This material is marketing communication.

Note that the information below describes the share class (I USD), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class return. The information below regarding returns therefore differs from the returns in other share classes.

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

1) Share Class I USD

Performance for other share classes towards the end of the report.

FUND MANAGER COMMENTARY

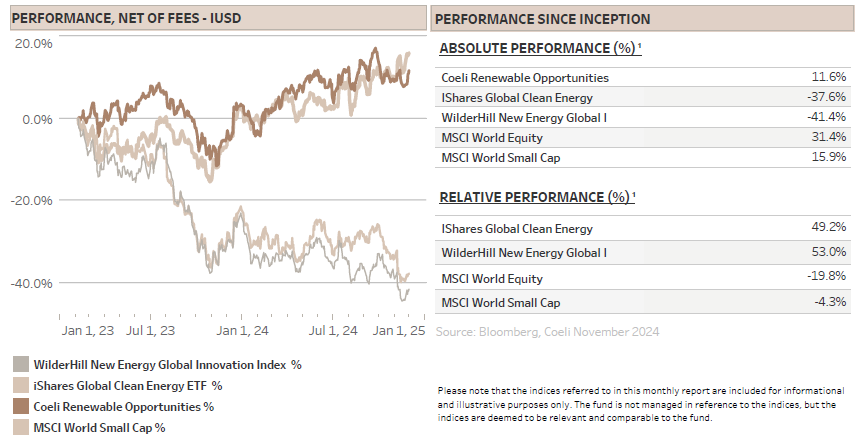

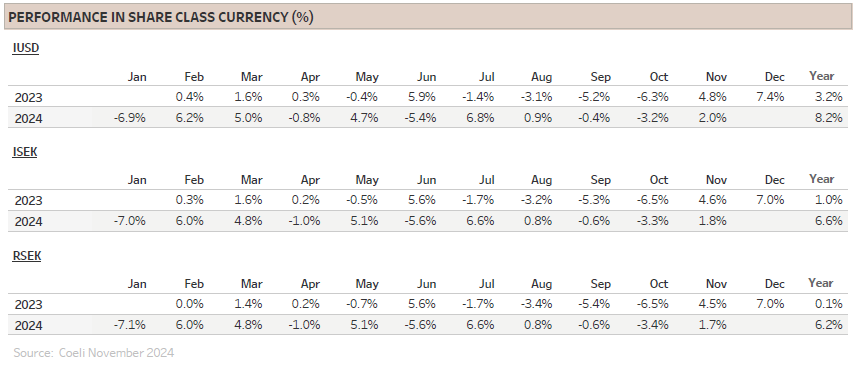

The Coeli Renewable Opportunities fund gained 2.0% net of fees and expenses in November (I USD share class). It has increased 8.2% year to date and is up 11.6% since the inception in February 2023.

In November, the fund outperformed the most comparable indices, the Wilderhill New Energy Global index (NEX) and the iShares Global Clean Energy (ICLN) by 6.0% and 7.4% respectively. It extended the year-to-date outperformance to 31% and 28%, respectively and the fund is ahead by 53% and 49% since the inception in February last year.

For our Swedish investors, we remind you that our SEK denominated share classes are currency hedged and therefore not affected positively or negatively by the change in the USDSEK rate.

November was all about the US election. Although having derisked into the election-night, the fund was inevitably skewed towards the so-called Harris-trades and faced losses as the worst outcome, a Republican sweep, seemed likely the next day. However, following a carefully prepared trading plan, we managed to reduce the next day loss to 0.4% versus a fall of 6-11% for the renewable energy indices.

During the rest of the month, the volatility was high, and dispersion set new records as the worst-case scenario was priced into many stocks while others followed the broad market indices and hit all-time highs. It was not a surprise that the ‘Diversified Renewables’ theme was the best performer in November, adding 4.4% to NAV, as it contained only stocks that were either neutral to the election outcome, like Chart Industries (GTLS) and Siemens Energy (ENR) or direct beneficiaries like the bitcoin miners. Surprisingly, the worst performing theme was ‘Grid Equipment’ which lost 1.8% of NAV despite having limited ‘Harris-risk’. Instead, as it includes mainly European names, it might have suffered from the selloff in Europe versus the US post the election.

