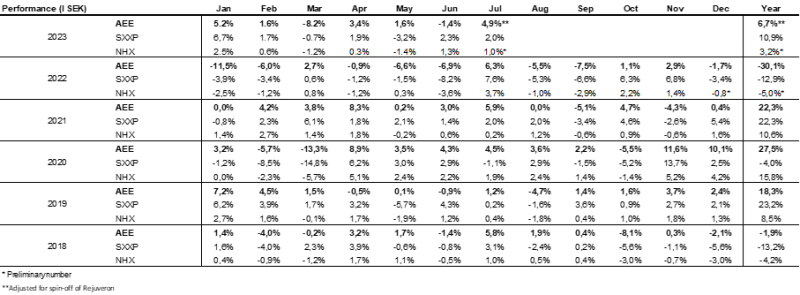

Note that the information below describes the share class (I SEK), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class' return. The information below regarding returns therefore differs from the returns in other share classes.

Before making any final investment decisions, please read the prospectus, its Annual Report, and the KID of the relevant Sub-Fund here

This material is marketing communication

Monthly Newsletter Coeli Absolute European Equity – July 2023

JULY PERFORMANCE

The fund's value increased by 4.9% in July (share class I SEK), adjusted for the spin-off of Rejuveron. Unadjusted, the fund's value decreased by -3.1%. The Stoxx600 (broad European index) increased during the same period by 2.0% and HedgeNordic's NHX Equities increased provisionally by 1.0%.

For 2023, the fund has risen by 6.7%, adjusted for the spin-off of Rejuveron. Unadjusted, the fund's value has decreased by 1.5%. The Stoxx600 and NHX Equities have risen by 10.9% and 3.2% respectively during the year.

EQUITY MARKETS / MACRO ENVIRONMENT

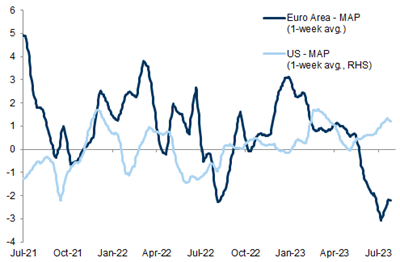

The month of July got off to a weak start with the broad European indices down 3-4%. On July 6th we recorded the weakest exchange rate development since the banking turmoil in March and, as a law of nature, the Swedish krona simultaneously dropped to a new low against the euro at 11.95. In a thinly traded summer market, we were presented with several different data points that showed a continued strong economy in the US and thus an interpretation by the market that interest rate increases are continuing more than feared. The US two-year-old also reached its highest level since 2007. The European stock markets were significantly weaker than that of the US. The explanation for that was a combination of profit warnings from mainly cyclical chemical companies, as well as the large difference in economic data points. The US surprised positively, while Europe surprised negatively. Below image clearly illustrates the difference in the form of the Goldman Sachs Economic Surprise Index.

Source: Goldman Sachs

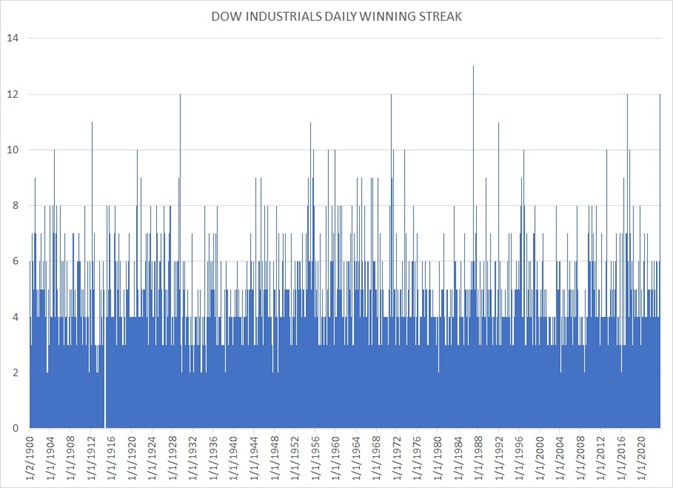

After the first week was over, there was a remarkable turnaround in investor sentiment and stock prices rose across the board. The Nasdaq, once again, rose the most (in local currency) during the month by 4% and thus has, in July, alone risen for 16 years in a row. The Dow Jones rose for 13 consecutive days which was the longest period of positive days since 1987. The picture below is missing the thirteenth day (far right bar) but note that in 123 years it has only happened twice! Also interesting was those American regional banks (which started the banking crisis in March) rose by 19% in July. European banking shares rose 5.5% over the same period, marking the best month for banking stocks since November 2016.

