This material is marketing communication.

Note that the information below describes the share class (I USD), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class return. The information below regarding returns therefore differs from the returns in other share classes.

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

1) Share Class I USD

FUND MANAGER COMMENTARY

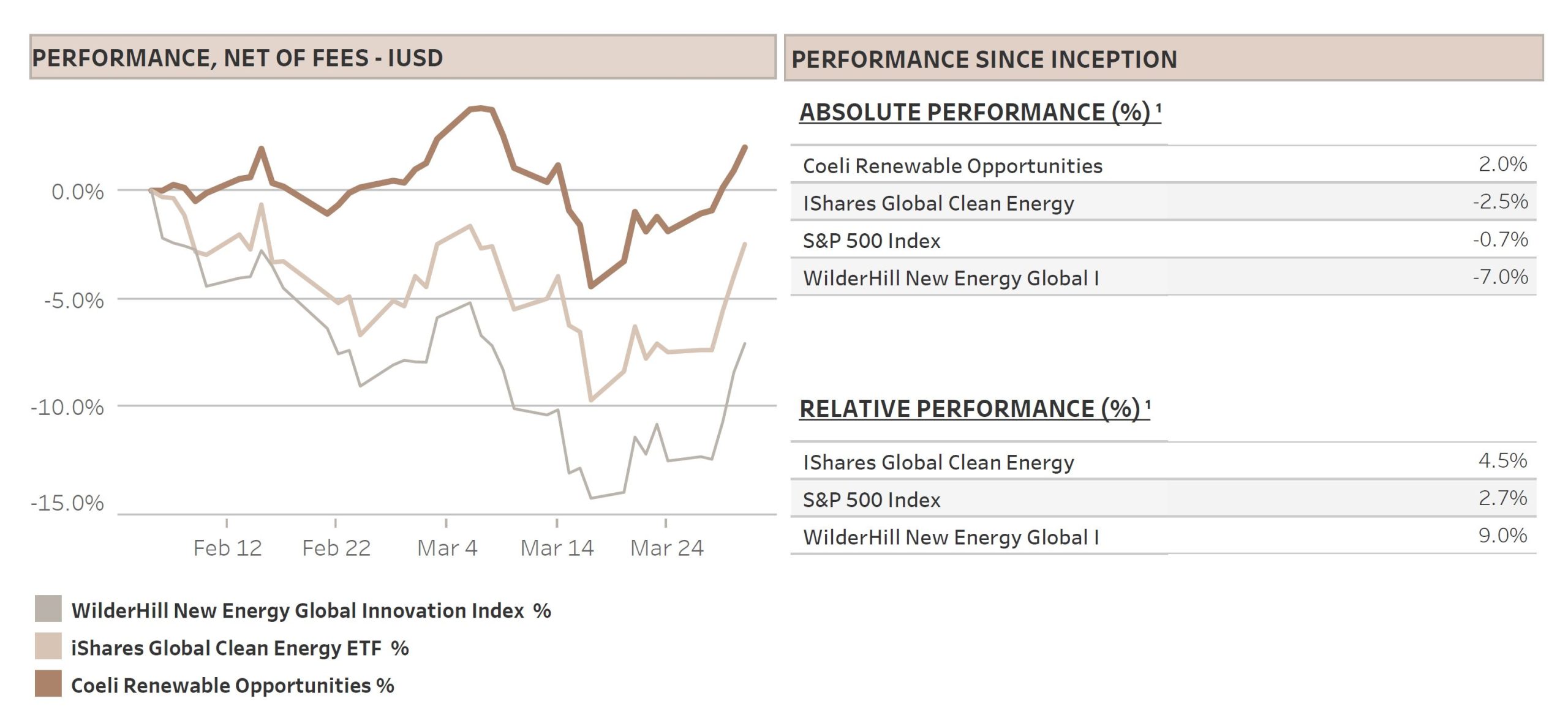

The Coeli Renewable Opportunities fund generated a profit of 1.6% net of fees and expenses in March. It is up 2% since the inception on the 6th of February 2023.

