This material is marketing communication.

Note that the information below describes the share class (I USD), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class return. The information below regarding returns therefore differs from the returns in other share classes.

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

1) Share Class I USD

FUND MANAGER COMMENTARY

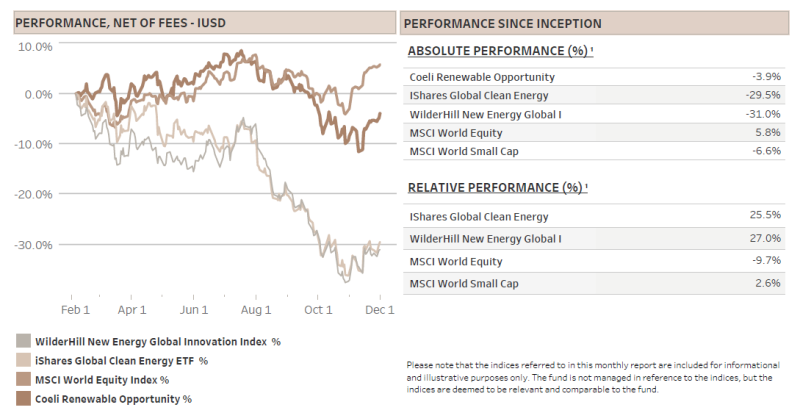

The Coeli Renewable Opportunity fund gained 4.8% net of fees and expenses in November. It is down 3.9% since the inception on February 6, 2023.

November was the fund’s second-best month since inception in February. Although the outperformance to the two most comparable indices, the Wilderhill New Energy Global index (NEX) and the iShares Global Clean Energy (ICLN) was reduced, the fund is still ahead since inception by 26% and 27%, respectively.

We were too early calling for a bottom in early October, but we thankfully stuck to the view that the market and the renewable energy sector were likely set up for some relief into year end. In early November, sentiment and positioning were notably bearish, just ahead of what is traditionally the strongest two-month period of the year. Valuations had become more attractive, and earnings expectations had been reset lower. Supported by macroeconomic tailwinds, including declining inflation and interest rate expectations, the markets experienced one of their best November’s so far this century.

In such a strong rally, most of the performance came from the long side, but it is notable that our short positions only lost 0.4% in November.

MARKET COMMENT – GOLDILOCKS IS BACK!

As the S&P 500 rallied 9% in November, it recovered just about the loss over the prior three months. The main driver was the same as on the way down, i.e. long-term interest rates. Notably, the yield on the US 10-year government bond saw a decrease of 60 basis points during November, marking the steepest absolute monthly decline this century, second only to the drops in November and December of 2008 during the great financial crisis.

Long term rates are plunging due to a combination of rapidly decreasing inflation and a labor market that is only gradually slowing. Most market commentators are confident that not only has the FED hiking cycle ended, but the focus is squarely on the timing of the first cut and the pace thereafter. Goldilocks is back and seemingly stronger than ever.

The market is currently pricing in a more than 50% probability that the FED will cut rates as early as in March next year followed by four more cuts in 2024. As we wrote last month, the S&P 500 has on average gained 16.8% in the 12 months following the last hike, which means that if July 2023 proves to be the last increase, there could be more than 10% upside to the S&P over the next 7-8 months.

While the S&P 500 recovered the previous three-month loss in November, the small cap index, Russel 2000, only recovered about half of its decline. In a scenario of continued S&P 500 gains, we believe it is likely that small caps will do even better and in particular renewable energy stocks as the Wilderhill Index has underperformed the S&P 500 by as much as 40% year to date.

RENEWABLE ENERGY – ARE WE AT THE PRECIPICE OF A NUCLEAR RENAISSANCE?

