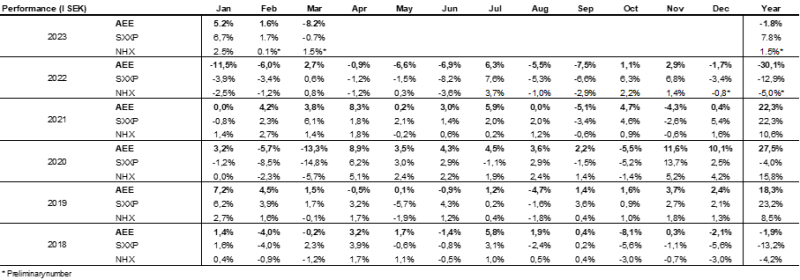

Note that the information below describes the share class (I SEK), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class' return. The information below regarding returns therefore differs from the returns in other share classes.

Before making any final investment decisions, please read the prospectus, its Annual Report, and the KID of the relevant Sub-Fund here

This material is marketing communication

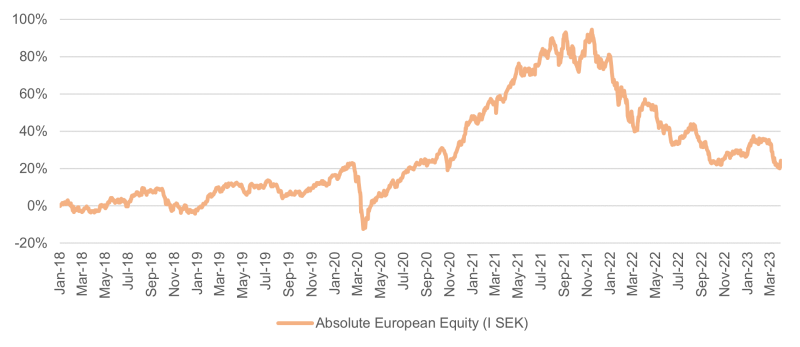

Monthly Newsletter Coeli Absolute European Equity – March 2023

FEBRUARY PERFORMANCE

The fund’s value decreased by 8.2% in March (share class I SEK). The Stoxx600 (broad European index) decreased during the same period by 0.7% and HedgeNordic’s NHX Equities decreased provisionally by 1.5%. The corresponding figures for 2023 are a decrease of 1.8% for the fund, +7.8% for the Stoxx600 and +1.5% for NHX Equities.

EQUITY MARKETS / MACRO ENVIRONMENT

March was an exceptionally turbulent month triggered by a (temporary?) banking crisis which, for the vast majority, came with great surprise and force. This led to large movements in the stock market and very large movements in the interest rate market. The European stock market, which since the bottom in October last year had a significantly stronger development than the American one, suddenly performed significantly worse than the American one. The main reason for that was a remarkable return of the big US technology companies while European bank shares, which are heavily weighted in European indices, fell sharply. During the end of the month, the markets calmed down gradually and day by day.

If the broad European indices performed weakly, it was even weaker "under the hood", i.e., among the smaller and medium-sized companies. When there is sudden severe turbulence, the buyers of the smaller shares often disappear. In a company like LVMH, for example, there is always a buy side, but in a company like SLP, for example, a vacuum arises and what we consider to be a temporary air pocket when the share falls as much as 21% from its peak at the beginning of the month. In this case, most likely, real estate funds were affected by outflows, but when they had finished selling and generalists bought up shares the recoil came in many names. About half of the decline was recovered in the last days of the month and as of writing the entire loss for the month has been recouped.

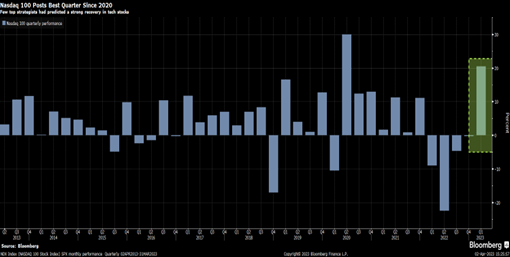

The fund's holdings were strongly affected by the above factors and had a weak performance resulting in a loss of 8,2%, which means a negative result of 1,8% for the first quarter. Some stock specific events had a significant impact on the result. We are of course disappointed by this, and we elaborate further in this letter. The MSCI European Small & Midcap index fell by 4.4% in March, while the Stoxx600 fell by 0.7%. S&P500 rose by 3.5% and Nasdaq by as much as 9.4%! Measured in euros, however, the yield was lower by 1.0 and 6.8% respectively.

The Nasdaq rose during the first quarter by 16.8%, which is the fourth strongest quarter in the last 20 years! March showed the tenth strongest development in the last 10 years. The large Mega cap technology stocks rose as a group as much as 31%, while the rest of the S&P rose by 2%. It is an extremely unusual development in such a short time. In this context, the large technology companies were seen almost as a risk-free asset with very high liquidity and strong balance sheets.

