This material is marketing communication.

Note that the information below describes the share class (I USD), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class return. The information below regarding returns therefore differs from the returns in other share classes.

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

1) Share Class I USD

Performance for other share classes towards the end of the report.

FUND MANAGER COMMENTARY

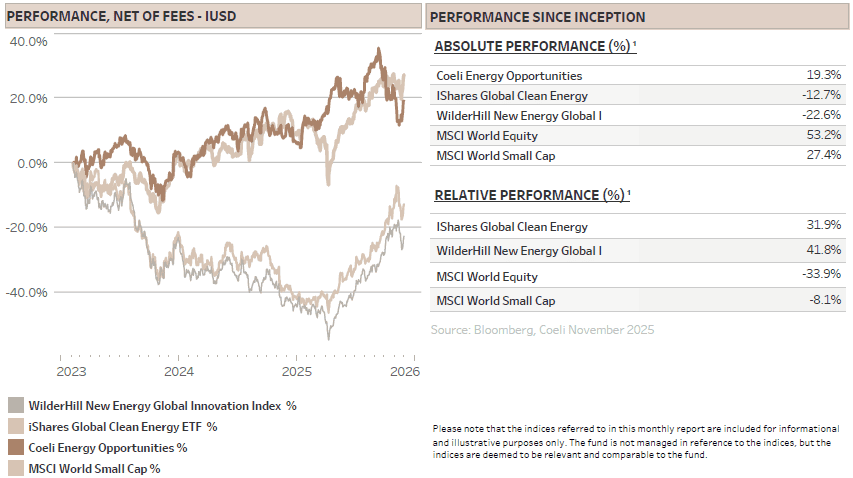

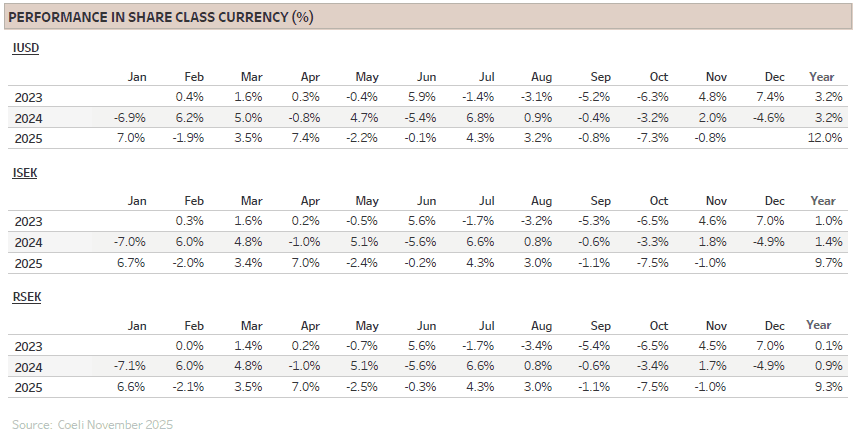

The Coeli Energy Opportunities fund lost 0.8% net of fees and expenses in November (I USD share class). Year-to-date, the fund is up 12.0% and has gained 19.3% since inception in February 2023.

The fund outperformed its most comparable indices, the Wilderhill New Energy Global index (NEX) and the iShares Global Clean Energy (ICLN) by 3% and 1%, respectively, in November. Year-to-date the fund is underperforming the NEX by 28% and ICLN by 39%, while since inception the fund remains ahead by 42% and 32%, respectively.

November was another volatile month for the markets and the fund. The meme rally that caused significant losses in September and October peaked in mid-October and continued to gradually unwind through November. As a result, the ‘US Hydrogen’ theme was the best performer, contributing 2.3% to NAV, recovering part of the earlier drawdown. Unfortunately, the short squeeze in some China related solar stocks persisted into November, peaking mid-month. Combined with weak performance in certain long utility scale solar positions, the ‘Solar’ theme detracted 3.7% of NAV. This was the only major losing theme in a month when roughly half the themes generated positive returns.

