Note that the information below describes the share class (I SEK), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class' return. The information below regarding returns therefore differs from the returns in other share classes.

Before making any final investment decisions, please read the prospectus, its Annual Report, and the KIID of the relevant Sub-Fund here

This material is marketing communication

Monthly Newsletter Coeli Absolute European Equity – April 2022

APRIL PERFORMANCE

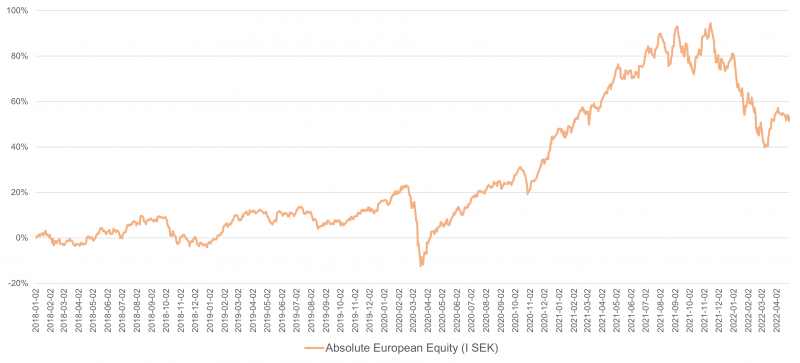

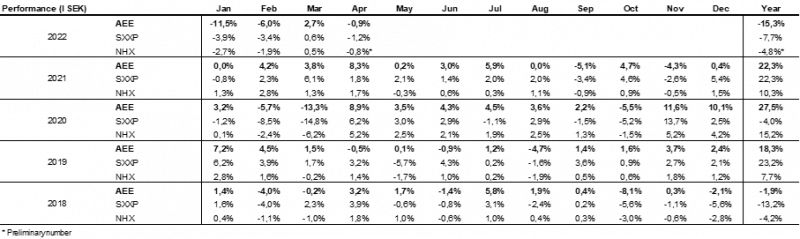

The fund's value decreased 0.9% in April (share class I SEK). The Stoxx600 (broad European index) decreased during the same period by 1.2% and HedgeNordic's NHX Equities decreased provisionally by 0.8%. The corresponding figures for 2022 are a decrease of 15.3% for the fund, -7.7% for Stoxx600 and -4.8% for NHX Equities.

EQUITY MARKETS / MACRO ENVIRONMENT

After a strong finish last month, April began relatively hesitant, waiting for the reporting season to start. The terrors of the war had a limited direct impact on the stock market, but the indirect consequences increase with each passing week. Food prices continue to rise, while oil prices, at least temporarily, have stabilized. What caused the stock market to turn downwards in the second half of the month was partly the headless and failed full force action in China to fight covid, and partly a continued upward pressure both in terms of inflation and rising interest rates.

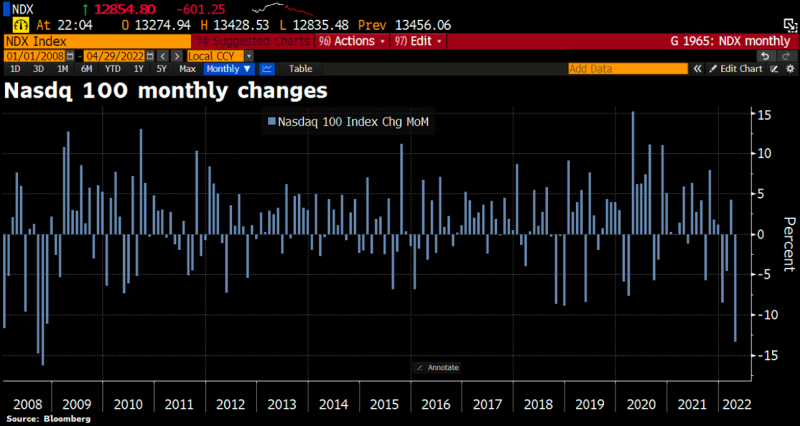

The European stock market developed significantly better than the US stock market in April, measured in local currencies. It was above all technology companies that were the big losers during the past month and which the USA has significantly more of. The explanation for this, in turn, is that rising interest rates put pressure on company valuations, but the fact that Amazon made a loss during the first quarter for the first time in seven years did not help. With a decline of 13.3% in April, it was the worst development for Nasdaq since 2008. The S&P500 fell by as much as 8.8%, which was the worst month of April since 1970 (when the index closed at 85.71 (!) against today's 4131,9).

