Note that the information below describes the share class (I SEK), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class' return. The information below regarding returns therefore differs from the returns in other share classes.

Before making any final investment decisions, please read the prospectus, its Annual Report, and the KIID of the relevant Sub-Fund here

This material is marketing communication

Monthly Newsletter Coeli Absolute European Equity - March 2022

March Performance

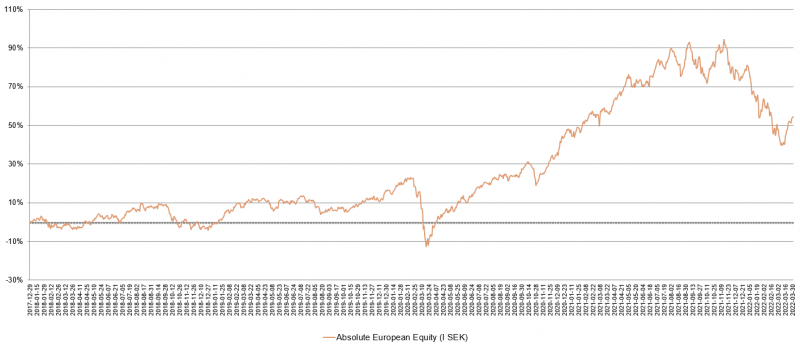

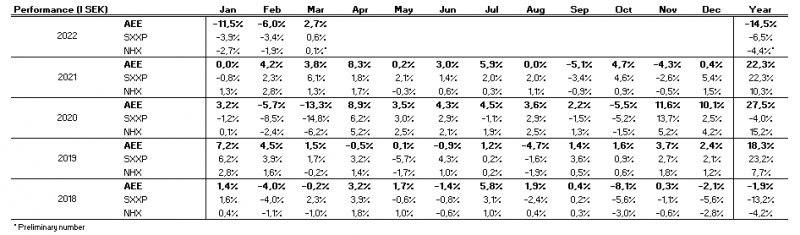

The value of the fund increased 2.7% in March (share class I SEK). The Stoxx600 (broad European index) increased during the same period by 0.6% and HedgeNordic's NHX Equities rose provisionally by 0.1%. The corresponding figures for 2022 are a decrease of 14.5% for the fund, -6.5% for Stoxx600 and -4.4% for NHX Equities.

EQUITY MARKETS / MACRO ENVIRONMENT

The first quarter of the year is behind us, and it will, unfortunately, forever be included in the history books. After a strong start with new ATHs at the beginning of the year, the US long-term interest rate rose because of rising inflationary pressures and put pressure on growth stocks. After the worst of the storm subsided and investors paused and calculated how big the public euphoria of regained freedom would be after COVID-19, a geopolitical catastrophe burst on February 24th with Russia's unprovoked attack on Ukraine.

With these conditions, the financial markets rolled into March. The first two weeks were exceptionally turbulent for, effectively, all available asset classes at once. The second half of March saw a significant increase in risk appetite and the stock markets showed a positive development. To demonstrate the extreme volatility, here are some examples:

- German DAX fell by 15% (!) In the first five days to rise by 11% in the next three days

- The Hong Kong stock market fell by 11% in two days and then rose by 17% in the following two days

- The oil price ranged between 95 - 135 USD

- The U.S. 10 Year Treasury Note rose from 1.73% to a high of 2.47%

- Bitcoin rose by 10%

- Price movements for individual shares were extreme. The share price in our own Victoria plc, for example, first fell a further 10% and then rose by about 40% in one week. Crazy and more important than ever to understand implicit valuation when stock prices move dramatically

- The Nickel price rose by about 100% in a few days and then fell back 40%

- Wheat and other raw materials also rose sharply by a high of 50%. This is really bad, especially for the world's poorest communities and we could see riots as a result (a new Arab Spring?)

- Our put options in DAX rose by about 500% from the end of February and two weeks forward and were at the top a significant position for the fund. We sold some and bought some further out and thus took a bit of profit. The price now from the highest levels is down 60-70%. Eyes on the ball.