Source: Bloomberg

How was it possible that suddenly and in just one week three American banks collapsed and the week after the long-established Swiss bank, Credit Suisse? Many of us have now learned that in addition to increased earnings for the banks when interest rates rise, major problems can also arise if you have not hedged or balanced your bond portfolio in line with your commitments to customers.

On March 8, it was announced that Silicon Valley Bank had problems as their bond portfolio declined sharply in value as interest rates rose. The bank tried to raise USD 2 billion in capital from investors but without success. Very large outflows from the bank's customers in just a few hours forced it into bankruptcy on Friday, March 10. On Sunday evening, a joint press release was sent out by the US central bank, the Treasury Department, and the agency responsible for the deposit guarantee, that US authorities took over the bank and guaranteed that all customers' deposits were safe. During the same short period of time, Silvergate Capital and Signature Bank also experienced major problems with the same dramatic consequences as a result.

These banks were nothing compared to Credit Suisse, which in a few days after had major problems. Credit Suisse's CHF530 billion balance sheet was double that of Lehmann's when they crashed in 2008. The Swiss National Bank quickly provided CHF53 billion in liquidity. It lasted a few days, but after closing on Friday, March 17, tough negotiations began, which ended with UBS buying Credit Suisse in a “shotgun marriage” on Sunday evening for a low three billion CHF. The market capitalization on Friday was CHF 8 billion, so shareholders took a real hit on Monday.

Even worse off were the bondholders of Credit Suisse who had CHF 17 billion in so-called AT1s and who, after the bailout, had their holdings written down to zero amid great uproar. EU authorities were quick to distance themselves from the Swiss decision to let shareholders come before bondholders in the event a bank is bailed out by authorities. The last word has not been said and it is highly likely that soon lawsuits will follow suit. Striking in this context is that during the 2008 financial crisis, no bondholders to the banks lost any of their capital. Also interesting is that Credit Suisse had a market capitalization in 2007 that was bigger than Apple's.

The drama will in the future affect banks' cost of capital, which in turn means lower loan volumes and thus a negative contribution to economic growth. The banking crisis was in practice an additional increase in interest rates by the central banks. Goldman Sachs estimates that the banking crisis will negatively affect the US economy by 0.25-0.50% in 2023.

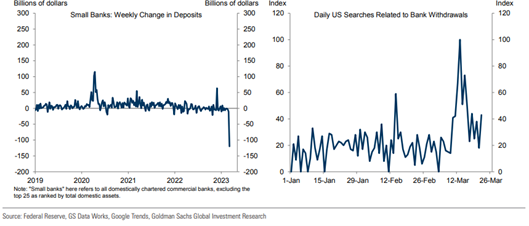

The development quickly led to a crisis of confidence in the banking system and very large withdrawals were made from primarily the smaller American banks, see picture below.

The development prompted the US central bank to pump liquidity into the market to secure the banking system, which in turn caused the FED's balance sheet to quickly increase again after a year of decline with all the consequences that that entailed.

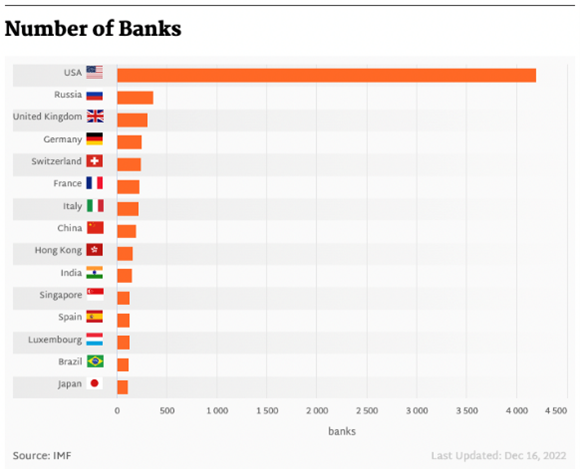

The concentration of banks in the USA is significantly lower than in most other countries, see picture below. As in a mantra from various leading business leaders and politicians, we have been told in recent weeks that the European banks are well capitalized and have high and healthy liquidity and do not have the same problems as smaller regional banks in the USA. We'd like to believe that's true, but the only thing you can be certain of is that you don't know everything for sure.

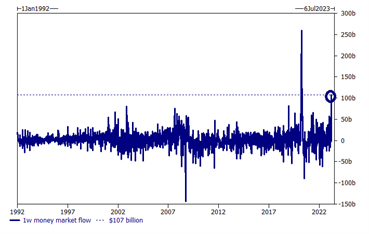

The chart below shows that since the Fed began its tightening a year ago, deposits in money market funds have risen sharply while deposits at banks have fallen sharply.

