This material is marketing communication.

Note that the information below describes the share class (I USD), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class return. The information below regarding returns therefore differs from the returns in other share classes.

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

1) Share Class I USD

FUND MANAGER COMMENTARY

The Coeli Renewable Opportunities fund generated a profit of 0.3% net of fees and expenses in April. It is up 2.3% since the inception on February 6, 2023.

The fund has outperformed the most relevant reference indices, the Wilderhill New Energy Global index (NEX) by 14.8% and the iShares Global Clean Energy (ICLN) by 10.1% since inception. During April, which was the second full month of operations, the fund outperformed the NEX and ICLN by 6.2% and 5.8%, respectively.

Although we are pleased with the relative performance, April ended poorly with a large drawdown as the solar space sold off into the month end. Still, our ‘Solar’ theme, which is skewed long, only deducted 1.2% of the monthly performance while the TAN index (Invesco Solar ETF), the main solar ETF, declined by more than 7%.

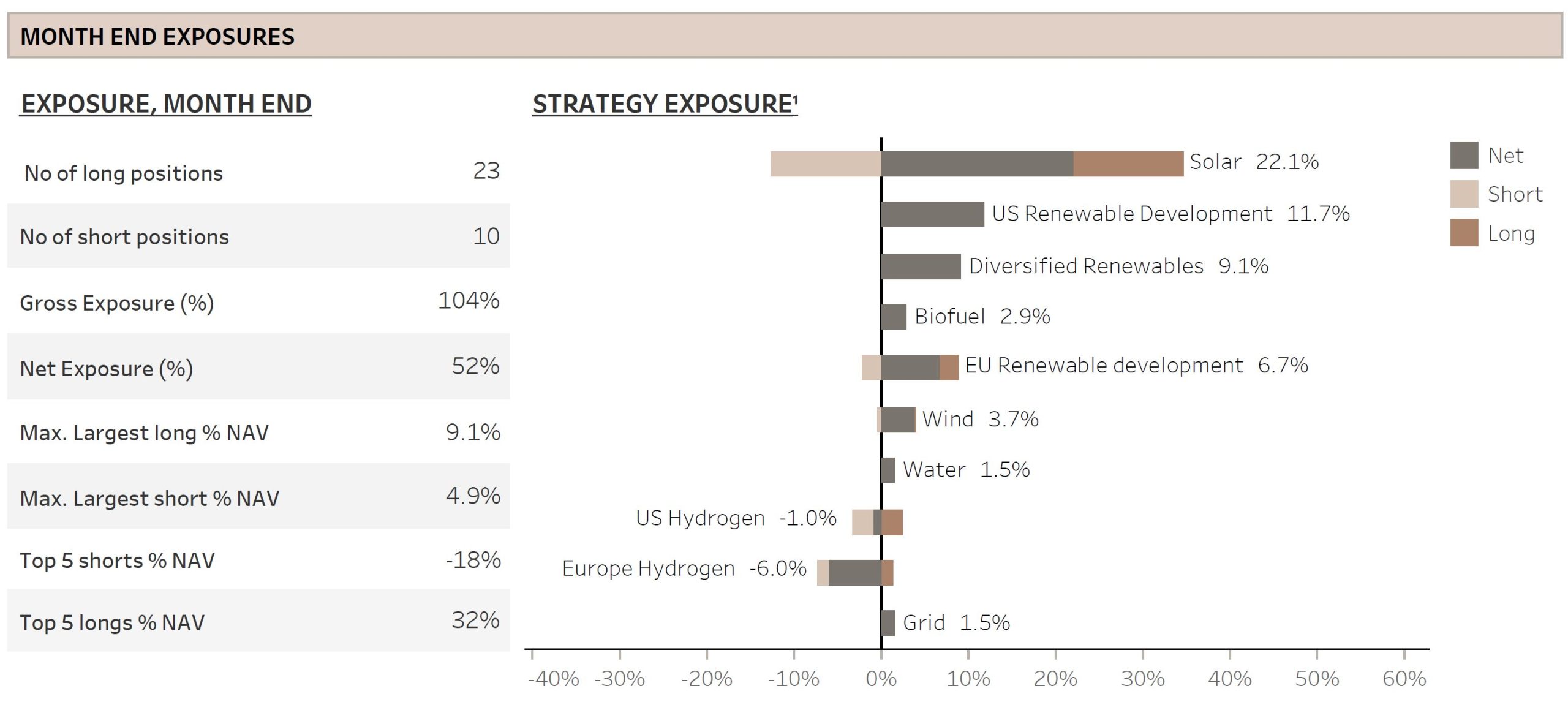

As renewable energy reference indices fell high single digits, it was not a surprise that the profit was made on the short side which contributed 2.3% vs the longs losing 2.1%. We maintained a net exposure in the 40-50% range during the month as we decided to reduce some exposure mainly due to US debt ceiling concerns. Remember that we target a net exposure of between 40% and 80%. The gross exposure averaged about 100% and ended the month at 104%. More details on fund performance further below.

MARKET COMMENT – STRONGER THAN EXPECTED EARNINGS SEASON

The S&P 500 continued its ascent in April, increasing 1.5% and lifting the year-to-date performance to 8.6%. Following the volatile March with the mini-banking crisis, April was the opposite with the VIX (the volatility index of the S&P 500) trading at low levels only seen over brief periods since the start of the pandemic.

The main reason for the calm, we believe, was much stronger first quarter earnings than feared. Profit margins are holding up better than expected as companies have been able to increase prices to offset input cost inflation. S&P500 profit margin expectations for 2023 have stopped declining, for now at least. Being able to push through higher prices is great for the individual companies but will not help pushing inflation down to FED’s 2% target.