Note, however, that measured in euros, the decline for the S&P500 was only 4.2% as the USD strengthened significantly (which tends to happen when markets are worried). The broad European index fell by a more modest 1.2% measured in local currency, but 6% in USD.

The worst month for Nasdaq since 2008!

Source: Bloomberg

The political and economic weakness in Europe combined with a more troubled world becomes painfully clear by studying the development of the euro against the USD over the past year. The value of the euro against the USD has reduced by 15%.

Source: Bloomberg

China is failing with its covid strategy and causing major problems worldwide with delivery issues when it locks people in. China also fails to control its exchange rate, see the development against the USD below and above all how the currency moved when the covid problems became clear a few weeks ago. China is now experiencing its worst period (if not the worst) since the 2008 financial crisis.

Source: Bloomberg

It’s a ghastly sight when you realise that the Russian rouble is now at a higher level than before the outbreak of war. Clearly the economic sanctions have, so far, not been powerful enough, which is also signalled by the oil price. It is the people of Russia who have, until now, taken the biggest blow and not the Russian state. BUT, with each passing week, sanctions are gaining more traction in the Russian economy. Russia's central bank reserve has shrunk by at least two-thirds and Russia can in principle no longer import anything, which means that soon nothing will be produced in the country. The EU has stopped imports of Russian coal. Europe's oil imports will also soon likely decrease, followed by gas imports. Russia is storming towards bankruptcy, and everything is orchestrated by only one person - Putin. It must be the pinnacle of human insanity?

Source: Bloomberg

During the last week of the month, Putin played the gas card and shut down gas supplies to Poland and Bulgaria when they refused to pay in roubles. It had no major impact on the financial markets, although the price of gas rose sharply that day. Below is a picture that shows different countries' dependence on Russian gas. Germany and Italy are worst placed of the large economies. We'll see how it ends. Putin is in desperate need of capital as the Western world now begins to supply heavier weapons and equipment to Ukraine. We take the liberty and quote Estonia's Prime Minister Kaja Kallas from last week: "Gas might be expensive, but freedom is priceless"

Ronald Reagan and Margaret Thatcher contributed to the collapse of the Soviet Union as military armaments increased markedly in the 1980s. We look forward to the replay now that the whole Western world is supporting Ukraine.

Source: Bloomberg

Rising inflation and interest rates have been controlling the financial markets with an iron fist for almost six months. Politicians and central banks have continued in an unimaginably aggressive way with expansive policies, even though the economy has been at its peak in and in several cases has shown clear signs of overheating. When even the Riksbank (Swedish Central Bank) turns around and raises the interest rate, then you know that the last man at the back of the line understood what was happening. Two months ago, Stefan Ingves (Governor of the Riksbank) announced that the interest rate would be raised in the second half of 2024, and now there is talk of several increases already this year. How is it possible to be so tone deaf on that level? And it is unfortunately not the case that the Riksbank's track record has been brilliant over the past 15 years. The Swedish krona exchange rate goes up and down in tandem with each press conference they hold. Incredible.

Source: Twitter

If you think the criticism is harsh against the central banks, look at the attached clips. Watch the whole sequence. If you must formulate yourself kindly, there is potential for improvement.

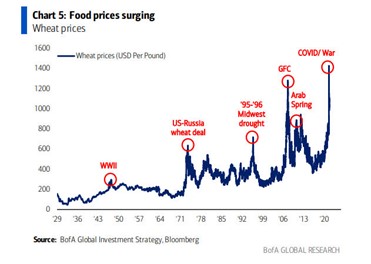

The biggest problem with rising prices is in food, and here the war in Ukraine is a clear contributing factor. The most disadvantaged have to take the biggest blow and there have already been riots and similar events in different parts of the world.

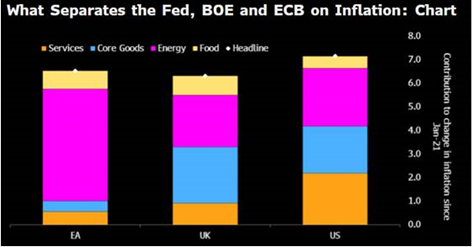

All central banks have major challenges, but they operate under different conditions. In Europe, energy is the largest component of inflation. In the UK and the US, it looks different, see picture below. Europe's total cost of energy is currently about nine percent of GDP, compared to only about 4.5% for the United States.