We are pleased to have moved past the binary risks associated with the U.S. election. While a Trump presidency introduces some uncertainty for the renewable energy sector, the range of outcomes has narrowed after the election and total risk is reduced. Additionally, we anticipate that dispersion among the various sub-sectors will remain elevated, creating a favorable environment for our stock-picking, long/short strategy.

MARKET COMMENT – MASSIVE OUTPERFORMANCE IN US VS EUROPE

The S&P 500 rose 5.7% in November, its best month in 2024, increasing the year-to-date returns to more than 26%. In contrast, European markets struggled, with the Eurostoxx 50, Europe’s leading blue-chip index, losing 1% in November.

The primary driver of US outperformance over Europe was, of course, the US election outcome. A Trump presidency is widely expected to bring lower corporate taxes for US companies, potentially offset by tariffs on European exports to the US. However, the US outperformance extends beyond the election. 2024 was already shaping up to be one of the strongest for US stocks relative to their European counterparts since the Reagan presidency in the early 1980s.

Investor risk appetite in the US stock market remains robust as we head into December, traditionally a strong month for equities. Meanwhile, the bond market appears to be pricing in a soft landing, with inflation under control and a balanced labor market. This backdrop supports expectations for 2-3 additional Federal Reserve rate cuts, including one anticipated in December.

Nevertheless, political uncertainties surrounding the Trump administration's potential policies, such as tariffs on friends and foes alike, the deportation of illegal immigrants, and significant unfunded tax cuts, could lead, we believe, to a repricing of risk after President Trump’s inauguration in mid-January next year.

RENEWABLE ENERGY – THE URGENCY TO SECURE POWER

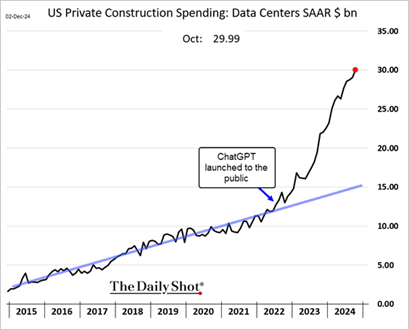

The demand for electricity driven by AI is surging at an unprecedented pace. Since the introduction of ChatGPT, spending on data centers (DCs) has skyrocketed, showing no signs of slowing down.

Source: TheDailyShot, The United States Census Bureau

While the easy-to-develop sites for data centers have been claimed, the next phase of expansion will be more challenging. As discussed in previous reports, such as March 2024’s ‘Roadblocks on the AI Highway’, the single greatest obstacle to AI growth is securing grid connections and reliable power supplies.

Electrical grids across the US are congested, with regulators increasingly voicing concerns that DCs are consuming disproportionate amounts of power, potentially driving up energy costs for consumers. This is facing increasing resistance, and the Chairman of the Public Utilities Commission of Texas (PUCT) recently stated that DC developers will need to supply generate some of their own power since "they can afford it." This concept of asking large users like hyperscalers to add their own power is known as ’additionality’ and it is gaining traction across the US.

A recent notable example is Microsoft’s 20-year Power Purchase Agreement (PPA) with Constellation Energy (CEG), a holding in the fund, to restart a reactor at the Three Mile Island nuclear power plant that was shuttered as recently as in 2019. While the costs of the deal are substantial and Microsoft is paying a significant premium over grid prices, the agreement appears to be a clear win for both Microsoft and Constellation Energy (CEG).

However, opportunities like this are limited, and innovative DC developers are increasingly willing to pay ever-higher premiums for power that is immediately available. This strategy makes sense, as the high capital costs of DCs and their expected returns make ‘time to power’ far more critical than the ‘cost of power’. Until clearer data emerges on the returns from these investments, we expect this trend to continue.

On the current trajectory, DC power demand is likely to significantly outpace potential supply over the next years. Morgan Stanley projects a staggering 36GW power shortfall for US DCs between 2025 and 2028. This is more than twice Sweden’s total electricity consumption. The estimate, based on anticipated 57GW of DC power demand from AI hardware investments less the power secured from DCs already under construction, highlights the critical challenge ahead.

Source: Morgan Stanley

Although this is a crude calculation, we believe it is directionally accurate and worth investigating the different options available to data center (DC) owners to address their growing power demands.

