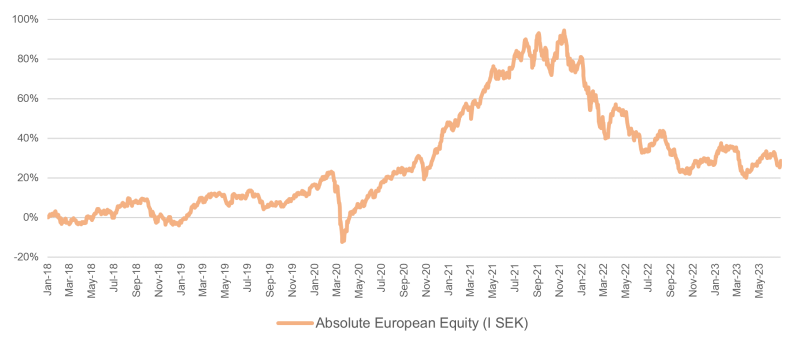

Note that the information below describes the share class (I SEK), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class' return. The information below regarding returns therefore differs from the returns in other share classes.

Before making any final investment decisions, please read the prospectus, its Annual Report, and the KID of the relevant Sub-Fund here

This material is marketing communication

Monthly Newsletter Coeli Absolute European Equity – June 2023

JUNE PERFORMANCE

The fund’s value decreased by 1.4% in June (share class I SEK). The Stoxx600 (broad European index) increased during the same period by 2.3% and HedgeNordic’s NHX Equities increased provisionally by 0.6%. The corresponding figures for 2023 are an increase of 1.7% for the fund, +8.7% for the Stoxx600 and +1.5% for NHX Equities.

EQUITY MARKETS / MACRO ENVIRONMENT

After a weak development in May, the stock markets got a boost of energy at the beginning of June. Underlying reasons were, among other things, upgrades by influential strategists of the target price for the S&P 500 and continued strong economic data from the US, which in turn reduces the likelihood of a recession. US GDP growth for the first quarter was revised up to 2% against an expected 1.4% and labor market statistics as well as private consumption were also better than expected. Economic surprise indices accelerated, hitting 12-month highs in June. Where is the recession that was expected since a year ago? At the end of the month, further support came as bank shares rose after the Fed's stress test showed good resilience.

In Sweden, too, several forecasters published upward adjustments to their expectations. Arbetsförmedlingen (Jobcentre Plus) is busy, and the number of vacancies is pouring in, but companies are struggling to find the right skills. Even the Economic Institute is surprised by the strength of the labor market and that companies continue to invest at a high level. The flip side of this is that it further increases the pressure on the central banks and an interest rate cut is, all other things being equal, postponed.

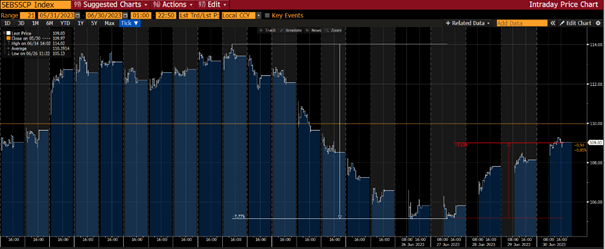

In the middle of the month, however, we experienced a drop in the stock market and especially for smaller companies. Double increases from both the Bank of England and the Norwegian central bank put a damper on the mood. In addition, several profit warnings were published which further contributed to a more negative sentiment. The chaos in Russia also did little to cheer up the world's investors.

Below is the development of the SEB Small Cap Index for June. Note the sharp decline from mid-month of 8% in as many days! By the time the month was over, barely half of the decline had been recovered. The development was similar for other small company indices in Europe. As a point of reference, the broad European index fell at most by 3.7% intra-monthly.

Source: Bloomberg

The dispersion between the price development of the smaller companies compared to the larger companies is still very large. We see many interesting investment opportunities among small and medium-sized companies and our strong opinion is that more investors will follow suit. In the US, the S&P 500 has risen this year by 15.9% compared to the Russell 2000, which rose by 7.2%. In Europe, the SXXP 600 has risen by 8.7% compared to MSCI Small Cap Europe, which has risen by 3.8%. In Sweden, the OMX 30 has risen by 13% (measured in euros by 7%) compared to the Carnegie Small Cap index, which rose by 4.5%. All measured in local currency.