Source: Bloomberg

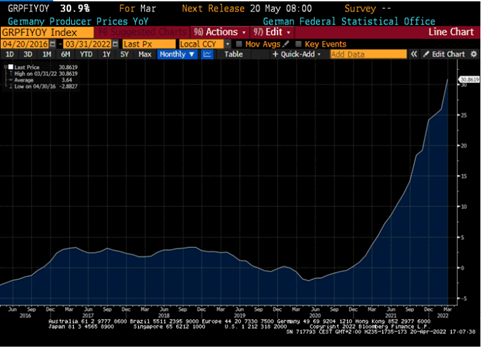

Below is a graph of German producer prices. The rate of increase is now 30.9% (!), which is the highest level in 73 years. Note that the interest rate in Germany right now is about 0, 9%. Is it just a temporary hump ECB? The ECB is still buying assets in the market!

Source: Bloomberg

Note the correlation between the oil price and German inflation expectations. If the world enters a slower growth, the textbook says that the oil price will go down and thus inflation. Important graph.

Source: Bloomberg, Holger Zschaepitz

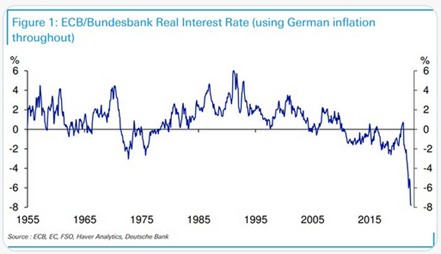

The real debt burden is also declining at a rapid pace. Below a 70-year timeline of the German real interest rate which right now is almost -8%!

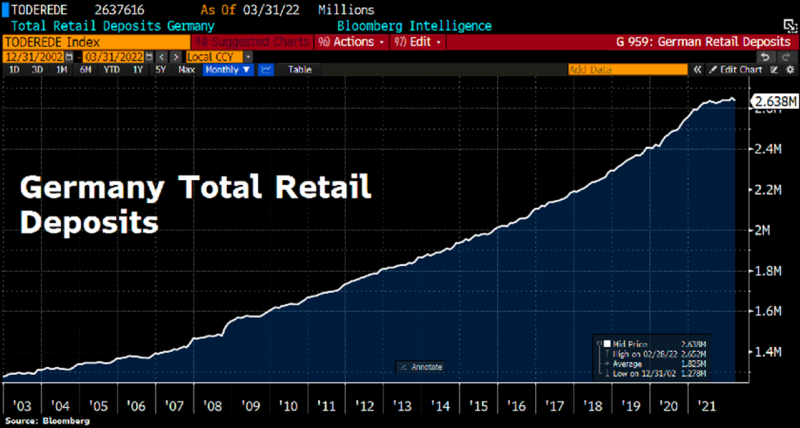

The Germans set a record with money in the bank. With the current inflation rate of around seven percent, this means EUR 185 billion in reduced purchasing power.

Source: Bloomberg

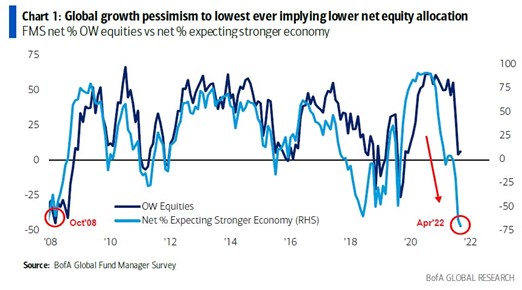

It is perhaps not so strange that the world's investors are gloomiest on record in terms of the world's growth prospects. We are now at the same level as the lowest point during the financial crisis. A big difference from 2008 is that the banking system is in a much better condition. Other companies and households are also at high levels in terms of financial preparedness. However, we did not have a war in Europe at that time. One conclusion is that the difference between economic activity in the world and allocation to shares is very large. Will we see continued reduced exposure to equities? Bonds and cash are not particularly attractive. Companies with "pricing power" will come out of this stronger.