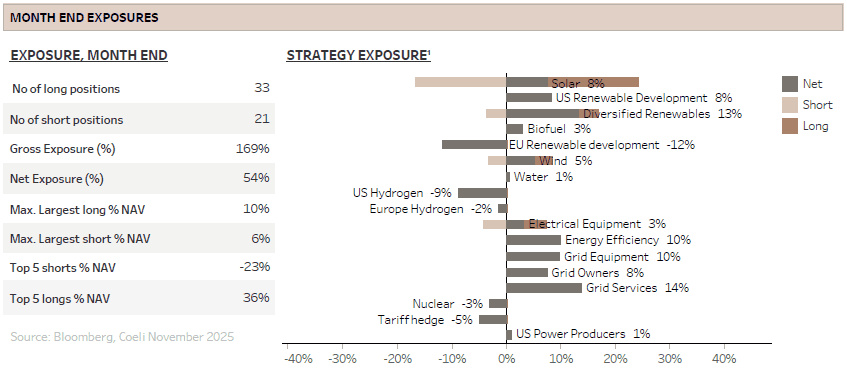

While the meme bubble continued to deflate, the powering AI thematic also took a breather despite hyperscalers increasing capex guidance and reiterating optimism on AI opportunities. This led to the first negative month since March for ‘Diversified Renewables’, a theme skewed long with Siemens Energy (ENR), Bloom Energy (BE) and bitcoin miners. The theme detracted 0.5% from NAV, while other powering AI related themes were mixed. In aggregate, long positions contributed -0.8% to performance while shorts were flat. At month-end, overall net and gross exposures stood at 54% and 169%, respectively.

MARKET COMMENT – FED TURNED THE MARKET

The S&P 500 rose +0.1% in November, marking its seventh consecutive monthly gain despite a mid-month drawdown of 4.5%. S&P 500 Equal Weight Index gained 1.9%, while the Nasdaq declined as much as 4.5% amid renewed concerns of an AI bubble. Russel 2000, representing small cap stocks, increased 0.8%, rebounding from an 8.5% drawdown after the FED signalled that a December rate cut remained likely.

One of the most influential market drivers during the month was the expectation of a Fed rate cut in December. Following Chair Powell’s late-October comment that a rate cut was “far from a foregone conclusion,” several Fed governors reinforced that view, pushing market-implied odds of a cut below 30%. However, just before the Fed’s pre-meeting blackout period, one of Powell’s closest allies on the Board made remarks suggesting that a cut was likely. This was widely interpreted as an indication of Powell’s own position. Equity indices promptly bottomed and rallied into month-end as markets once again priced in a near-certain December cut. Nevertheless, a hawkish cut could still pose a risk to December’s traditional Santa rally, particularly if dissent within the Board is strong.

As highlighted in our September-2025 report, “Are we in an AI bubble?”, the dominant macro driver remains AI-related spending and return expectations on those investments. AI capital expenditure continues to underpin both GDP growth and equity markets. Back in September, we noted that the market was still in the “easy phase”, where greater AI spending automatically led to higher extrapolated revenues and profits, pushing valuations higher. We now could be entering the next and more challenging phase, where investors increasingly focus on returns from these substantial investments. We believe this transition could result in heightened volatility for the market and greater dispersion among winners and losers.

BATTERY ENERGY STORAGE IS BOOMING IN OIL COUNTRY – BUT IS IT A GREAT INVESTMENT?

In no other region is data centre expansion as evident as in Texas. Demand is surging, and if every data centre currently requesting grid connection were approved, Texas would add 78GW of capacity by 2030, a staggering figure that, at full utilization, would represent nearly 700 TWh of annual power demand, a 50% increase on the entire state's 2024 consumption.

Obviously, this will not materialize. Insufficient power generation, grid connections and natural gas pipeline capacity will constrain growth. However, it reveals two critical insights: First, the Electricity Reliability Council of Texas (ERCOT), the grid operator, attracts substantial data centre demand through its “energy only” market structure and business-friendly regulatory set-up. Second, the interconnection queue contains numerous speculative data centre projects that will likely never be built.