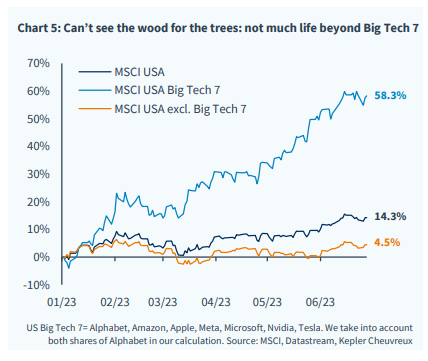

The large technology companies with their AI exposure continue to outclass other stocks. During the first half of the year, the remaining 493 companies in the S&P 500 rose by a modest 4-5% compared to the seven largest technology companies, which rose by an average of 58%!

One of the worst years ever for the Nasdaq last year (-33%) led to the best first half year ever, +38.75%!

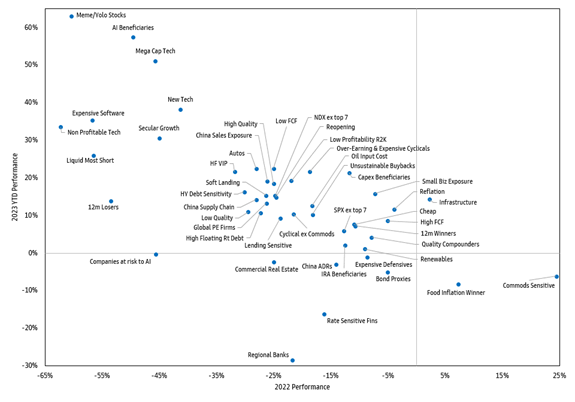

In general, the development for the first half of the year is in many cases exactly the reverse compared to previous year's development. The excellent image below shows on the Y-axis this year's development in relation to 2022's development on the X-axis. Fascinating!

Source: Goldman Sachs

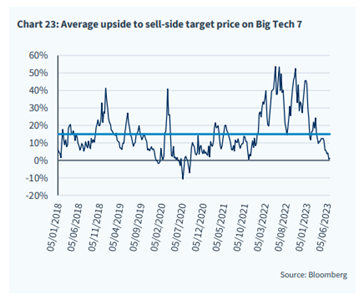

The AI theme has been and continues to be a very strong catalyst for the big tech companies' share price development. In relation to the analysts' target prices, however, the air is becoming thin and the potential limited. Of course, they could be completely wrong and underestimate this technological revolution, which is still in its infancy, but it feels like there needs to be some upward adjustment of the profit estimates to drive them forward in the short term.

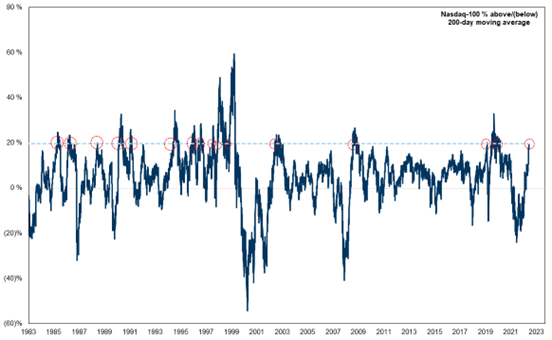

There haven’t been many instances in the last 40 years where the Nasdaq 100 has traded 20% above its 200-day moving average.

Source: Goldman Sachs

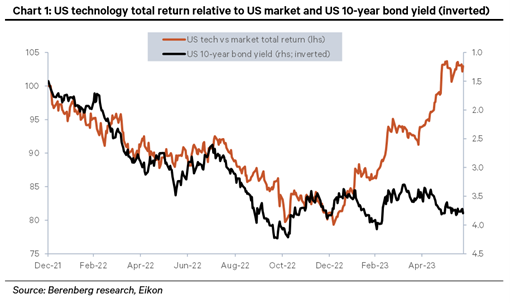

The returns for American technology companies have been completely disconnected from interest rate trends. Most likely they will meet again, but it is unclear whether it is the interest rate or the stock market that will give way first. Again, AI is a big explanation for the development (in our opinion). Another thing one should keep in mind, which has almost been forgotten, is when the Nasdaq was under maximum pressure a year ago, the Fed was progressing with four (!) 75-point interest rate increases in a row and inflation was considered to be out of control. What is now being discussed is whether there will be another hike of 25 or 50 points in the coming quarters, then interest rates will likely turn downward again. A completely different environment and for the better.

The point of the above images is to illustrate a very unusual situation with a small part of the market lifting the major broad indices. In Europe, unfortunately, we have no technology companies that can be compared to the American ones, but rather the luxury companies in Paris, where the fund has a large position in LVMH, which has risen 27% year-to-date. Despite that, Europe has generally held up well. The breadth is also better than in the US. Typically, Europe's equivalent of US growth stocks are small caps, but so far this year, that hasn't been the case. That could possibly be explained by the high concentration in this year's rise.