Rising interest rates are making their mark on the bond market. The picture below shows the development of corporate bonds over the past 30 years for 24 different markets. The beginning of 2022 shows the worst development ever. Is there a level where we are starting to think about whether a declining collateral pool will affect any loans? We hear nothing about it for now at least.

Source: Bloomberg, Goldman Sachs

Elon Musk has placed a bid on Twitter. His tweet below is the second most liked in Twitter's history.

Source: Twitter

Sweden made a fool of themselves during the Easter weekend.

Source: Steget efter

Emmanuel Macron won the French presidential election. Marie Le Pen lost.

Source: Twitter

Long positions

Lindab

We once again experienced a positive surprise from Lindab, which beat earnings expectations by as much as 28% for the first quarter of 2022. Several construction-related subcontractors seemed to experience a good first quarter and we therefore increased our position ahead of the report release. In our opinion, the share is trading at low multiples even though it is a significantly better company today than just a couple of years ago and despite having positively surprised many quarters in the last three years. In our estimates, the share is traded at only 13x and 12x free cash flow in 2022e and 2023e. Despite the good report, the share price fell by 4% in April. We are taking advantage of the situation and have continued to increase our holdings after the report.

ArcticZymes

Another source of joy in April was Norwegian ArcticZymes. Sales and earnings were far better than expected and the share rose by 18% on the reporting day. We have become accustomed to the company alternating good and bad quarters, but now they managed to perform two quarters in a row. Will it be a third, maybe we can call it a trend? ArcticZymes continues to impress with high organic growth, sky-high margins, and low capital intensity. The stock rose 12% in April.

Wincanton, Tate & Lyle & Victoria

A couple of our British companies, more specifically the logistics company Wincanton and the ingredients company Tate & Lyle, had rising share prices without significant news in April and thus contributed to the monthly result.

However, the British carpet company Victoria continued its roller coaster. After a good March when the share rose by 25%, the share fell by 29% in April (crazy). Our assessment was and is that there has been a large and stressed institutional seller in the company who has had to sell since the end of February due to significant outflows. We gradually increased our position and the most recent shares we bought were a large block of 610 pence on April 28th. We hope this was the last to be shovelled out from this seller. The stock is trading as of this writing a few days later around 670 pence.

Sedana Medical

The problem child of the month is called Sedana Medical. The company communicated sales that were slightly below expectations, while gross margins were clearly better than expected. What caused significant turbulence was the company's announcement to move out the financial target for Europe by one year to 2025 and the mentioning of a Russian supplier (but this was a minor matter). All in one report was too much for the market, which on the reporting day sank the share by 31%. Our projected guess was a decline of between 10-15% and we were therefore surprised by the price reaction. It is clear that we are in a market where disappointments are severely punished.

We do not find it particularly worrying that Sedana is moving forward a financial goal that was set in 2017 when a new CEO was recently appointed. The Russian supplier problem seems to be solvable, and the company have stock of that particular component which covers sales for about a year. The market capitalization is low in relation to our projected sales for the next few years, where we see gradually increasing sales from Europe. At the same time, there is great value in the US, where Sedana is expected to commercialize its product in 2025. The share price fell as much as 44% in April.

Short positions

The short portfolio contributed with a positive result during the month. Our futures on a Swedish small-cap index were the largest contributors on the short side. Some stock-specific short positions that contributed positively to the result were Catena, Vestum and the wind power companies Nordex and Vestas.

Exposure

The net exposure, adjusted for our unlisted holdings, at the beginning and end of the month was 62 and 63%, respectively.

Summary

April was a frustrating month when the value of some of the fund's core holdings fell significantly and, in our opinion, unjustified. Victoria, Sedana and Truecaller had the largest negative impact. At the other end of the spectrum, the fund's largest positive contributors were Arcticzymes, Wincanton, Pebble Group, Tate & Lyle and Sampo. In addition, our short positions produced good returns and our negative position in the SEB Small Cap index accounted for one of the month's larger positive results. The largest impact overall was our unlisted holding in Swiss Rejuveron, which we invested in just over two years ago and which, in connection with a new capital raising round, saw its valuation rise. The fund had only about one percent position but given that the valuation rose from CHF 30 to 120, it had a good impact on the fund's results in April. The fund invested at CHF 19 per share.