Deposits in money market funds exploded and only during the Covid crash have we experienced greater inflows, see image below.

Source: Goldman Sachs

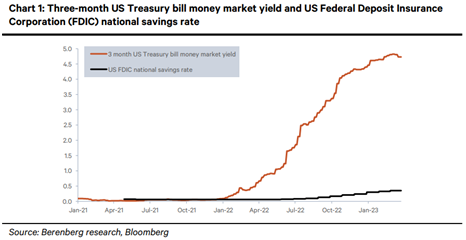

The flight of capital from the banking system will force the banks to raise the deposit rate for their customers and thus their earnings growth will decrease somewhat. The figure below shows the 3-month bond rate relative to the FDIC's national deposit rate.

In the aftermath of Credit Suisse, the Deutsche Bank stock also came under intense pressure for no apparent reason. The CDSs (Credit Default Swap) rose sharply, which made the stock market nervous, see picture below. German Chancellor Olaf Schulz came out and defended the bank by saying that they are profitable and that the outlook of the bank is robust and stable.

Source: Bloomberg

It can be concluded that the volumes in the CDS market are relatively modest and it does not take that much capital to significantly move the CDS levels. It could be that there were actors who, with relatively small capital, traded up the CDS level and at the same time went short the stock for significantly larger amounts.

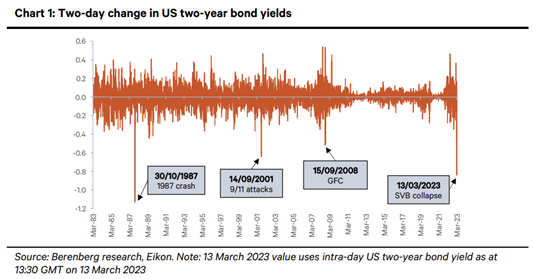

If you must pick one event during the month that stands out a little extra it has to be the movement in one of the world's safest asset classes, the US two-year Treasury bond. In eight trading days starting March 8, the rate fell 130 basis points from just over 5% to about 3.8%. It was in practice the world's safest asset class that brought down a few banks in the United States.

Source: Bloomberg

Such a sharp movement in government bond yields did not even occur during the financial crisis of 2008. The image below summarizes the magnitudes well.

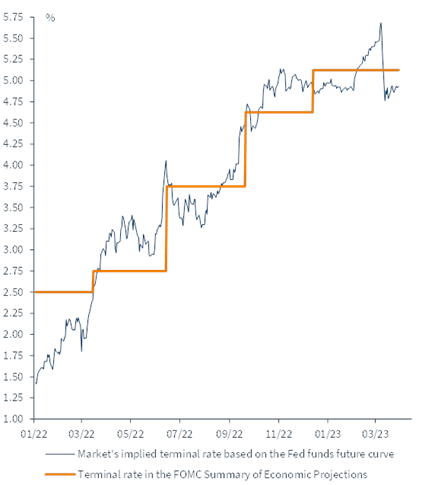

In one day, the market's expectations about the final terminal rate for the various central banks also came down. The image below shows that the market's expectations for the US central bank's interest rate peak fell from close to 5.75% to around 4.75%. The corresponding expectation for the ECB went from just over 4% to just over 3.5%.

Source: Kepler Cheuvreux

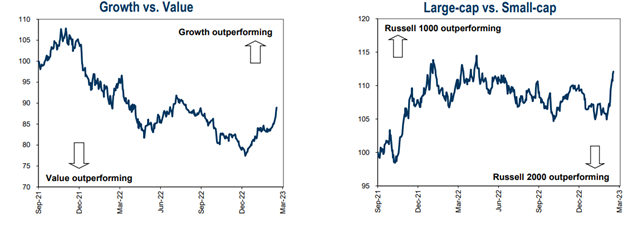

The segments in the stock market that were most affected during March were simply put the large technology companies, which rose sharply at the same time as banks and real estate companies performed poorly. Another clear difference was that small companies had a weaker development than the large companies. Note the drastic change on the far right in the images below.

Source: Goldman Sachs

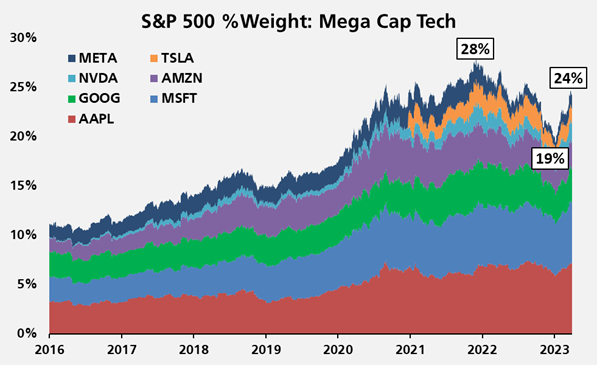

Seven of the eight largest companies in the S&P500 are the major technology companies (Berkshire Hathaway is the eighth). Since the turn of the year, their weight in the index has risen from 19 to 24%.