Source: Holger Zschaepitz, X

In Europe, the SXXP600 rose in July by 2%, while the MSCI Europe Smallcap increased by 3.2%. In general, smaller companies had a stronger price development than the larger companies. By far the worst was OMX, which fell by 2.6%. However, measured in euros the decline for OMX was -0.8% (yes, that's true, the Swedish krona strengthened in July).

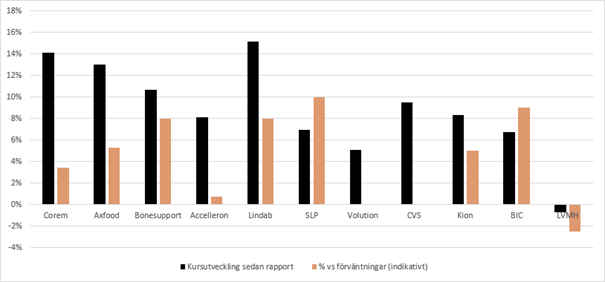

In the middle of the intensive reporting period, the fund performed well and generated a positive return of 4.9%, adjusted for the spin-off of Rejuveron which we told you about in last month's newsletter. For the third time in a row, our companies offered a very good price development in connection with their reports, which led to significant excess return. As a backdrop and to put into context, the companies that did not meet expectations saw their shares come under heavy price pressure. Some well-known Swedish companies' price movements at the reporting date were Hexagon -10%, SSAB -14%, Electrolux -20%, Ericsson -9%, Viaplay -49% and Essity -9%.

The image below shows the price development of our core holdings from the reporting date until the end of July. As clearly illustrated the outcome for our companies in relation to the market's expectations was clearly positive, which for many holdings gave a very strong price development. The only one of our companies that was worse than expected was LVMH with -2.5% in negative deviation and where the share fell by 5% on the day of the report, only to rebound the next day with a rise of 4%.

Source: Coeli European

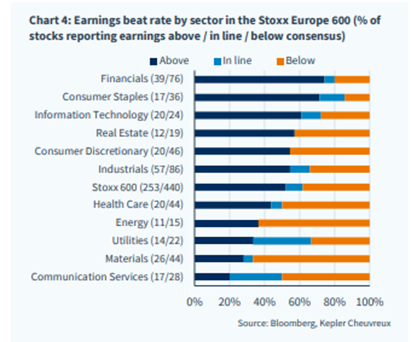

Up until July 31st, the results among the European sectors were as follows. Banks at the top and telecom at the bottom. Real estate stood out positively and oil and mining companies negatively. So far, 46% of the companies have had their profit forecasts adjusted upwards compared to 54% for downward adjustments. It is worse than it has historically been, and real estate, banks and automotive companies contribute to the biggest upward adjustments. The largest share of downward adjustments comes from mining and oil companies and technology companies.

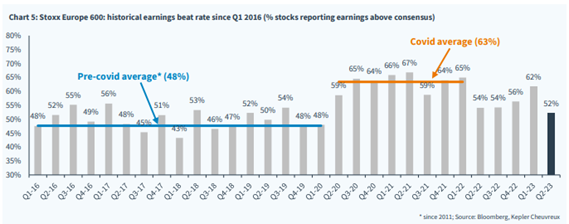

The percentage of companies that exceed the market's expectations is significantly lower in the current quarter compared to the first of the year and compared to the entire Covid period. Compared to the period before Covid; however, it still looks solid.

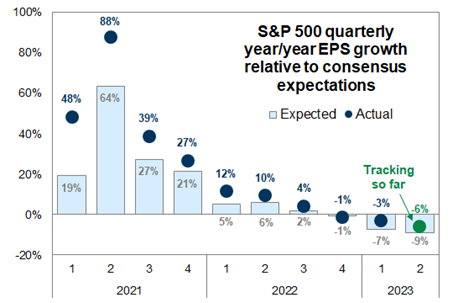

The corresponding outcome for the American stock market at the end of July was as follows.

