This material is marketing communication.

Note that the information below describes the share class (I USD), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class return. The information below regarding returns therefore differs from the returns in other share classes.

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

1) Share Class I USD

FUND MANAGER COMMENTARY

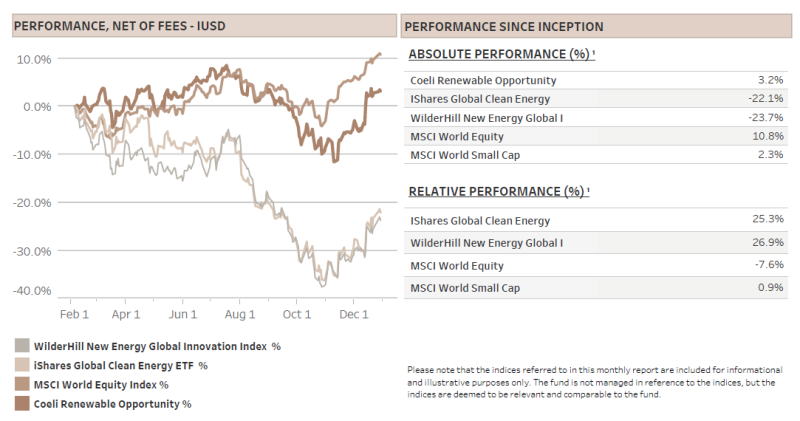

The Coeli Renewable Opportunity fund gained 7.4% net of fees and expenses in December. It is up 3.2% since the inception on February 6, 2023.

December was the fund’s best month since inception in February. While the outperformance to the two most comparable indices, the Wilderhill New Energy Global index (NEX) and the iShares Global Clean Energy (ICLN) has narrowed, the fund still closed the year ahead by 27% and 25%, respectively.

It is worth noting that while the fund’s performance bottomed at down 11.5% in early November versus a 36-37% loss for the two reference indices, the fund rose almost as much as the indices off the bottom, i.e. 17% for the fund compared to a gain of 22% for the indices. We believe it validates our strategy that the fund outperforms by more than 3x on the way down and capture almost 80% of the long-only reference indices’ return in the rally off the bottom.

While we were too early calling the bottom in early October, the expected year-end relief rally played out in November and December. Moreover, while renewable energy equities only performed in line with the market in November, they, like we had alluded to in the previous monthly report, caught up in December as small caps finally caught a bid. Obviously, this was partly driven by short squeezes as positioning and sentiment were still relatively bearish in early December.

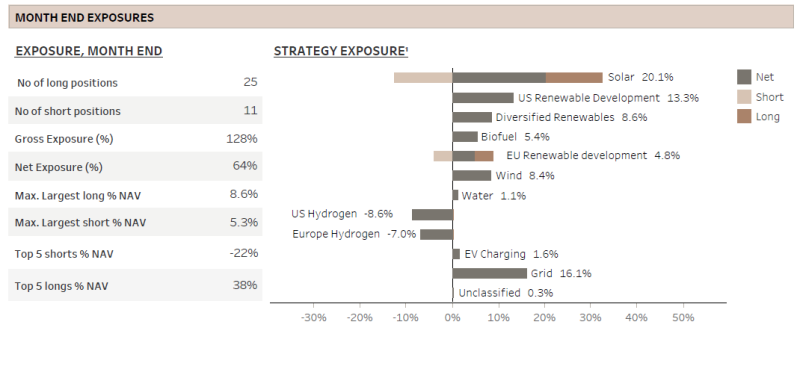

Our long holdings added 10.4% to the NAV, while the shorts lost 3.0% in December. All but one of the themes made a profit. Net exposure was in the 60-70% range over the month and ended at 64%.

MARKET COMMENT – GOLDILOCKS BECAME CONSENSUS!

The S&P 500 rose 4.4% in December, following on from the 9% increase in November and closing the year less than 1% from its all-time high in January 2022. The key reason for the rally was again lower rate expectations as inflation continued to surprise on the downside and the economy and labour markets on the upside. The yield on 10-year US Treasury bills dropped by 45bps to 3.85%, a level last seen in July before the big sell off in small cap equities started.