- The Swedish Krona strengthened by as much as 6% in March.

That the Swedish krona strengthened by 6% in a few weeks is unusual and shows how wrong the Riksbank (Swedish Central Bank) interpreted its environment. An extremely skewed view of reality from the Riksbank put great pressure on the Swedish krona in February. When the reality came in the form of raw inflation data (+4.5%), the Executive Board woke up. What was communicated a few weeks earlier, that a first interest rate increase would not come until the second half of 2024, would now probably need to be revised. Astounding - how is it possible to make such significant forecast errors for several decades and still gain continued confidence? Since the Governor of the Riksbank is elected by the General Council of the Riksbank, who in turn is elected by the Riksdag (Swedish Parliament), it is probably due to a lack of understanding from politicians. Safe to say the above does not contribute to a long-term strengthening of the Swedish krona. Surely, it also fires up inflation. For everyone's convenience, we leave this topic.

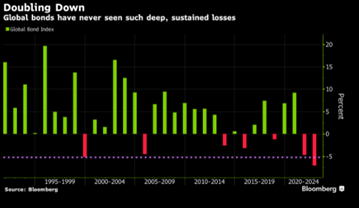

The sharp rise in long-term interest rates in the western world put considerable pressure on bond prices. Never before, has the price of bonds fallen so sharply in such a short time and a 40-year-old bull market thus seems to be over.

Source: Bloomberg

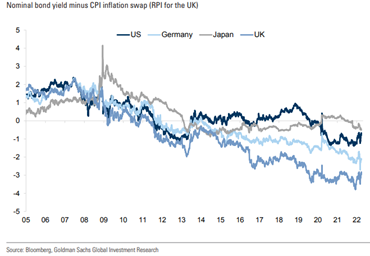

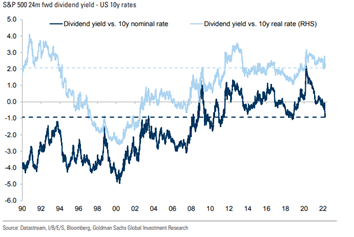

With an extremely mediocre nominal return, the real return on bonds remains in clear negative territory.

Trying not to be too self-confident here, but over time, equities provide better inflation protection than bonds as there is a growth element in equities. The most important thing; however, is to choose the right stocks. The direct return on stocks in S&P500 remains positive compared with the real interest rate.

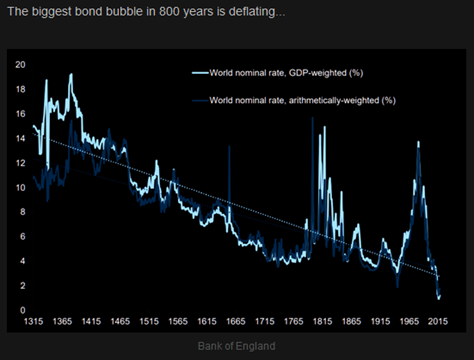

It is important to have the right perspective. The Bank of England demonstrates some skill in technical analysis below with a track record of 700 years.