The fund has outperformed the most relevant reference indices, the Wilderhill New Energy Global index (NEX) by 9% and the iShares Global Clean Energy (ICLN) by 4.5% since inception. During March, which was the first full month of operations, the fund outperformed the NEX by 0.8% and underperformed the ICLN by 1.4%.

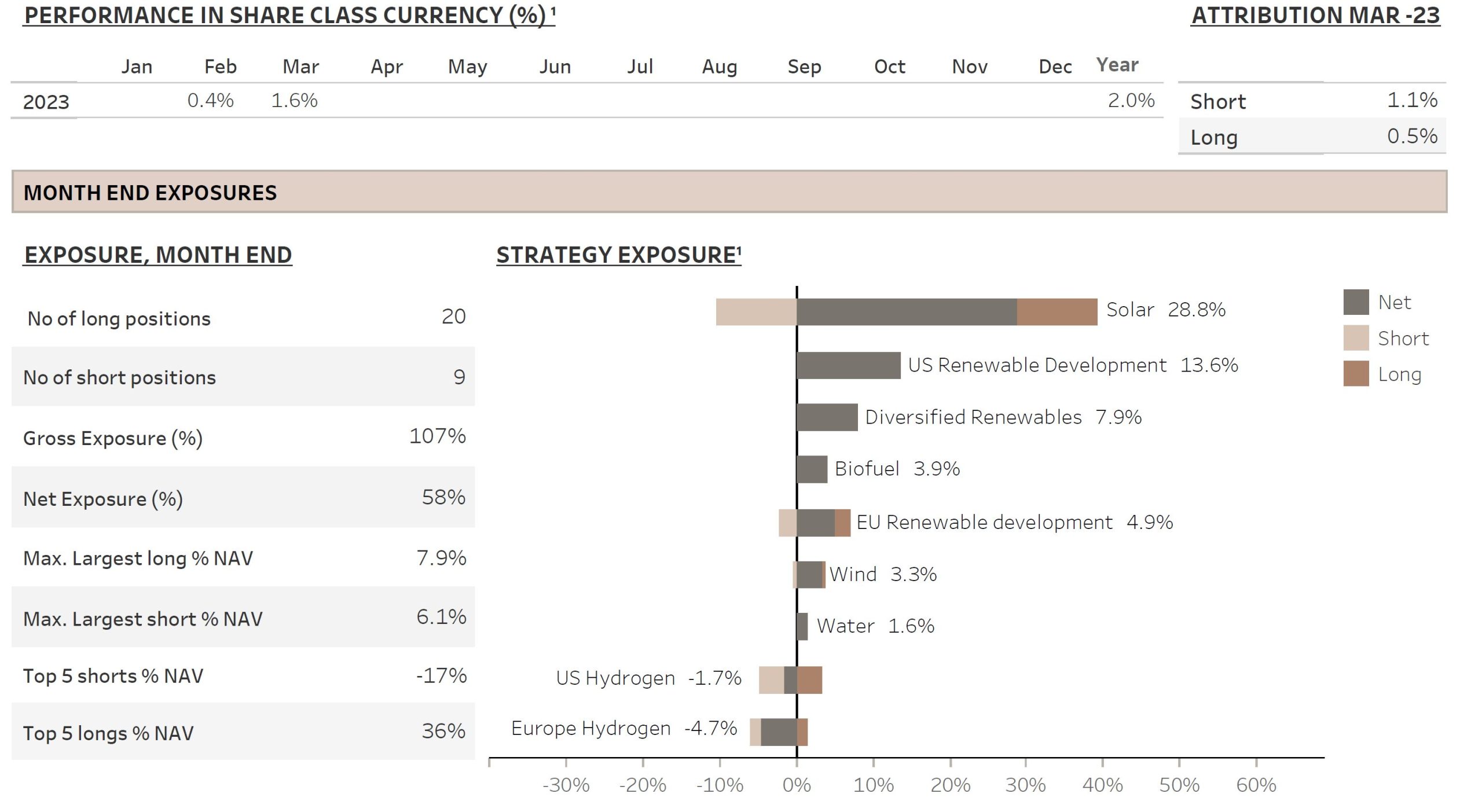

When the net exposure is low, we fully expect the fund’s performance to lag on a relative basis during rallies. During March, the net exposure was about 40-50% as we are still skeptical to the overall market fundamentals. This should be compared to our target net exposure of 40-80%. Still, we tactically increased the net toward the end of the month and closed with a net exposure of 58% and a gross of 107%.