Expectations were low with a combined profit decline of 9% for the second quarter. With 81% of the companies reported, the decline is only 6%. The last quarter was also better than feared.

Source: Goldman Sachs

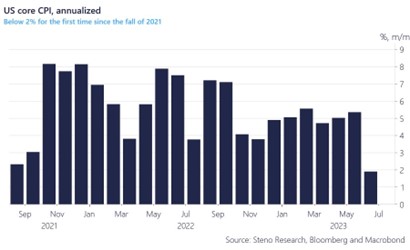

Inflation continues to fall in most countries. The USA is also at the forefront here, and forward-looking core inflation based on the latest monthly data is now below two percent! This then provided good fuel for July's share price development. Will there be more interest rate hikes? Possibly one more is our guess, then it reverses.

Will we see a significant drop in European inflation after the summer? There are many indications of that, and we feel somewhat reassured for the future.

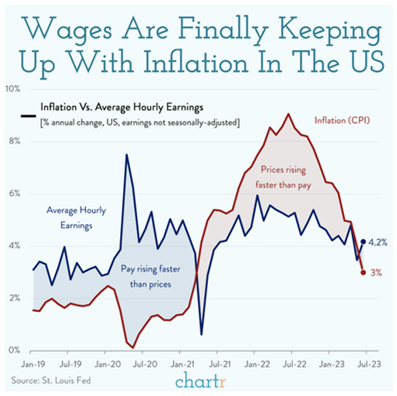

American wage growth now exceeds inflation, see intersection on the right of the image. It is of course very gratifying for the consumer and thus for the economy as a whole. Here, Europe is probably 6–9 months behind in development (and Sweden most likely at the back of the queue).

Source: St. Louis Fed, chartr

The Fed continues to dismantle its gigantic balance sheet. The temporary bump in March was when the banking crisis was in full swing, and they were forced to increase liquidity in the market. The Fed's balance sheet now corresponds to 31% of US GDP compared to the ECB's 53% and the Bank of Japan's 128%. The Riksbank's balance sheet corresponds to approximately 30% of Sweden's GDP.

Source: Bloomberg

Long positions

Accelleron

We last wrote about Swiss Accelleron in our monthly newsletter in November 2022. At that time, the company had just been spun off from ABB. In connection with the spin-off, we saw an opportunity to buy the shares at a discount. Since Accelleron is Swiss and small compared to ABB, there were probably many ABB owners who, due to fund restrictions and other reasons, did not want and/or were able to own Accelleron shares. This created initial selling pressure which we used to buy our first shares at a price of 16-17 Swiss francs, compared to today's rates of around 22.80.

The business consists of selling and maintaining turbochargers for large engines with applications for ships and in certain industrial applications. The company is the industry leader with a high market share. About 25% of the revenue consists of product revenue, while the other 75% consists of stable aftermarket revenue consisting of service and the sale of spare parts. The service revenue has very good profitability, and in the long run Accelleron should reach an operating margin of around 25%.

In July, Accelleron came out with some welcomed news: They raised this year's sales forecast to 15%, compared to the previous guidance of 2-4%. This is a substantial increase in forecasts motivated by strong end customer segments. In addition to a strong marine market, we already know that Accelleron has exposure to US natural gas infrastructure. This is likely to be very strong after Russia's invasion of Ukraine, which has meant that Europe needs to import energy from elsewhere, which in turn has led to a strong expansion of American LNG infrastructure.

The new forecast for 2023 implies an organic growth of 6% for the second half of the year, to be compared with 20% in the first half of the year. This appears conservative, and we believe there are good opportunities for Accelleron to beat its forecast once more before the turn of the year.

After a 7% rise in July (9% in euros), Accelleron still trades at a P/E ratio of 12-13x for 2024 on our estimates. We think that is far too low for a market leader with predictable revenues and a high return on capital employed of over 30%. The company's high cash conversion should allow a dividend yield of 7–8% for the profit in 2024.

Lindab

It is hardly a secret that the construction industry is having a tough time right now. In a European context, the Nordic region is particularly negatively affected. So far in the cycle, it is primarily housing construction that has taken a serious hit in relation to previous years. Commercial and industrial construction has been more stable. As so often in a downturn in the construction industry, it is new construction that has taken the biggest hit compared to renovation activity, which is typically more stable.

