After years of near-uninterrupted outperformance, cracks may be starting to form in the US tech sector. The “Magnificent Seven”, Apple, Microsoft, Alphabet, Amazon, Meta, Nvidia, and Tesla, are, as we pointed out above, down roughly 15% in the first quarter, while the remaining 493 stocks in the S&P 500 were broadly flat. Whether this marks a temporary pause or something more structural remains unclear, but the relative weakness has become difficult to ignore.

Over the past five years, the S&P 500 Technology sector has accounted for more than a third of MSCI World’s returns and one of the key drivers has been excitement around artificial intelligence. While we are not tech investors, AI-driven capex from the large US tech companies has become a central driver of global power demand, and by extension, demand for electrical equipment and infrastructure. Developments in this space are now closely tied to our investment universe, which means we follow the hyperscalers and their investment plans closely.

The five largest US tech companies are expected to spend over USD 300 billion in capex this year, primarily on data centre infrastructure. For context, five years ago, the combined capex was less than USD 100bn. Using Microsoft as an example, in 2020 it spent about a quarter of its operating cash flow on capex, while it last year invested four times more than in 2020 as capex consumed almost 50% of operating cash flow. This year, capex is set to grow to above USD 80bn and consume about two thirds of expected operating cash flow. Obviously, this trend must turn at one point and investors are rightly asking whether these AI-driven investments will generate attractive returns, and to whom the value will accrue.

One emerging concern is software commoditization. With the rapid democratization of generative AI, it is not hard to imagine someone building alternatives to Microsoft Word or Adobe Photoshop with minimal resources. If this dynamic take hold, even companies with strong historical moats could see their pricing power eroded. Rapidly changing competition could even challenge large software ecosystems.

Another risk, which is somewhat interlinked, comes from Chinese competition. Tesla, long viewed as a frontrunner in EVs, is already overtaken by Chinese competitors on quality and price, and Apple is losing share in China to domestic brands like Huawei and Xiaomi. While these trends are most visible in consumer hardware, China’s ambitions go much further. The country is actively investing in semiconductors, quantum computing, and AI, areas where it has historically lagged.

Even before the recent introduction of higher tariffs on China, the last three US administrations have fought this trend by protecting its domestic market from Chinese competition and by restricting technology transfer from Western companies. This failed massively with regards Huawei, which was gradually cut off from Western technology from 2012 onwards. However, necessity is the mother of innovation, and the restrictions put on Huawei only increased its incentives to innovate. With R&D budgets almost matching the US tech giants, it is the market leader in telecom equipment having replaced western chips and software with newly developed Chinese IP. This technology is now offered around the world in competition with products and services from the US tech giants.

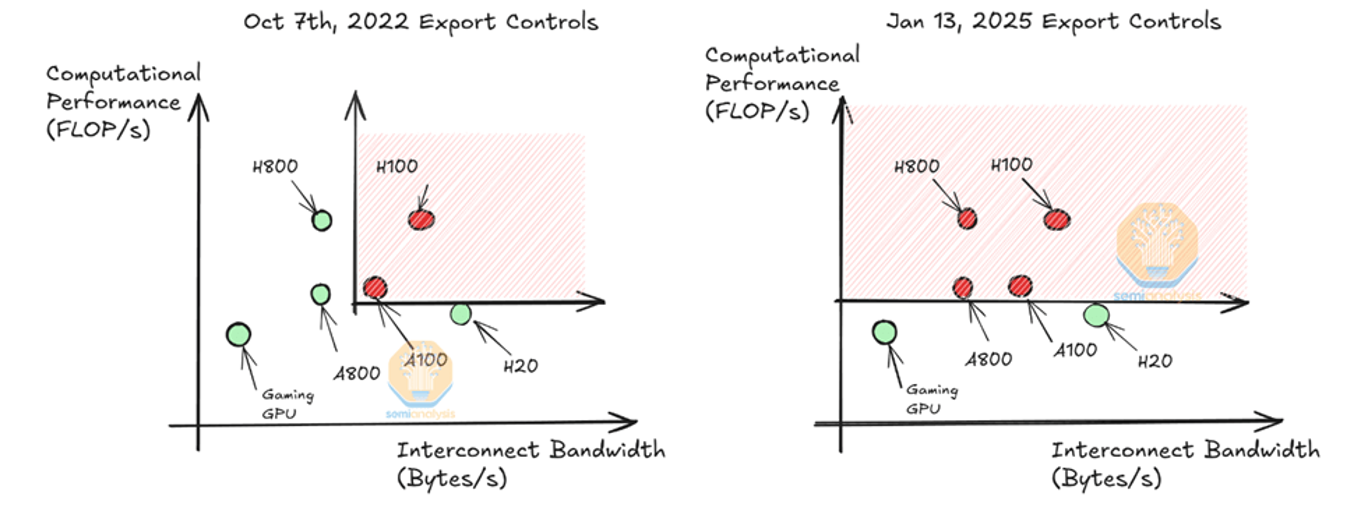

In that regard, we are particularly concerned about Nvidia, the world’s third most valuable company with a market cap of more than USD 2 trillion dollars. Today, Nvidia has a near-monopoly position in production of advanced GPUs required to train large AI models. US export controls have long sought to limit China’s access to high-performance chips, banning for example Nvidia’s A100 and H100 models and, later, even their modified H800 version. In response, Nvidia launched the H20, which complies with the FLOPS (Floating Point Operations) restrictions but comes with higher memory bandwidth which is of key importance in so-called reasoning tasks. As SemiAnalysis, a specialist consultancy, nicely depicts, the H20 excels when it comes to Interconnect Bandwidth. Many argue though that this is circumventing the spirit of the ban.

