This material is marketing communication.

Note that the information below describes the share class (I USD), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class return. The information below regarding returns therefore differs from the returns in other share classes.

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

1) Share Class I USD

FUND MANAGER COMMENTARY

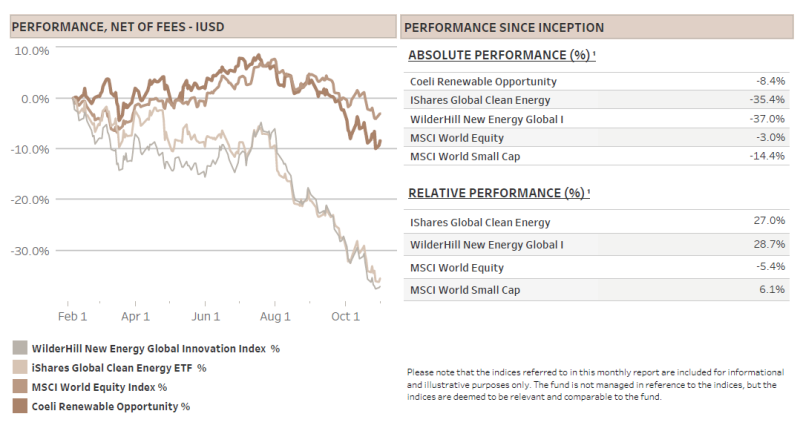

The Coeli Renewable Opportunity fund lost 6.3% net of fees and expenses in October. It is down 8.4% since the inception on February 6, 2023.

Even with October's steep drawdown, the fund’s outperformance keeps growing. Relative to the two most comparable indices, the Wilderhill New Energy Global index (NEX) and the iShares Global Clean Energy (ICLN), the fund expanded its margin of outperformance by 7.3% and 4.8%, respectively. As these indices are down by about 30% over the last three months, booking their worst 3-month period for more than 10 years, the fund has successfully bolstered its cumulative outperformance since inception to 29% against the NEX and 27% versus the ICLN.

Last month we argued that certain companies in the renewable universe were about to find a bottom, and in early October we increased our net exposure from the low 40% to the low 70%. As the fund aims to have a net exposure in the 40-80% range, it means we went from bearish to bullish within a week. In hindsight, this was clearly wrong or at least too early. Despite the dismal sentiment and bearish market positioning at the time, it seems like the market’s concerns can always get worse.

Nevertheless, we still believe the sector could experience some relief into the year-end. First, seasonality is strong with November and December historically the best 2-month period of the year. Second, while sentiment and positioning are still negative, valuations have become less challenging as share prices have slumped significantly the last months. Third, earnings estimates for many companies have been reset lower while sell-side analysts’ have finally slashed their price targets.

Finally, there is a consensus among economists that long-term interest rates may have reached their zenith. Should rates begin to stabilize or even recede, sectors that have been hardest hit in recent months could see renewed investor interest. Morgan Stanley's thematic strategies analysis indicates that the Renewable theme has been the worst performer since long-term rates began their sharp ascent in August.

MARKET COMMENT – IT IS ALL ABOUT LONG-TERM YIELDS

The S&P 500 experienced a 2.2% decline in October, marking its third consecutive monthly fall—a rarity observed just once in the past decade during the COVID-19 pandemic. Such an event normally occurs with major macroeconomic events, last time coinciding with the Eurozone crisis in 2011 and the global financial crisis in 2008.

The main culprit this time is increasing long term government rates. The US 10-year Treasury bond briefly traded above 5% yield and ended October at 4.9%. As outlined in our last monthly report, numerous factors are driving this uptick in rates. A key one is the unexpectedly robust performance of the US economy, which reported an almost incredible 4.9% GDP growth in the third quarter, coupled with strong job creation while inflation is concurrently receding towards FEDs target of 2%.

Although higher interest rates mechanically lower valuation of all assets, the ‘good news’ for the stock market, assuming that the high rates does not cause a recession, is that the higher long-term rates have tighten financial conditions to a point that the bond market no longer expect further FED hikes. Historically, the S&P 500 has gained on average 16.8% in the 12 months following the prior six conclusions to FED tightening cycles – far outperforming the index’s historical return.