At group level, Lindab generates most of its revenue from the commercial sector and approximately half of the revenue is of a renovation nature.

Ahead of Lindab's Q2 report, we noted several things that made us increase our position:

- British cement and brick maker, Forterra, saw its shares rise on a profit warning that indicated analysts' expectations needed to be revised down by about 20-30%. Sector colleague, Ibstock's share rose at the same time out of sympathy.

- The British construction-related company, Kingspan, delivered good results given the conditions and the share price reached its highest level seen in the last year.

- We have also noted that companies in completely different “bombed out" industries, such as the European chemical sector, have seen rising share prices on profit warnings. It could possibly indicate that we would see similar reactions in other sectors with poor sentiment.

- Analysts' estimates had been adjusted down considerably before the report was released.

When the report later came out, EBIT expectations were beaten by 9% and the stock rose 11% during the day. Organic growth was negative at -13%, which was however, better than expected. During the conference call, we noted that CEO, Ola Ringdahl, said that June was a better month than May, which in turn was better than April. We dare not extrapolate this sequential improvement to future quarters, but of course hope for the best.

Like most good companies operating in a down market, the near term is all about gaining market share. In the longer term, we believe that the market will focus on the long-term trends that benefit the company. Regulatory requirements from the EU will likely provide good structural growth for many years to come. Based on our estimates, Lindab trades at a single-digit EV/EBIT multiple in 2025e, which is very low in relation to Lindab's historical average. Although the next 12–18 months are difficult to forecast, we see great upside in the stock in the long term. The Lindab share rose 6% in July.

Volution

Another ventilation company, UK-based Volution, provided a brief but positive update for the financial year ending last July. Organic growth for the full year is expected to land at 5%, even though the business mostly consists of ventilation products for homes. We partly own the share for similar reasons to Lindab as we expect good underlying market growth over time while the company can supplement this with acquisitions where Volution has a proven good track record.

We significantly increased our position in June when the stock, without news, fell by around 15%. In July, Volution shares recouped some of the losses, rising 6%.

CVS Group

We have owned the British veterinary company for a long time. The predictable organic growth, supplemented by the acquisition of smaller clinics at low price tags, has been a successful recipe so far in the company's history. In July, the company came up with yet another report that pleased the market, when it announced its entry into the Australian market. Australia's veterinary market is significantly more fragmented than in the UK and Europe, giving CVS another avenue for growth. The stock rose 10% on the day of the report and 4% for the month.

Bonesupport

During July, Bonesupport delivered another strong report. Since the launch of Cerament G, the company has delivered far above expectations, which has meant that estimates have constantly had to be raised. In the weeks before the Q2 report, expectations were turned up considerably. Despite that, Bonesupport beat expectations by just over 8%. The company had growth of 75% compared to last year and adjusted for the currency, with the US being the big driver, a phenomenal 107% growth. Cerament G sales in the US are now as large as the predecessor BVF and on a rolling basis Cerament G is sold in the US for SEK 100 million, an enormous achievement for a newly launched product. Next year, the company is expected to receive approval for indication trauma, which is twice as large a market.

During the conference call in connection with the report, it was also said that the company is planning a new capital markets day already this autumn. Last year's capital markets day focused on the rollout and commercial journey Cerament G faced. The focus this time will be on new indications and areas of use. If we have to guess, spine will be a topic that is highlighted, and that market is four times as large as the market Bonesupport is active in today. One should ignore the multiples the company is trading at currently or next year. This is a product that will probably grow for many years to come.

If we assume that the company reaches the same penetration in the UK as in the US, then we can multiply the rolling sales by 8. Then they are still only active in 60 of 420 available hospitals in the US, that is, you can take the new number and multiply with 4. In orthopedics, a standard of care usually has between 40-60% market share. It is of course difficult for us to say whether Cerament G will become the standard of care in the US, but the fact that there is no standard of care, and that the procedure is far better, smoother and with better health economics makes it, undoubtedly, a hot candidate. The point is, again, that the market doesn't even price in a 10% market share. At the time of writing, the stock has risen nearly 70% this year and trades at EV/Sales 8.3x on our 2025 estimates.