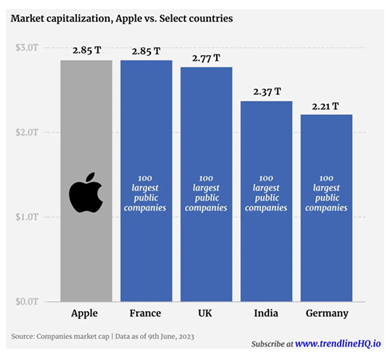

Hats off to Apple, which at the end of the month passed USD 3 trillion in market capitalization, larger than the 100 largest companies in France, for example. Digest and think about what it means in terms of power between countries and regions.

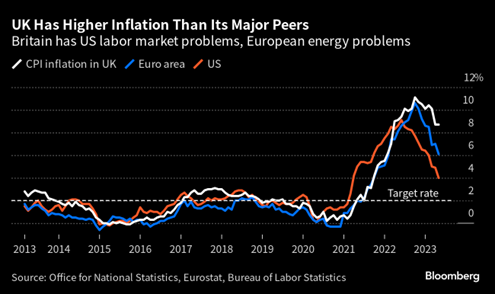

Inflation continues to fall and is moving fastest in the United States, which is beginning to approach normal levels. The eurozone also shows progress, but here the picture is somewhat divided. Sweden and our dysfunctional currency are pushing up inflation and, unfortunately, it is still above the average in Europe. Great Britain with its self-inflicted Brexit policy, is also struggling with inflation. The UK labor market is tight and largely due to the fact that the important influx of imported labor has almost completely disappeared. Did I hear Brexit? Please see the mastermind behind the spectacle, Nigel Farage, who openly admits that Brexit has been a huge disappointment. Being the great leader that he is, he blames the incumbent government for not implementing Brexit as intended. He cannot see anything wrong with Brexit itself.

➜ See the video with Nigel Farage: https://www.youtube.com/watch?v=uzfxGptsdGo

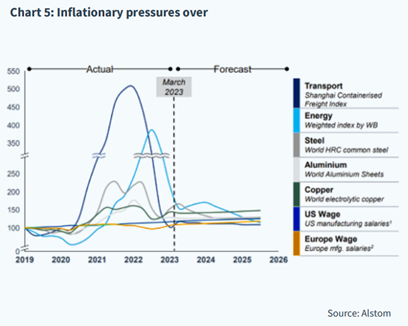

Illustrated in a different way and with the help of French Alstom. Inflation is now yesterday's history and considering how production prices are falling, we would not be surprised if in a year's time there is as much talk about inflation as today, although from the other perspective, that it is below two percent.

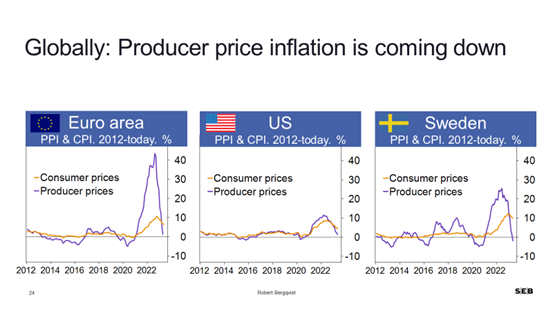

The Swedish producer prices published in June showed negative growth! The euro area and the USA also show sharply falling producer prices and if history repeats itself, the consumer price index is about 9 months behind in development.

The correlation between PPI and CPI in the UK below. It looks promising.

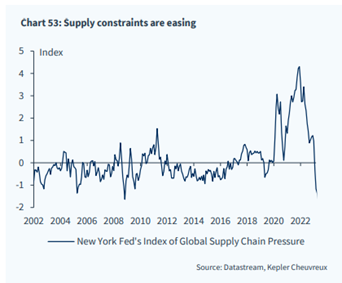

We experience greatly reduced bottleneck problems. Good for the economy including inflation.

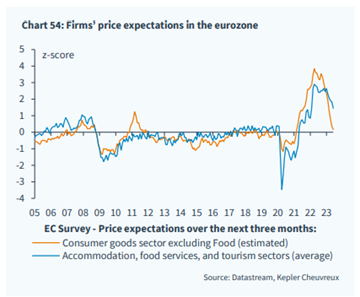

Price expectations among companies are also sharply decreasing. Also, positive.

Despite most things pointing in the right direction, the world's central banks continue to blindly push forward with interest rate increases and steer the future by looking in the rearview mirror. The interest rate weapon is a blunt weapon in today's world. The war and its economic consequences do not end because interest rates are raised. A high electricity price due to huge political errors in the last 20 years is not going to decrease when the central banks raise interest rates.