Source: Bloomberg, Bank of England

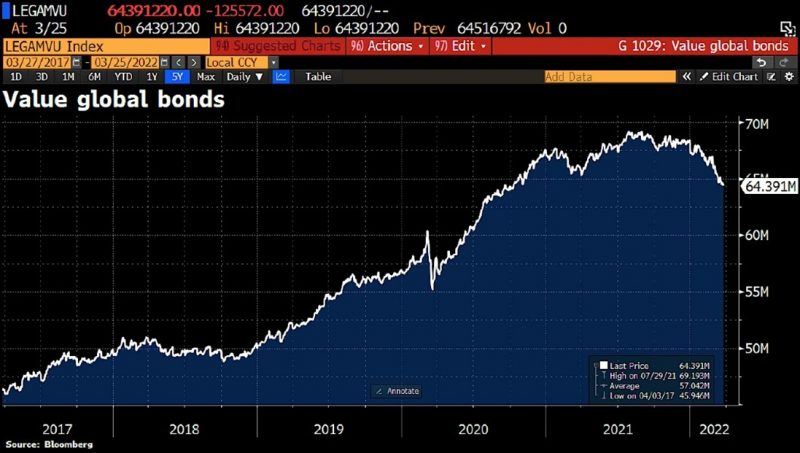

The bond bubble continues to burst after inflation has taken hold in the world's economies. In the last week of March, the value of world bonds fell another $745 billion in value and has now lost a total of $48 trillion since its peak a few months ago. It is about -10% and translated into stock terms, it roughly corresponds to Apple and Microsoft's market capitalization combined.

Even Germany's three-year interest rate turned positive in March for the first time since 2014.

This in turn was due to Germany's inflation being 7.3% year-on-year in March. The last time this happened was in 1981, but then the Bundesbank's policy rate was 11.4%, compared with today's zero per cent.

Source: Bloomberg, Holger Zschaepitz

It’s never easy. The picture below illustrates both the US 10-year interest rate (white) and the bank index in relation to the S&P500 (green). Banks are typically a big winner when interest rates rise as it signals both increased economic activity and that it will be easier for banks to increase their margins. In recent weeks, there has been a clear decoupling and it is probably due to investors becoming increasingly concerned about stagflation and/or a recession. In addition, it could also be interpreted as meaning that the risk of recession is now so imminent that it is believed that the Fed will soon begin to back away from its aggressive rhetoric. The answer is probably somewhere in between.

Source: Bloomberg, Goldman Sachs

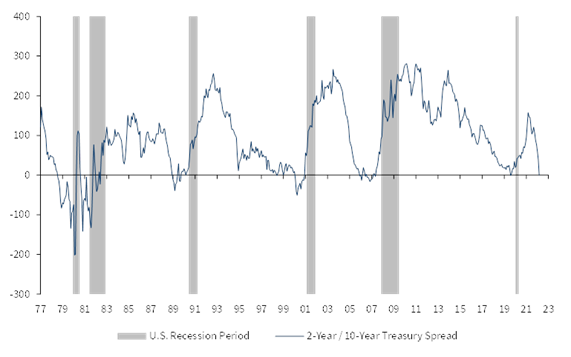

Below is one of the month's hot topics. The difference between the US 2-year interest rate and the 10-year interest rate is now non-existent, which is seen as a clear historical indicator that we have a recession to expect within 12 months. That may be so, but we note that the US economy is under too much pressure and that most historical connections have been completely obliterated by the unprecedented economic policies of politicians and central banks over the past two years. An open mind is to be recommended.

Source: Kepler Cheuvreux

A year ago, the US 2-year interest rate was 0.15% compared with today's approximate 2.4%. A year ago, the expectations were that the Fed would keep the interest rate unchanged until the end of 2023. Today, the expectations are instead that there will be 7-8 interest rate increases in 2022 and that the policy rate is 2.75% at the end of 2023. The point is that a lot has happened in a short period of time. The Fed and other central banks have been seriously wrong in their assumptions and that we are now only at the beginning of a longer period of interest rate hikes.

The picture below does not show a red-hot speculative stock but the US mortgage rate. It is three times higher than the Swedish housing interest rate and consumers are not happy. President Joe Biden is under heavy pressure, but the picture also illustrates how incredibly strong the US economy is at present.

Source: Bloomberg

Source: Twitter

European gas prices are 10-12 times higher than the corresponding price in the USA. A bit like the difference between the price of electricity in southern and northern Sweden. It can also be expressed as the difference between being a self-sufficient realist and being naive. It filters through all layers and levels, interweaving, and is one of many reasons why Europe has had, and probably will continue to have, permanent long-term lower growth and a permanently higher risk premium than the United States. This in turn attracts less capital, which dampens economic growth.