SLP

SLP reported its Q2 report in July. The operating profit came in 10% better than expected and showed a growth of 27% compared to last year. We have written several times before that SLP is a real craft, which we are now gradually witnessing. Despite the yield requirement being raised by 10 points to 5.9%, the company managed to achieve positive value changes, which shows that the work they put into improving their properties and projects is paying off. SLP trades at a 5 discount to our expected NAV in 2025, something we think is attractive. After having raised SEK 500 million a few months ago, they now have a fighting position in a market with more sellers than buyers. The management and its strong balance sheet will likely continue to create value for us as owners for many years to come.

Corem

Corem was the portfolio's best stock during July with a rise of 40%. The report itself was relatively undramatic but came in better than analysts expected. Rental income rose by 11% compared to last year. It is a sign that the underlying business is working. Net lettings were also positive again during the second quarter.

So far this year, Corem has sold properties for almost SEK 12 billion and all close to book value. This means that you can now redeem all bond maturities in 2023 and start buying back bonds maturing next year.

We think the odds are good that they will succeed in selling more properties this year at acceptable prices. Successfully selling properties at book value is a really good deal for shareholders when the company is traded at around a 70% discount to NAV. On our wish list as owners is to continue selling properties for 7–9 billion this year. That would enable all 2024 due dates to be met. After that, our view is to initiate a substantial buyback program and execute. If, against the odds, the stock continues to trade around these levels after sales mentioned above, enormous shareholder value is immediately created for all of us owners. To be continued.

Axfood

We made our first investment in Axfood in April this year when we were looking for defensive companies with strong growth and a high return on capital employed. The company, with its strong position in the Swedish food market, has in an almost unique way outclassed its competitors in recent quarters, with revenue growth well above ICA and Coop. It is Willy's low-price concept that has hit home with the Swedish people by offering attractive value for money deals. Sales growth during the second quarter was 19.7% compared to the market's estimate of 9%. Growth fell slightly from Q4-Q1 where it was as much as 23-24%, where the market was also around 9% during that period.

Despite strong results in the past year, the share has had a very weak development. This is due to (in our opinion) an initially high valuation and the fact that, starting last autumn, investors began to allocate capital to businesses with a higher risk profile than Axfood. The result for the second quarter was about 5% better than expected, and with comments about a continued good outlook for the company, the share rose by as much as 8% on the day of the report. It's unusual for this type of stock, but it had entered the reporting period really weak. The position was one of the fund's larger ones, which led to Axfood making a significant contribution to the month's results.

Source: Bloomberg

Kion

We last wrote about the company a month ago, when Kion was a strong contributor to the fund's results in June. It was followed up in July when the share rose by another 3% after a quarterly report that was better than the market's expectations. Despite the company being cyclical, with all that it entails, where we are now in the economic cycle the investment thesis is about restructuring the company after a very difficult 2022. With two good quarters behind it, the risk premium is now decreasing which, in this case and on good grounds, has been very high.

At the current share price (38 euros) and after a 17% increase in June/July, the stock is trading around 12x, 10x and 7x net earnings for 2023-2025e respectively. About 1.5 years ago, the share price cost was approximately 100 euros.

Short positions

The short portfolio contributed with a minor negative result during the month.

Exposure

The net exposure, adjusted for our unlisted holdings, at the beginning and end of the month was 73% and 85% respectively.

New strategy for Coeli Absolute European Equity

Since inception of Coeli Absolute European Equity at the beginning of 2018, the focus has been to create an attractive excess return with a limited number of holdings. Simplified and except 2022, that objective has been achieved.

With six years now behind us, we have decided to focus exclusively on long positions.

Why do we do this?

• If you study historical returns data in detail, it is clear that a few stocks in our long portfolio have made a very strong contribution to performance over long periods. It was also the main reason that last year, in global competition, we won a large mandate for Norway's sovereign wealth fund, with a focus on small and medium-sized companies in Europe.

• Historically, we have been better at generating excess returns in the long portfolio compared to the short side.

• When we today look at Coeli European AB's total managed capital, Coeli Absolute European Equity accounts for around 15%. The short positions in relation to total capital represent only about 3% but require significantly more resources. Time that has a high opportunity cost when we look for interesting long investments.