Source: Goldman Sachs

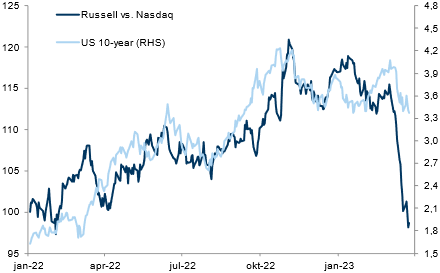

Since the beginning of last year, Nasdaq has now fully recovered its underperformance that began in early 2022. Note the difference in just the last twenty trading days.

Source: Kepler Cheuvreux

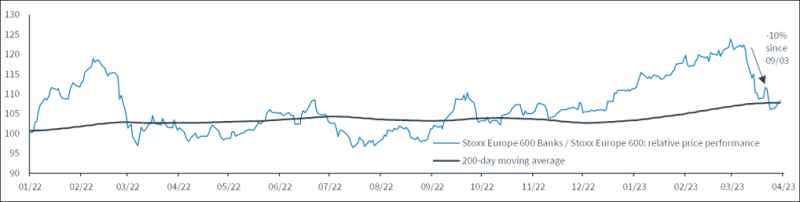

The opposite applies to European banks; during the last six months they have had the best conditions for several decades in terms of profitability, which meant that investors generally had greater exposure to the sector than they have had in a very long time. At the end of the month, the volatility of European bank shares also fell.

Source: Kepler Cheuvreux

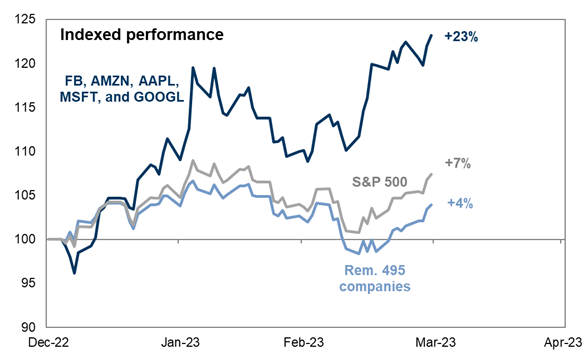

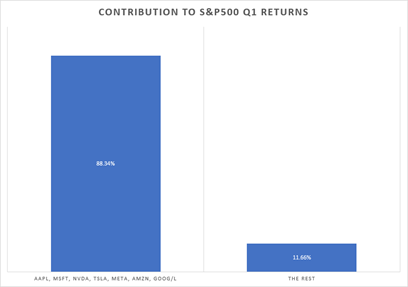

The excellent picture below shows how high the concentration was during the first quarter. 495 out of 500 companies in the S&P500 this year have a return of 4% compared to 23% for the large technology companies.

Source: Goldman Sachs

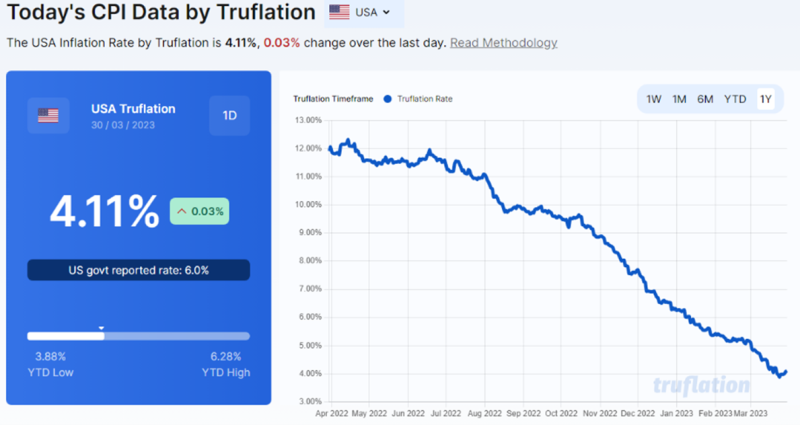

Inflation continues to fall. Core inflation in many countries remains high and it will take time to push it down but given how quickly some commodities and costs have fallen, it is likely only a matter of time. Truflation.com (independent source) provides ongoing estimates of the current US inflation rate. With more than 10 million data points, they claim to be 30 times faster than traditional inflation estimation. The image below includes the latest reading as of March 31 and 12 months back. The trend is clear and positive.

