This material is marketing communication.

Note that the information below describes the share class (I USD), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class return. The information below regarding returns therefore differs from the returns in other share classes.

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

1) Share Class I USD

Performance for other share classes towards the end of the report.

FUND MANAGER COMMENTARY

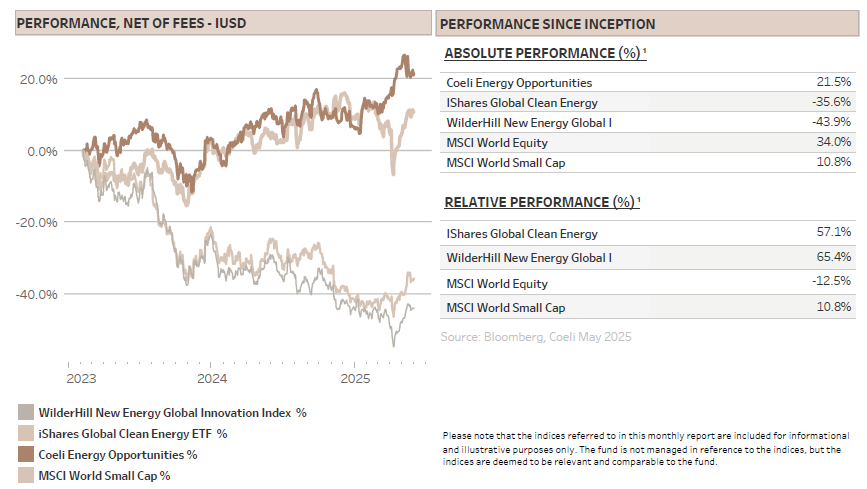

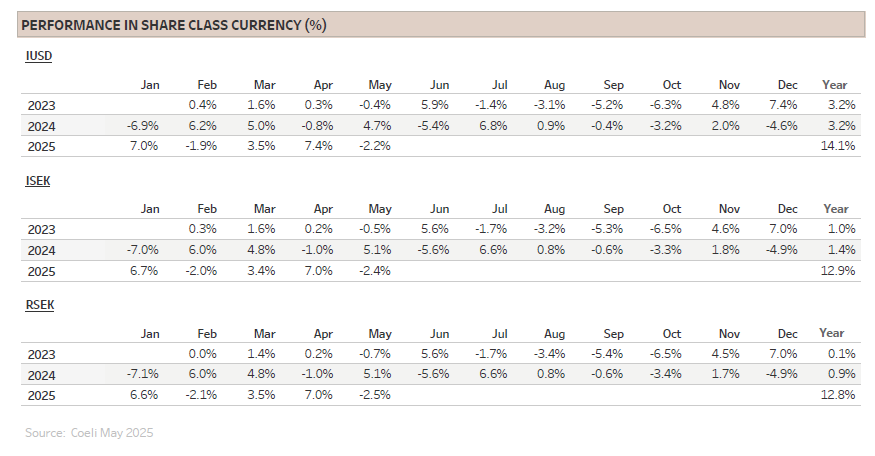

The Coeli Energy Opportunities fund lost 2.2% net of fees and expenses in May (I USD share class). Year-to-date, the fund is up 14.1% and it has gained 21.5% since inception in February 2023.

The fund underperformed the most comparable indices, the Wilderhill New Energy Global index (NEX) and the iShares Global Clean Energy (ICLN) by 9.9% and 9.8% in May. The year-to-date outperformance is 13% and 3%, and since inception the fund is ahead by 65% and 57%, respectively.

After a great start to the year, the fund underperformed in May, as our positioning at the beginning of the month was too cautious for the rally that followed the tariff de-escalation between China and the US. As we wrote in last month’s report, we expected President Trump to continue to ‘blink’ or ‘chicken out’ (Trump Always Chicken Out - TACO) and we argued that a reduction in tariffs between the US and China was inevitable as the punitive rates effectively acted as a trade embargo. Still, the scale of the de-escalation and the 90-day pause took both us and the broader market by surprise, fuelling the rally.