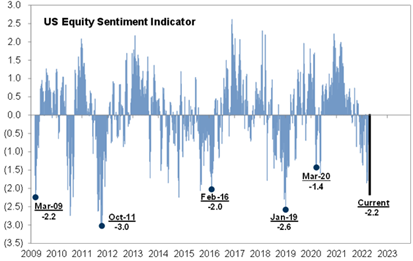

For many stocks and their owners, it has already been a significant crash and we are 8-9 months into the correction. The mood among investors is at historically very low levels and the war in Ukraine puts an extra muffler on the mood. Below Goldman Sachs sentiment indicator. It usually pays to increase the risk at current low levels.

Source: Goldman Sachs

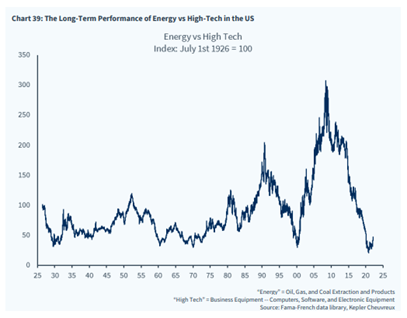

One who is clearly going against the flow is Warren Buffett, who in the last two months has put Berkshire's cash at work and bought more shares than probably ever before. He is usually right, to put it mildly.

Below is the development of energy shares compared with technology shares. It is interesting to note that Berkshire's purchases this year mostly consist of Chevron, which is now their fourth largest holding in total.

The challenge for central banks is greater than ever before as they must curb inflation, which is a poison to all involved, while not wanting to create a recession. The difference this interest rate hike period compared to other occasions when the Fed has not created a recession, is that the labour market is stronger, inflation is higher and real interest rates more negative.

It may be difficult for us here in Europe to understand the power of the US economy, but the labour market is very strong. The difference between the demand for labour (blue line) and the labour supply is illustrated below. The difference is the largest in the entire post-war period. That is hardly the case at home. In our opinion, the risk of a recession in the US this year must be assessed as low. Next year is more open.

Source: Goldman Sachs

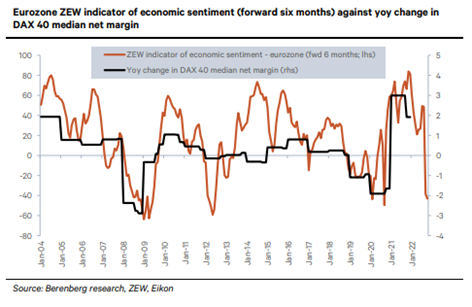

The picture below shows the relationship between expected economic activity in the eurozone over the next 6 months and the change in the operating margin this year compared to last year for Germany's 40 largest listed companies. The ZEW indicator for economic activity now shows -43, which is the same level as during the financial crisis of 2008/2009, the debt crisis in Europe 2011/2012 and the covid-19 crisis two years ago. If the correlation is correct this time, German companies will have a real headwind in terms of profitability in the coming months. To be continued.

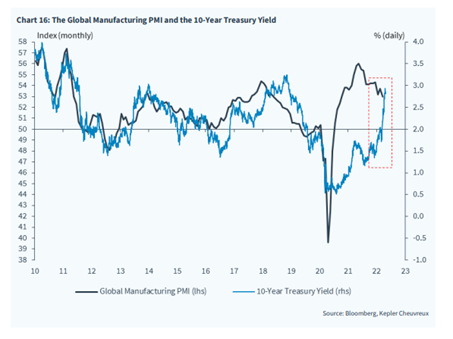

The interest rate level has caught up with the global purchasing index after being well below historical covariations in the last two years. The rising interest rate last month created significant economic and financial stress in the system, which leads us to believe that (US) interest rates will peak at approximately current levels while economic activity will continue to decline. The current quarter may also be the quarter when inflation peaks but no promises. After the summer, at least the comparative figures will start to look simpler, which, all other things being equal, will reduce the inflationary pressure upwards.

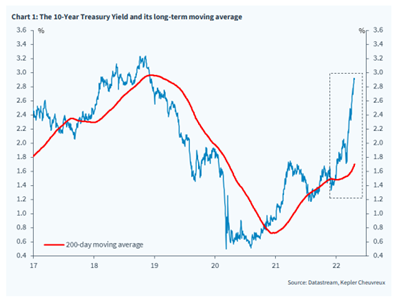

Below the American 10-year-old against his moving historical average value.