The figure below shows US inflation minus the Fed's key interest rate. If you zoom out, you can see that great progress has been made. Also it shows how massively behind the Fed (and all other central banks) were when it came to controlling inflation with interest rate hikes. The Fed's first increase came in April 2022. Consider that it is only 16 months since the Riksbank's (Swedish Central Bank) forecast that a first interest rate increase would take place in the second half of 2024... It is hard to fathom. An epic and historic erroneous forecast which explains why you should take all their forecasts with a very large pinch of salt. That they sit on so much power is fundamentally wrong for societies and citizens, but that is a longer discussion that we leave here.

Source: Bloomberg

As expected, our own Riksbank (Swedish Central Bank) raised the policy rate by another 25 basis points on June 29th and the policy rate is now 3.75%, which is the highest level in 15 years. Riksbank governor Erik Thedéen said he was completely at a loss as to the weak krona exchange rate, which may seem strange when most people who invest in currencies know that the Riksbank has been constantly working against a strong Swedish currency for the past 20 years. The expression "it's never too late to sell Swedish kronor" is a mantra among currency traders around the world. A frightening anecdote is when Trelleborg in spring sold its American company for just over 2 billion dollars and was going to change it back to kroner. It took all of 10 days to complete, as there was so little liquidity in the market. The rate would have moved far too much otherwise. It feels mediocre, to put it mildly. There are also more and more articles about holidaying Swedes abroad who are refused to exchange their Swedish kronor for the local currency as the exchange offices lose money when the kronor keep falling in value. How did we end up here?

Last month we wrote that it is incomprehensible that the Riksbank does not sell its euro and dollar assets to buy kroner. It was therefore gratifying that the Riksbank, after a review, concluded that they should now start doing this. They were careful to say that it was only to be seen as risk management and firmly denied that it was not to strengthen the krona. The foreign exchange reserve is 410 billion and the market assessment is that they will buy kronor for 100 billion over time. Very welcomed!

Apart from that, people were grateful for the in-depth analysis conducted by Sveriges Radio during the holidays, which had discovered that the krona had weakened. They had done an analysis of where you could go on holiday if you "wanted to get a lot for your Swedish kronor". The alternatives were four countries: 1) Turkey 2) Romania 3) Hungary and 4) Albania. Three former communist dictatorships and to add insult to injury Turkey is what is recommended. Thank you Public Service for this great advice, but it will probably be Österlen (south of Sweden) for us instead.

The mood dropped that day when it was noted that even the Albanian currency, Lek, developed 28% better than the Swedish krona in the last 18 months (see image below). Since mid-May alone, the Sweden's population has lost 6% in purchasing power compared to the residents of the eurozone. These are extremely large numbers.

Source: Bloomberg

Undoubtedly the biggest event of the month was when the head of the Wagner Group, "Putin's Executioner" Prigozhin, took his men on Midsummer's Day and headed for Moscow to challenge the Russian Defense Minister. It was full steam ahead in Moscow and after a 20-mile journey it was telegraphed to the world that everything had been canceled and that Prigozhin had instead been offered a free ride to Belarus. Putin addressed the people and compared it to the revolution of 1917. Undoubtedly, Putin's position has weakened and the probability of Prigozhin celebrating Christmas this year is probably very low. Reality is now quickly catching up with Putin, as it always does sooner or later for dictators. Wars are never decided on the battlefield, but through negotiations. Ukraine has strengthened its cards and is now gearing up for the big offensive. Financial markets reacted with a shrug except for world defense stocks which came under heavy pressure on Monday as markets opened. Investors interpreted the events as meaning that the war, all other things being equal, will now last for a shorter time than what was on the cards the day before. Somewhat cynical but hopefully accurate.

Source: Financial Times

In the country of Annorlunda, there was a lot of focus in the Riksdag (Swedish Parliament) with raised inflexion and intense debates regarding the existance of their lottery operations. Not impressed with their prioritization.

Long positions

Bonesupport

The Bonesupport share continued to perform strongly in June, with an increase of 8%. This after an increase of 15% in May, and +23% in April. The stock is the fund's largest positive contributor in 2023. On July 13th, the company will come out with its report for the second quarter of 2023. The main number, again, is how the company's launch in the US is progressing. At the time of writing, the large American asset manager, Capital, has flagged that they own 5% of the votes in Bonesupport.

ISS

After the company's esteemed CEO, Jacob Aarup-Andersen, announced his resignation in March to move over Carlsberg, the ISS share has had a slow development. There has been much speculation about his successor. Our favorite candidate for the job has been the company's finance director Kasper Fangel. This is because he is very enthusiastic about the company's turnaround strategy, which has been appreciated by the market and which is the main reason why we invested in the company. In June, it became clear that it is Kasper Fangel who will take over the helm after Aarup-Andersen, which we think is gratifying. The ISS share rose 9% in June.