World leaders are currently gathered at the COP28 summit in Dubai to discuss and improve on measures agreed in previous COP conferences. Of particular importance to us is the commitment made by 118 countries to aim for a threefold increase in the global capacity of renewable energy generation, targeting at least 11,000GW by 2030. Bloomberg New Energy Finance (BNEF) suggests that this ambition would require more than a doubling of annual investments from 2024 to 2030, amounting to a staggering USD 9.4 trillion, which is approximately 10% of the global GDP of 2022. Additionally, BNEF projects that 96% of this investment will be channelled into wind and solar energy, requiring a quadrupling of their combined capacity compared to last year's levels. Obviously, this pledge is not an agreement written in stone, but at a time when many investors question the future of offshore wind and expect limited growth in utility scale solar in western markets, we believe this is a good reminder of the wall of capital about to hit these industries.

Another interesting development, one that probably caught more people’s attention in Sweden, was an ambitious plan among 22 countries, of which Sweden was one of five from western Europe, stating the importance of nuclear energy in achieving global net-zero, and declaring to work for a tripling of nuclear energy capacity by 2050. No doubt an ambitious goal, but it deserves some closer scrutiny and is an opportunity to review the risks and opportunities of nuclear newbuilds for the Coeli Renewable Opportunities fund.

Currently, the world is home to approximately 445 nuclear reactors, collectively generating around 400GW of electricity. The average nuclear reactor has been operational for about 36 years, with some even surpassing the 60-year mark.

Focusing on the future, tripling the global capacity would take us to 1,200 GW by 2050, nearly 9,000 Terawatt hours (TWh) a year at 85% utilization, i.e. almost three times the EU’s current annual electricity consumption. However, what matter is global consumption and its expected total in 2050. According to ThunderSaid Energy, an energy consultancy, the world will consume about 120,000TWh of usable energy in 2050, which means that nuclear energy, if it hits these targets, would account for about 7.5% of total energy supply. This is significant and it would help the decarbonization journey, however it is a journey clearly led by renewable energy.

In any case, nuclear will be an interesting investment opportunity, one that has been on our radar for a while. However, it warrants a cautious approach. The journey towards nuclear development has historically been fraught with financial risks, as evidenced by several stalled or over-budget projects in the Western world.

The Vogtle project in the US, originally budgeted at USD 6.1 billion for a 2016 startup, has been plagued by delays and cost overruns, now expected to be finalized in 2024 with a ballooned budget well in excess of USD 30 billion. Similarly, the UK's Hinkley Point C, the first new British nuclear reactor in over three decades, has encountered its share of hurdles. Starting in 2012 with an estimated cost of GBP 16 billion, its latest completion timeline has been pushed to 2027, with costs likely reaching GBP 33 billion. Few would be surprised if the total cost ends even higher.

Lastly, France's EDF Flamanville EPR project and Finland's OL3 project were both more than a decade delayed and saw costs four and three times higher respectively than in the original budget. Building nuclear plants in the west have plainly been a high-risk activity for everyone involved over the last 20 years.

Advocates of nuclear energy however point to a number of different reasons why each project failed and that countries like South Korea do in fact manage to construct power plants on time and on budget. Why should not the west be able to do the same? Maybe it will with time, but historical evidence points squarely in one direction for now. We do hope this will change.

Digging a little bit deeper, an interesting new development is the advent of Small Modular Reactors (SMRs). Many experts claim they will be less expensive as the modules can be manufactured in factories where learning curves will be steeper. It certainly seems reasonable that the reactor pressure vessel could become cheaper over time if many identical units were produced.

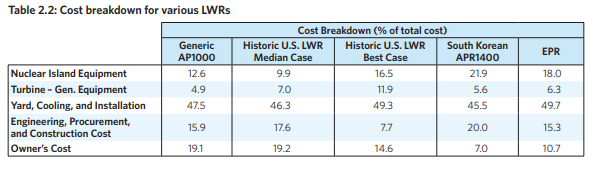

However, a 2018 study by the Massachusetts Institute of Technology (MIT) sheds light on a critical aspect: the nuclear island, comprising the reactor pressure vessel, piping, steam generator etc, accounts for merely 13% of a nuclear power plant's capital cost (AP1000 reactor). The bulk of the expenses are tied up in the yard, cooling, and installation work. This could imply that a shift to numerous smaller reactors might inadvertently hike overall costs due to the proliferation of facilities and more yard work. See below for MIT’s overview of common reactor designs and costs breakdown.