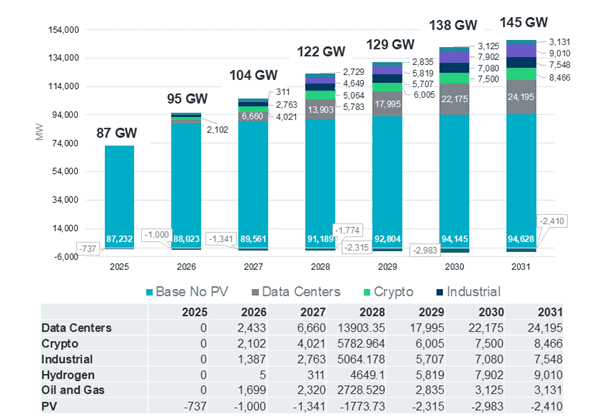

Digging deeper, ERCOT has calculated a more realistic scenario filtering out speculative projects. As shown in the table below, it estimates an "adjusted" large load forecast of 22 GW of incremental data centre demand by 2030. This is still a massive figure, representing more than 40% of all of Sweden's total annual consumption. It also signals a significant acceleration: ERCOT is forecasting a CAGR of 9.7% between 2025-2030, more than double the historical 4.3% CAGR during 2002–2024.

Source: ERCOT “Adjusted Large” Load Breakdown - cumulative

How will the market provide this volume of incremental power in such a short timeframe? We have in previous monthly reports explored various options for powering data centres, but renewables, like solar and wind, will be essential due to their rapid deployment and low cost. However, intermittent renewables combined with data centres featuring fluctuating, unpredictable power demand will require substantial storage to balance supply and demand. Battery Energy Storage (BESS) represents a key solution, as evidenced by the interconnection queue: 165GW of BESS projects are currently requesting grid connection in ERCOT. This is nearly three times more than the second largest US electricity region. Everything is indeed bigger in Texas.

Returns have historically disappeared quickly

BESS technology has existed for years, but early deployments profited substantially from ancillary services, i.e. specialized grid-stabilization functions. In ERCOT during 2018–2021, ancillary services comprised 70–80% of BESS revenues, with payback periods often under 2 years. Those days are gone. Market saturation has collapsed revenues, and this segment no longer justifies new investment.

While BESS systems are often optimized for specific applications, they can serve multiple functions, especially in ERCOT’s “energy only” market where high price volatility creates opportunities to charge during low-price periods and discharge during peaks. However, increased demand has triggered more supply, eroding arbitrage profitability, leaving developers with thin margins.

Additionally, rapid battery cost declines have spurred deployments that now pressure older, higher-cost systems. A battery installed two or three years ago struggles to compete with newer, cheaper alternatives in the same bidding environment, regardless of supply-demand dynamics. This compounds valuation and return risk unless backed by long-term contracts.

If returns are poor, why are developers expanding BESS?

Several factors explain continued investment. First, many BESS systems paired with solar are sold under long-term Power Purchase Agreements (PPAs), providing revenue certainty. Second, accelerating power demand may unlock previously unprofitable market segments. Third, new batteries placed Behind-The-Meter (BTM), discussed in our October 2025 report, "Bring Your Own Power: How the Data Center Is Rewiring the Grid" avoid competing with grid-scale systems.

Grid Constraints – How batteries enable data centre growth

We have long argued and believe it is now widely understood that grid capacity and power are the primary bottlenecks for AI expansion. We discussed this in our reports from March-24 “Roadblocks on the AI highway”, November-24 “The urgency to secure power” and April-25 “Power without wires – Why the grid is the real bottleneck”.

Moreover, grid operators overwhelmed by interconnection requests, are increasingly demanding that data centre developers bring their own power and reduce power demand during peak hours. Senate Bill 6 (SB6), recently enacted in Texas, is focused on this topic. The regulation requires the ability to curtail non-critical loads during grid emergencies, in return accelerating interconnection approvals for projects equipped with backup power such as BESS, diesel or gas generators. We expect to see more of this kind of regulation across the US.

Interestingly, while hyperscalers publicly commit to demand curtailment, regulatory filings reveal they continue seeking full operational flexibility. We anticipate significant developments on this front. Ultimately, data centers will need to implement peak-hour demand response to secure grid connections and sustain AI expansion. BESS will be critical to enabling this flexibility, allowing data centres to operate continuously while temporarily relieving grid strain.