Corem

Real estate shares continued to be under pressure in June, where the turbulence around SBB continues to put pressure on the sector. It also affected the Corem share, which fell by 16%. Earlier this year, the company had communicated a declaration of intent in a large structural deal, where it intended to sell parts of its holding in Klövern to a major foreign player. The planned handover was at the end of the second quarter. It dragged on due to complexity and negotiations which pushed the share price down, but on Monday July 3rd the deal was announced. The value of the company consists of 24,000 attractive building rights. Our assessment is that until now the market has probably valued the holding in Klövern at zero, as it is currently challenging to develop housing. The fact that Corem needs to reduce its debt also does not favor their holdings in a housing developer.

Our view of the sale is very positive as it now frees up a total of 1.4 billion (compared to the market value of 7 billion) which will be used to buy back bonds maturing in 2024. After that, approximately 3.5 billion remains. This year alone, they have sold properties for 8.8 billion, sold their holding in Castellum for 1.2 billion and now sold shares in Klövern for 1.4 billion. A total of 11.4 billion and all properties around book value, while the share at the end of June traded at approximately 80% discount to NAV. In addition to the above, the risk premium in the company also decreases.

Our view of Corem is that they should continue to sell to buy back the last bonds maturing in 2024. To our knowledge, there is no other company in Sweden that has sold as much in relation to its balance sheet as Corem this year, and at book values. When it is ready, the buyback of their own shares will be on the agenda. At current levels, it is extremely valuable to buy back shares while selling around book value. The stock rose by 14% percent on July 3 and thus recouped the entire month of June's price loss.

Finally, we note that the main owner of Corem, M2 Asset Management, on the last two days of the month announced two property sales, as well as redeeming the balance (174 million) of a bond issue due in July (926 million in total).

SLP

Our other property holding, SLP, rose by just over three percent in June and ended the month by announcing its biggest project to date. Together with Ahlsell, they are investing and completing a project totaling approximately 800 million to then rent it to Ahlsell. The rental value of approximately 50 million per year corresponds to 10% of today's entire rental value. The contract length is 15 years, which means that the duration in the portfolio increases. Well done!

Sacyr

After owning French Vinci during last year, we chose to sell the holding at the beginning of 2023, after a strong price development and due to valuation reasons. We discovered an equivalent asset to Vinci at a significantly more attractive valuation in Spanish Sacyr. The business consists of running and being responsible for various concessions in the world and mainly consists of developing and operating private motorways. A stable and cash flow generating business which we appreciate.

In June, it successfully sold its service operations for just over 700m euros including debts, which makes the company debt-free. Including dividends, the share rose by 18% in June and was the fund's strongest contributor during the month. This year, including dividends, the stock has risen by around 27%. As a parenthesis, Vinci has risen by 17%.

Kion

Another strong contributor to the month's results was Germany's Kion. It is a cyclical company which, combined with a major restructuring, offers, in our view, an attractive investment at these price levels. Better-than-expected macro data likely contributed to Kion's and other cyclical companies' positive price performance in June. The share rose during the period by 13%.

Volution

Our holding in UK Volution offered decent volatility in the second half of June. The company is a leader in energy savings for indoor climates and has maintained a high quality of earnings and balance sheet for many years. After being stable in terms of price for a longer period, the share came under considerable pressure. At most, the stock had fallen almost 25%. The catalyst was likely the British construction market company, Travis Perkins, issuing a profit warning. By the end of the month, Volution shares had fallen 15%. We believe that the price drop triggered various stop losses where managers sell to reduce risk. In addition to the profit warning mentioned above, there were also European construction statistics that showed continued low activity.

An update to the market is scheduled for July 20th and we're looking forward to it! Travis Perkins stock only fell 7 percent in June! Below is Volution's share price over the past year.

Source: Bloomberg

Short positions

The short portfolio contributed with a minor negative result during the month. The biggest negative contribution came from our put options in the German DAX.

Exposure

The net exposure, adjusted for our unlisted holdings, at the beginning and end of the month was 73% and 79% respectively.

Important change to our investment in Rejuveron

The Fund invested in Rejuveron in December 2019. The initial position size for the portfolio was approximately 1% at a valuation per share of 19 CHF. The year after we participated in another financing round at a valuation of 30 CHF per share. The Fund’s position during this time around was 1-2% of assets under management.

In April 2022, the company once again raised more capital at a valuation of 120 CHF per share which increased the size of the position approximately four times. We did not allocate any more capital to the company in this financing round.