Another way of describing it is the development of Europe's engine, Germany, on a relative basis over the last 20 years. From a European and economic perspective, it is nothing more than an economic meltdown. Only two German companies are among the 100 largest companies in the world in terms of market capitalization: Linde and SAP. Our politicians are either unaware of what has happened, or they are fully occupied with handing out money to us ordinary citizens so we can afford to pay for their mistakes and so they can continue to keep their well-paid jobs. The Swedish design of fuel compensation and for "Putin prices" on electricity is so pathetically mediocre that one almost does not think it is true.

Source: Bloomberg, Goldman Sachs

And as if it were not enough with increased costs, the Social Democrats now also want to introduce a "Contingency Tax". It may be naive of us ordinary citizens, but we thought that a full defence was already included in the current social contract as we have one of the world's highest tax pressures.

Source: Stelbenta Sture

Prime Minister Boris Johnson survived politically once again after the Partygate scandal. He succeeded in comparing the driving forces behind Brexit (liberation, etc.) with the struggle of the people in Ukraine in an extremely disgusting way. See the statement here.

It is a new low watermark of a, seemingly, increasingly internationally isolated politician. Watch the video from the latest NATO meeting here.

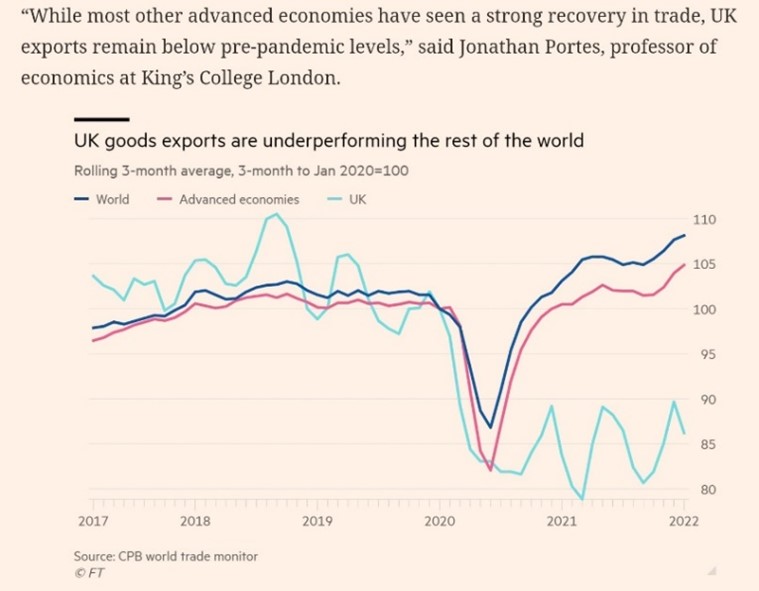

What did we say? Which country wants to leave the EU after studying the picture below? Boris and his friends who continue to dream of times gone by - The Empire where the sun never sets. It feels as if the fuel has run out and that Britain will now, year after year, see a reduction in its economic and political power. Well done boys!

Source: CPB world trade monitor, FT

Long positions

SLP

Despite war, rising interest rates and general fears, Swedish Logistic Property (SLP) was the first stock exchange listing this year and it made a brilliant entry on the Stockholm Stock Exchange. The share rose by as much as 52% on the first trading day and made a 1.1% contribution to the fund's development in March.

The interest in the company was enormous and in fierce competition from Swedish and international investors we managed to become anchor investors. The offer amounted to SEK 750 million and was oversubscribed several times. We got in touch with the company last autumn and have met the management a few times since then. We saw this as a very good opportunity to join some of Sweden's leading real estate entrepreneurs. This is the third time we are anchor investors, where the first were K-fastigheter and Truecaller.

SLP is a real estate company based in Malmö. The business concept is to acquire, refine and manage properties within the logistics space. The company was founded in late autumn 2018 by Peter Strand, Mikael Hofmann, Greg Dingizian and Erik Selin. Since then, more property resources have been added, such as Sofia Ljungdahl, Unni Sollbe and Jacob Karlsson (K-fastigheter). It is difficult not to get excited when large parts of the real estate elite are gathered in one company and own all the shares together with the employees. Value creation tends to increase the greater the financial incentive you have.