Nevertheless, the main reason for May’s underperformance was the ‘Solar’ theme which detracted 5.4% of NAV. We, along with most investors, were surprised, if not outright blindsided, when the US House of Representatives presented its first draft of the budget reconsolidation bill with relatively small cuts to tax credits for solar companies. It was widely believed that the first draft would be the harshest, so the unexpectedly benign proposal triggered a significant rally in solar stocks, for which the fund was not well positioned. The fund lost 3.2% on the day which coincided with the de-escalation in the US/China tariff war. However, thanks to swift repositioning and trading, we recouped those losses and more the following day, ending up 4.3%. Unfortunately, our concern that this was too good to be true was validated when the final bill from the House, released a few days later, included substantial cuts, forcing us to unwind some trades and lock in some losses, negatively impacting this month’s performance. However, with the knowledge of what the fiscal hawks in the House are willing to accept as the bill moves to the more moderate Senate gives us confidence in our solar positioning over the coming weeks and potentially months. We discuss the details further in this report.

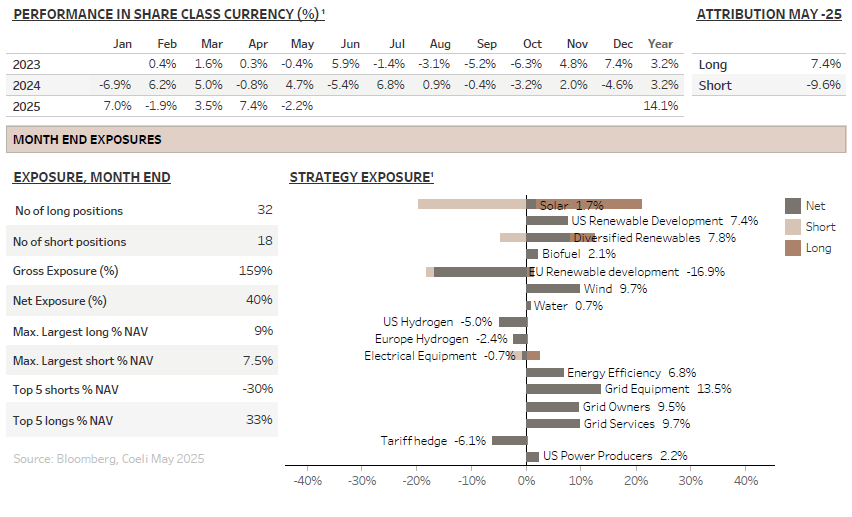

Despite the negative monthly performance, the majority of our 16 investment themes posted gains for the month. The best performers, benefitting from renewed momentum in the powering AI trade, were ‘Grid Services’ and ‘Grid Equipment’, adding 2.1% and 1.6% to the NAV, respectively. Overall, long positions contributed 7.4%, while shorts lost 9.6% as several solar shorts squeezed. We began May with a net exposure in the low 20%, which we increased to low 40% as the tariff war de-escalated and the first draft of the reconciliation bill was released.

As we noted last month, we remain concerned that the market is underestimating the economic damage caused by ongoing tariff uncertainty. However, we recognize that it might take longer for these effects to be reflected in fundamentals and for stocks to adjust accordingly. We ended the month with a net and gross exposure of 40% and 160%, respectively.

MARKET COMMENT – DOES TRUMP ALWAYS CHICKENS OUT?

The S&P 500 rose 6.2% in May and is now flat for the year, recovering all the losses from the 18% slump in early April when Trump initiated his tariff war. ‘Sell in May and go away’ has rarely been this wrong as the index posted its best May return since 1990. Although Europe’s Stoxx 600 underperformed the S&P 500 for the first time this year, its 4.0% gain was still the best May in over 20 years.

Several drivers drove the strong performance. First, sentiment improved as US-China tariffs de-escalated and a trade deal was announced with the UK. Second, reduced trade war risk lowered recession fears and lifted forward-looking consumer confidence indicators, which had been flashing red in April. Meanwhile, tariffs have yet to appear in hard economic data. Third, S&P 500 earnings grew 12% year-over-year in the first quarter, beating consensus expectations of 6% growth and surpassing early January forecasts by 2.5%. Finally, the market adopted the “TACO” view - Trump Always Chickens Out - believing that extreme tariff threats are negotiating tactics that will be quickly reversed if markets react poorly.

Looking ahead, about a month remains before the 90-day grace period for reciprocal tariffs expires in the second week of July. Trade deals have been scarce, and we expect more tariff noise and uncertainty as the deadline approaches. While Trump threatened the EU with 50% tariffs, announced and delayed within days in late May, most countries have been asked to submit their best offers on tariff reductions, quotas, and non-tariff barriers, aiming to conclude all deals by early July. The fact that these reciprocal tariffs were deemed illegal by the US Court of International Trade (CIT) is unlikely to incentivise countries to submit ‘their best offers’ right away. However, the risk is that some countries, most likely US allies that can be bullied, will be made examples off.