The logical consequence is to change the strategy to an actively managed European equity fund which frees up analytical capacity to focus on our long holdings, likely benefitting all of us invested in Coeli Absolute European Equity.

What does this mean for investors?

• Typically, the policy change will be implemented 30 days after this announcement. It is therefore estimated to be at the beginning of September.

• In practical terms, at that point we will close our short positions and then be fully invested with existing long holdings. This is expected to take place over one day.

• The performance fee of 20% will be replaced by a relative performance fee of 15% in benchmarked to the MSCI Europe SMID Cap Net Total Return Index.

• No performance fee will be charged to existing or new investors in existing share classes until the unit value reaches its high watermark. That level is approximately 40% higher than what the share value is today. For any future investments in a newly opened share class, a performance fee according to the new method will be charged.

• The name of the fund changes 30 days after this announcement to Coeli European.

As significant co-investors and as managers of the fund, we ourselves are very much looking forward to this change in strategy. This is because we are convinced that it provides better conditions for creating long-term value for our investors. We hope and believe that you too see this as a positive change.

Summary

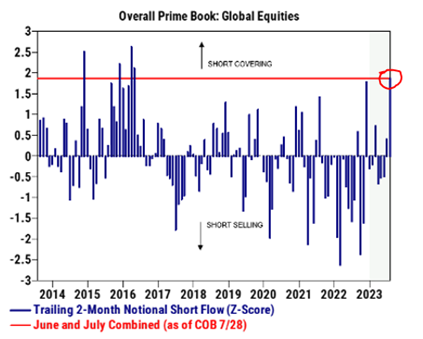

A summation of the summer so far is better than expected economic data from the US which in turn increased investors' hopes for an economic soft landing. Europe has displayed the opposite, where the manufacturing industry in many places now shows clear signs of lower activity. China's economic development has so far been disappointing and now the government's incentives are increasing to try to jump-start the economy. Investors latched onto it and over the summer the Chinese stock market has seen large net investments from foreign capital. The combination of the above produced a positive return on the European and American stock markets in July. A significant contribution came from investors largely closing their short positions.

Strong economic data has meant that US cyclical companies have performed significantly better than defensive companies, measured in the last three months. In the period May to July, cyclical companies have risen by around 18%, while defensive companies have risen by a more moderate two percent. The image below also shows the Goldman Sachs Surprise Index (yellow line) together with Cyclical/Defensive Development (white line).

Corresponding development in Europe during the same period more moderate +2.5% for cyclical companies, while defensive companies have fallen by 2.5%. It becomes very clear that cyclical companies are dependent on positive financial data to develop strongly (and the opposite is also true).

Source: Goldman Sachs

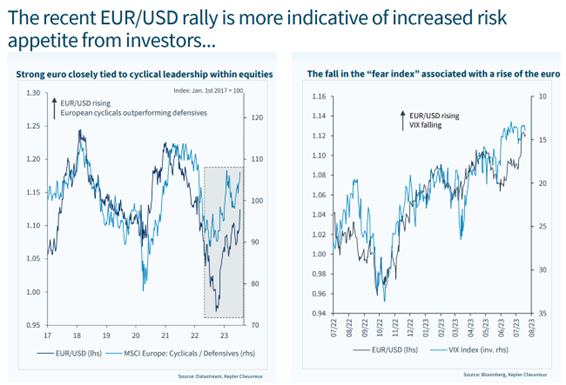

A strong euro indicates increased risk-taking, which can be seen in the share price development of cyclical companies and a falling volatility index.

When a majority of the companies have now reported, it can be stated that the expectations going forward are a significant improvement in profits. Below you can see the expectations for the American market (S&P500). After declining profits in the first half of the year, the forecasts are now profit growth of 5.4% in the third and 8.1% in the fourth quarter.

Source: SoFi, Refinitiv

If you adjust for the largest American technology companies, the valuation still looks attractive in many places. Below S&P500, MSCI China and MSCI World excluding the USA.

Source: Kepler Cheuvreux

After the AI hype of the last few months, the American stock market has developed significantly better than the European one. Over the past three months, the S&P500 has risen by 10%, while the SXXP has only risen by one percent. However, the annual return so far this year is very similar, see picture below with current data as of August 7th. On the far right is the yield measured in euros and Sweden's weaker development is clear.