Tax credits and domestic competitive advantage

Tax credits play a critical role in renewable energy and battery development economics. While solar and wind credits were curtailed, BESS emerged as a “winning” technology in the updated One Big Beautiful Bill Act (OBBBA). This was likely due to its grid-stabilisation importance and its perceived distance from the “green energy scam” narrative. As a result, BESS developers can claim Investment Tax Credits (ITC) through 2035 and US battery manufacturers can claim manufacturing credits through 2032.

However, new rules around Foreign Entities of Concern (FEOC) and Prohibited Foreign Entities (PFE) introduced more complexity. While Chinese manufacturers offer the lowest costs, they cannot claim US manufacturing tax credits. Additionally, battery project developers must meet the “domestic content cost ratio” for ITC eligibility: 55% of project costs from non-PFE sources for construction beginning in 2026. This requirement tightens by 5% every year. Consequently, Chinese owned battery factories established in the US under the Biden-era Inflation Reduction Act will require new ownership structures. Yet, the pending FEOC guidelines create significant uncertainty, delaying transactions and complicating battery integrators tax credits eligibility.

How material are the tax credits in the cost calculation? Chinese imported BESS, such as those from Contemporary Amperex Technology (CATL), the world’s largest battery supplier, costs approximately USD130/kwh, by our numbers. Domestically produced batteries price closer to USD200/kwh. However, once FEOC guidelines are finalized, project developer will receive at least 30% ITC on the USD200/kwh capital cost, while domestic manufacturer should qualify for an additional USD45/kwh. Combined, this takes the domestic alternative from a USD70/kwh price disadvantage to a USD35/kwh price advantage, at least until Chinese manufacturers further reduce costs.

Key US domestic players include Tesla (TSLA), already the largest domestic supplier, planning to add 50 GWh (more than double current domestic capacity). Fluence (FLNC), another battery integrator, is developing a FEOC-compliant supply chain, potentially with its Chinese cell supplier AESC. Since its year low, the stock has increased more than fivefold, largely on expectations of domestic advantage amid AI-driven battery demand.

While the fund holds no positions in these companies, we monitor developments closely. A significant risk we identify is that domestic suppliers may become cost-uncompetitive in some years, even before the tax credits run out as Chinese manufacturers likely continue to lower costs and make batteries more efficient.

Why we favour developers over manufacturers

We are optimistic on battery deployment, particularly in ERCOT, where data centre growth and market design create ideal storage conditions. However, we currently avoid pure-play battery manufacturers and integrators. China's dominance and cost leadership make long-term competitiveness for US cell factories uncertain. Instead, we favour companies developing solar-plus-storage projects that sell PPAs to hyperscalers, or those benefiting from the volume work of installing and integrating systems into the grid.

FUND PERFORMANCE – MEME RALLY DEFLATES AND AI BUBBLE FEAR INTENSIFY

November's -0.8% performance was driven entirely by the long book, while short positions were flat. The longs were pressured by heightened concerns over an AI valuation bubble, despite robust capex guidance from the hyperscalers. Market focus is gradually shifting toward expected returns on AI investments, increasingly important since a substantial portion of this capex will need to be financed through credit markets. On the short side, while some meme stocks in the hydrogen space peaked in October and have since fallen 40-70%, several solar names only peaked in November, resulting in losses that were not fully offset by other short positions.

‘US Hydrogen’ was the month's best performing theme, contributing +2.3% to NAV. These stocks have experienced significant declines as the narrative of green hydrogen powering data centres has largely faded from social media discourse. The fact that many of these companies took advantage of the hype to raise new equity, significantly diluting shareholders, was not well received. While additional capital extends their runway, the gap between capital burn and potential revenues remains so large that we view this favourably: it increases short opportunity and reduces squeeze risk.

‘Nuclear’ was the second-best performer, adding +1.1% to NAV. This theme is short-biased, not because we doubt nuclear’s important role in the energy transition, but because valuations are irrational given the industry's structural challenges. We detailed these issues in our June 2025 monthly report, "Nuclear Energy – Is a Bubble Brewing?"