China and the EU are less likely to be pushed around, though. China faces its own trade deal deadline in mid-August, but negotiations are progressing slowly. Given the US goal of weakening China as a global competitor, an extension of the deadline with current reduced tariffs is likely the best case. For the EU, few expect tariffs to reach the threatened 50%, but to illustrate what is at stake; Goldman Sachs believes this would reduce EU export to the US by more than half and reduce EU GDP by up to 1.7%, likely triggering a recession. Although the EU is unlikely to be offered similar terms as the UK, we are not convinced that the EU would easily accept even these terms without introducing some reciprocal tariffs on US imports.

In summary, more tariff turmoil is likely, and markets may be too complacent assuming that President Trump is all bark and no bite. While we have long believed Trump would avoid risking a recession or financial crisis ahead of next year’s midterms, he appears determined to force manufacturing back to the US to create blue-collar jobs and more importantly, the US needs the revenues from tariffs.

Notably, tariff revenues from executive actions are excluded from Congress’s budget calculations. However, the Republican led Congress is openly assuming that the bond market will factor in these revenues when it argues the budget will not increase the deficit and add to the national debt. Clearly, expected tariff revenues are already part of the US strategy to balance its books to avoid further spending cuts or tax hikes.

RENEWABLE ENERGY – CLEAR WINNERS AND LOSERS EMERGING IN SOLAR

Readers of our monthly reports know that the fate of the Inflation Reduction Act (IRA) is critical for renewable energy stocks. Uncertainty over its survival, especially since Trump took the lead in the polls last summer, has made some renewable energy tech segments, including solar, almost uninvestable. Now, with the Republican-controlled Congress nearing agreement on the so-called “One Big, Beautiful Bill,” which includes IRA cuts, we are approaching the risk-clearing event we have long awaited.

We were caught off guard and the fund underperformed when the first House draft was substantially better than expected for most renewable energy tax credits. Although the final bill included substantially more cuts to tax credits, we now believe uncertainty has been substantially reduced for most solar segments.

Below we briefly summarize the most important changes to tax credits relevant for solar and our portfolio. This is not a comprehensive review of all credits.

45X: Better Than Feared, Crucial for Onshoring

The Advanced Manufacturing Production Credit (45X), created by the IRA in 2022, incentivizes domestic production of clean energy components. Ironically, most new plants were built in Republican states, which may help explain why this credit survived almost unchanged with only a one year earlier phase down. This is great news for US manufacturers, especially First Solar (FSLR), our only long-term solar holding since Trump’s election. If the Senate changes anything, it will likely be to delay the phase-down again. FSLR remains the biggest IRA winner and benefits further from Trump’s tariffs on global imports, especially China, as FSLR sources most inputs domestically and avoids Chinese-made polysilicon.

PTC / ITC: Front-Loaded Demand, Medium-Term Noise

The Clean Electricity Investment Tax Credit (ITC) and Production Tax Credit (PTC) have been around in some form for decades and were both enhanced by the IRA. For example, ITC allows most clean energy projects a 30% tax credit, potentially rising to 60% with domestic content or other adders, and was originally available through at least 2032. The first House draft accelerated the phase-out to start in 2029 and end in 2031, but the adders survived. The final bill was harsher, projects must now be in service by the end of 2028 and construction commenced within 60 days of the bill’s signing. This will be tough for smaller developers, but large players like Nextera Energy (NEE) and AES, both in our portfolio, should manage, having already safe harboured projects into 2027. Moreover, there are strong signals that the Senate will moderate the phase-out. In any case, this will likely pull forward demand and trigger a construction boom over the next two years, benefiting developers and EPCs like Quanta(PWR) and Mastec (MTZ), both portfolio holdings in ‘Grid Services’.

FEOC: The Silent Killer in the Fine Print

Unfortunately, the frontloading of demand described above can be hampered by the House’s Foreign Entity of Concern (FEOC) language, which aims to block not only Chinese-owned companies from US tax credits but also any project using Chinese components, a near-impossible standard today, though it would be a major tailwind for FSLR.

However, given the US’ AI race with China and power being one of the key constraints, we expect the Senate to soften the FEOC language and phase in restrictions over several years. Nevertheless, Chinese companies will likely be squeezed out of the US market, essentially their only profitable market. We remain short Chinese solar stocks with US manufacturing exposure.