Source: Bloomberg

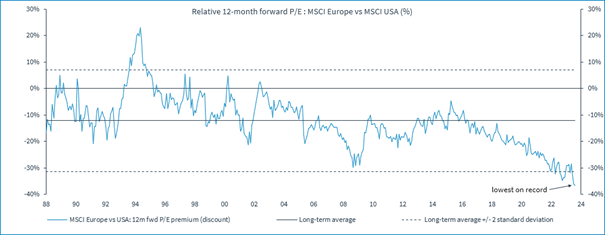

The latest development has in turn created the biggest value difference ever between the US and Europe.

Source: Kepler Cheuvreux

Below the difference in P/E between the US and Europe.

Source: Kepler Cheuvreux

The relatively record-expensive US stock market is also record-expensive in relation to the 10-year Treasury yield. Currently, not much compensation is offered relative to the risk associated with owning shares.

Source: @soberlook

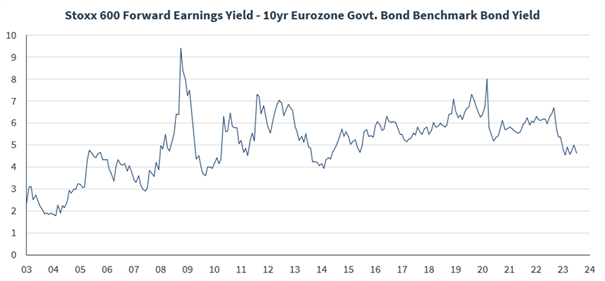

Europe exhibits completely different relationships where the profit level in relation to the 10-year bond yield is five percent compared to the US's one percent.

Source: Kepler Cheuvreux

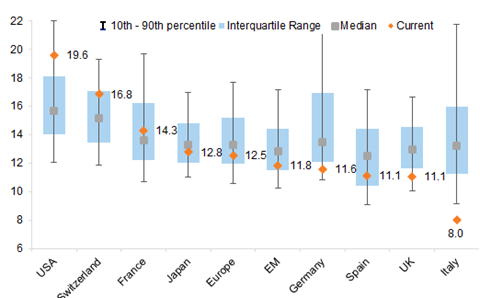

Below is a current picture showing the valuation for several important stock markets.

Source: Goldman Sachs

So how do we see the development from here? At the time of this writing, the first days of August have started with a downward recoil of around three percent. The US downgrading by Fitch can probably be considered the catalyst and a reason to take home profits in the short term. A strong development in July combined with the fact that European and American investors are now going on vacation means that the conditions in the short term (weeks) are moderate.

Outflows from equity funds have historically been significant in August, which has historically had an impact on the current month's return.

Source: Goldman Sachs

CTAs (trend-following strategies) have increased their equity exposure over the summer and are predicted by Goldman Sachs to lead to sales in August regardless of price performance.

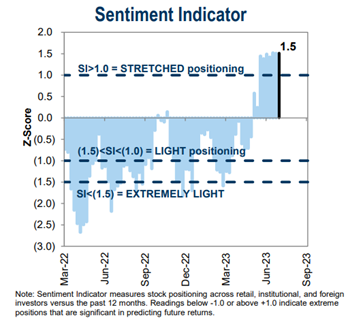

Risk appetite has increased significantly, and investors are now more exposed.

Source: Goldman Sachs

There have been very high volumes (see picture below) in terms of covering short positions and is now largely settled.

Source: Goldman Sachs

On the positive side and if we zoom out, the companies' earnings have continued to be higher than expected. Now the giant buyback programs are also starting up again, which support the share prices and, in many cases, create significant shareholder value.

Although the impact has diminished in recent months, it is still the central banks' fight against inflation and, by extension, interest rates, which largely dictates the development of the world's equity markets. Here, our view continues that they have been too aggressive this time as well, which in turn, if we are right, will lead to a reversal and a significant fuel for the global risk appetite. When Jerome Powell held his press conference in connection with the Fed's interest rate announcement on July 26th, he said, among other things: "You'd start cutting before you go to 2% inflation". When the ECB held the corresponding press conference the following day, Christine Lagarde was asked if the ECB had more work ahead: "At this point I wouldn't say so".

Thank you for your trust and interest.

Mikael & Team

Malmö on August 9th, 2023