Fueling the rally was FED chairman Powell emphasizing at the FOMC meeting in early December that rate cuts will happen long before inflation has reached the 2% target. This combined with the new FED dot-plot indicating three rate cuts in 2024 cemented the view that a soft landing was not only possible but even likely. Goldilocks became consensus and the bond market is at the moment pricing in as many as five 25bps cuts in 2024 with a ~60% probability of a cut already in March.

We admit that we last year did not subscribe to a soft-landing scenario where inflation would come down without any significant slowdown in the economy. However, it admittedly looks likely and three or more rate cuts in 2024 is a great backdrop for the renewable energy space, one of the largest thematic losers in 2023 despite enjoying one of the strongest long term fundamental tailwinds.

While valuations are not as depressed as at the beginning of November, we are still very optimistic to the year for the broader decarbonization space. First, valuations in most of the subsectors have come down significantly over the last three years. In some cases, companies are valued on their existing assets only, i.e. with no value attributed to growth.

Second, the supply chain and inflation linked problems that caused significant negative earnings surprises are in the rearview mirror. However, the difficulties have helped some of the leading companies to advance their market shares during the downturn. Moreover, the competitive landscape has become less intense as numerous companies have either withdrawn from the sector or scaled back their ambitions. Contrasting with the situation three years ago, private capital is not as aggressively entering the sector, which is positive for established players and their expected returns on investments.

Third, electricity prices have more than kept up with inflation. An undersupplied power market is a good starting point for more renewable investments irrespective of decarbonization goals.

Finally, renewable energy equities were among the worst hit sectors by the rise in interest rates during 2023. We believe it is likely that they will be among the largest relative beneficiaries when rates fall as well.

Still, there are always some clouds on the horizon creating trading opportunities on both the long and the short side of our fund. One of the biggest uncertainties near term is election risk and in particular the US election, which kicks off this month with the primaries for the US presidential election.

WILL AND CAN TRUMP KILL THE INFLATION REDUCTION ACT?

Our short answer to both questions is that we doubt it. Even if the Republicans win both Houses of Congress and the presidency, we doubt that there is an appetite for a full repeal of the Inflation Reduction Act (IRA). However, there might be adjustments to the law and this risk will constitute significant noise for US renewable energy equities until the election. Moreover, this noise will only intensify the better the Republicans do in the polls.

Former president Donald Trump, who is a strong favourite to win the Republican Party’s primaries, is campaigning on gutting much of the Inflation Reduction Act (IRA) and to dismantle President Biden’s climate change policies. We can only hope that he will tone down the rhetoric in the general election to appeal to centrist voters, but there are no guarantees.

What would it take to repeal the IRA? The Republicans would need a red sweep, meaning winning the presidency and a simple majority in both the House and the Senate. The IRA was passed in a partisan vote by the Democrats under budget reconciliation, a special parliamentary procedure that overrides the Senate’s filibuster rules, which means that it can similarly be repealed or altered by a simple majority of republican senators.

Before discussing the likelihood of a repeal, what would be the consequences if the Republicans would gut the IRA?

First, according to BNP Paribas, about USD 700bn to USD 1.1tr of capital expenditures over the next 5 to 7 years rely on the IRA. This represents about 5-7% of all US corporate capex across those years. Factoring in the multiplier effect, the impact on US economic growth could be substantial. Moreover, the IRA has supposedly created more than 100,000 manufacturing jobs already and researchers with the Foundation for Renewable Energy & Environment estimates that IRA could help to create 900,000 jobs per year over the next decade, totaling more than 9 million jobs. Compared to a labour force of about 167 million, we take that estimate with a grain of salt, but it is obvious that there is a significant positive contribution to employment.

Second, it is estimated that 70-80% of these jobs will be created in red or purple states, i.e. republican dominated or swing states that could go both ways in the election. Obviously, a repeal of the IRA subsidy would jeopardize many of these jobs, a highly unpopular outcome.