RENEWABLE ENERGY – LONG TERM CASE FOR RENEWABLES IS INTACT

Last month we wrote “there is blood in the streets” and we tactically increased our net exposure. We may be wrong, or just early, but for the first time in many years, there is strong valuation support in many of the great companies involved in the energy transition.

Nevertheless, this year has presented a complex narrative for investors. Are renewable energy investments something that only works when interest rates are zero? Or is the energy transition just a big hoax? The answer to both questions is no.

In the last monthly, we explained why renewable developers would be able to incorporate the higher cost of capital and still make good returns on their investments. In this report, we will discuss the longer-term structural opportunity which is unique to the energy sector.

Even though fighting climate change and ESG are important factors to mention, they pale in comparison to the need to grow energy supply to meet increasing demand. We need more gigawatts of energy, period.

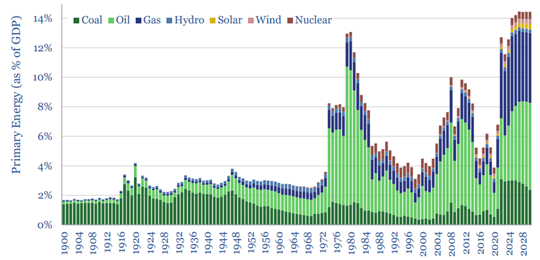

The year 2022 marked a critical inflection point in the global energy landscape, revealing the vulnerability of our energy systems, in particular to geopolitical shocks. Primary energy consumption, a measure of the total energy consumed across all energy sources, surged to over 12% of global GDP, according to Goldman Sachs, and even higher in Europe, from a 5-6% average since the mid 1980’s. This signalled not just a post-pandemic economic reboot or supply chain anomalies, but more importantly an underlying chronic underinvestment in energy infrastructure.

ThunderSaid Energy, a leading energy consultancy firm, estimates that energy markets could be undersupplied by 2.5-5% between 2025 and 2030, translating to a shortfall of about 2,500 to 5,000 terawatt-hours or a staggering USD 1 trillion of underinvestment per annum. Note that this is predicated on conservative energy per capita growth assumptions. It is this growing mismatch between supply and demand for energy which is one of the key reasons why we are long term optimistic to renewable energy.

The undersupply will cause energy costs as percentage of GDP to stay structurally higher in the second half of this decade, according to ThunderSaid Energy. This will likely put significant strain on the global economy.

The solution is more investments in energy, but due to ESG and the fight against climate change, many investors find it difficult to invest in fossil fuels. Others see fossil fuel investments as too risky since carbon taxes will only become a more fervent topic as the planet warms. We therefore anticipate that investments in renewable energy will only accelerate to cover the impending energy supply shortfall. This trend will likely result in structurally higher power prices over the next decade, hurting the global economy, but growing the total addressable market (TAM) for renewable companies while boosting their financial returns.

Moreover, historically, in periods with high energy prices, real economic growth has been relatively weak and brought about a challenging investment environment. In these instances, investing in energy companies has been an effective hedge as they benefit from the higher power prices.

The quicker the shift away from fossil fuels, the greater the returns for renewable investments as they stand to fill an ever-widening gap. This transition is not only about adhering to environmental imperatives but also about pragmatic economic planning.

