This material is marketing communication.

Note that the information below describes the share class (I USD), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class return. The information below regarding returns therefore differs from the returns in other share classes.

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

1) Share Class I USD

FUND MANAGER COMMENTARY

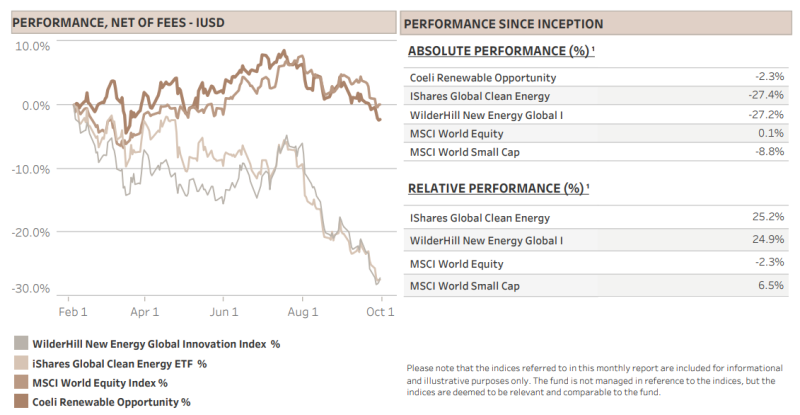

The Coeli Renewable Opportunity fund lost 5.2% net of fees and expenses in September. It is down 2.3% since the inception on February 6, 2023.

The fund’s relative outperformance keeps growing as renewable energy equities continued its decline in September. The two most comparable indices, the Wilderhill New Energy Global index (NEX) and the iShares Global Clean Energy (ICLN), both booked their worst two-month period over the last 10 years. Our fund outperformed the NEX by 5.1% and the ICLN by 3.8% in September, boosting outperformance since inception versus both indices to about 25%.

As we were both worried about the macro environment and skeptical to the valuations in our sector, we have since our launch in February maintained a cautious net exposure between 40% to 55% compared to our 40-80% target. The clean tech bubble of 2020-2021 continues to deflate with September marking a significant step down in valuations across renewable energy equities. In early October, the Wilderhill Index plunged back to its pre-pandemic level, wiping out a 190% rally during 2020 and early 2021.

Several factors give us optimism that certain companies might be finding a bottom. Most stocks in our universe are hovering around their 52-week lows, while short interest has peaked at a 52-week high and hedge fund net exposure in renewables stands at its lowest in four years, as per Morgan Stanley's data. This pronounced bearish stance, coupled with traditionally strong Q4 market seasonality, could be a good set up for a year-end rally, particularly in the year's largest underperformers. We significantly increased our net exposure in the beginning of October. Stay tuned.

MARKET COMMENT – PEAK GOLDILOCKS?

September is historically the worst month for the stock market with a good margin. This year was no exception as both the S&P 500 and Nasdaq dipped roughly 5%. The main culprit was higher long-term rates as the yield of the 10-year US Treasury rose by 50bps to 4.6% and has continued higher into October.

What is prompting the rise in long-term rates? Several factors are at play, but an obvious one is the imbalance between the supply and demand of US Treasuries. As the US deficit widens, more bonds will flood the market. Compounding this, two of the most significant buyers in recent decades have shifted their strategies: the Federal Reserve has commenced quantitative tightening, allowing bonds to mature without replacement, and China, at best, is maintaining its holdings even as the total number of bonds in circulation grows. The result? Greater supply coupled with diminished demand pushes bond prices down and yields up.

Another explanation for higher rates, with a lot of support currently, is that the US economy is much stronger than expected. While inflation is declining, the labour market is robust with solid job creation and low unemployment. GDP growth is above trend, and earnings estimates for 2023 have recovered and returned to the level at the beginning of the year. It is clear that the US economy is demonstrating greater resilience to rising interest rates than many analysts, ourselves included, had expected.

RENEWABLE ENERGY – THERE IS BLOOD ON THE STREETS

The last months have been awful for the renewable energy universe. Since the 10-year US Treasury started its recent ascent from 3.8% in mid-July to above 4.6% at the end of September, the two clean tech indices have declined by about 21% while the S&P 500 Utilities index fell by 12%.

The main culprit for the weak performance is clearly higher interest rates. When the risk-free rate increase and is perceived to shift to a higher level, the net present value of all future cash flows declines. Valuation multiples must be reduced. It is not complicated.

