This material is marketing communication.

Note that the information below describes the share class (I USD), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class return. The information below regarding returns therefore differs from the returns in other share classes.

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

1) Share Class I USD

FUND MANAGER COMMENTARY

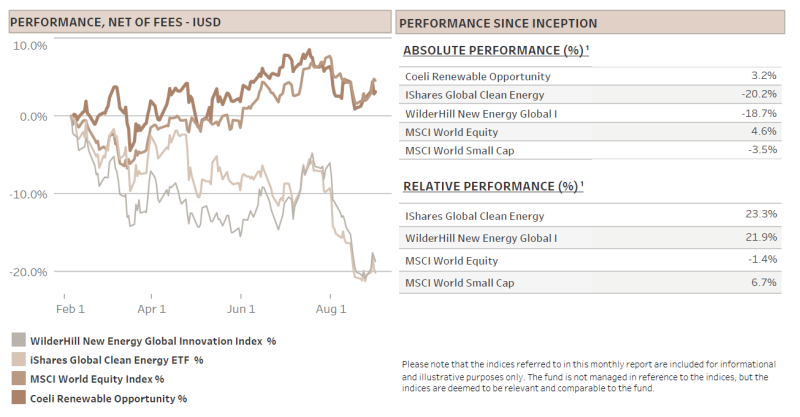

The Coeli Renewable Opportunity fund lost 3.1% net of fees and expenses in August. It is up 3.2% since the inception on February 6, 2023.

August was at the same time our best and worst month since inception. The drawdown was painful, but in line with the returns of the MSCI World equity index. More importantly, the fund substantially outperformed the most comparable renewable energy indices, the Wilderhill New Energy Global index (NEX) by 10.5% and the iShares Global Clean Energy (ICLN) by 9.0%.

Since inception, seven months ago, the outperformance is 22% and 23%, respectively. We believe this clearly validates our strategy of not only trying to go long the winners, but also actively creating alpha by shorting overvalued companies that lack a sustainable competitive advantage. We are convinced that this approach offers a distinct edge over a straightforward long-only investment strategy in this sector.

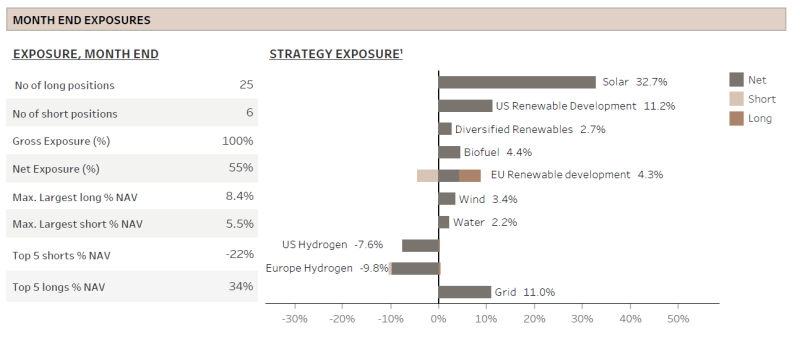

In terms of market exposure, we maintained a cautious stance throughout the month. Our net exposure hovered around 50%, aligning with our target to maintain a net long position of 40-80% within the renewable energy sector. While eight out of our ten themes contributed negatively to performance, our short-focused themes on hydrogen technology mitigated some of these losses.

MARKET COMMENT – TOO MUCH GOOD NEWS?

The market rally took a breather in August as both the S&P 500 and the Nasdaq 100 declined by nearly 2% following a very strong performance in the first seven months of the year.

Inflation has substantially retreated from its recent highs, while economic indicators are outpacing expectations. In our previous monthly commentary, we discussed how this "Goldilocks" scenario appeared to be already factored into market valuations.

In August, macro indicators again surprised on the upside. The yield on the 10-year US Treasury note surged, exceeding last October's peak and reaching heights not witnessed since before the 2008 financial crisis. What distinguishes this spike from that of last October is its driver: this time it is not inflation causing the rise but rather real interest rates. This is unfavorable for equity markets, particularly for long-duration equities like renewable energy stocks. Such stocks often rely on the promise of positive cash flows extending far into the future.

RENEWABLE ENERGY – HEADWINDS CONTINUE IN OFFSHORE WIND

Renewable energy stocks are out of favour. August ranked as one of the top three worst-performing months for renewable energy indices over the past decade. This downturn can be attributed to a combination of factors: rising real interest rates discouraging investments in long duration assets, coupled with a flurry of negative news affecting various segments. Some sectors are suffering from weakened demand due to high interest rates, while others are impacted by depressed prices stemming from oversupply, while delays and cancellations of orders have affected other parts of the industry.

