administrations have fought this trend by protecting its domestic market from Chinese competition and by restricting technology transfer from Western companies. This failed massively with regards Huawei, which was gradually cut off from Western technology from 2012 onwards. However, necessity is the mother of innovation, and the restrictions put on Huawei only increased its incentives to innovate. With R&D budgets almost matching the US tech giants, it is the market leader in telecom equipment having replaced western chips and software with newly developed Chinese IP. This technology is now offered around the world in competition with products and services from the US tech giants.

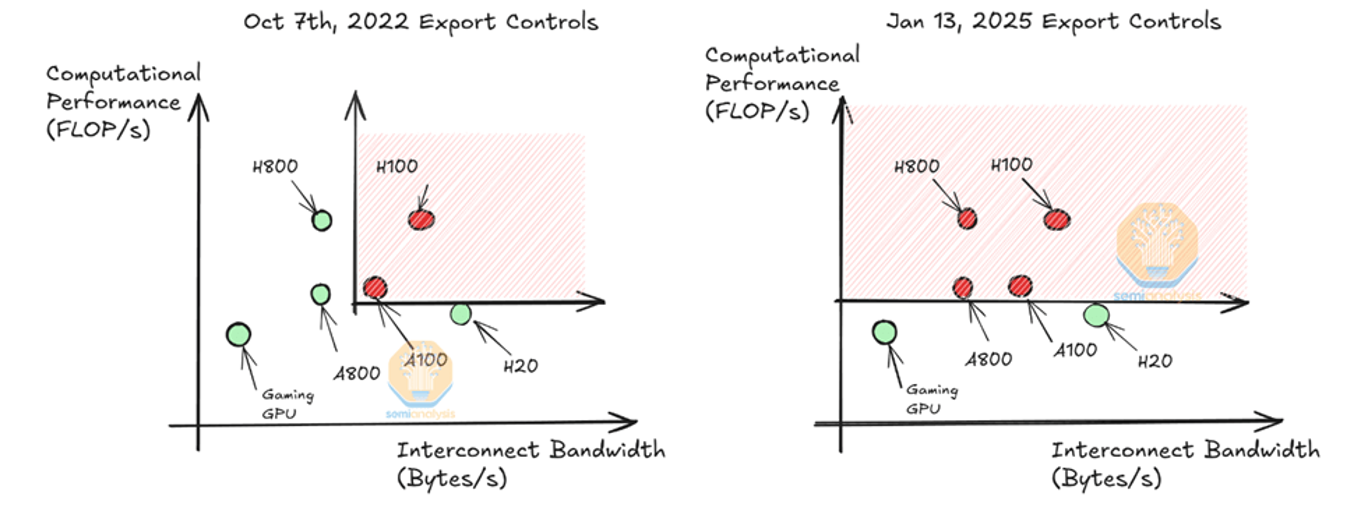

In that regard, we are particularly concerned about Nvidia, the world’s third most valuable company with a market cap of more than USD 2 trillion dollars. Today, Nvidia has a near-monopoly position in production of advanced GPUs required to train large AI models. US export controls have long sought to limit China’s access to high-performance chips, banning for example Nvidia’s A100 and H100 models and, later, even their modified H800 version. In response, Nvidia launched the H20, which complies with the FLOPS (Floating Point Operations) restrictions but comes with higher memory bandwidth which is of key importance in so-called reasoning tasks. As SemiAnalysis, a specialist consultancy, nicely depicts, the H20 excels when it comes to Interconnect Bandwidth. Many argue though that this is circumventing the spirit of the ban.

Source: Semianalysis.com

Despite the restrictions, roughly 11% of Nvidia’s last year’s revenues still came directly from China. In addition, it is an open secret that Singapore, a city of only 5.6m inhabitants and accounting for 18% of Nvidia’s last fiscal year calendar 2024 revenues, is a backdoor for its sale into China. Whether or not this ‘backdoor’ will be allowed to remain open, considering the brewing trade war, is an open question as the Trump administration has already hinted at tighter export restrictions. If so, almost a third of Nvidia’s sales might be a risk.

Furthermore, China is also mulling stricter energy efficiency requirements on chips used in data centres, a move that would disqualify Nvidia’s H20 chip which supposedly does not comply with the new rules. One might have expected China to have liked to acquire as many Nvidia chips as possible, but it seems like it has other more important long-term objectives, like self-sufficiency, regulatory leverage and market control and data security. Whether Chinese chips will be able to compete head on with Nvidia near-term is still uncertain, but we would not underestimate the Chinese’s technological ability over the long term. Who would have thought three years ago that Chinese EVs would overtake Tesla on quality? Moreover, considering China’s recent introduction of a 34% tariff on all import from the US, and assuming it remains, Chinese chips’ have suddenly narrowed the cost efficiency gap even further.