‘Energy Efficiency’ claimed the third spot, contributing +0.8% to NAV. This is a pure long theme concentrated in European construction-exposed companies. After several months of underperformance, these stocks rallied on improving odds of peace in Ukraine and approaching deployment of German fiscal stimulus. Most holdings also reported solid third-quarter order intake, supporting our thesis that growth is improving and valuations remain attractive.

The standout losing theme was "Solar," which detracted -3.7% from NAV. As noted in last month's letter, the meme rally migrated to US-listed Chinese solar stocks in October and did not peak until mid-November. Despite key holdings declining more than 30% from peak, we crystallized some losses early in the month due to risk management. We remain short this space and see significant fundamental downside ahead.

The Solar theme was further pressured by weakness in utility-scale solar stocks, where we maintain a long exposure. While utility-scale remains the preferred solar subsector, there are some clouds on the horizon. We addressed several of these challenges (Section 232 tariffs, AD/CVD duties, FEOC regulation, and permitting delays) in our July 2025 report, "Solar Energy – Trump's War on Wind and Solar Continues." Clarity on these issues has taken longer than anticipated, but decisions over the coming quarters could substantially raise costs and create material supply shortages relative to underlying demand.

However, power prices are rising across most US regions, partly driven by soaring demand from AI data centres, now a politically sensitive topic. President Trump campaigned on three simultaneous objectives relevant to us: (1) winning the AI race with China, (2) lowering energy costs, and (3) dismantling the "Green scam." Logically, only two of these three are achievable at the same time. With midterm elections less than a year away, we believe rising power costs may compel the Trump administration to moderate its stance on renewables, at least on solar, which is the only energy source deployable at scale in a short time frame.

Looking ahead to year-end and into 2026, while we believe the meme rally's peak is behind us, a December Fed cut and potential Santa rally suggest some momentum may persist. We remain cautious about aggressively scaling shorts until this opportunity fully exhausts. Simultaneously, while we remain bullish on AI's transformative impact on productivity and society, equity valuations are elevated, and even minor ambiguity about AI triggers noticeable market dislocations. We continue to identify quality hedges within the Powering AI complex and are positioning for the next cycle of this trade.

Thank you for your continued trust and confidence. We look forward to updating you next month.

Sincerely

Vidar Kalvoy & Joel Etzler

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

- Portfolio Manager and Founder of the Coeli Energy Opportunities Fund.

- Over 15 years of investment experience spanning both public markets and private equity.

- Managed the Coeli Energy Transition Fund from 2019 to 2023.

- Spent six years at Horizon Asset in London, a market-neutral hedge fund.

- Started working with Vidar Kalvoy in 2012.

- Five years in Private Equity at Morgan Stanley.

- Began his investment career in the technology sector at Swedbank Robur in Stockholm in 2006.

- Holds an MSc in Engineering from the Royal Institute of Technology (KTH), Stockholm.

- Portfolio Manager and Founder of the Coeli Energy Opportunities Fund.

- Has managed energy equities since 2006 and brings more than 20 years of experience in portfolio management and equity research.

- Managed the Coeli Energy Transition Fund from 2019 to 2023.

- Head of Energy Investments at Horizon Asset in London for nine years, a market-neutral hedge fund.

- Experience from energy investments at MKM Longboat in London and equity research in the technology sector in Frankfurt and Oslo.

- Holds an MBA from IESE in Barcelona and a Master’s in Business and Economics from the Norwegian School of Economics (NHH).

- Before entering finance, he served as a lieutenant in the Royal Norwegian Navy.

IMPORTANT INFORMATION. This is a marketing communication.

Before making any final investment decisions, please refer to the prospectus of Coeli SICAV II, its Annual Report, and the KID of the relevant Sub-Fund. Relevant information documents are available in English at coeli.com. A summary of investor rights will be available at https://coeli.com/financial-and-legal-information/.

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

Please note that the management company of the fund may decide to terminate the arrangements made for the marketing of the fund in one or multiple jurisdictions in which there exists arrangements for marketing.