The focus is on growth. The property value has gone from zero in 2018 to SEK 6.5 billion at the end of 2021. The overall goal is to achieve an average annual growth in net asset value of at least 15%. We believe that the company will surpass that. The management team was, after all, very much a contributing factor to Victoria Park's impressive development, which ended with German Vonovia placing a bid for the company.

The management combines previous strategies from Tribona and Victoria Park and acquires undervalued logistics properties (often off-market) with a rental potential. Value growth comes from efficient property management, property improvements and financing. The projects are labour-intensive and require solid craftsmanship, which means that SLP typically faces less competition. As such, SLP has the potential to acquire a more attractive yield and thereby create great value for shareholders.

Another reason why we want to own SLP is the logistics properties segment, which has a large structural tailwind. The acceleration in e-commerce is an important driving force and the modernization of supply chains is another. Although COVID-19 accelerated e-commerce growth (33% in 2020), it should be remembered that the trend was stable even before the pandemic (22% growth in 2019) and is expected to continue for many years to come (about 15% per year until 2025, SHB estimates). E-commerce has created a paradigm shift in the supply chain. Successful resellers try to drastically reduce delivery times to be able to compete for customers. At the same time, automation and "just-in-case" processes have taken over the previous "just-in-time" delivery that relies on costly and increasingly unreliable global supply chains.

SLP was listed at a valuation of just over SEK 4.9 billion (post-money). In relation to the most recently reported net asset value, this meant a premium of approximately 30%. We saw this as attractive as the premium was in the lower range in comparison with European real estate companies with a logistics focus. At the same time, we believe that SLP has better conditions for growing net asset value faster than many competitors. Our analysis indicates that the net asset value has good opportunities to grow into the valuation within 1-2 years, which we consider to be an attractive calculation.

In summary, we believe that SLP has the potential to become one of Sweden's leading real estate companies in logistics. The board and management team are some of the absolute foremost in Swedish real estate and have created significant value over time. In addition, everyone involved has significant ownership interests, which makes us believe this is just the beginning of a long journey. Logistics properties have interesting prospects in both the short and long term, but it is above all SLP's management team and business model that attracted us.

Victoria

The share price in Victoria has been extremely volatile during the year. From the beginning of the year to the bottom in March, the share had fallen by as much as -46% (!) even though no material news was released. As the holding in Victoria is one of the fund's largest positions, this has had a major negative contribution to the fund's development in 2022.

During the month, the company, positively, decided to begin a share repurchase program, which resulted in the share price recovering part of the loss for the year. We increased our position during the entire decline and at most at a price of 650 (the lowest level). The share price increased by 25% during March bringing the YTD performance to -25%.

Source: Bloomberg

Photocure

The Photocure share has worked well during the year. As we mentioned in our previous monthly letter, the report for the fourth quarter gave more insights - maybe this is what the market has taken note of? Our analysis indicates that the number of cystoscopes deployed in the US (an indicator of future sales) during the first quarter of 2022 was clearly better than we previously estimated. We look forward to the rest of the year which is one of the more exciting so far for Photocure. The share rose 18% in March and has risen 15% during the year.

London Stock Exchange

Since the beginning of the year, we have a position in the London Stock Exchange. The company had a turbulent 2021 when the stock market lost confidence in management after the company announced higher integration costs than expected of a major acquisition. Since then, operational development has been good, recurring revenues have more than doubled and valuations have nevertheless been lower than the historical average. The share has risen about 14% since we bought our first shares, which is 21% points better than the European index.

Sampo

With the turbulence that occurred during the first quarter of this year, we have been looking for companies/shares that are slightly larger than what we typically invest in to balance the portfolio. We have also historically owned Sampo on the theme of a well-run and attractively valued financial company. The company has cleaned up its assets and soon the management has sold off its entire Nordea holding. Above all, Sampo's insurance business, which has something of an oligopoly position in the Nordic region (which is probably the world's best insurance market), remains. This is a defensive holding where a large part of the return is likely to come from dividends and share repurchases. The stock rose 5% in March.