Source: The Future of Nuclear Energy in a Carbon-Constrained World – MIT 2018

SMRs will surely have their share of teething problems but hopefully the standardized module design can over time also streamline the more important yard, cooling, and installation work.

While nuclear power undoubtedly offers a carbon free energy solution, the high stakes involved in nuclear projects call for a thoughtful approach. Beyond the financial implications, the spectre of nuclear accidents, like the infamous Chernobyl disaster of 1986 and the Fukushima Daiichi crisis of 2011, looms large, highlighting the potential hazards of this technology. Newer designs with better passive safety systems are showing promise, though.

Moreover, nuclear power remains a polarizing issue, with critics pointing to its high costs, safety concerns, and the unresolved dilemma of radioactive waste disposal. In contrast, renewable energy presents a safer alternative with better track record of cost reductions along with more straightforward financing options.

However, the prospect of developing nuclear energy in colder countries like Sweden could be rational. In these regions, nuclear power can provide a stable, reliable source of energy to cope with the high energy demands during long, cold winters. This is particularly relevant when renewable sources like solar and wind may at times be less reliable or efficient due to weather conditions. Additionally, the geographical stability, the public support, and the advanced technological infrastructure of countries like Sweden could mitigate some of the safety and logistical concerns associated with nuclear energy.

While we are optimistic about nuclear energy being part of the carbon-free energy mix and hope that it will be feasible to construct nuclear plants in Europe on time and within budget, the historical evidence suggests caution. As investors, we plan to observe these developments with keen interest from the sidelines, at least in the initial stages.

FUND PERFORMANCE – SECOND BEST MONTH ON RECORD

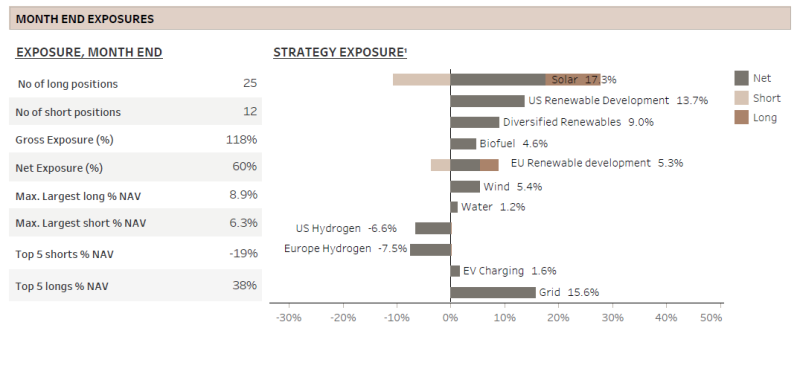

The fund gained 4.9% (I USD) in November as two thirds of the themes contributed positively, long positions made 5.3% and shorts lost 0.4%. Considering the strong market rally, we are pleased to have limited the losses in the short book, especially since net exposure was in the 60-65% range most of the month. The month ended with a net exposure of 60% and a gross exposure of 118%.

The two best performing themes in November were not surprisingly the largest losers from the last month. The “Grid” theme added 1.8% to NAV as all 5 stocks made a positive contribution, but in particular NKT A/S (NKT) which was up 20% in November and ended the month on an all-time high. In several past monthly reports, we have highlighted the especially favorable risk-reward profile we perceive in suppliers of transmission and distribution networks.

The “Solar” theme contributed 1.3% to NAV, clawing back only about a third of the large loss from October. The culprits were our two large utility scale positions in Array Technologies (ARRY) and Shoals Technologies (SHLS). Both companies reported earnings early in November and took a double digit hit on the day. The stocks had by the end of November only recovered about half of their losses, despite the rally and the fact that 2024 EBITDA estimates declined only by low single digits. Shoals’ 2023 EBITDA is even 10% higher than prior to the Q3 results, which means that the stock trades at half the multiple it did as late as in July this year. We detailed in the last monthly why we are still positive to the long-term growth in the utility scale solar sector and why we find the valuations of ARRY and SHLS in particular to be attractive.