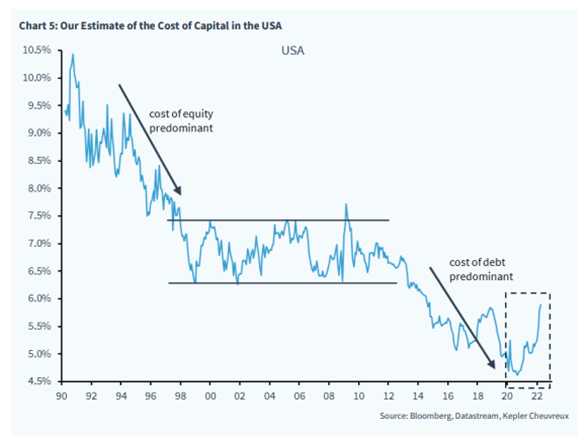

Kepler Cheuvreux has estimated the cost of capital for companies in the United States. The last few years have been at extremely low levels, and we are now moving towards somewhat more normal levels.

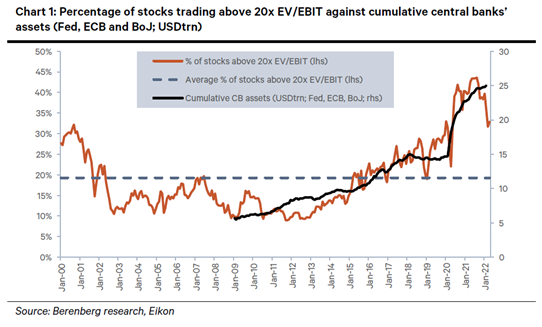

It is quite clear that central banks have contributed to excess valuations in recent years. The figure below shows the proportion of shares valued at more than 20 times the operating profit in relation to the central banks' accumulated assets.

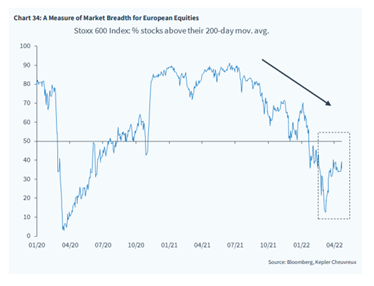

The breadth of the market has stabilized, which indicates that a lot of bad news has been discounted.

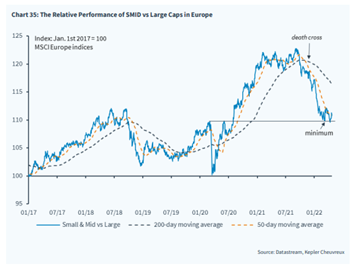

Development for European small companies have also stabilized. Either the sellers are ready, or the valuations have reached sufficiently attractive levels for buyers to start considering.

Our market view has remained unchanged since last month. We believe that this year's minimum level was set in March and that we will trade around current levels for several months. In a few days, the US Federal Reserve will issue its interest rate announcement and an increase of 0.5% will be on the cards. Only in July can we expect to hear something about how the ECB views any interest rate hikes.

In conclusion, I had fun during Valborg (Walpurgis) out on Österlen (southern Sweden) watching Berkshire Hathaway's general meeting where 91-year-old Warren Buffett and 98-year-old Charlie Munger for several hours entertained shareholders who had travelled to Omaha from all over the world. It was, as usual, oceans of wisdom that were communicated by these two unique personalities.

A story worth sharing is when Buffett tells with great surprise that for two weeks at the end of February, they bought 14% of Occidential Petroleum. He wondered how it is possible to buy 14% of a large oil company in just two weeks. Imagine being able to buy 14% of all farms in the country in two weeks. Or 14% of all car dealers and so on. Their conclusion was that the stock market over the past two years has turned into a casino where algorithms run stock prices up and down and many of the owners of flesh and blood have no idea what they own.

We recognized ourselves in that description when certain days in April offered very large volatility in various shares. It is more important than ever to be confident in your company analysis and know why you own certain companies. In the short term, it is impossible to predict how different stocks will be traded. We invest and allocate your capital with a long-term view, and we are convinced that current volatility will reward us in the future in the form of rising share prices. The only thing that is absolutely certain is that you never get bored in this profession. Written one hour after some thug pressed the wrong button and plummed the Stockholm Stock Exchange by 8% in two minutes…

Enjoy May!

Mikael & Team

Malmö, 5th of May 2022