Short positions

The short portfolio contributed with a negative result during the month. Despite some profit-taking, the worst profit contribution was our put options in the German DAX, which fell in value when volatility decreased. Index positions in the American Nasdaq and Swedish small company indices also had a negative impact. Some stock-specific short positions that contributed positively to the result were Swedish Sectra, BHG Group and Danish Carlsberg.

Exposure

The net exposure, adjusted for our unlisted holdings, at the beginning and end of the month was 60 and 62%, respectively.

Summary

The month of March was clearly divided between great distress in the first half and "risk-on" in the second half. Many were naturally burdened and shocked in the first weeks of Russia's attack on Ukraine, but as always humans adapt, and the market was less and less affected by various war headlines on the screens. Regarding human suffering in Ukraine, it has become clearer with each passing day that Russia is undoubtedly committing war crimes with the indefensible executions of civilians. Their day will come when they are brought to justice.

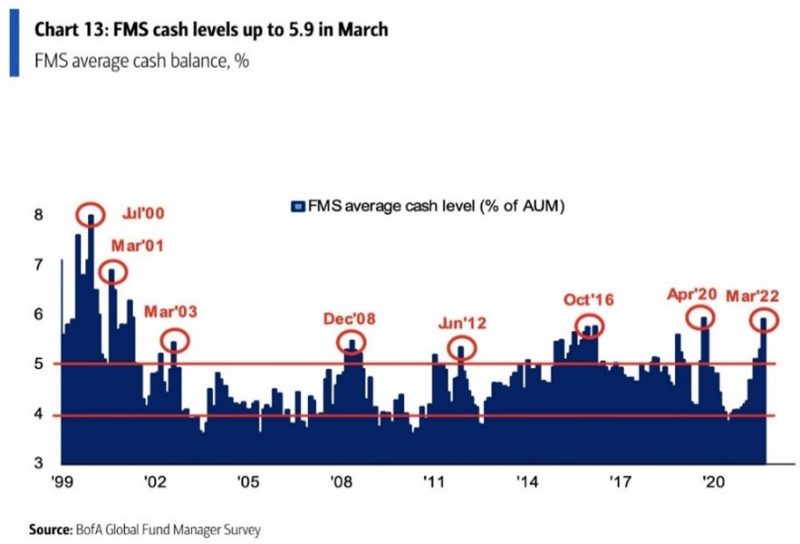

Another reason that led to the turnaround in the market was the US Federal Reserve meeting on March 15, which was eagerly anticipated for several months. The Fed raised the key interest rate by 25 basis points, which was the first increase since December 2018. Few investors wanted to increase their risk before they knew how much the interest rate would be raised and what would be communicated. The cash levels of the world's institutional investors were at the time record high, which is always a good contraindicator.

Source: BofA Global Fund Manager Survey

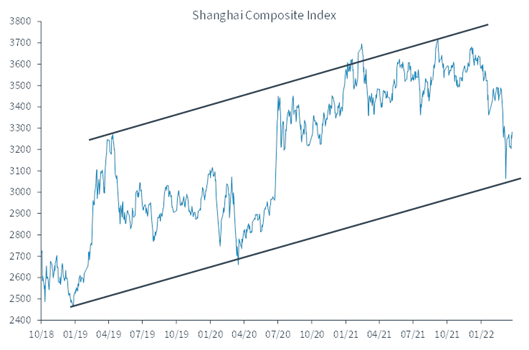

The third reason why the market turned in the middle of the month was the Chinese central bank, which on March 16 communicated several market-friendly policies and thus effectively stopped the market crash that occurred on the Shanghai Stock Exchange during the first 10 days of the month, see picture below.

Source: Kepler Cheuvreux

The fact that the major technology companies in the United States coped with the worst of the pressure and withstood important technical levels contributed to investors increasing their allocations into equities again. See below MSCI Growth compared to MSCI Value.

