This material is marketing communication.

Note that the information below describes the share class (I USD), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class return. The information below regarding returns therefore differs from the returns in other share classes.

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

1) Share Class I USD

FUND MANAGER COMMENTARY

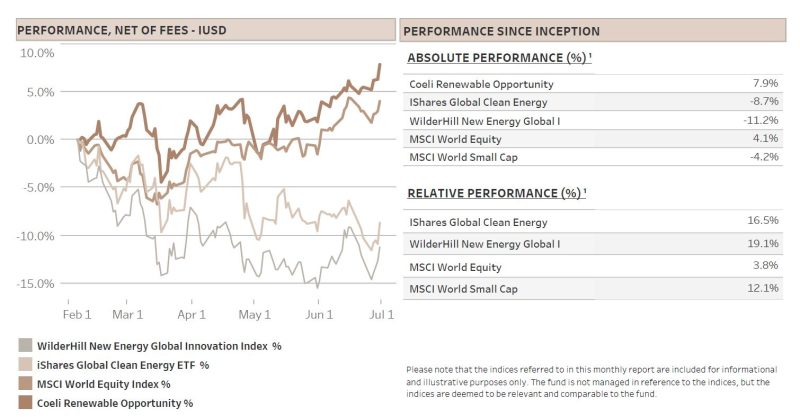

The Coeli Renewable Opportunities fund generated a profit of 5.9% net of fees and expenses in June. It is up 7.9% since the inception on February 6, 2023.

The fund has outperformed the most comparable indices, the Wilderhill New Energy Global index (NEX) by 19.1% and the iShares Global Clean Energy (ICLN) by 16.5% since inception. During June, the fund outperformed the NEX and ICLN by 0.8% and 4.9%, respectively.

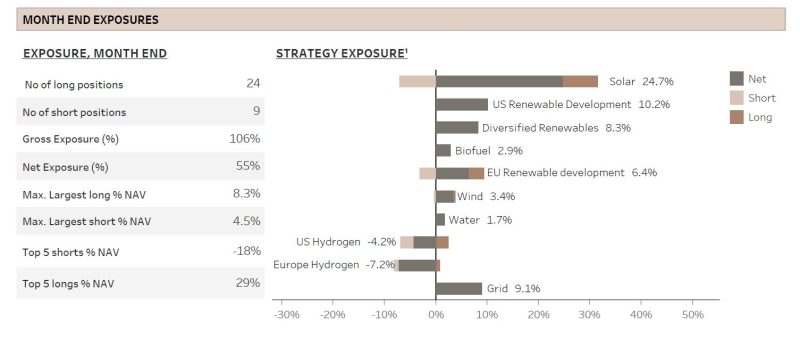

In June, all but one of the fund’s 10 themes contributed positively to the performance. The ‘Diversified Renewables’ theme accounted for about half of the return, but the ‘Grid’ theme, ‘Solar’ and the two renewable development themes also did well. We are also pleased that short contribution was positive by 0.4% of NAV in a month where the market rallied. The net exposure was around 60-65% for most of the month but was scaled down to 55% by the end of the month. Gross exposure at the month end was 106%.

At the half year mark, it is a good time to review the performance since the fund launch in early February. The short side has so far contributed to two thirds of the returns, which is not unexpected considering that renewable energy stocks have mostly declined. However, we are pleased that our shorts generated approximately 15% on the invested short capital while the renewable energy indices are down by about 10% in the same period. It is also encouraging that we made close to 3% of NAV on the longs despite the poor performance in this space. In total, as our net exposure has averaged about 50%, you can argue that alpha generation is about 12-13% in the first five months. More detailed information on the fund's performance can be found below.

MARKET COMMENT – TRADING A GOLDILOCKS ECONOMY?

June was a very strong month for the markets as the S&P 500 and Nasdaq both gained 6.5%, taking the half year return to 16% and 39%, respectively. Historically, based on data since 1928, the S&P in the second half of the year goes up more than 10% when the first half rallies by more than 15%.