1. Renewable Energy: A Partial Solution

Hyperscalers, the largest owners of DCs, have ambitious decarbonization targets and would prefer to rely solely on renewable energy, even at premium prices. Unfortunately, renewable energy alone cannot meet DCs’ constant load requirements. Batteries can help smooth fluctuations but are currently too expensive and slow to deploy at the necessary scale.

Renewable energy, therefore, can only be part of the solution, requiring either a robust grid connection or other forms of power backup. On the bright side, hyperscalers are likely to continue to drive demand for renewable Power Purchase Agreements (PPAs) to offset emissions from other power sources. However, current demand for renewables already far outpaces supply, which is hindered by permitting delays, lack of grid access, and equipment shortages. These are logistical challenges and will be resolved over time. The fund is positioned to benefit from this trend through investments in leading US renewable developers such as NextEra Energy (NEE) and AES.

2. Nuclear Power: Limited Potential

Could nuclear energy fill the gap? While notable examples like Microsoft’s deal to restart a reactor at Three Mile Island are promising, these opportunities are rare. Only a handful of shuttered reactors are supposedly economically viable for reactivation, and all are likely less attractive than Three Mile Island.

What about new large-scale nuclear reactors? The few that have been built in the West the last decades have taken literally decades to build and with huge cost overruns. Either way, they would not be a solution for time constrained DC owners.

A better option might be Small Modular Reactors (SMRs) that come with outputs of about 200-300MW and the promise of lower costs and shorter construction time. In fact, hyperscalers like Google and Amazon are already supporting SMR startups, although we question the authenticity of their backing. Neither of these SMR startups have approval from the Nuclear Regulatory Commission (NRC), which easily could take at least four to five years. Since financial commitments are not until the construction phase, any cash outlays are many years into the future. This could resemble a cheap PR option, and we can only wonder why they did not decide to back more established SMR companies. In any case, new nuclear solutions are unlikely to address the immediate power shortage and significant contributions are likely a decade or more away.

3. Natural Gas: A Practical Stopgap

Natural gas, which currently accounts for nearly 45% of US electricity generation, offers a readily available resource to meet DC demands. While it is not a clean energy source, it emits less carbon than coal and could serve as a decent power option even from a climate perspective when paired with renewables and batteries.

Despite its advantages, natural gas infrastructure is arduous and time consuming to develop. Power plants take more than five years to construct, and pipelines require often even longer to plan, permit and build. However, the Trump administration’s favorable stance on domestic fossil energy development will likely accelerate these projects.

For example, META recently announced plans to construct a USD 10 billion AI-focused DC in Louisiana, near three new natural gas-fired power plants being built by Entergy at a cost of USD 3.2 billion. This will be METAs largest data center globally. However, note that META is sticking to its decarbonization target and has committed to offsetting 100% of its electricity use with clean, renewable energy. The fund stands to benefit from the buildout of gas infrastructure through investments in companies like MasTec (MTZ), Chart Industries (GTLS), and Siemens Energy (ENR).

4. Fuel Cells: An Emerging Solution

With the low hanging fruits picked, innovative approaches such as fuel cells are gaining attention. For instance, AEP, a major US utility, recently agreed to purchase up to 1 GW of fuel cells from Bloom Energy, a leading manufacturer in the space. While these fuel cells are primarily powered by natural gas, they produce fewer air pollutants and similar greenhouse gas (GHG) emissions compared to traditional gas power plants. Moreover, they could eventually transition to green hydrogen, however we doubt this will happen any time soon.

Bloom Energy still needs to prove that its fuel cells can scale effectively to meet the rigorous uptime requirements of DCs. Nevertheless, given the lengthy procurement times for gas turbines, fuel cells may emerge as a vital stopgap as energy demand continues to grow. The fund is closely monitoring developments in this space.

5. Repurposing Industrial Sites and Bitcoin Mining Facilities

Another innovative approach is repurposing existing industrial sites with substantial grid connections and ample land resources. Sites of soon-to-be-closed industrial facilities that are no longer economically viable are ideal candidates. The profitability of the DC business is so high that it may even make sense to acquire less profitable businesses solely to convert their land and energy infrastructure for DC use.

One particularly intriguing solution involves targeting bitcoin miners. These companies often own large sites with high grid power connections and long-term contracts for clean energy. In some cases, it might even make sense to shut down bitcoin mining operations and repurpose these facilities for High-Performance Computing (HPC) DCs. The fund has invested in a few bitcoin miners for this reason.