Source: Goldman Sachs

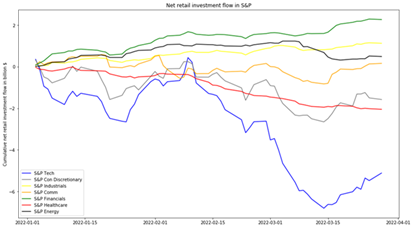

Although the US consumer is gloomy at the moment, private individuals have started buying technology shares again. Technology stocks in blue.

Source: Goldman Sachs

The picture below was in our previous monthly newsletter as well. Then we were in an extreme situation, which usually indicates good buying opportunities. This was also the case this time and the rise in the broad European index from the lowest levels during the month was just over 12% until the end of March.

The fund was also under pressure at the beginning of the month with continued extreme price movements in some of our large core holdings. We remained calm and even went against the most extreme price movements. It is gratifying to note that the stock that fell the most, Victoria, was also the stock we bought most aggressively in. In six days, the price rose by almost 40% and Victoria was in the end the fund's best contributor in March with as much as 1.7%.

Price movements as the one above in Victoria often occurs when some investors face liquidity problems and become forced sellers. Given the outbreak of war, the entire European stock market received enormous outflows, see picture below, which led to sell-offs. During the first three months of the year, we ourselves have been in the fortunate situation that we have had continuous inflows into the fund. Something we are obviously extremely grateful and humbled for. Thanks!

Source: Goldman Sachs

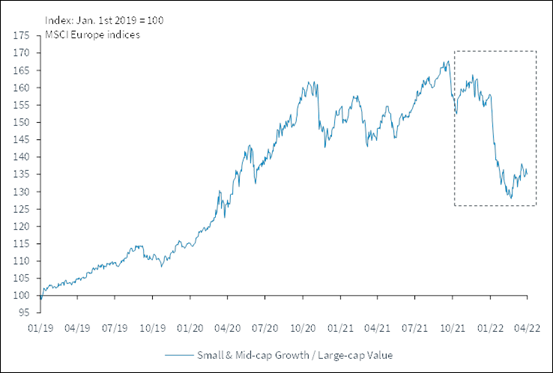

We wrote in last month's letter that the favourable conditions have begun to emerge for smaller growth companies (Europe's equivalent to typical Nasdaq companies) to break a long-term negative price trend. It happened in March (at least temporarily), and it was also very clear that growth companies began to recover lost ground towards more classic value companies, despite the fact that interest rates rose.

Source: Kepler Cheuvreux

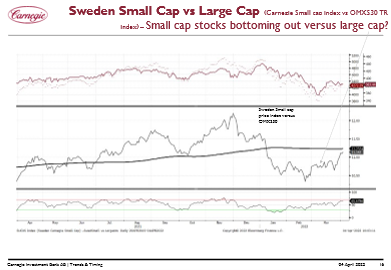

Below is a corresponding picture for the Swedish market. Smaller company price development in relation to OMXS30 - a similar pattern as in Europe.

Source: Carnegie

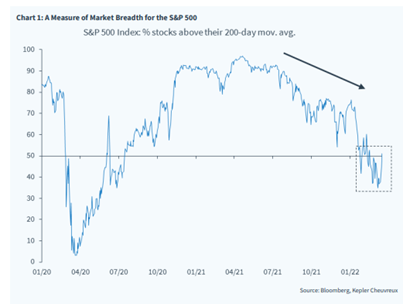

When the stock market turned around in the middle of the month, the fund's value rose in line with the market, despite a net exposure of 50-60%. It is many months since we last had a long period of strong days and the biggest reason for that (we think) is the increased breadth of the market that suddenly arose. The fund has a small part of the investments in what we call "market shares". The trend with a declining breadth has been going on since last summer, which we have felt, but in March the proportion of shares traded above its rising 200-day moving average suddenly rose and the fund began to develop strongly. Typically, a rising breadth in the market is an important factor for a more lasting upturn.