The company is currently in the final stages closing a convertible note with prominent investors included. The next step is to do a public IPO which has been prepared for a long time. Due to market conditions and changes to the capital raising strategy, the process has been delayed, however, the target for the IPO is now Q4 this year. Everything is well prepared and ready to go if market conditions are suitable. If everything goes according to plan, we will make an exit accordingly which is by the latest when our lock-up expires following the IPO (typically the lock-up is 6 months but this is to be confirmed).

Due to the strong development of the share price and thus a large position for the fund, we have decided to create a separate share class for Rejuveron. This can be compared to a share dividend. The size of the position in the portfolio at the time of the separation was approximately 7.6%. Any future withdrawals from the fund would increase the size of the position and vice versa.

Alternative options to creating a separate share class were thoroughly explored, but our assessment is that it is the best solution and in the interest of shareholders and investors.

The NAV in existing share classes fell on the 3rd of July by the equivalent of the value that the shareholders received in the new share class. However, the shareholder's total investment will have the same value, i.e., the existing share class plus the new share class.

No valuation adjustments have been made in connection with the convertible. We have during the second half of last year done two write-downs of the valuation, mainly due to the interest rates rising and the market conditions at the time. Our valuation stands at 91 CHF per share which is approximately 25% lower than the valuation at the last capital raise. That combined with the current strong demand for the convertible makes us optimistic that we will make an attractive exit next year.

We are still fully responsible for the position and the new share class. No management fee is charged from the new share class.

About Rejuveron

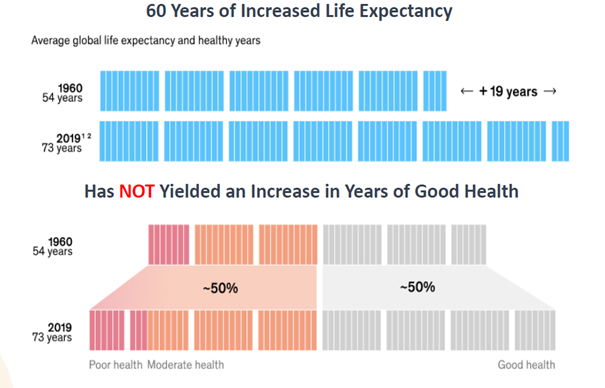

Rejuveron is a Switzerland based clinical stage biotechnology company that develops and invests in therapies for age-related diseases and human longevity.

Rejuveron strategy is to help people age better and live longer. As can be illustrated in the picture below, global lifespan has increased but without quality.

Source: McKinsey Health Institute Report

Rejuveron’s business strategy is drug discovery within aging and to build a broad pipeline of new therapies via founding or investing into a diversified set of therapeutics companies. Its portfolio currently consists of five different therapies/companies:

• Stem cell regeneration (Endogena)

• Vascular systems (Vascular therapeutics)

• Cancer senolytics (Senescence therapeutics)

• Telomere shortening (Telomere therapeutics)

• Muscle degeneration (Rejuvenate Biomed)

For two of the above investments, Endogena and Senescence therapeutics, the company thinks a large M&A or licensing deal is likely within 1-2 years.

Summary

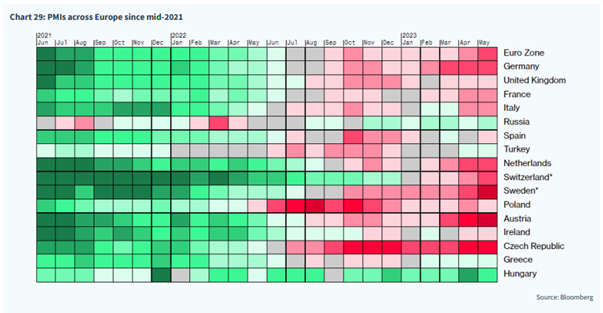

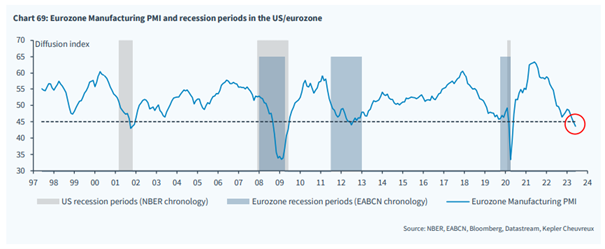

Despite a clear slowdown in most economies since a year ago, Europe is not yet in recession. Despite challenging conditions, the companies continue to show good profitability and impressive endurance, which surprised most. Below is the monthly development for the Purchasing Index (PMI) for various European countries.