Yet, even within this backdrop, renewables notably underperformed compared to other growth sectors. The clean tech bubble of 2020-2021 is still in the process of deflating likely causing many investors to throw in the towel on the sector. While the market was willing to put extreme values on growth pipelines three years ago, it is currently in complete disbelief that future growth has any value. Some companies are trading at less than 50% of currently locked in, contracted cash flows, implying sharply negative value of future growth. This is what happens when a bubble deflates, we have gone from extreme greed to extreme fear in three years.

Compounding the challenge of rising interest rates, the sector has been beleaguered by a series of unfavourable announcements. In September, Nextera Energy Partners (NEP), the YieldCo of Nextera Energy (NEE), the world’s largest renewable developer, warned that that it would have to reduce equity distribution growth targets due to higher financing costs.

If a company financing projects for the largest developer in the US have issues raising capital, the market is assuming that this problem is probably widespread and even worse for smaller developers. We believe this is only partly true as NEP is a financing company with a lot more leverage than the average renewable energy developer. Yet, we agree that everything else equal, it is logical that higher rates will result in some project cancellations and at least some delays. However, higher interest rates will not stop the growth in this industry.

While the cost of capital has increased, there are mitigating factors that we believe the market might be overlooking or undervaluing. First, LevelTen Energy, a renewable energy consultancy, estimates that the average power purchase agreement price (PPA) for onshore wind surged by approximately 85% since cost inflation took off in early 2021. During the same period, utility-scale solar PPAs have risen nearly 60%, reflecting both increased input costs for solar installations and the rise in electricity prices due to the energy crisis. Moreover, the Lawrence Berkeley National Laboratory estimates that in 2022, the construction cost (Levelized Cost of Energy – LCOE) of an average utility-scale solar project in the US was USD 39/MWh, whereas it calculates the wholesale value of the electricity to be worth USD 71/MWh. This offers a considerable margin of safety to account for any cost inflation.

How much would LCOE increase with higher interest costs? According to Morgan Stanley, a 1%-point higher financing costs would raise the LCOE by around 5% or roughly USD 2/MWh from a base of USD 39/MWh. We believe the increase could be higher, maybe closer to 10% in certain circumstances, but still well below the rise we have seen in the PPAs the last two years.

Additionally, the tax credit adders in the Inflation Reduction Act (IRA) will soon come into full effect when the final details are published. These two adders, a domestic content bonus and an energy community bonus, provide supplemental tax credits—10% for each—added to the already generous Production Tax Credit (PTC) of USD 27.5/MWh. For projects obtaining both adders, an additional USD 5.5/MWh could be available. These two adders alone would, using Morgan Stanley’s calculation, cover a 2.75%-points increase in the financing cost.

Finally, solar panel prices have dropped sharply as Chinese manufacturers have oversupplied the market. Prices for delivered panels in Europe have declined by about USD 10c/W, which for an average solar project could lower LCOE by as much as USD 3/MWh. There are indications that the US has witnessed a similar price reduction, albeit from a higher starting point.

Despite all these offsets, we can understand the market’s reaction that when rates rise steeply, companies with cash flows far into the future get indiscriminately sold. However, at one point interest rates will stop going up and investors will again appreciate the intrinsic value of these companies. It is a matter of time. We think a good time might be, as Baron Rothschild said, when there is “blood on the streets”.

FUND PERFORMANCE – STRONG RELATIVE BUT WEAK ABSOLUTE PERFORMANCE

The fund lost 5.2% (I USD) in September, pulled down by an 8.8% loss on the long holdings and only partly offset by a 3.5% profit on the shorts. As the general market sold off by more than 5% and renewables are massively out of favour, it is unsurprising that all our long-skewed themes lost money.

The largest losing themes were ‘Solar’ and ‘US Renewable Development’, which are the same two culprits as in August. The ‘US renewable development’ theme lost 1.7% of NAV in September, caused equally by Nextera Energy (NEE) and AES. As we have described above, NEEs yieldco Nextera Energy Parntners (NEP) warned of lower growth and distributions going forward due to higher financing costs. The stock dropped nearly 50% the next 3 days into month end. NEE owns 51% of NEP and saw its market cap shrink by 13%, or more than USD 17bn despite the lost value due to lower NEP stake only amounts to about USD 1bn.