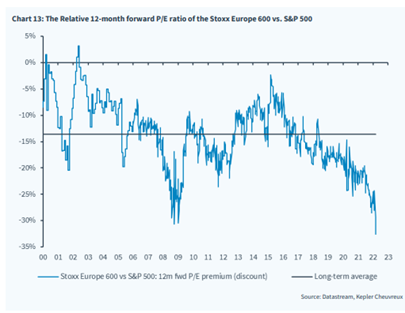

The large withdrawals from the European stock markets that were shown earlier, have also pushed down valuations in Europe to rarely seen levels. Compared with the US stock markets, these are the lowest levels in over 20 years, see picture below.

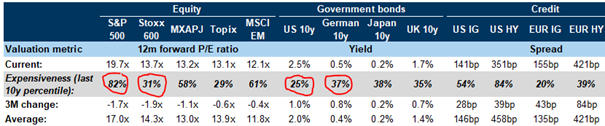

It becomes even clearer if you study the data below from Goldman Sachs. Based on the last 10 years, the S&P500 is now traded (based on the P/E ratio 12 months ahead) in the 82% percentile, i.e. in 82% of the observations, the P/E ratio has been lower. For Europe, the corresponding figure is only 31%. There is a huge difference, and our view is that it is largely due to the tragic development in Ukraine. There should be a certain "cushion" in the low values in Europe.

Source: Goldman Sachs

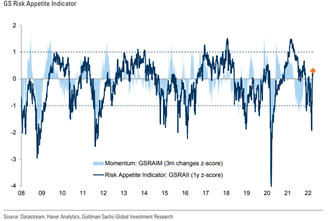

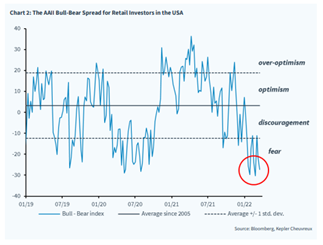

Given the values in the United States, it is perhaps somewhat surprising that the American private investor is still feeling miserable. It would have been interesting to see what the corresponding picture looked like for an average European private investor. The Bull-Bear Spread below is at least positive from a sentiment perspective, it cannot get much worse and is thus a good contraindicator.

We are now rolling into this year's first reporting season, and it is likely to be one of the more interesting seasons in many years. The profit warnings will probably be heard in companies with limited opportunities to raise their prices. Various bottleneck problems that arose during the pandemic and are now continuing with the war in Ukraine will probably hit hard in some places. Those who manage to maintain or increase their gross margins and have a growth in sales are likely to be rewarded properly and for the remainder of the year. We have worked hard to go through company after company and we hope our strong trend from the previous reporting period continues.

Profit estimates have begun to fall in recent weeks because of accelerating inflation and the war in Ukraine. We have seen the largest downgrades from analysts among consumer companies (such as H&M), but also cyclical companies such as in the chemical industry (oil prices hit hard). Two sectors that continue to see sharply rising profit estimates are oil companies and mining companies.

In summary, expectations have begun to fall in recent weeks and sentiment remains weak among investors. We believe that we are in a classic "pain trade" market, which provides support on the upside. At the same time, real interest rates remain strongly negative. We believe that the market reached its bottom on March 15 and now have help from both China (policy) and the USA (the big tech companies have rebounded).

Volatility in the market has fallen and the proportion of aggressive sellers is now significantly lower than a few weeks ago. For those of you who like statistics, we note that just over 90% of the shares in the S&P500 were above their 10-day moving average at the end of March. With those conditions and since 1982, the index has been higher 35 of 36 times a year later.

We continue to maintain a more balanced portfolio as we will probably trade around these levels for a few months to come. During the broad indices, on the other hand, there will be large movements. This is where we are most active, and we continue our work to create an excess return for ourselves and you this year as well.

An unusually big thank you for your patience during the first quarter and we are now pressing ahead for the next quarter.

Mikael & Team

Malmö, 6th of April 2022