However, there are still lingering concerns on the horizon. Despite the Federal Reserve (FED) pausing its interest rate hikes in June, Chairman Powell has indicated that two more hikes might be necessary this year. While there are signs of inflation receding, the pace of decline is clearly not fast enough for the FED’s liking. Two months ago, the bond market anticipated three interest rate cuts by the FED this year, while today an additional hike is priced in for July and the first cut is not expected before mid-2024. Higher for longer has become consensus, and as the 2-year US bond returned to its levels before the mini-banking crisis in March, the yield curve has inverted to a level that has historically been associated with an impending recession.

Moreover, the manufacturing PMIs both in the US and globally have dipped into contractionary territory and from the amount of profit warnings from early-cyclical industry the last weeks, it is obvious that the economy is facing some challenges.

Finally, while sentiment and positioning were bearish and very light just a few months ago, these have now shifted to the opposite extreme. Numerous sentiment indicators show investor sentiment levels at ‘extreme greed’ and hedge fund gross leverage is at high levels not witnessed in years.

On the other hand, the reason why the bond market is no longer expecting FED cuts this year is a diminished risk of recession. Given that many experts were anticipating at least a mild economic downturn, it is no wonder that negative sentiment and bearish positioning dominated the market throughout the year. One could argue that the potential for a recession had already been factored into market pricing, and as that risk has diminished, the subsequent rally in stocks is justified.

Also, most economic activity indicators are in fact surprising to the upside. The consumer confidence just hit a new high for the year and the labour market remains incredible resilient. Despite easing wage growth, which bodes well for inflation expectations, surveys show that US consumers have in aggregate increasing spending power.

Company earnings have so far also exceeded expectations. Most top-down analysts expected or are still expecting a significant drop in aggregate profit margins. Although reported and bottom-up earnings estimates are decreasing, they are declining much slower than initially feared.

As we have learned many times in the past, but often seem to forget, the market is a pricing mechanism and what truly matters is not if the data comes in positive or negative, but if it comes in better or worse than what was expected and what was priced in.

In conclusion, the market appears to be embracing a "Goldilocks" economy—characterized by moderate growth and controlled inflation. While we maintain our view that market valuations, particularly relative to real yields, are stretched, it is important to note that rich valuations alone have never been enough to trigger a market downturn. Furthermore, the market seems poised to weather one or two additional interest rate hikes, supported by the potential for significant productivity improvements promised by artificial intelligence. As a result, the positive sentiment could persist in the short term.

RENEWABLE ENERGY - Will green hydrogen deliver on its promise of decarbonization?

There is a lot of hype surrounding green hydrogen, with claims that it is a magical solution for decarbonizing heavy transportation, steel production, and cement manufacturing. While hydrogen is versatile, like a Swiss army knife, it is not necessarily the best at any specific task.

Green hydrogen faces additional challenges, but one of the most significant ones is its energy efficiency, or rather the lack of it. When converting renewable electricity to hydrogen, approximately 30% of the energy is lost in the process. Furthermore, if the end-use is for mobility, the fuel cell, which converts hydrogen back into electricity for the electric motors, incurs another 30-40% energy loss. This means that more than half of the clean energy is lost. In comparison, fully electric mobility experiences total energy losses of less than 10%.

Despite these efficiency concerns, the European Union remains optimistic about hydrogen as a key driver of decarbonization. Similarly, in the US, the Inflation Reduction Act (IRA) offers attractive credits to hydrogen producers who can minimize emissions. While we still await specific details from the IRS on the IRA, the basic premise is clear—the tax credits are strictly tied to emission targets during hydrogen production, without considering its end-use.

To qualify for the maximum credit, a staggering $3 per kilogram of hydrogen produced, emissions must be a mere 0.45 kg of CO2 per kg of hydrogen, or less. However, current hydrogen production relies heavily on steam methane reforming, which emits around 10 kg of CO2 for every kg of hydrogen. This means that when the US government pays $3/kg for hydrogen with CO2 emissions below 0.45 kg, the implied carbon abatement cost is more than $300/tonne. In comparison, transitioning from coal to natural gas costs less than $50/tonne of CO2. To make it worse, keep in mind that there could be additional costs depending on how the hydrogen is consumed.