Moreover, the ‘Deepseek moment’ seems to have spawned the next level of competitiveness in the Chinese tech sector. Many western experts are starting to worry that Chinese AI ecosystems, optimized for Chinese chips could become both cheaper and easily accessible for the rest of the world. There is a real risk that global developers, especially in emerging markets, will pivot toward these models. In that scenario, US dominance of the AI stack could begin to erode.

While it is too early to decide if US tech dominance is really under threat, the roll-out of Generative AI has lowered the barriers to innovation globally and clusters like Silicon Valley could lose some of its edge. At the same time, the brewing trade war is hardly helpful. As the Trump administration is focused on taxing goods where the US has a trade deficit, the rest of the world might go after services where the US has large surpluses, partly due to services offered by US big tech.

What does it mean for our universe of companies? First, in our January investor letter, “DeepSeek and Its Impact on Power Demand,” we argued that valuations across the AI trade looked stretched and were due for a reset. That view has since been validated.

Second, it is uncertain how a potentially waning long-term US dominance in AI and tech impacts our electrification focused companies. However, as we described in our December-24 report, AI is only the icing on the cake for this universe. Even if the US should enter a recession, the grid still needs to be upgraded, and the trends of onshoring and industrial electrification will persist. Near-term data centre buildouts and rising power demand are real and visible. And while few of our positions are truly recession-proof, many of our long holdings benefit from strong market positions, solid balance sheets, and large clients likely to continue investing even through a downturn. Some may appear expensive in a recessionary context, but that risk is possible to hedge in a market full of weak-balance-sheet companies unlikely to survive a prolonged downturn.

Nevertheless, the brewing trade war is a major negative for the world economy. The S&P 500 is at the time of writing down almost 20% since peak but still trading on inflated valuation multiples considering that bottom-up earnings estimates have yet to be cut. Still, compared to the previous crises we have experienced; from the bursting of the internet bubble to the great financial crises, the euro crisis, Brexit and finally Covid, this is the only crisis caused single handedly by one man. Fortunately, this also means that one man can put an end to it.

We are confident that a de-escalation will eventually occur, but the timing is uncertain. Also, the longer it drags on, the greater the damage to the global economy. Uncertainty and high volatility are likely to prevail for some time and until we get more clarity, we continue to seek opportunities to take advantage of irrational price moves on both the long and the short side.

FUND PERFORMANCE – STRONG ABSOLUTE AND RELATIVE PERFORMANCE

The fund delivered strong returns of 3.5% in March, outperforming Russel 2000 and MSCI World Small Cap index by 10.5% and 7.6%, respectively.

The strong performance in March was broadly driven by four strategic decisions. First, we targeted tariff exposed stocks on the short side as we maintained our long-held view that Trump’s tariff threats are substantive, not merely a negotiation tactic to achieve other objectives. Second, following the Deepseek announcement in late January, we trimmed our net exposure to the AI power thematic, primarily by adding short positions in overvalued, short-cycle names with limited earnings upside. Third, we skewed the book towards Europe as Germany announced fiscal stimulus while the US signalled tighter government spending. Record-high US valuations relative to Europe at the beginning of the year further supported this move. Fourth, given heightened uncertainty around Trump’s policies, we reduced net exposure below our typical target range to mitigate potential market volatility.

The best performing theme in March was ‘Solar’, contributing 2.1% to NAV as tariff exposed shorts declined sharply. On top of tariff risk, most parts of the global solar equipment market, outside of the protected US market, are suffering from massive oversupply. This is only exacerbated by the fact that from the end of June, the Chinese government will be imposing limits on solar installations in China as the grid is overwhelmed by the new solar capacity. It is hard to see any improvement in pricing this year.