Source: Semianalysis.com

Despite the restrictions, roughly 11% of Nvidia’s last year’s revenues still came directly from China. In addition, it is an open secret that Singapore, a city of only 5.6m inhabitants and accounting for 18% of Nvidia’s last fiscal year calendar 2024 revenues, is a backdoor for its sale into China. Whether or not this ‘backdoor’ will be allowed to remain open, considering the brewing trade war, is an open question as the Trump administration has already hinted at tighter export restrictions. If so, almost a third of Nvidia’s sales might be a risk.

Furthermore, China is also mulling stricter energy efficiency requirements on chips used in data centres, a move that would disqualify Nvidia’s H20 chip which supposedly does not comply with the new rules. One might have expected China to have liked to acquire as many Nvidia chips as possible, but it seems like it has other more important long-term objectives, like self-sufficiency, regulatory leverage and market control and data security. Whether Chinese chips will be able to compete head on with Nvidia near-term is still uncertain, but we would not underestimate the Chinese’s technological ability over the long term. Who would have thought three years ago that Chinese EVs would overtake Tesla on quality? Moreover, considering China’s recent introduction of a 34% tariff on all import from the US, and assuming it remains, Chinese chips’ have suddenly narrowed the cost efficiency gap even further.

Moreover, the ‘Deepseek moment’ seems to have spawned the next level of competitiveness in the Chinese tech sector. Many western experts are starting to worry that Chinese AI ecosystems, optimized for Chinese chips could become both cheaper and easily accessible for the rest of the world. There is a real risk that global developers, especially in emerging markets, will pivot toward these models. In that scenario, US dominance of the AI stack could begin to erode.

While it is too early to decide if US tech dominance is really under threat, the roll-out of Generative AI has lowered the barriers to innovation globally and clusters like Silicon Valley could lose some of its edge. At the same time, the brewing trade war is hardly helpful. As the Trump administration is focused on taxing goods where the US has a trade deficit, the rest of the world might go after services where the US has large surpluses, partly due to services offered by US big tech.

What does it mean for our universe of companies? First, in our January investor letter, “DeepSeek and Its Impact on Power Demand,” we argued that valuations across the AI trade looked stretched and were due for a reset. That view has since been validated.

Second, it is uncertain how a potentially waning long-term US dominance in AI and tech impacts our electrification focused companies. However, as we described in our December-24 report, AI is only the icing on the cake for this universe. Even if the US should enter a recession, the grid still needs to be upgraded, and the trends of onshoring and industrial electrification will persist. Near-term data centre buildouts and rising power demand are real and visible. And while few of our positions are truly recession-proof, many of our long holdings benefit from strong market positions, solid balance sheets, and large clients likely to continue investing even through a downturn. Some may appear expensive in a recessionary context, but that risk is possible to hedge in a market full of weak-balance-sheet companies unlikely to survive a prolonged downturn.

Nevertheless, the brewing trade war is a major negative for the world economy. The S&P 500 is at the time of writing down almost 20% since peak but still trading on inflated valuation multiples considering that bottom-up earnings estimates have yet to be cut. Still, compared to the previous crises we have experienced; from the bursting of the internet bubble to the great financial crises, the euro crisis, Brexit and finally Covid, this is the only crisis caused single handedly by one man. Fortunately, this also means that one man can put an end to it.

We are confident that a de-escalation will eventually occur, but the timing is uncertain. Also, the longer it drags on, the greater the damage to the global economy. Uncertainty and high volatility are likely to prevail for some time and until we get more clarity, we continue to seek opportunities to take advantage of irrational price moves on both the long and the short side.

- Portfolio Manager and Founder of the Coeli Energy Opportunities Fund.

- Over 15 years of investment experience spanning both public markets and private equity.

- Managed the Coeli Energy Transition Fund from 2019 to 2023.

- Spent six years at Horizon Asset in London, a market-neutral hedge fund.

- Started working with Vidar Kalvoy in 2012.

- Five years in Private Equity at Morgan Stanley.

- Began his investment career in the technology sector at Swedbank Robur in Stockholm in 2006.

- Holds an MSc in Engineering from the Royal Institute of Technology (KTH), Stockholm.

- Portfolio Manager and Founder of the Coeli Energy Opportunities Fund.

- Has managed energy equities since 2006 and brings more than 20 years of experience in portfolio management and equity research.

- Managed the Coeli Energy Transition Fund from 2019 to 2023.

- Head of Energy Investments at Horizon Asset in London for nine years, a market-neutral hedge fund.

- Experience from energy investments at MKM Longboat in London and equity research in the technology sector in Frankfurt and Oslo.

- Holds an MBA from IESE in Barcelona and a Master’s in Business and Economics from the Norwegian School of Economics (NHH).

- Before entering finance, he served as a lieutenant in the Royal Norwegian Navy.

IMPORTANT INFORMATION. This is a marketing communication. Before making any final investment decisions, please refer to the prospectus of Coeli SICAV II, its Annual Report, and the KID of the relevant Sub-Fund. Relevant information documents are available in English at coeli.com. A summary of investor rights will be available at https://coeli.com/financial-and-legal-information/. Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested. Please note that the management company of the fund may decide to terminate the arrangements made for the marketing of the fund in one or multiple jurisdictions in which there exists arrangements for marketing.