Also, as the FED signaled that the mini banking crisis in March helped to tighten financial conditions, the market quickly priced in that the last interest rate hike would come in May. Historically, the end of the FED hiking cycle has been a positive catalyst for equity markets. Unfortunately, this is mostly the case the last four decades when inflation has been under control, which is not necessarily the case today. Moreover, if a recession is required to curb inflation, profit margins will shrink, earnings will decline, and stocks will underperform. The market is not pricing that scenario at the moment.

Nevertheless, in the first days of May, more regional banks tanked, and the market was suddenly uncertain if the banking crisis really was in the rear-view mirror. There are huge imbalances in the financial system and this uncertainty will likely linger for some time.

In addition, the debt ceiling debate which was expected to be a topic for July and August suddenly hit the headlines as Treasury Secretary Yellen sent a letter to Congress stating that the US Government might run out of money in early June. Only a few punters believe the US Congress will make the US default on its debt; however, most economists believe the run up to an agreement will be noisy and the draconian consequences of a ‘no deal’ will cause a lot of volatility in financial markets.

Finally, the FED increased the base rate by 25 bps as expected in early May. Although, chairman Powell did allude to this being the last hike if the data allowed it, he refused to bless the market’s two rate cuts by the end of the year.

As we have long argued, it will be challenging to push inflation down to the target with record low unemployment, strong profit margins and a consumer that is still spending savings from the pandemic. Instead, we fear that inflation and interest rates will only decline to pre-pandemic levels when the economy declines and unemployment increases, which is normally not a conducive environment for stock markets.

RENEWABLE ENERGY – VIRTUAL POWER PLANTS WILL ADVANCE GRID EFFICIENTLY

April proved to be a challenging month for renewable energy stocks as indicated by the 5-6% decline in the main indices. The solar sector was particularly weak with the TAN falling by 7.3% during the month. The primary catalyst was Enphase’s Q1 earnings report, which reminded the market of the fear of a significant slowdown in the US residential solar market in the second half of the year. This is primarily attributed to the impact of the new net metering regulation (NEM 3.0) in California, but higher interest rates are also impacting demand in important solar states like Texas and Florida.

To be clear, this is old news. However, the last factor to impact solar stocks and its investors is the commencing debt ceiling debate where the Republicans are asking for an extensive list of cost reductions, including slashing the IRA and other funding for fighting climate change. This would be terrible for solar companies and one sell side analyst categorized it as a ‘buyers strike’ until there is more clarity on this issue.