FUND PERFORMANCE – ANOTHER TOUGH MONTH IN RENEWABLES

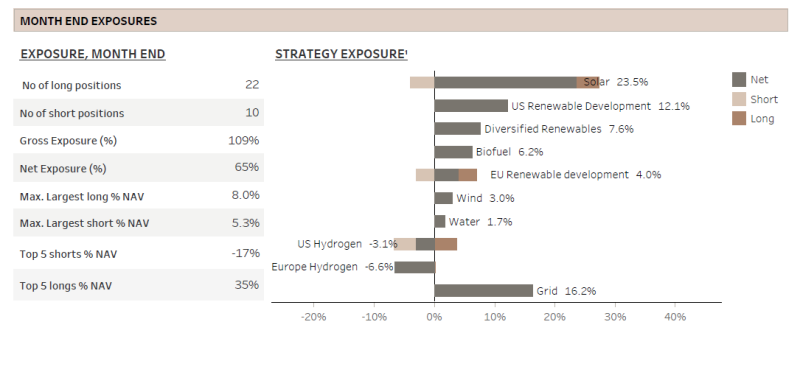

The fund lost 6.3% (I USD) in October as long positions lost 12.3% and shorts only made 6.0%. Half of the themes were positive or flat on the month, but the losing themes all incurred relatively large drawdowns. The net exposure was in the high 60% to low 70% for most of October, which clearly contributed to the loss as the key renewable indices fell between 11 and 14%. We ended the month with a net exposure of 65%, having pared down some positions in anticipation of early November earnings reports, but they were added back as soon as earnings-report-risk had passed. Gross exposure was in the 110-120% range most of the month.

Not surprisingly, the largest losing theme drawing down 3.7% of NAV was “Solar”. It has the highest gross capital, it is skewed long, and it contains three of our largest long positions, the utility scale companies Array Technologies (ARRY), Shoals Technologies (SHLS) and First Solar (FSLR). All were down double digits in October, similar to their decline in September. The stocks sold off partly due the higher long-term rates and in sympathy with the ongoing sell-off in the residential solar stocks.

However, the stock market is also fearing and pricing in a significant slowdown in the utility scale market. Indeed, there is a noticeable deferral of some projects, with the most significant factor being the anticipation of detailed Inflation Reduction Act (IRA) tax credits guidelines. This uncertainty is causing a holdup in financing, as banks and investors seek complete clarity on the potential returns and associated risks before committing their funds. Finally, some projects are rumored to be held up due to interconnection permitting issues.

These worries are legitimate, but the real issue is whether we are looking at a temporary setback or the start of a longer slump. We remain confident that the utility scale market's growth trajectory for the coming years remains intact. Once the specifics of the IRA are unveiled, we expect project approvals to accelerate and financing to resume. As highlighted in our report last month, utility-scale solar remains the most cost-effective energy source in many markets, with a U.S. project pipeline that is nearly 30 times the capacity installed this year.

When Nextera Energy (NEE US), the world largest developer, reported its third quarter earnings they confirmed that they are not slowing down investments and that higher financing costs did not hamper their ability or willingness to invest. Also, Nextracker (NXT), the main peer of ARRY reported strong Q3 results, order intake and outlook for 2024. Finally, Quanta Services(PWR), the largest service contractor of grid transmission and interconnection in the US, confirmed its guidance and 2024 outlook.

Nevertheless, the market is unforgiving these days and as we are writing this report in early November, SHLS and ARRY just reported their third quarter results that were punished by double digit declines the next day.

SHLS delivered strong Q3 results, meeting revenue targets and surpassing earnings expectations. While there was a slight reduction in the full-year revenue outlook, earnings projections have increased. Despite these positives, SHLS shares took a hit due to an expected warranty issue that turned out to be more costly than the market anticipated. However, SHLS plans to seek partial reimbursement from the supplier, and its record order intake suggests customers are not holding SHLS responsible for the warranty mishap.

Moreover, the market value of the shares has declined by about 10 times the size of the maximum warranty loss since it was first announced three months ago. We believe this is an overreaction. While this issue may weigh on the company in the near term, EBITDA forecasts for 2023 have been raised, with 2024 expectations remaining stable.

ARRY's Q3 report presented a more mixed picture with revenue falling short of expectations but offset by higher-than-anticipated margins, leading to better EBITDA and EPS figures. However, the company trimmed its full-year outlook, indicating a weaker fourth quarter, citing project delays from financing hurdles and permitting issues as we discussed above. Initial order intake seemed low at USD 250 million, yet there's a significant USD 300 million in orders on hold, awaiting IRA guidelines—a substantial amount that could boost future intake figures. Additionally, ARRY secured 3GW in volume commitments not yet reflected in the backlog, potentially adding another USD 300 million. The company also reported a doubling of its potential U.S. project pipeline from the second to the third quarter, pointing to strong 2024 order intake. Despite these developments, the market reduced its EBITDA forecast for 2024 by about 3% following the third-quarter report, and the stock price saw an 18% drop.