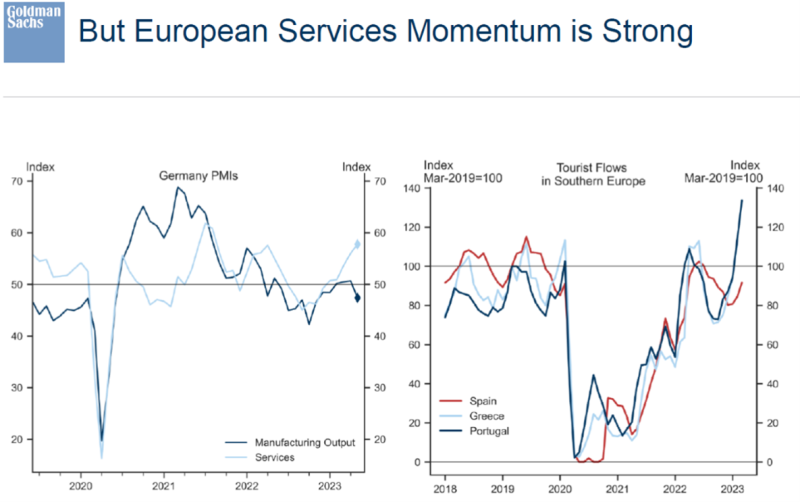

The picture below on the left shows the German purchasing index in the manufacturing industry. The picture on the right shows the tourist flows in southern Europe and we are back, or above 2019 levels.

The image below shows the manufacturing and services PMI for Europe. Services appear to be declining and an unusually large gap has opened between the manufacturing PMI and the broad European index Stoxx 600. If the economy does not gear up in the coming months, there is a risk that the stock market will fall back. Recent weeks have seen profit warnings presented among chemical companies, which resonates well with the graph as they are early in the economic cycle.

Source: Bloomberg

There have been many extraordinary events in recent years with an extreme recession three years ago, followed by extraordinary monetary policy measures and then the outbreak of war in Europe, which left investors waiting for over a year for a recession. With the manufacturing PMI around 45, we may already be in a recession, but if so, our view is that it will be mild. A big reason for that is a continued strong labor market.

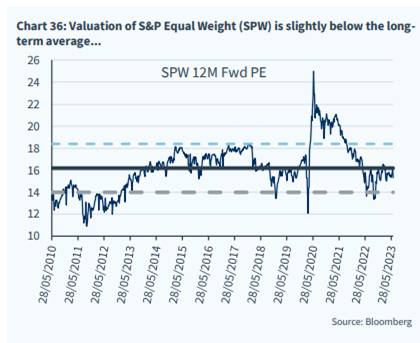

Although the stock market has risen this year, there is a lot of room for negative profit revisions. Based on how the market has historically been valued for various sectors in Europe, the valuation today is up to 40% lower. Important to keep in mind.

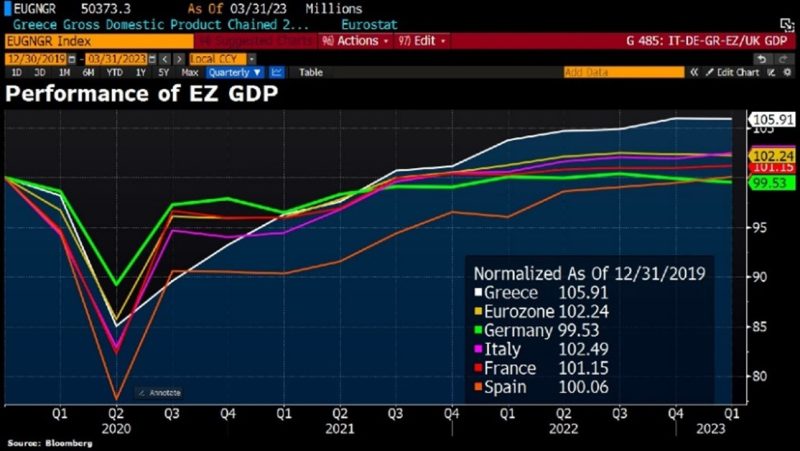

The Eurozone's GDP is now above the corresponding level in the first quarter of 2020. A problem in this context is that Europe's engine, Germany, has a worse development. The explanations for this are, among other things, a disproportionately large exposure to China that limps and major problems with the energy supply.

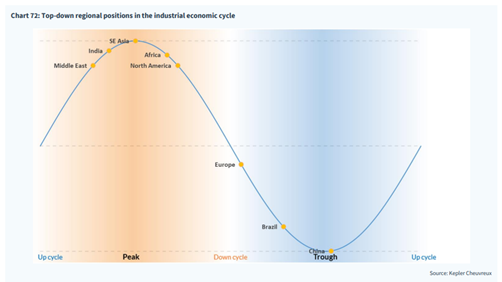

China's expected awakening as pictured below, will provide an extra and much-needed boost to Europe's economies which, with a shift, are expected to accelerate upwards.