Over time, we expect to generate alpha on both the long and the short side, it was hence encouraging that both contributed positively to March’s performance. The “Solar” theme was the biggest contributor but considering that it had the largest gross and was skewed net long, the theme should have done even better. However, the spreads in the solar space were even larger than normal with the best performer up more than 50% and the worst down almost 20%. The high dispersion increases Solar’s attractiveness as an investment theme. More details on fund performance further below.

MARKET COMMENT – MINI-BANKING CRISIS OR THE BEGINNING OF A LARGER ONE?

March was a volatile month, the S&P 500 traded in a 6.5% range but ended up 3.5%. The big winner however was the Nasdaq which increased by 9.5% and entered a new bull market as it closed 20% higher than the bottom in December. What was the great news? And why did large cap tech companies like Apple, Microsoft, Amazon etc. do so well?

The collapse of Silicon Valley Bank, Signature Bank and later Credit Suisse sent shockwaves through the market, but also pushed the FED to slow the pace of rate increases to 25bps at its March meeting. During the month, expectations of further FED increases were reduced from nearly 125bps of hikes and a peak in September to only a ~70% probability of a 25bps increase in May and close to three 25bps cuts by the end of the year. The expectation is that the stress in the banking system will tighten credit conditions, making it easier for the FED to beat back inflation to the 2% target.

At the same time, the 10-year US Treasury yield which peaked above 4% early in the month dropped to below 3.5% by month-end and has continued down in April. This likely indicates that the market is pricing in higher risk of a recession. Either way, the lower interest rates imply reduced discount rates and higher valuation multiples for equities.

So far, large tech companies with strong margins and low leverage have been the largest beneficiaries of the latest rotation out of financial and cyclicals. Although the lower market discount rate and higher valuation multiples should benefit all equities, the increasing probability of a recession is likely to continue to put pressure on earnings estimates. The market is betting on the decline in discount rates overcompensating for the deterioration in earnings estimates. This is a risky bet as history shows that it is unwise to own equities into a recession, even when the FED is reducing interest rates.

RENEWABLE ENERGY – GRID CONNECTION THE NEXT BOTTLENECK?

The energy transition is experiencing truly unique tailwinds with both the US Inflation Reduction Act and the EU Net Zero Industry Act. We are in the second phase of the renewable energy transformation, which is driven by energy security and safekeeping of supply chains as much as the fight against climate change. In our view, this second phase will be substantially larger and more significant, and it will accelerate the energy transition.

However, it will not be smooth sailing despite the incredibly favorable regulatory backdrop. Last month we talked about the rapid improvements in regulation around permitting, especially in Europe, which has been a key bottleneck. As permitting is about to become less costly and faster the next bottleneck is likely to be grid connection and transmission capacity. When we switch from an energy system that transports a mix of fossil fuels and electricity to one that increasingly transports electricity, it is understandable that the physical wiring requires upgrades. This is true for most regions in Europe and most states in the US. Before a renewable energy project is connected to the grid it requires an approval to connect. These interconnection approvals are becoming more costly and are already prohibitively expensive in some regions.

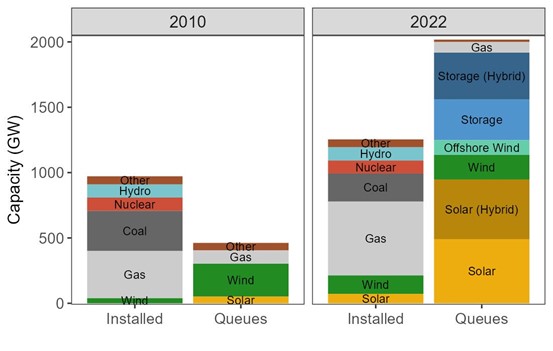

In the US, it is not only an ageing grid, but it is also a political issue as different states have different electrical systems. There are currently close to 2,000 GW of clean energy projects waiting for interconnection in the US, according to Lawrence Berkeley National Laboratory. This is approximately 50% more than the combined output of all the currently operating power plants in the country. See below.