It has clearly been a mistake holding on to and growing these two large positions. Although, we are still optimistic to growth in the utility scale solar market and continue to see ARRY and SHLS as two of the best positioned companies in this space, we will tread carefully into year-end.

If we should have one concern for the growth in utility scale solar, it would be grid connection bottlenecks. Speeding up permitting helps, but you still need to expand the grid. This is one of the reasons why the ‘Grid’ theme has become our second largest theme.

However, the “Grid” theme lost 1.5% of NAV in October, pulled down by risk-off in renewables but also impacted by the growing uncertainty in the utility scale market. Not only did Quanta sell off into its strong earnings report, but the European grid companies took a beating following offshore wind cancellations in the US. Our largest position, NKT (NKT DC), has substantial exposure to HVDC cables, which is why we like the company but is has zero exposure to the US offshore wind space. The company issued a positive profit warning in early November and reported continued strong order intake. Since 2019 the company has grown its backlog from about EUR 1bn to EUR 11bn.

Another theme that did poorly in October was “Diversified Renewables” which lost 1.8% of NAV. The only stock in the theme, Chart Industries (GTLS), declined by 31% during the month and fell 25% on the day it reported Q3 earnings. The report was on the weaker side due to projects delayed into Q4, but full year guidance and EBITDA for 2024 were confirmed. GTLS was our largest position earlier in the year, but we more than halved it as the stock returned almost 50% during the spring and summer. We still believe GTLS is a great energy transition company, and we anticipate a rebound in its share price, likely triggered by a strong free cash flow report in Q4.

The only large winning theme in October was “European Hydrogen”, which contributed a 2% gain to the NAV. This success was not just a result of the wider sell-off in renewables; it was also driven by underwhelming order intakes for our shorted companies, which is impactful as they are all trading on EV/Sales multiples. We had tactically dialed back our net short position in the US Hydrogen theme as we increased our net exposure at the start of the month. In retrospect, this was clearly wrong.

We look forward to updating you again next month.

Sincerely,

Vidar Kalvoy & Joel Etzler

- Portfolio Manager and Founder of the Coeli Energy Opportunities Fund.

- Over 15 years of investment experience spanning both public markets and private equity.

- Managed the Coeli Energy Transition Fund from 2019 to 2023.

- Spent six years at Horizon Asset in London, a market-neutral hedge fund.

- Started working with Vidar Kalvoy in 2012.

- Five years in Private Equity at Morgan Stanley.

- Began his investment career in the technology sector at Swedbank Robur in Stockholm in 2006.

- Holds an MSc in Engineering from the Royal Institute of Technology (KTH), Stockholm.

- Portfolio Manager and Founder of the Coeli Energy Opportunities Fund.

- Has managed energy equities since 2006 and brings more than 20 years of experience in portfolio management and equity research.

- Managed the Coeli Energy Transition Fund from 2019 to 2023.

- Head of Energy Investments at Horizon Asset in London for nine years, a market-neutral hedge fund.

- Experience from energy investments at MKM Longboat in London and equity research in the technology sector in Frankfurt and Oslo.

- Holds an MBA from IESE in Barcelona and a Master’s in Business and Economics from the Norwegian School of Economics (NHH).

- Before entering finance, he served as a lieutenant in the Royal Norwegian Navy.

IMPORTANT INFORMATION. This is a marketing communication. Before making any final investment decisions, please refer to the prospectus of Coeli SICAV II, its Annual Report, and the KID of the relevant Sub-Fund. Relevant information documents are available in English at coeli.com. A summary of investor rights will be available at https://coeli.com/financial-and-legal-information/. Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested. Please note that the management company of the fund may decide to terminate the arrangements made for the marketing of the fund in one or multiple jurisdictions in which there exists arrangements for marketing.