Another critical aspect to consider is the concept of "additionality" – is the renewable energy generation truly new – i.e. additional? Will producers of green hydrogen be required to utilize only new renewable power sources to collect subsidises, or can they simply tap into the existing grid or purchase electricity from already established renewable plants? If only new renewable energy can be utilised for green hydrogen production, the costs and risks will be significantly higher, and mass production of green hydrogen will surely take more time.

On the other hand, if producers can connect to the grid or utilise existing renewable energy, we would essentially be diverting clean power from its original consumption, forcing fossil fuel plants to increase output to meet the rising demand. This of course undermines the overall decarbonization effort. The solution, both in the EU and in the US, should probably be to allow some usage of existing renewable energy during a relatively short transition period.

There is no doubt that there are many challenges on hydrogen’s path to success and this is where our fund's perspective becomes relevant. We strongly support the energy transition, but we recognize that it will be expensive and there are significant risks of misallocation of resources. This could have dire consequences, not only economically but also in the loss of public trust and support of the energy transition. That is why our investment strategy focuses not only on finding technologies and companies with the greatest potential for decarbonization, but it also aims to take short positions in those that divert capital and expertise down the wrong path. Within the hydrogen sub-sector, we believe there are some companies with solutions that fit that description. We will explore this further as we sum up the performance since inception below.

FUND PERFORMANCE – STRONG JUNE AND GOOD PERFORMANCE SINCE INCEPTION

The fund returned 5.9% (I USD) in June with nine out ten themes profitable. The largest contributor by far was ‘Diversified Renewables’ adding 2.9% to NAV. This theme holds only one long position, Chart Industries (GTLS), our largest position currently and top two since inception. We have discussed the investment case for this company in previous monthly letters and we were waiting for the stock to break out, which happened in June when the stock rose more than 40%.

The second-best performing theme was ‘Grid’ adding 0.8% to the NAV. This is a theme with three long positions in companies focused on grid connection and transmission. In our March monthly letter, we discussed the increasing demand for transmission and distribution grid to support the energy transition. Grid connections and capacity are likely the next bottlenecks as we electrify our economy and huge investments are required going forward. We believe we are still in the early innings of this development.

Our largest theme ‘Solar’ also did well in June, adding 0.7% to NAV despite both of our inverter companies, SolarEdge Technologies (SEDG) and Enphase Energy (ENPH) performing poorly following continued speculation that Tesla (TSLA) will eat into their market share as it is using its strong hold on batteries to win market share for its inverter offering. While we acknowledge that Tesla may capture some market share through the discounts on their batteries, we believe this is already partly factored into the share prices of both ENPH and SEDG. Nevertheless, we have lowered our exposure to the two stocks as they could continue to underperform as the rumors gain more widespread attention.

The only losing theme in June was ‘Wind’, deducting 0.2% from NAV. The largest holding, Vestas Wind Systems (VWS DC) was pulled down by a major profit warning by Siemens Energy (ENR GY), the owner of Siemens Gamesa, the largest competitor of Vestas. The main reason for the profit warning was vibration issues on approximately 15-30% of Gamesa’s most recently installed onshore wind turbines. The cost to rectify the issue could come to more than EUR 1bn. To us and most experts, this seems to be a company specific issue and if anything, it might be a positive for Vestas and other competitors as Gamesa becomes a less attractive supplier until ENR has worked through these issues. On the other hand, Vestas had similar, although much smaller, issues in the past. This serves as a reminder to the market of the inherent risks associated with the construction of increasingly larger wind turbines.