Residential Solar: Roller Coaster Off the Tracks?

Republicans have never favoured residential solar, seeing it as a subsidy for wealthy homeowners. The House initially claimed to remove this subsidy, saving about USD 77bn over 10 years, but it only cut credits for direct ownership, leaving leased solar systems still eligible for 30-40% tax credits. As leasing already accounts for over 50% of the market, we anticipated this would quickly approach nearly 100%, making the actual savings much smaller than intended. Nevertheless, as we expected the first draft to be the worst, we adjusted our positions when direct-ownership-focused companies sold off and leasing specialists rallied.

However, the House addressed this “loophole” in the final bill, explicitly making leasing systems ineligible as well, continuing the rollercoaster for residential solar stocks. Unfortunately, the text was written in haste and introduced a new error that still allows leasing to qualify for tax credits. We expect the Senate to correct this issue, and we do not expect Senate Republicans to push to retail the subsidy. If residential solar loses tax credits at year-end, expect a rush of installations followed by a 50–70% demand slump over the next years. We believe this risk is not fully priced into US-focused residential solar stocks.

Outlook: Policy Volatility, Structural Tailwinds

Regardless of the final cuts to the IRA, we see this as a clearing event for solar stocks, making the sector investable again. Moreover, the bigger picture is that this is not just about solar, it is about US energy policy in the age of AI. If the US wants to win the AI arms race, it cannot afford to slow solar deployment or remove manufacturing tax credits. We believe these realities will ultimately shape the legislative outcome.

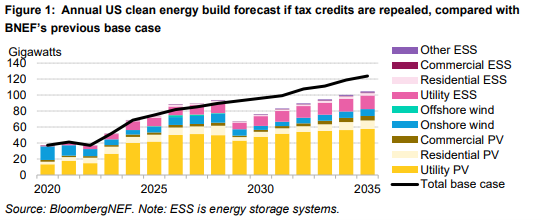

What if our assumption is incorrect and the Senate does not reverse some of the cuts outlined above? Bloomberg New Energy Finance has estimated demand for solar, wind and batteries (ESS) through 2035, based on the scenario where the House bill passes the Senate unchanged. As illustrated in the graph below, demand is expected to accelerate through 2028, followed by a sharp fall across most sub-sectors in 2029. Notably, utility-scale solar is projected to rebound relatively quickly from 2030 onwards. Furthermore, even though utility-scale solar installations are expected to dip in 2029, we expect FSLR to remain sold out as it continued to benefit from a tariff advantage over foreign-produced solar panels.

By 2029 however, the US will have a new administration that could have a very different view of the importance of renewable energy. Considering the expected strong growth in power demand and the time it takes to build alternative power like nuclear and gas power plants, we would not be surprised if new subsidies will be made available in some shape or form.

We continue to prefer utility-scale stocks, with FSLR as our largest position. We have also added a significant stake in Nextracker (NXT), the leading tracker provider for utility-scale projects, and maintain smaller positions in other utility-scale names. We remain net short residential solar companies and Chinese panel makers listed in the US, while staying long renewable developers like NEE and AES, as we see AI-driven power demand expectations increasing.

We will continue to monitor the bill’s progress in the Senate and provide updates as the situation evolves.

FUND PERFORMANCE - SOLAR WEAKNESS DRIVE UNDERPERFORMANCE

The fund declined 2.2% net of fees and expenses in May, underperforming both the broader market and the main renewable energy indices. As previously discussed, this underperformance was primarily due to overly cautious positioning at the start of the month and significant volatility in solar stocks, resulting in a 5.4% loss within the ‘Solar’ theme.

At the beginning of May, the fund was net short in ‘Solar’, with First Solar (FSLR), the fund’s largest position, being the primary long holding. This substantial position reflected our conviction that FSLR would ultimately emerge as the biggest winner from the Inflation Reduction Act (IRA) and was best positioned to benefit from increased tariffs. FSLR also served as a hedge against shorts in residential and Chinese solar stocks, which we expected to underperform due to changes to the IRA and heightened tariffs.

However, the first draft of the House budget reconciliation bill was unexpectedly positive for the sector, especially for residential solar, prompting us to shift to net long by covering and buying residential solar names and increasing exposure to utility-scale solar stocks. Unfortunately, the final bill proved far more restrictive than the first draft, leading to sharp declines in both residential and utility-scale solar stocks. Despite these setbacks, we increased our utility-scale positions further as the priorities of House Republicans became clearer, while accepting losses in residential solar.