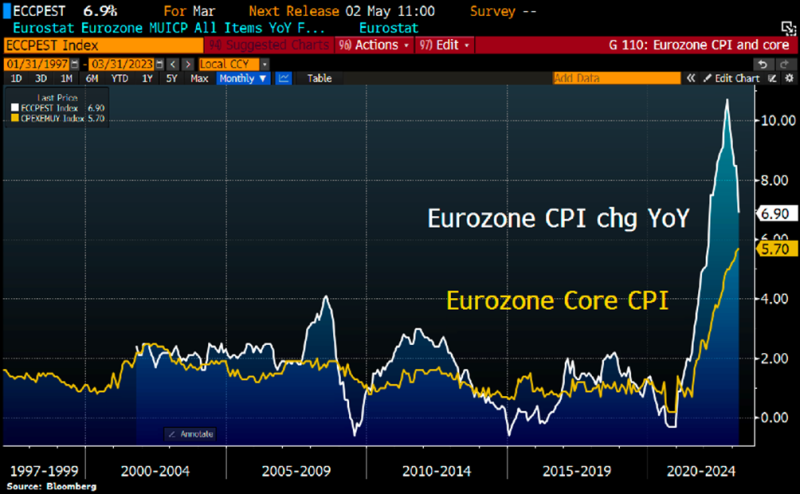

Below is the euro zone's broad inflation and core inflation. Amid the tumult during the month, the ECB raised its key interest rate by 50 basis points. Given their lackluster track record no other action was expected. The likelihood of them overshooting the target again is high (our assessment).

Source: Bloomberg, Holger Zschaepitz

Spanish inflation has in a short time halved and on March 30 published a low 3.3% against the expected 3.9% and 6.0% the previous month. Things are moving fast now that the comparable numbers are improving. The biggest problem is food prices, but we are likely to see a decline here as well, presumably after the summer. Unfortunately, Sweden currently has the highest inflation in Western Europe and a record weak Swedish krona does not help. Sooner or later, reality always catches up and it is now visible with all undesirable clarity in the Swedish economy. But even if Sweden is among the laggards in Europe, we too will soon see improvements.

Consumers in Europe do not suffer as much as in Sweden. The percentage of people with variable loan rates is significantly lower, the amount of debt is lower, the electricity subsidies are higher, and they don’t have a dysfunctional exchange rate, to name a few. German consumers are starting to wake up and similar tones are also being heard from the UK.

Source: Bloomberg

Source: Twitter

Long positions

4Imprint

During the month, 4imprint released its 2022 full-year report, which was in line or slightly better than communicated in a January press release. Thus far sales are described as encouraging.

4imprint has been one of the fund's big winners over the past year. In one year, the share has risen around 72% and in March the share rose 8%. Despite a strong price trend, we believe that there is still upside from current levels if the company manages to maintain or improve the profitability it achieved in 2023. We believe conditions for that are good and we therefore keep the company in the portfolio.

Wincanton

March's big loser for the fund was the holding in the British logistics company, Wincanton. During the month, the company released an update for the fiscal year ending in March 2023, which was in line with market expectations. At the same time, however, they warned that next year will be more challenging. All in all, profit is currently expected to decrease by around 20% and there are two underlying factors for this. First, a general economic downturn that leads to lower volumes, and second, that the company has unexpectedly lost a major profitable contract.

That the macroeconomic situation would affect Wincanton should hardly come as a shock to anyone, but the loss of the important contract came as a surprise. As Wincanton's business is largely contract driven, individual contract losses are a natural part of the business. In this case, however, it was an unusually profitable contract, which means that the loss of it has a disproportionately large effect overall.

After a price decline of 31% in March, the stock is now trading at a profit multiple on the result after tax of approximately 7x and 6x for 2024 and 2025 respectively. With that said, the company already has a small net cash at the end of last year. It is incredibly low for a company that has implemented major structural changes which have improved business in recent years. The stock has been penalized for what we see as temporary problems, and therefore we have taken advantage of the price decline to increase our position. We believe that Wincanton will emerge from the economic downturn stronger and better than its competitors. The question is of course how long and deep it will be.

As one of the few national UK logistics companies, Wincanton is likely to have industrial value for other, larger players. Not too long ago, competitor Clipper Logistics was bought at a decent premium to Wincanton's current valuation. If the company's valuation remains at today's levels, we do not consider it too unlikely that Wincanton could be the subject of bids.

Lindab

The Lindab share made a nice contribution to the month's results after the share rose 9% in March. We have not seen any extraordinary news to explain the rise. However, we note that CEO, Ola Ringdahl, has been clear that they want to reach a 10% operating margin again in 2023, to be compared with the analysts' estimate of around 9 - 9.5%. If we assume that the sales forecasts remain and that Lindab reaches the operating margin of 10%, then the analysts' estimates for the full year should be beaten by upwards of 15%.