The latter is very much the case in offshore wind, which we wrote about in the last monthly arguing that there are some signs of tailwinds despite all the headwinds. We still believe that is the case, but the headwinds are currently much stronger than expected. Late in August, Orsted (ORSTED DC), the global leader in offshore wind development, surprised the market with a large impairment of up to DKK 16bn on its US offshore wind portfolio. The stock fell 24% on the day and has continued to slide in September.

The surprise was not so much that Orsted had to do impairments, but rather the size and the fact that it came only 3 weeks after the second quarter report where Orsted had assured investors that there was no need for write-downs. Although the company is emphasising that the impairment is up to DKK 16bn and dependent on the near-term development in both long term interest rates and tax negotiations in the US, the sudden deterioration in the US supply chain, accounting for a third of the impairment, is a bad omen.

In terms of costs, offshore wind continues to become more expensive, while the costs associated with onshore wind have stabilized, and solar energy costs are decreasing. It is becoming evident that execution risks in the offshore wind sector are not adequately priced in. Specifically, the risk premium within the cost of capital appears underestimated, implying that prices may need to further increase to provide developers with an appropriate risk-adjusted return on investment.

We still believe offshore wind has a future, but it seems likely that it will take a smaller share of the total electricity market than what was generally expected only months ago. It is increasingly likely that it will take longer to achieve the ambitious targets set by policymakers than was initially anticipated.

FUND PERFORMANCE – STRONG RELATIVE BUT WEAK ABSOLUTE PERFORMANCE

The fund lost 3.1% (I USD) in August, pulled down by a 7.3% loss on the long holdings and partly offset by a 4.2% profit on the shorts.

The worst performing theme was not surprisingly ‘Solar’, which drew down NAV by 2.1%. Solar is still our largest theme and with a significant net length despite having reduced exposure within residential solar in July. Most of the net length is within utility scale solar where the largest position, Array Technologies (ARRY) was up as much as 30% during the month. Unfortunately, the second largest position, Shoals Technologies (SHLS) declined by 30%. For comparison, the solar index (Invesco Solar ETF - TAN US) was down 15% in August.

The second worst performing theme was ‘US Renewable Development’, which deducted 1.5% from NAV. The theme only contains the two leading renewable developers in the US, Nextera Energy (NEE) and AES. We are strong believers in both companies but acknowledge that these stocks are unlikely to perform as long as renewable energy is out of favour and higher interest rates are putting pressure on utility stocks in general.

The ‘European Renewable Development’ theme only lost 0.2% of NAV despite positions in Orsted, RWE and EDP Renovaveis (EDPR). The two latter stocks fell in sympathy with Orsted and over the increased uncertainty in offshore wind development. Fortunately, the net exposure in the theme was not excessive and the short positions contributed positively during the month.

The only two themes with positive returns were ‘US Hydrogen’ and ‘Europe Hydrogen’, both were net short and contributed 1.1% and 1.0% respectively to NAV. The US theme benefited considerably from a timely adjustment of our position in Plug Power (PLUG). We substantially reduced our position at the end of July and sold the rest in early August as the stock plunged 40% into second quarter earnings report and mid-month capital markets day. We have in many previous monthlies described how we are skeptical to the value proposition and thus the valuation of hydrogen companies.

We look forward to updating you again next month.

Sincerely,

Vidar Kalvoy & Joel Etzler

- Portfolio Manager and Founder of the Coeli Energy Opportunities Fund.

- Over 15 years of investment experience spanning both public markets and private equity.

- Managed the Coeli Energy Transition Fund from 2019 to 2023.

- Spent six years at Horizon Asset in London, a market-neutral hedge fund.

- Started working with Vidar Kalvoy in 2012.

- Five years in Private Equity at Morgan Stanley.

- Began his investment career in the technology sector at Swedbank Robur in Stockholm in 2006.

- Holds an MSc in Engineering from the Royal Institute of Technology (KTH), Stockholm.

- Portfolio Manager and Founder of the Coeli Energy Opportunities Fund.

- Has managed energy equities since 2006 and brings more than 20 years of experience in portfolio management and equity research.

- Managed the Coeli Energy Transition Fund from 2019 to 2023.

- Head of Energy Investments at Horizon Asset in London for nine years, a market-neutral hedge fund.

- Experience from energy investments at MKM Longboat in London and equity research in the technology sector in Frankfurt and Oslo.

- Holds an MBA from IESE in Barcelona and a Master’s in Business and Economics from the Norwegian School of Economics (NHH).

- Before entering finance, he served as a lieutenant in the Royal Norwegian Navy.

IMPORTANT INFORMATION. This is a marketing communication. Before making any final investment decisions, please refer to the prospectus of Coeli SICAV II, its Annual Report, and the KID of the relevant Sub-Fund. Relevant information documents are available in English at coeli.com. A summary of investor rights will be available at https://coeli.com/financial-and-legal-information/. Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested. Please note that the management company of the fund may decide to terminate the arrangements made for the marketing of the fund in one or multiple jurisdictions in which there exists arrangements for marketing.