Existing U.S. capacity (2010 and 2022) compared to interconnection queue capacity (2010 and 2022).

Source: Lawrence Berkeley National Laboratory.

The good news is that there is tremendous interest in developing renewable energy projects. The bad news is that the interconnection queue is growing faster than projects are installed. Interconnection times have already increased by 2.5x since the mid-2000s, now averaging 3 years for solar and wind projects in the US. The growth in renewable energy would have been even stronger if not for this issue.

To allow for more connections, the transmission grid requires substantial upgrades and expansion. For example, Bloomberg New Energy Finance (BNEF) estimates that USD 21tn will need to be spent to expand and reinforce the grid to reach net zero by 2050. This is a substantial investment opportunity for the fund.

During March, the FERC (Federal Energy Regulatory Commission) chairman said it is working ‘feverishly’ to advance a transmission reform, a key step in alleviating the grid connections bottleneck. This makes a lot of sense as the projects currently waiting for interconnection are alone enough to reduce US’ Green House Gas emissions in 2030 by 50% from the peak in 2007 and put the country firmly on the path to net zero by 2050. We are hopeful.

FUND PERFORMANCE – MOST THEMES WITH POSITIVE PERFOMANCE

The fund was up 1.6% (I USD) in March with longs contributing +1.1% and shorts +0.5%. Seven out of nine themes were in positive territory, the two losing themes were “Biofuels” and “Diversified Renewables”.

In a month where Nasdaq rallied almost 10%, it is telling that the two themes with only long holdings lost money. The market rally was concentrated in relatively few profitable large tech companies and the renewable energy sector lagged significantly until the last week of the month when heavily shorted unprofitable stocks shot up as well. This reduced the profit in the themes “EU Hydrogen” and “US Hydrogen” which were both skewed net short. However, both themes still contributed positively during the month.

The best performing theme in absolute and relative terms was “Solar”, adding 1.8% to NAV. However, the performance in the theme was mixed with 3 out of 9 longs significantly down, 2 were flat and only 4 rallied with the market. 2 out of 3 shorts were also up on the month. Not pleased with the performance, we are still happy to see this dispersion as it offers great trading opportunities.

The two largest winners were First Solar (FSLR) and Array Technologies (ARRY), but also Solaredge Technologies (SEDG) and Shoals Technologies (SHLS) contributed positively.

FSRL, as we mentioned in the last monthly, is the biggest Inflation Reduction Act (IRA) winner so far. It has a unique position with an already established and largely sold-out US manufacturing capacity as well as a differentiated technology that is not depending on the China dominated polysilicon production. FSLR is also expanding its US capacity and although we are confident that the US panel market will be oversupplied later this decade, we believe FSLR still has fundamental valuation upside as it is trading at 11x P/E ’24 and a PEG ratio of 0.37x based on 2023-2026 CAGR. Importantly, and not very common in the clean technology sector, the company is trading at high teens free cash flow to EV yield in 2025-2026 with the majority of these cash flows already contracted.

ARRY is the leading supplier of tracking systems to utility scale solar in the US. It was our largest loser in February as the shares declined by 16% but recovered nearly everything in March when it reported solid Q4 results.

Near term, we are more optimistic to the utility scale solar market than to the residential solar market, and this month we started building a new position in a company called Shoals Technologies (SHLS). It is the market leader in Electrical Balance of System (EBOS) solutions for utility scale solar energy (essentially the wiring, racking and connection boxes) with a market share of more than 50% in the US. Its products can be installed much faster than the peers’ and without the need for licensed electricians, which constitute a huge cost saving. Moreover, it has sizeable moat through strong IP protection, and it is expanding abroad. We have followed Shoals for some time and feel the timing is right to own the shares as the valuation has become attractive at ~22x ’24 P/E and 0.43x PEG based on 2023-2026 EPS CAGR.