This was one key reason why we reduced net exposure early in the month. However, in the bigger picture, it is a speed bump. Let us take a step back and consider the long-term opportunities in rooftop solar and while our optimism may be tempered in the near term, it remains high for the future.

While utility scale solar is the cheapest form of energy globally, rooftop solar is not. However, it offers several other advantages. First, it does not require additional land use as it utilizes existing rooftops. Second, it generates power at the point of consumption, reducing the need for extensive grid infrastructure. Moreover, rooftop solar is highly resilient since there is no single point of failure risk associated with large power plants. This decentralized energy resource (DER) concept also opens up opportunities for virtual power plants (VPPs). A VPP is effectively a number of residential batteries managed in the cloud as storage backup during peak load periods. For the customers, this is beneficial as they can choose to opt in or out of the programme and monetize their surplus electricity. During the last quarter, we witnessed the establishment of several VPPs across the US.

At the end of the month, The Brattle Group, a premier consulting group, released a notable study on the economic impact of VPPs on the grid. According to their findings, leveraging VPPs to balance the grid load can be considerably cost-effective. In fact, it found that VPPs were 40-60% cheaper than traditional natural gas-fired peaker plants or utility-scale batteries. This cost advantage underscores the financial viability and attractiveness of VPPs as a grid management strategy.

More importantly, we expect the value proposition of VPPs to grow over time. As the number of electric vehicles (EVs) integrated into the grid increases, their batteries can serve as valuable storage backup for VPPs and thus reduce the need for expensive infrastructure investments.

Please note that we are not suggesting that costly infrastructure investments will not be necessary, the energy transition requires a diverse range of solutions. However, the integration of VPPs and the potential utilization of EV batteries would be important contributions to strengthen the grid to prepare for increased electrification, not only of cars.

The energy transition is often subject to politicization, with proponents of specific technologies, such as for instance solar or nuclear, vying for dominance. The truth is, we need a diversified portfolio of energy sources. A common misconception is that meeting the charging demands of EVs will be impossible. However, the reality is that electrifying personal transportation alone does not pose a major challenge for the grid. For instance, by our calculations, electrifying every car in Sweden would increase electricity demand by only about 10 TWh or 7% of the total electricity consumption. This estimate assumes 5 million cars driving an average of 35 km per day, consuming on average 150 Wh/km.

The attractiveness of owning an EV will improve as more VPP offerings are introduced. The car will effectively start generating cash flow while supporting the grid. Moreover, increased EV penetration drives more demand for rooftop solar and smart home energy solutions. This is one reason why we believe the longer-term outlook for the residential solar players is bright.

FUND PERFORMANCE – P&L HURT BY SELL OFF IN SOLAR

The fund was up 0.3% (I USD) in April with shorts adding 2.3% and longs deducting 2.1% from NAV. Only three out of ten themes lost money, but our biggest one, Solar, reduced NAV by 1.2% and lost 2% on the average gross capital in the theme.

As discussed briefly in the previous section, we reduced our net exposure to the low 40% into earnings season, partly due to concerns around the debt ceiling and its potential risks to the IRA. One of the positions we reduced by more than half was Enphase Energy (ENPH), as we also feared weak revenue guidance going forward. This turned out to be correct as the stock fell 26% on the day of earnings. Despite our reduced position, the stock was still the biggest negative contributor on both an absolute and relative basis, losing 0.9% of NAV during the month.

ENPH reported better than expected first quarter results but guided Q2 revenues 6% lower than the sell-side consensus. On the other hand, the company guided to higher gross margins and earnings estimate for 2023 were in fact increased by 8% after the Q1 report. Still, the market was indiscriminate and cut the company’s value by a quarter. It also took down with it the rest of the solar space.