Conclusion: An "All of the Above" Approach

To sum up, we believe that addressing the power shortfall will likely require an “all of the above” approach. From renewables and batteries to nuclear, gas, and innovative technologies, every avenue will have to be explored. As long as the market is willing to fund the continued expansion of AI development, the race to secure reliable power will remain intense, shaping the future of the energy market.

FUND PERFORMANCE – STRONG TRADING POST THE ELECTION

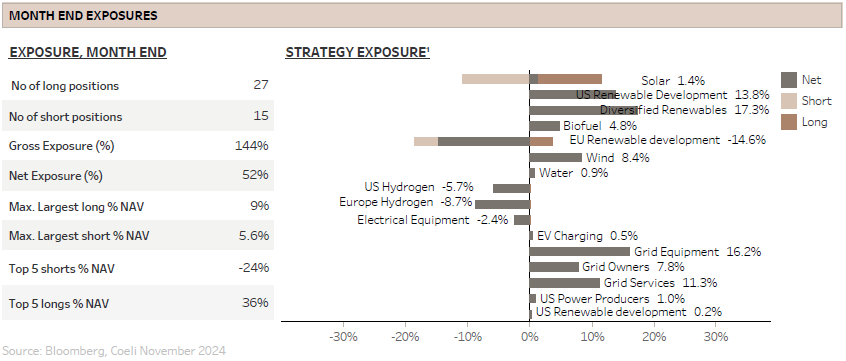

In a trading-intensive month where the renewable indices sold off by 8-10%, we are pleased that the contribution from our long positions contributed positively, adding 0.6% to performance as the fund delivered a net return of 2% after fees. Generating alpha on both the long and short sides is the ultimate objective of our long-biased long/short strategy, and November was in that sense a good example.

The net exposure was 44% going into election night, reduced to 40% the following day, and then gradually increased to 50% by month-end as we made significant adjustments across most of our investment themes. At 50%, our net exposure remains below the midpoint of our target range of 40-80%, reflecting a cautious stance toward our investment universe despite entering a seasonally strong period toward year-end. Gross exposure began the month in the 110-115% range and ended close to 140%, reflecting increased conviction in our portfolio adjustments.

In a month were more than half of the themes lost money, it was ‘Diversified Renewables’ that saved the performance by contributing 4.4% to NAV. All holdings are long and all did well, although our long-standing favourite energy transition stock Chart Industries (GTLS) stood out. We have discussed this name in many previous monthly reports and with its still significant exposure to natural gas and LNG, two areas that should face an improved regulatory environment under a Republican administration, we expected it to have upside risk on a Trump win, although 30% gain post-election was a positive surprise.

Siemens Energy (ENR) also increased significantly during the month, although partly due to a positive third quarter report with strong mid-term guidance. ENR is addressing some of the most critical bottlenecks in grid expansion, and with few competitors and high barriers to entry, we expect its fundamentals to continue improving in the coming years.

Finally, as discussed earlier, we own some bitcoin miners due to their access to power and grid connections. However, since Trump was promising laxer regulation and possibly crypto currency acceptance by the US government, we believed it was likely that bitcoin would rally and drag along the bitcoin miners. We added to these names post the election, but we are watching the positions very carefully as we are awaiting the first DC power deals for bitcoin miners.

The second-best performing theme was ‘EU Hydrogen,’ which consists entirely of short positions and added 2.3% to NAV in November. As we have extensively discussed in previous reports, we remain skeptical about the economic viability of many green hydrogen use cases. A lack of large contracts and reduced government support for subsidies continue to validate our view. Interestingly, the ‘US Hydrogen’ theme was up in November, likely driven by concerns over a potential short squeeze. The market anticipate that the Biden administration might finalize Inflation Reduction Act (IRA) tax credit details for hydrogen before President Trump’s inauguration. While such a move is possible, we doubt the finalized guidelines will be generous enough to trigger large-scale investment decisions, particularly as these would still be subject to Congressional review and vulnerable to changes under a Republican-controlled Congress.