With regards to the shorts in “Solar”, our residential short delivered positive returns, while our utility scale and solar module name shorts contributed negatively to NAV. The utility scale name is a good company, but it is relatively more expensive than the competitors and as it has more earnings uncertainty, we believe the stock should lag. Our module short is simply too expensive relative to FSLR, which in the US market has a massive lead that we expect to continue.

The two losing themes were “Diversified Renewables” and “Biofuels”. Both themes contained only one stock each. In the former, Chart Industries (GTLS), a global manufacturer of equipment used in the production, storage and end-use of industrial gases, hydrogen, carbon capture and water reuse, lagged the market, likely as is does not qualify as large cap tech nor unprofitable tech as it is booking positive earnings and trades cheaply on mid-single digit EV/EBITDA multiples. On the other hand, its debt burden increased substantially when it during Q1 closed the large acquisition of Howden. The high leverage means that the stock generally sells off with highly levered names. Nevertheless, we believe the company will be one of the earliest winners of the IRA and its debt metrics will improve as it gradually integrates Howden. GTLS is one of our largest positions and we believe the stock will regain its pre-Howden valuation, which implies considerable upside to current share price.

In the theme “Biofuels”, our single long, Darling Ingredients (DAR), also significantly lagged the market rally. DAR is a global leader in gathering of feedstock for production of renewable diesel (RD) and it also owns 50% of the Diamond Green Diesel (DGD), the second largest producer of RD in the world. Its near-term earnings estimates have come down somewhat as feedstock prices have come under pressure at the same time as renewable diesel prices have declined with fossil fuel diesel. However, we do not own DAR for the short term. There is a massive expansion of renewable diesel production over the next years and supply of feedstock is unlikely to keep up without significant improvement in prices. DAR is a market leader that controls 15% of current feedstock supply and has through its scale a large margin advantage. Similarly, DGD is the second largest producer of RD in the world and a likely leader in the production of Sustainable Aviation Fuel (SAF), another major market that is about to take off.

We look forward to updating you again at the end of April.

Sincerely,

Vidar & Joel

- Portfolio Manager and Founder of the Coeli Energy Opportunities Fund.

- Over 15 years of investment experience spanning both public markets and private equity.

- Managed the Coeli Energy Transition Fund from 2019 to 2023.

- Spent six years at Horizon Asset in London, a market-neutral hedge fund.

- Started working with Vidar Kalvoy in 2012.

- Five years in Private Equity at Morgan Stanley.

- Began his investment career in the technology sector at Swedbank Robur in Stockholm in 2006.

- Holds an MSc in Engineering from the Royal Institute of Technology (KTH), Stockholm.

- Portfolio Manager and Founder of the Coeli Energy Opportunities Fund.

- Has managed energy equities since 2006 and brings more than 20 years of experience in portfolio management and equity research.

- Managed the Coeli Energy Transition Fund from 2019 to 2023.

- Head of Energy Investments at Horizon Asset in London for nine years, a market-neutral hedge fund.

- Experience from energy investments at MKM Longboat in London and equity research in the technology sector in Frankfurt and Oslo.

- Holds an MBA from IESE in Barcelona and a Master’s in Business and Economics from the Norwegian School of Economics (NHH).

- Before entering finance, he served as a lieutenant in the Royal Norwegian Navy.

IMPORTANT INFORMATION. This is a marketing communication. Before making any final investment decisions, please refer to the prospectus of Coeli SICAV II, its Annual Report, and the KID of the relevant Sub-Fund. Relevant information documents are available in English at coeli.com. A summary of investor rights will be available at https://coeli.com/financial-and-legal-information/. Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested. Please note that the management company of the fund may decide to terminate the arrangements made for the marketing of the fund in one or multiple jurisdictions in which there exists arrangements for marketing.