The funds sole long position in the solar theme, First Solar (FSLR) declined with the sector in March due to fear of repeal of the Inflation Reduction Act (IRA). However, the stock rallied and outperformed peers by double digits the day after Trump’s tariff announcement. As we have noted many times before, the stock would be a huge tariff winner with its vast domestic manufacturing capacity. If all stars align, FSLR has three potential positive near-term triggers. First, the announced reciprocal tariffs on South-East Asian countries are maintained on top of the already high anti-dumping and circumvention tariffs that was initiated during the Biden administration. Second, the manufacturing IRA tax credits that FSLR depends on survive the budget reconciliation. Third, the manufacturing tax credits are preserved, but Congress use Foreign Entity of Concern (FEOC) laws restricting tax credits to flow to entities with large Chinese shareholding. This would in fact block or restrict Chinese companies from running US manufacturing capacity. At the current FSLR valuation, if only one of these three outcomes come through, the stock would be a good buy at these levels.

The second-best performing theme was ‘Grid Owners’ which consists of European grid operators. We discussed this theme in prior months, but the gist is that these companies are allowed regulated returns on their capex. As investments in both transmission and distribution grids are set to increase significantly around Europe, the returns and thus earnings will grow with the increased investments. We expect the share prices to follow earnings growth and see limited downside and very good risk reward.

We increased our position in Elia (ELI BB) during the month as it finally executed on its long-awaited equity raise. EON (EOAN) also did well post the announcement of the German fiscal stimulus, where a significant part is expected to be allocated to the energy transition, to which the grid is the backbone.

Another theme that did well in March was ‘Wind’, adding 1.2% to NAV as Nordex (NDX1) performed on a combination of positive German sentiment and improved expectations of both strong order intake and improved margins in 2025 and 2026. Additionally, Germany, where NDX1 controls more than a third of the market and earns above average margins, is likely to be the most attractive onshore wind turbine market over the next years. We have traded around the position the last weeks but will be using the market panic to size up the position again.

The worst performing theme and the only one down more than 1% of NAV was ‘Diversified Energy’, which lost 1.8% of NAV in March. While the fund made good trading profit in the gas turbine names, Siemens Energy (ENR) and GE Vernova (GEV), this was overshadowed by the 25% drawdown in Chart Industries (GTLS). As far as we know, there were no company specific news, but the stock is levered and probably perceived to be a tariff loser with its global sales and operations. However, it has 64 manufacturing locations around the world and significant pricing power in many of its core products. The company has its roots in the oil service world though and despite limited oil exposure today, the stock often declines with the oil services sector when oil prices fall. These events have historically been a good buying opportunity, and we have been adding to the position.

Uncertainty remains elevated, the question is no longer if Trump’s tariffs will harm the economy, but rather how severely, and how far he will push before facing resistance. Trump responds only to strength, not weakness, and while we had hoped the Republican led Congress would find its backbone and do its constitutional duty to be a check on executive power, we are now rather expecting the financial markets to stand up to him and compel him to tone down his detrimental economic policies.

We remain cautious but will actively navigate volatility and trade the many likely bear markets in the coming months.

Thank you for your trust, and we look forward to updating you again next month.

Sincerely

Vidar Kalvoy & Joel Etzler

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

- Portfolio Manager and Founder of the Coeli Energy Opportunities Fund.

- Over 15 years of investment experience spanning both public markets and private equity.

- Managed the Coeli Energy Transition Fund from 2019 to 2023.

- Spent six years at Horizon Asset in London, a market-neutral hedge fund.

- Started working with Vidar Kalvoy in 2012.

- Five years in Private Equity at Morgan Stanley.

- Began his investment career in the technology sector at Swedbank Robur in Stockholm in 2006.

- Holds an MSc in Engineering from the Royal Institute of Technology (KTH), Stockholm.

- Portfolio Manager and Founder of the Coeli Energy Opportunities Fund.

- Has managed energy equities since 2006 and brings more than 20 years of experience in portfolio management and equity research.

- Managed the Coeli Energy Transition Fund from 2019 to 2023.

- Head of Energy Investments at Horizon Asset in London for nine years, a market-neutral hedge fund.

- Experience from energy investments at MKM Longboat in London and equity research in the technology sector in Frankfurt and Oslo.

- Holds an MBA from IESE in Barcelona and a Master’s in Business and Economics from the Norwegian School of Economics (NHH).

- Before entering finance, he served as a lieutenant in the Royal Norwegian Navy.

IMPORTANT INFORMATION. This is a marketing communication.

Before making any final investment decisions, please refer to the prospectus of Coeli SICAV II, its Annual Report, and the KID of the relevant Sub-Fund. Relevant information documents are available in English at coeli.com. A summary of investor rights will be available at https://coeli.com/financial-and-legal-information/.

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

Please note that the management company of the fund may decide to terminate the arrangements made for the marketing of the fund in one or multiple jurisdictions in which there exists arrangements for marketing.