The “Wind” theme also had a good month as it added 0.8% to the NAV. We have consistently appreciated Vestas Wind Systems'(VWS) strong competitive standing, but we have been reluctant to size the position as the company navigates through low-margin legacy projects. Despite the stock’s relatively high valuation, Vestas stands out in the broad renewable energy sector with a very strong market position. Furthermore, we anticipate a surge in US onshore wind order intake in the upcoming quarters and with Siemens Energy (ENR) temporarily out of the picture, Vestas is likely to expand its market share.

Moreover, Nordex (NDX1), a smaller German competitor that we also own, will likely also gain from the pickup in US onshore wind activity. However, Nordex is not involved in offshore wind, where Vestas maintains a leading role together with General Electric (GE), especially as ENR grapples with its legacy projects and technology development challenges. Both VWS and NDX1 still have a couple of quarters ahead of them with weaker margins as the largest and most difficult legacy projects initiated at lower prices during the pandemic are coming to an end. Nevertheless, by the end of 2024 and moving into 2025, we foresee both companies approaching their ambitious margin goals.

The “US Renewable Development” theme which consists of only Nextera Energy (NEE) and AES, contributed 0.7% to NAV as both stocks continue to recover after the massive interest rate induced sell-off in the third quarter. We maintain that both companies are among the best positioned renewable development companies in the US and in the world. AES has recovered about two thirds of its losses since the US 10y Treasury yield rose above 4% in early August while NEE still has only recovered about half. We are staying long and have increased both positions.

The two most significant detractors in our portfolio were, as expected, the hydrogen-focused themes “US Hydrogen” and “European Hydrogen,” which reduced the NAV by 0.4% and 0.3%, respectively. Given the surge in renewable stocks and considering that both themes consist exclusively of short positions, we are satisfied that only one short position outperformed slightly the NEX index. Additionally, two stocks actually declined over the month, despite the short squeeze driven rally.

Our outlook on the hydrogen sector remains cautious. We believe that the long-term demand projections are increasingly uncertain, showing a noticeable retreat from last years’ optimistic forecasts. The industry is also coming to terms with the high risks associated with pioneering 100MW+ systems – risks that neither buyers nor sellers seem willing or, in many cases, capable of shouldering, particularly in terms of construction and startup. Consequently, we continue to anticipate a downward adjustment in revenue projections and correspondingly, a reduction in valuation multiples.

We look forward to updating you again next month.

Sincerely,

Vidar Kalvoy & Joel Etzler

- Portfolio Manager and Founder of the Coeli Energy Opportunities Fund.

- Over 15 years of investment experience spanning both public markets and private equity.

- Managed the Coeli Energy Transition Fund from 2019 to 2023.

- Spent six years at Horizon Asset in London, a market-neutral hedge fund.

- Started working with Vidar Kalvoy in 2012.

- Five years in Private Equity at Morgan Stanley.

- Began his investment career in the technology sector at Swedbank Robur in Stockholm in 2006.

- Holds an MSc in Engineering from the Royal Institute of Technology (KTH), Stockholm.

- Portfolio Manager and Founder of the Coeli Energy Opportunities Fund.

- Has managed energy equities since 2006 and brings more than 20 years of experience in portfolio management and equity research.

- Managed the Coeli Energy Transition Fund from 2019 to 2023.

- Head of Energy Investments at Horizon Asset in London for nine years, a market-neutral hedge fund.

- Experience from energy investments at MKM Longboat in London and equity research in the technology sector in Frankfurt and Oslo.

- Holds an MBA from IESE in Barcelona and a Master’s in Business and Economics from the Norwegian School of Economics (NHH).

- Before entering finance, he served as a lieutenant in the Royal Norwegian Navy.

IMPORTANT INFORMATION. This is a marketing communication. Before making any final investment decisions, please refer to the prospectus of Coeli SICAV II, its Annual Report, and the KID of the relevant Sub-Fund. Relevant information documents are available in English at coeli.com. A summary of investor rights will be available at https://coeli.com/financial-and-legal-information/. Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested. Please note that the management company of the fund may decide to terminate the arrangements made for the marketing of the fund in one or multiple jurisdictions in which there exists arrangements for marketing.