The strongest contributors in May were the ‘Grid Equipment’ and ‘Grid Services’ themes, which together added 3.7% to NAV. These gains were partly driven by renewed optimism around the accelerating AI-related power demand. Although we have been concerned about hyperscalers potentially scaling back data centre investments, there is still little evidence of such a pullback. Instead improving expectations for returns on these investments continue to support positive momentum in the sector.

‘Diversified Renewables’ was the third-best performing theme, contributing 0.7% to NAV despite being net short into a market rally. This was largely due to robust performance from Siemens Energy (ENR) and Chart Industries (GTLS), which rose 26% and 16% respectively in May. We remain particularly optimistic about ENR, which continues to deliver strong earnings momentum, especially in its gas turbine business. Since the beginning of 2024, consensus EPS expectations for 2026 have more than doubled, and we see further upside potential versus consensus for 2028.

For GTLS, we are taking a more cautious approach following its recently announced merger of equals with Flowserve (FLS). While FLS is a high-quality company, we question the timing of the merger. GTLS was on track to meet its leverage target this year and we believe this alone would have lifted the valuation. Also, FLS’s growth prospects and margins are lower. On the other hand, FLS’s low debt profile means the combined company will be deleveraged and able to pay dividends after the expected close in the fourth quarter. Additionally, more than half of FLS’s revenues come from aftermarket services, which should help stabilize GTLS’s more cyclical business and potentially boost the valuation multiple. Notably, the two companies generated a combined USD 1.8 billion in cash flow over the 12 months from Q2/24 to Q1/25. With an enterprise value of USD 18 billion, this is not expensive, especially as both companies are growing, targeting USD 300 million in cost synergies and 2% revenue synergies. We continue to digest the merger as we conduct further due diligence on FLS.

Looking ahead, while the ongoing tariff conflict introduces uncertainty, recession risk appears to have receded and US earnings are stable, at least for now. The removal of the most punitive tariffs has helped stabilize risk assets and improved risk appetite, which should continue to support equities in the near term. On the other hand, with the S&P 500 nearing last year’s all-time highs while earnings forecasts remain subdued, valuations are at historically elevated levels and market risk premiums are near record lows.

We aim to remain nimble and adjust the portfolio during these volatile times. Structural tailwinds, particularly from AI-driven power demand, will continue to shape the opportunity set for us and remain core to the strategy.

Thank you for your continued trust, and we look forward to updating you again next month

Sincerely

Vidar Kalvoy & Joel Etzler

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

- Portfolio Manager and Founder of the Coeli Energy Opportunities Fund.

- Over 15 years of investment experience spanning both public markets and private equity.

- Managed the Coeli Energy Transition Fund from 2019 to 2023.

- Spent six years at Horizon Asset in London, a market-neutral hedge fund.

- Started working with Vidar Kalvoy in 2012.

- Five years in Private Equity at Morgan Stanley.

- Began his investment career in the technology sector at Swedbank Robur in Stockholm in 2006.

- Holds an MSc in Engineering from the Royal Institute of Technology (KTH), Stockholm.

- Portfolio Manager and Founder of the Coeli Energy Opportunities Fund.

- Has managed energy equities since 2006 and brings more than 20 years of experience in portfolio management and equity research.

- Managed the Coeli Energy Transition Fund from 2019 to 2023.

- Head of Energy Investments at Horizon Asset in London for nine years, a market-neutral hedge fund.

- Experience from energy investments at MKM Longboat in London and equity research in the technology sector in Frankfurt and Oslo.

- Holds an MBA from IESE in Barcelona and a Master’s in Business and Economics from the Norwegian School of Economics (NHH).

- Before entering finance, he served as a lieutenant in the Royal Norwegian Navy.

IMPORTANT INFORMATION. This is a marketing communication.

Before making any final investment decisions, please refer to the prospectus of Coeli SICAV II, its Annual Report, and the KID of the relevant Sub-Fund. Relevant information documents are available in English at coeli.com. A summary of investor rights will be available at https://coeli.com/financial-and-legal-information/.

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

Please note that the management company of the fund may decide to terminate the arrangements made for the marketing of the fund in one or multiple jurisdictions in which there exists arrangements for marketing.