As the ENPH shares crashed, we were clearly too early to build back part of the position. Nevertheless, we are still comfortable with the company’s fundamentals and the market position longer term. As discussed in the previous section, we are optimistic to the residential solar space over the long-term, in particular as the growth in VPPs accelerate. We were encouraged by the strong gross margin guidance in the inverter business, we believe the reasons for the weak battery sales into Q2 are well understood, and with a new generation of batteries launching later this year, we believe ENPH is well positioned to take advantage of increased battery attachment rates and the long-term growth in DER.

Timing is always difficult. The debt ceiling negotiation is about to commence, and the uncertainty might linger until July or maybe even into August. However, we are still to find a political expert that believe the Republicans will kill off a law that has already created tens of thousands of jobs in Republican states.

Moreover, the US solar residential market is perceived by many to be halting as higher inflation and interest rates combined with political uncertainty reduce demand for roof top solar. Although the residential solar market might only grow by low single digits this year, we expect the market to increase significantly from 2024 onwards as the IRA tax credits combined with lower solar module prices and higher utility electricity rates make rooftop solar even more attractive.

Another big loser this month was First Solar (FSLR). As we explained in the last monthly, FSLR is one of largest winners of the IRA. Although the stock is also hurt by the uncertainty created by the debt ceiling / IRA, the main reason for the 17% fall in the last week of the month was very weak first quarter results combined with declining growth in the order backlog. However, we are not concerned about the weak Q1 as full year guidance was unchanged and scheduling of large orders often result in lumpy quarterly sales. With regards to the backlog growth, the company is sold out until the end of 2026 and our concern is not if FSLR can sell the capacity but at what price. We found it encouraging that average selling price increased compared to the prior quarter.

Reducing the losses in the solar theme was a positive contribution from a large short position in the utility scale space and a trading long in one of the large residential players.

On the positive side, it was the net short hydrogen themes that made the biggest contribution this month as well. US Hydrogen added 0.7% to the NAV as non-profitable tech continued to underperform the market.

Diversified Renewables, containing only Chart Industries (GTLS), contributed 0.6% to NAV. As we mentioned in the last monthly, the company announced positive order numbers mid-month and strong Q1 numbers later in the month.

‘EU Renewable Development’ also did well as we added RWE to the theme ahead of its positive earnings update. Although RWE is not a pure-play renewable developer and not a typical company we invest in, it is one of the world’s largest investors in renewable energy and we like its plan for transitioning from brown to green energy.

We look forward to updating you again at the end of May.

Sincerely,

Vidar & Joel

- Portfolio Manager and Founder of the Coeli Energy Opportunities Fund.

- Over 15 years of investment experience spanning both public markets and private equity.

- Managed the Coeli Energy Transition Fund from 2019 to 2023.

- Spent six years at Horizon Asset in London, a market-neutral hedge fund.

- Started working with Vidar Kalvoy in 2012.

- Five years in Private Equity at Morgan Stanley.

- Began his investment career in the technology sector at Swedbank Robur in Stockholm in 2006.

- Holds an MSc in Engineering from the Royal Institute of Technology (KTH), Stockholm.

- Portfolio Manager and Founder of the Coeli Energy Opportunities Fund.

- Has managed energy equities since 2006 and brings more than 20 years of experience in portfolio management and equity research.

- Managed the Coeli Energy Transition Fund from 2019 to 2023.

- Head of Energy Investments at Horizon Asset in London for nine years, a market-neutral hedge fund.

- Experience from energy investments at MKM Longboat in London and equity research in the technology sector in Frankfurt and Oslo.

- Holds an MBA from IESE in Barcelona and a Master’s in Business and Economics from the Norwegian School of Economics (NHH).

- Before entering finance, he served as a lieutenant in the Royal Norwegian Navy.

IMPORTANT INFORMATION. This is a marketing communication. Before making any final investment decisions, please refer to the prospectus of Coeli SICAV II, its Annual Report, and the KID of the relevant Sub-Fund. Relevant information documents are available in English at coeli.com. A summary of investor rights will be available at https://coeli.com/financial-and-legal-information/. Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested. Please note that the management company of the fund may decide to terminate the arrangements made for the marketing of the fund in one or multiple jurisdictions in which there exists arrangements for marketing.