Obviously, the market is fearing that NEE will struggle to finance its growth as drop downs to NEP will probably not be possible for the next two years. We believe this concern is somewhat overstated. NEE sold about USD 1bn in assets annually to NEP compared to a total annual capex of about USD 20-25bn. Although asset sales to NEP were supposed to increase over the next years, we believe NEE has many alternatives for financing. First, it can do project debt financing like most of its peers. Second, tax credit transfers have become more straightforward after the introduction of the IRA. Third, it can add leverage to existing projects. Basically, NEP always added leverage after acquiring assets from NEE. This became problematic for NEP as interest rates rose, but NEE is investment grade rated with a solid balance sheet and low-risk cash flows from its regulated business in Florida.

We believe the sharp share price fall in NEE this year is an overreaction. Of course, the value of the existing assets deserves to be revalued as interest rates have increased, but as we have described above, we expect NEE to have pricing power to increase PPAs. Furthermore, combined with tax incentives and lower solar costs, the value of its pipeline should be more or less unchanged compared to the start of the year. We expect the company to confirm this view and to present hard data on its different financing options when it reports Q3 in some weeks. We have added to our NEE position during the first week in October.

The worst performing theme in September was ‘Solar’ which deducted 4.3% from NAV. Despite maintaining a slight net long exposure in residential solar, our primary focus remains on utility-scale firms that supply solar equipment to renewable developers. As the market lost faith in the growth outlook for utility scale solar and interest rates rose, this segment of the market took a big beating in September. Array Technologies (ARRY), Shoals Technologies (SHLS) and First Solar (FSLR) all witnessed declines ranging from 7% to 16%.

Clearly, we believe this is an overreaction and our view is supported by industry data. WoodMac, the gold standard in solar forecasting, has recently increased its estimate for installations in 2023 due to improved solar panel availability. The US imported 32GW of panels in the first seven months of 2023, which is 150% more than in the same period in 2022. EIA estimate that 24GW of utility scale solar will be connected to the grid in 2023 versus about 9GW installed in the first seven months. Finally, according to EIA, the pipeline of utility scale projects in the US is 947GW. Of course, the number is inflated by projects that are unlikely to get a permit, but combined with the fact that utility scale solar is the cheapest form of energy in most markets, we believe the growth outlook is solid.

The only two themes with positive returns in September were ‘EU Hydrogen’ and ‘US Hydrogen’, both were net short and contributed 2.0% and 0.9% respectively to NAV. Order intake for many of these companies are disappointing and we foresee cuts to 2024 and 2025 revenue estimates. This is unfortunate for companies that are still trading on inflated EV/Sales forward multiples. To make it worse, some have not yet raised sufficient financing to construct the capacity needed to deliver on the optimistic revenue forecasts.

We will stay short hydrogen, although we have reduced the net in those themes in the first part of October. The terrible sentiment in renewable energy combined with extremely negative positioning and strong Q4 seasonality could be good set up for a rally into year end, especially in the biggest decliners of the year.

We look forward to updating you again next month.

Sincerely,

Vidar Kalvoy & Joel Etzler

- Portfolio Manager and Founder of the Coeli Energy Opportunities Fund.

- Over 15 years of investment experience spanning both public markets and private equity.

- Managed the Coeli Energy Transition Fund from 2019 to 2023.

- Spent six years at Horizon Asset in London, a market-neutral hedge fund.

- Started working with Vidar Kalvoy in 2012.

- Five years in Private Equity at Morgan Stanley.

- Began his investment career in the technology sector at Swedbank Robur in Stockholm in 2006.

- Holds an MSc in Engineering from the Royal Institute of Technology (KTH), Stockholm.

- Portfolio Manager and Founder of the Coeli Energy Opportunities Fund.

- Has managed energy equities since 2006 and brings more than 20 years of experience in portfolio management and equity research.

- Managed the Coeli Energy Transition Fund from 2019 to 2023.

- Head of Energy Investments at Horizon Asset in London for nine years, a market-neutral hedge fund.

- Experience from energy investments at MKM Longboat in London and equity research in the technology sector in Frankfurt and Oslo.

- Holds an MBA from IESE in Barcelona and a Master’s in Business and Economics from the Norwegian School of Economics (NHH).

- Before entering finance, he served as a lieutenant in the Royal Norwegian Navy.

IMPORTANT INFORMATION. This is a marketing communication. Before making any final investment decisions, please refer to the prospectus of Coeli SICAV II, its Annual Report, and the KID of the relevant Sub-Fund. Relevant information documents are available in English at coeli.com. A summary of investor rights will be available at https://coeli.com/financial-and-legal-information/. Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested. Please note that the management company of the fund may decide to terminate the arrangements made for the marketing of the fund in one or multiple jurisdictions in which there exists arrangements for marketing.