ISS

Another share that weighed on the fund's results in March was ISS, which fell by 9%. The reason for that was that the company's esteemed CEO, Jacob Aarup-Andersen, resigned in favor of the CEO job at Carlsberg. It is hardly strange that he chooses one of the finest CEO jobs you can take as a Dane. Aarup-Andersen has been highly appreciated by the stock market; partly because he carried out a successful turnaround of the business (which is still progressing) and partly because he has been very good at communicating with the market.

The stock fell 7% on the announcement of Aarup-Andersen's departure but recovered in the following days when several insiders bought shares. As a nice gesture, Aarup-Andersen bought shares, but also the company's CFO Kaspar Fangel.

We do not believe that ISS stands and falls with the company's CEO and the management team that remains have all bought in to the strategy that Aarup-Andersen helped launch. All in all, we thought it was sad that Aarup-Andersen left, but we understand, and he is now leaving a company in much better shape than when he joined a few years ago. We maintain our relatively large position in ISS, which has now become even more attractively valued as it trades around 11x current year earnings and below 10x 2024e.

Corem

After a strong start to the year, the property sector, including Corem, came under pressure in March. Corem's share fell by as much as 20%, driven by growing concern about the company's ability to refinance issued bonds and probably also concern about the main owner's (M2) financial situation. We are very satisfied with the sales Corem has completed or are about to complete. In total, properties worth close to SEK 7.5 billion have been sold since the end of last year, all basically at book value, which is remarkable given a material discount of 65-70%. In addition, Castellum shares have been sold for a total of 1.0 billion.

On April 3, a letter of intent was signed with a foreign actor who buys 25% of Klövern for 1.35 billion (Corem owns 49%) whose assets are mainly 24,000 attractive residential building rights. In addition, the international investor undertakes to invest up to 3 billion in new issues to operate and finance the construction project portfolio. The company is thus rigged and ready without Corem having to allocate more capital into Klövern. We assume that the banks are satisfied.

The transaction, which intends to be carried out during the second quarter, is an important step in the right direction for Corem, which therefore will likely give it a two-to-three-year head start as it is currently unable to launch major projects itself. Corem's focus for the last six months has been to consolidate the balance sheet. The company will also receive SEK 650 million, which will be very useful, not least for the repurchase of the costly hybrid that the company has outstanding. Since the lowest share price level on March 30, the share has risen by approximately 20%. The company is close to the point where you can buy back all the bonds due this year plus the hybrid. The share is traded based on the closing price in March of just under 10x cash earnings 2024e. We think this is a very low level and as the financial situation improves it should push down the risk premium and thus cause the share price to rise.

LVMH

The LVMH share is the closest Europe can get to the American major technology companies and the share also rose by seven percent during the month. YTD, the share has risen a whopping 24% and thus added 80 billion euros in market capitalization. The current market capitalization is 424 billion euros, which corresponds to half of the Stockholm Stock Exchange. An incomparable company.

Short positions

The short portfolio contributed with a small positive result during the month, which came from our short holding in a Swedish small company index.

Exposure

The net exposure, adjusted for our unlisted holdings, at the beginning and end of the month was 77% and 76% respectively.

Summary

The result in March mainly consisted of three different components:

- European small companies that suddenly found themselves out in the cold and with falling share prices as a result. At the end of the period, a recovery began.

- Two company events that each had a major impact on the result. The first was British Wincanton where we thought the price reaction after the company's update to the market was a strong overreaction which we took advantage of and bought more shares. The stock has risen just over 10% in the past week. The second event was ISS where the CEO left for a new position in the Danish crown jewel Carlsberg. It was the fund's largest holding and the share fell by 9% during the month. Here, too, the stock has risen from its lowest levels, and we note with satisfaction that both the outgoing CEO and some other insiders bought shares after the price drop.

- After a very strong performance run, Commerzbank's stock came under pressure like many other banks, falling 16% in March. We have more than halved our holding in Commerzbank and are awaiting developments. Our two real estate holdings in SLP and Corem were also under pressure, as was the entire real estate sector, when the banking crisis occurred. In both SLP and Corem, we have acquired shares at low levels as we believe that both shares offer good value in different ways. Both SLP and Corem rose in the last days of the month.

Overall, around 65% of the fund's negative monthly results came from Wincanton, Corem, Commerzbank, Accelleron and ISS. Wincanton was by far the biggest negative contributor. Commerzbank and Accelleron have given the fund a positive profit contribution this year, while the others have had a negative contribution.