The worst-performing theme in November was ‘Grid Equipment,’ which declined by 1.8% of NAV. This theme consists primarily of European names focused on selling and installing cables for the transmission and distribution grids. Since there is bipartisan support for strengthening the grid, the weak performance is not really due to the election outcome, but rather stem from profit-taking after a strong run, an exhaustion in earnings upgrades, and tempered medium-term expectations as new capacity ramps up over the coming years. Additionally, underperformance may have been influenced by the poor performance of European stock markets relative to the US in November. Supporting this view, our ‘Grid Services’ theme, comprising US-listed companies focused on installing and servicing the grid, gained 0.8% during the month, with all stocks in the theme delivering positive returns.

The second-worst performing theme was ‘US Renewable Development,’ dragged down primarily by AES, which is perceived as vulnerable to potential IRA tax credit rollbacks and elevated interest rates. As we outlined in last month’s report, we remain skeptical that tax credits important to AES will be removed. Even in a worst-case scenario, over half of AES’s backlog is with the hyperscalers, who have the capacity and willingness to pay higher prices for power. Importantly, it is not high costs that is currently holding back developments of renewable energy, but rather bottlenecks in permitting, grid access, and equipment shortages.

Similarly, if interest rates should stay elevated it would entail higher costs of doing business, but the industry can adapt as long as end customers continue to see value in renewable power. Of course, the net present value of already locked in cash flows are worth less at higher rates, but the market priced that in quickly as AES fell about 30% since the long-term rates bottomed in late September.

The ‘Solar’ theme also detracted, losing 1.2% of NAV in November. Losses could have been much worse if we had not quickly offloaded most of our residential solar positions before markets opened the day after the election. Residential solar tax credits face significant headline risk under a Republican-controlled Congress seeking to cut IRA spending. While we doubt these credits will be eliminated without replacements, the near-term downside risk outweighs the potential upside, making these positions unattractive. However, we are refraining from shorting these names due to their high short interest and significant fundamental upside if the tax credits remain intact.

Conversely, despite high short interests, we are still shorting solar companies with links to China and a large revenue share from the US market. It is hard to imagine the Republican controlled Congress at least not discussing severe policies against Chinese import and ownership of US assets.

The only solar stock we are still comfortable owning is the IRA winner First Solar (FSLR). The stock initially sold off after the election, as a Republican sweep was perceived as the least favorable scenario. We used that opportunity to increase our position. As the market has grown more confident that FSLR’s manufacturing tax credits will remain intact, the stock has shown resilience. With FSLR being the largest domestic producer of solar panels, it is uniquely positioned to benefit from both IRA incentives and potential new tariffs on imports. If the stars align, FSLR could find itself in the rare position of benefiting significantly from both the IRA and Trump’s tariff policies.

Sincerely

Vidar Kalvoy & Joel Etzler

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

- Portfolio Manager and Founder of the Coeli Energy Opportunities Fund.

- Over 15 years of investment experience spanning both public markets and private equity.

- Managed the Coeli Energy Transition Fund from 2019 to 2023.

- Spent six years at Horizon Asset in London, a market-neutral hedge fund.

- Started working with Vidar Kalvoy in 2012.

- Five years in Private Equity at Morgan Stanley.

- Began his investment career in the technology sector at Swedbank Robur in Stockholm in 2006.

- Holds an MSc in Engineering from the Royal Institute of Technology (KTH), Stockholm.

- Portfolio Manager and Founder of the Coeli Energy Opportunities Fund.

- Has managed energy equities since 2006 and brings more than 20 years of experience in portfolio management and equity research.

- Managed the Coeli Energy Transition Fund from 2019 to 2023.

- Head of Energy Investments at Horizon Asset in London for nine years, a market-neutral hedge fund.

- Experience from energy investments at MKM Longboat in London and equity research in the technology sector in Frankfurt and Oslo.

- Holds an MBA from IESE in Barcelona and a Master’s in Business and Economics from the Norwegian School of Economics (NHH).

- Before entering finance, he served as a lieutenant in the Royal Norwegian Navy.

IMPORTANT INFORMATION. This is a marketing communication.

Before making any final investment decisions, please refer to the prospectus of Coeli SICAV II, its Annual Report, and the KID of the relevant Sub-Fund. Relevant information documents are available in English at coeli.com. A summary of investor rights will be available at https://coeli.com/financial-and-legal-information/.

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

Please note that the management company of the fund may decide to terminate the arrangements made for the marketing of the fund in one or multiple jurisdictions in which there exists arrangements for marketing.