Finally, unless Trump intends to prohibit the construction of renewable energy installations, undermining US manufacturing of renewable energy equipment will play into the hands of the Chinese who are dominating most segments of the renewable energy industry.

Facing these consequences, why would the Republicans try to repeal the IRA? For many climate change sceptics, the IRA is a simply a waste of money. However, the IRA does almost more to the other objectives of the act, i.e. energy security, re-shoring supply chains and creating manufacturing jobs in the US. This is a fact we believe will be hard for the Republicans to ignore.

In Trump’s first presidential period, he talked constantly about creating blue-collar jobs for Americans and he restricted import of foreign manufactured goods, especially Chinese, in order to help US corporations. Repealing the IRA would be contrary to these goals. Additionally, many of the republican members of Congress have selfishly taken credit for bringing manufacturing jobs to their counties and states, even though none of them voted in favour of the IRA. For these politicians to vote for a repeal would be a risky step considering that there is always another election for congress around the corner.

Moreover, a full repeal looks unlikely considering that the last time the Republicans controlled both Houses and the presidency, Trump did not manage to keep his campaign promise of revoking the much-hated Affordable Care or ‘Obama care’ act. We believe the IRA has significantly more bipartisan support than Obama care. Furthermore, the investment tax credits (ITC) and the production tax credits (PTC) that preceded the IRA were both born during republican presidencies and have been extended ever since, including during Trump’s four years in power. Rather than eliminating subsidies, Trump introduced tariffs on Chinese products to bolster US manufacturers and to hurt the Chinese. Revoking the IRA would be doing the opposite, and we find it unlikely.

Instead of a full repeal, we do fear though that a red sweep might lead to modifications in certain aspects of the IRA. For instance, the Republicans have shown limited enthusiasm for direct consumer subsidies, suggesting that the USD 7,500 electric vehicle tax credit could be at risk. Similarly, direct support for residential solar, although part of the ITC since 2006, might face reductions. On the other hand, it is hard to envision the Republicans withdrawing support for nuclear energy or significantly altering manufacturing tax credits, given the clear negative impact such moves would have on their own constituencies.

A bigger fear we have is that a Republican president, with or without a Congressional majority, will reinterpret the guidelines for the IRA. The executive branch cannot eliminate a tax credit, but it can make access to the credit much more strident. This could have a significant impact on tax credit adders e.g. the important domestic content adder, which is so complex that the current administration has not yet been able to create the guidelines.

All in all, we doubt the IRA will be repealed, but there is little doubt that the White House occupied by a Democrat is better for the renewable energy universe. We are not making any prediction on electoral outcomes, but this uncertainty will create volatility through the year. However, since Trump started campaigning on repealing the IRA, it has been widely discussed by the sell side and the buy side have already factored in the risk. Any indication that the Democrats are in the lead would therefore be a significant positive catalyst. We will follow the developments closely and believe the fund should benefit from the opportunities on both the long and the short side during the year.

FUND PERFORMANCE – BEST MONTH ON RECORD

The fund gained 7.4% (I USD) in December, its best month to date. The profit was broad-based, with all but one investment theme showing positive returns. Long positions were particularly impactful, contributing 10.4% to the Net Asset Value (NAV). The robust rally in renewables and other small-cap stocks over the past two months was partially fueled by short squeezes in heavily shorted stocks, though not all sectors benefited equally. Notably, our 'EU Hydrogen' theme, which holds only short positions, was the third-best performer, adding 0.8% to the NAV in December. Moreover, it also yielded profits during the two-month rally spanning November and December. This indicates the strong cross-sectional dispersion in this sector.

At the opposite end of the dispersion spectrum was the ‘Grid’ theme which emerged as the top performer for the second consecutive month, adding 1.9% to the NAV in December. As we have described in previous monthly reports, this theme includes companies that sell products and services related to the electrical grid. With anticipated improvements in permitting processes in both the US and Europe, transmission and interconnection are expected to become bottlenecks for the development of renewable energy in these regions. We are increasingly optimistic to this theme which only includes long positions for now.