In last month's newsletter, we spent some time explaining why the European stock market has performed so much better than the American one in recent months. This time we have had to do the opposite, although Europe YTD has risen more than the US. In a simplified way, the development of the last few weeks is explained by the progress of the large technology companies. Only seven companies in the S&P500 account for almost 90% of the index's rise. Apple and Microsoft alone account for 40%. The S&P500 has not been so dependent on two stocks since 1978.

Source: Goldman Sachs

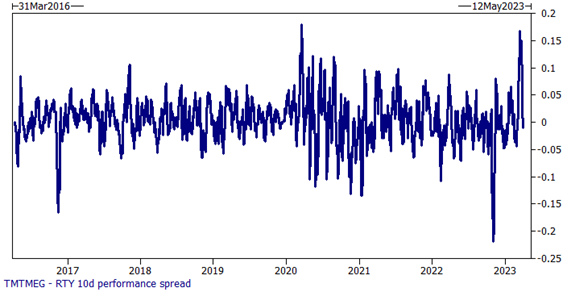

The image below shows a ten-day difference in returns between, on the one hand, technology companies in the US and, on the other hand, a broad index with mostly smaller companies. At its most, a 16% difference (!) was measured in 10 days, which is on par with the Covid crash. At the time of writing, the situation has normalized.

Source: Goldman Sachs

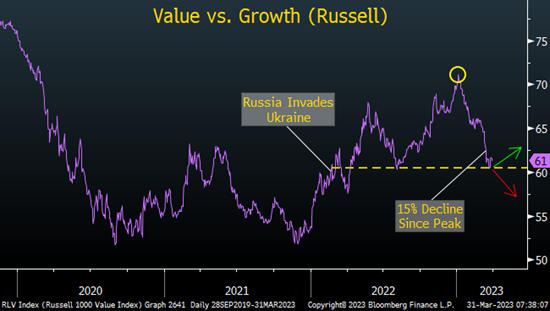

Portrayed differently below, value stocks' large outperformance compared to growth stocks in the second half of last year has been completely neutralized in a short period of time.

Source: Goldman Sachs

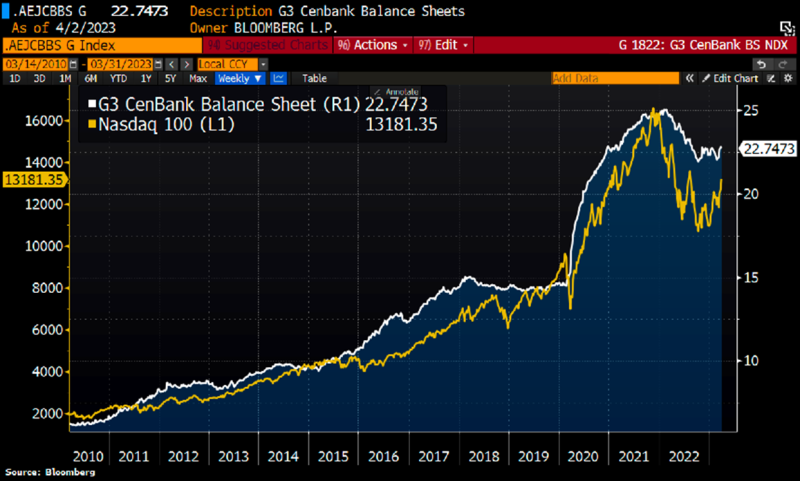

There seems to be a correlation. The image illustrates the development of the largest central banks' balance sheets in relation to Nasdaq's development since 2010.

Source: Bloomberg, Holger Zschaepitz

Below is the volatility index of the last month for the stock market. It is amazing that now, after so much drama, we are back to low levels again so quickly.

Source: Bloomberg

The MOVE index, on the other hand, which shows the volatility of the interest rate market, is at significantly higher levels than on March 9, when the banking crisis started. A stock index simply contains the best and biggest companies, while in the bond world it is the companies that borrow the most (which for all intents and purposes are often excellent companies).

Source: Bloomberg

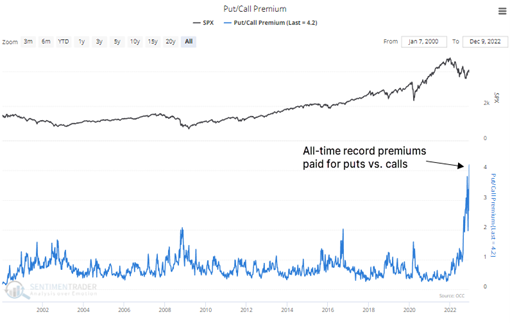

Sentiment among investors remains gloomy, as the images below show well. Never before has the relationship between buying puts and calling options been as extreme as in the past month.