At the half year mark, it makes sense to sum up what has worked well and what has not worked since inception in early February. Eight out of eleven themes have made a positive contribution. As we said in the introduction, two thirds of the almost 8% performance stems from the short side while our long positions managed to generate a profit of close to 3% of NAV. This implies a return of approximately 4% on our invested long capital, which can be compared to a roughly 10% decline for the two most comparable renewable indices/ETFs, the NEX and ICLN.

The largest contributor in absolute terms was ‘Solar’, adding about 3% to NAV. As we have mentioned in every monthly report, this theme has been skewed long and has also been allocated the largest share of capital. Not all our investments in Solar have worked as planned, but we are still pleased with the positive performance as the TAN, the most comparable Solar index/ETF, has declined by 10% since our fund’s inception.

The largest losing theme was ‘US Renewable Development’ drawing down NAV by 0.9% since inception. The theme consists of the two leading energy transition utility companies in the US, Nextera Energy (NEE) and AES Corp (AES). Basically, all of the loss can be attributed to May when AES issued growth targets slightly below the market’s expectations. As outlined in detail in last month’s report, these revised targets were a result of the company’s accelerated coal exit plan. However, we believe this strategic shift will ultimately enhance AES’s valuation multiple. Moreover, with the incredible wave of capital being made available for renewable development in the US, we are confident that the two leading companies with the most experience and scale will do well.

Finally, we have two hydrogen themes, one for European companies and one for US listed names. As can be inferred from the previous part of this monthly, our stance on certain hydrogen players has been relatively negative for some time, resulting in a skewed short position for both themes. Interestingly, if we were to merge the two themes, the combined profit surpasses that of our ‘Solar’ theme. However, gross combined capital has only been about one-third of our investment in the solar sector. Despite the higher risk associated with shorting at times less liquid small-cap companies in the dynamic field of hydrogen, the returns from our short hydrogen themes are far superior to what we have made in ‘Solar’.

All in all, the first five months of the fund’s performance have been good. Our aim is to create alpha on both the long and the short side and so far, we have been successful. We are still confident that the energy transition is the largest investment theme of at least the next decade. We struggle to find any sector with such unique tailwinds. Obviously, if you have read this far in, you understand that not every company will flourish and there is value in being able to take selective short positions. That is at least our firm belief.

We look forward to updating you again next month.

Sincerely,

Vidar Kalvoy & Joel Etzler

- Portfolio Manager and Founder of the Coeli Energy Opportunities Fund.

- Over 15 years of investment experience spanning both public markets and private equity.

- Managed the Coeli Energy Transition Fund from 2019 to 2023.

- Spent six years at Horizon Asset in London, a market-neutral hedge fund.

- Started working with Vidar Kalvoy in 2012.

- Five years in Private Equity at Morgan Stanley.

- Began his investment career in the technology sector at Swedbank Robur in Stockholm in 2006.

- Holds an MSc in Engineering from the Royal Institute of Technology (KTH), Stockholm.

- Portfolio Manager and Founder of the Coeli Energy Opportunities Fund.

- Has managed energy equities since 2006 and brings more than 20 years of experience in portfolio management and equity research.

- Managed the Coeli Energy Transition Fund from 2019 to 2023.

- Head of Energy Investments at Horizon Asset in London for nine years, a market-neutral hedge fund.

- Experience from energy investments at MKM Longboat in London and equity research in the technology sector in Frankfurt and Oslo.

- Holds an MBA from IESE in Barcelona and a Master’s in Business and Economics from the Norwegian School of Economics (NHH).

- Before entering finance, he served as a lieutenant in the Royal Norwegian Navy.

IMPORTANT INFORMATION. This is a marketing communication. Before making any final investment decisions, please refer to the prospectus of Coeli SICAV II, its Annual Report, and the KID of the relevant Sub-Fund. Relevant information documents are available in English at coeli.com. A summary of investor rights will be available at https://coeli.com/financial-and-legal-information/. Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested. Please note that the management company of the fund may decide to terminate the arrangements made for the marketing of the fund in one or multiple jurisdictions in which there exists arrangements for marketing.