Meanwhile, the 'Solar' theme ranked as the second-best performer in December, enhancing the NAV by 1.7%. A recurrent topic in our monthly updates, this theme maintains the largest gross capital, although positioning has become more balanced and not as long-biased as before. Despite the sub-sector’s robust rally, the theme’s December performance was a bit disappointing. Our long positions in utility-scale solar lagged behind the Solar Index (TAN US), while one of our short positions in a solar module manufacturer surged by nearly 75% in value during the month. However, this short position has given back half of its December gains so far in January.

The last theme to mention this month is the ‘Wind’ theme which finally started to work, adding 0.7% to NAV in December. The driver of the performance was Vestas (VWS) which increased 13% in December and almost 60% since the bottom in early October. The company reported onshore orders totaling almost 6.2GW in the fourth quarter, with 4.7GW designated for the US. We have waited all year for a hockey stick in Vestas’s order intake and are not too surprised that it finally happened. For the entire year, including unannounced Q4 orders, the total could reach nearly 18GW, surpassing both our optimistic initial estimate and the market consensus’. Next year will likely be even better as there are still a lot of IRA induced US orders to be announced and as Siemens Gamesa has pulled back from the onshore market, Vestas is well positioned for market share gains.

Additionally, offshore wind orders have yet to surge, but as optimism returns among developers and it becomes evident that offshore wind projects are delayed rather than cancelled, Vestas stands to see a substantial increase in order intake over the coming years.

Finally, it is notable that the majority of Vestas Q4 orders are scheduled for execution in 2025 and beyond. This is somewhat dampening the expectations to 2024 earnings, which are currently challenged by overcapacity in certain manufacturing plants, particularly in the US, and by low margin legacy contracts secured during the pandemic. However, the market is already well aware of the below-target margins for 2024. More important, the recent surge in order intake underscores the viability of Vestas’s 10% margin target for 2025. We believe Vestas will continue to trade on order intake and plan to increase our position if the stock sells off on disappointing Q1 results.

As we look forward to 2024, we remain optimistic about the broader renewable energy equities space. Despite anticipating continued strong cross-sectional dispersion, we foresee a shift towards a more stock-picker-oriented market within and across the different sub-sectors. This scenario is ideal for our strategy, and we look forward to updating you again over the coming months.

Sincerely,

Vidar Kalvoy & Joel Etzler

- Portfolio Manager and Founder of the Coeli Energy Opportunities Fund.

- Over 15 years of investment experience spanning both public markets and private equity.

- Managed the Coeli Energy Transition Fund from 2019 to 2023.

- Spent six years at Horizon Asset in London, a market-neutral hedge fund.

- Started working with Vidar Kalvoy in 2012.

- Five years in Private Equity at Morgan Stanley.

- Began his investment career in the technology sector at Swedbank Robur in Stockholm in 2006.

- Holds an MSc in Engineering from the Royal Institute of Technology (KTH), Stockholm.

- Portfolio Manager and Founder of the Coeli Energy Opportunities Fund.

- Has managed energy equities since 2006 and brings more than 20 years of experience in portfolio management and equity research.

- Managed the Coeli Energy Transition Fund from 2019 to 2023.

- Head of Energy Investments at Horizon Asset in London for nine years, a market-neutral hedge fund.

- Experience from energy investments at MKM Longboat in London and equity research in the technology sector in Frankfurt and Oslo.

- Holds an MBA from IESE in Barcelona and a Master’s in Business and Economics from the Norwegian School of Economics (NHH).

- Before entering finance, he served as a lieutenant in the Royal Norwegian Navy.

IMPORTANT INFORMATION. This is a marketing communication. Before making any final investment decisions, please refer to the prospectus of Coeli SICAV II, its Annual Report, and the KID of the relevant Sub-Fund. Relevant information documents are available in English at coeli.com. A summary of investor rights will be available at https://coeli.com/financial-and-legal-information/. Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested. Please note that the management company of the fund may decide to terminate the arrangements made for the marketing of the fund in one or multiple jurisdictions in which there exists arrangements for marketing.