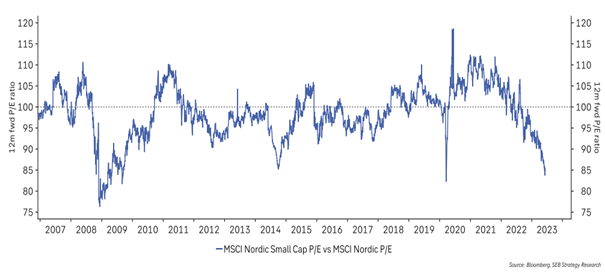

Our humble approach is that we continue to believe that investors are overly anxious and that stocks will generally offer a reasonable return from here until the turn of the year. As is well known, the rise during the first half of the year is thin, but our belief is that more companies will become in favour, including smaller companies. Small and medium-sized companies have historically given a stronger return than the stock market in general, and in time more people should start to discover this. The excellent image below shows the sharp relative loss in value for Nordic small companies compared to larger companies.

Source: Bloomberg, SEB Strategy Research

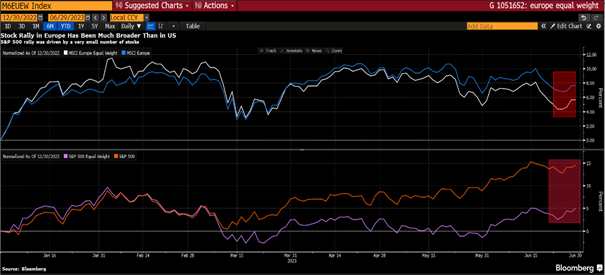

The rise in the first half of the year has been significantly wider in Europe compared to the USA. The image below shows the development for MSCI Europe compared to MSCI Europe equally weighted. The bottom image shows the same for the S&P 500.

For those who think the valuation of American companies is strained, it can be stated that for an equal-weighted index, the current valuation is below the historical average. Worth bearing in mind.

The US stock market is now higher than when interest rate hikes began at the beginning of last year. We've commented on the various reasons, but it's impressive to say the least. As a reference point, the Carnegie small company index needs to rise another 40% to reach its previous highest level.

Source: Bloomberg, Goldman Sachs

An important image below to understand that the stock market is not the same as the economy. The picture shows the development for American housing developers, which have risen by around 70% since last autumn. It does not reflect the development of their business, but cyclical industries tend to have dramatic turning points. The current interest rate for a 30-year loan in the US is 7.11% at the time of writing. Levels we in Sweden don't even dare to think about.

Source: Bloomberg

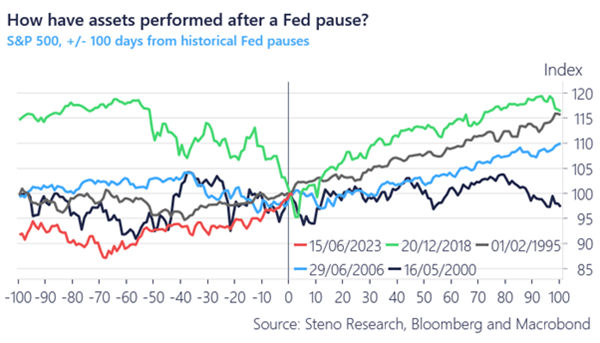

As you know, we are approaching the time when the interest rate increases have been implemented. Central banks don't usually stay at high levels for long (even if they currently communicate just that). They almost always overshoot, which usually leads to rapid interest rate cuts. The historical returns for the US stock market when the Fed takes a pause in its interest rate hikes look like below.

In conclusion, we note that June offered unusually little news flow from our companies, but all the more volatility in share prices. Our interpretation of that is mainly that several of our holdings came from a strong period in May and recoils come and go. We have taken advantage of the volatility both by buying at low prices, such as LVMH and Volution, and by reducing our positions in some of our holdings after a strong performance.

Following two strong reporting periods in a row, we look forward to this year's third reporting season. Generally speaking, we believe that the companies will once again show strong figures, even if expectations have risen somewhat after the very strong reporting for the first quarter of the year.

We conclude with the following positive image that shows the development of Nasdaq over the past 15 years per month. With 15 positive Julys in a row, the prospects in the short term feel good. Based on historical data and since 1928, the first two weeks of July are the strongest period of the entire year.

Source: Bloomberg

We wish you a sunny and relaxing July!

Mikael & Team

Malmö on July 5th, 2023