Source: Sentimenttrader

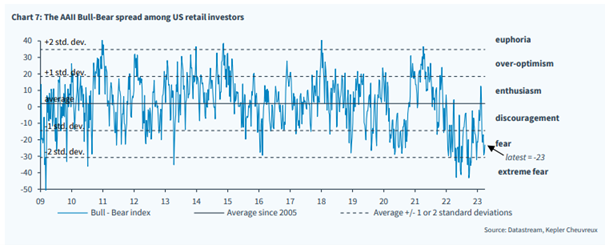

Optimists vs. pessimists reach new low. It usually does not last long at these low levels. Maybe it's different this time?

Source: Kepler Cheuvreux

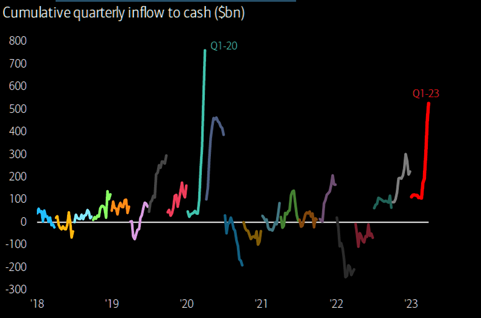

American investors added roughly $500 billion to cash holdings during the first quarter of this year. The last time these levels were reached was in the spring of 2020, which then led to a very strong rise.

Source: Themarketear.com, Bank of America

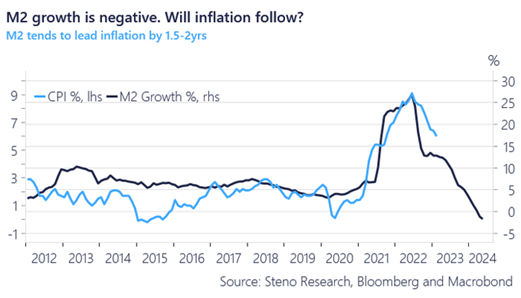

The sharp increase in money supply following the Covid crash led, after a few years, to rising inflation. When the money supply now falls sharply, inflation should follow, and we believe that is what we are now beginning to witness. In a year's time, the central banks may still have major problems, but then because inflation is below the target. Our view is that the central banks are too forceful instead of waiting and seeing how the effects filter through the economy.

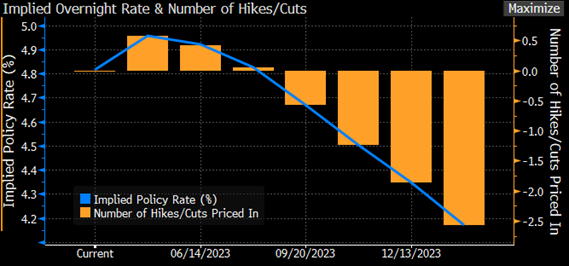

The banking drama led to an immediate change in the market's expectations of future interest rate cuts. Now the market expects the FED to cut interest rates twice before the turn of the year compared to, the day before the banking crisis on March 9, two more increases. Before March 9, the policy rate was expected to be around 5.4% at the end of the year against the current estimate of 4.4%. A very big and immediate change.

Source: Bloomberg, Goldman Sachs

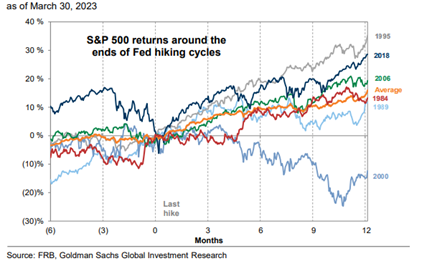

Historically, US stocks have performed strongly in the months following the FED's last rate hike with an average three-month performance of +8% (high +14% and low -1%). In 12 months, the development has been +19% and on none of the occasions has it been lower than +10%.

March offered unexpected and a great deal of drama. At the time of writing, the turbulence in the stock market has almost completely subsided. We'll see how long it lasts, but the authorities and central banks are fully prepared to intervene in case of any new problems. We are now rolling into the next reporting period, which we believe will generally show another period of surprisingly good earnings. Inflation undoubtedly helps on the revenue side.

In our portfolio, we see significant potential in many of our companies, not least those that have taken an undeserved beating in recent weeks. Corem is a good example where we bought more shares all the way down, and which in just over two trading days, rose close to approximately 20%. You might think that's crazy, but in several other cases it was also crazy on the way down.

If you look a little further into the future, rising interest rates and banking worries will lead to a slowdown in demand for new credit. Sweden is an excellent example of this, where we now have negative loan growth. This will lead to lower growth in the future, and it will be even more important to invest in companies that have something unique and preferably in combination with pricing power.

Inflation is likely to continue to fall and central banks will soon switch gears and start cutting rates. The problems with high indebtedness will gradually diminish as interest rates in a few quarters (our view) begin to fall.

We wish all readers and investors a Happy Easter!

Mikael & Team

Malmö on April 6th, 2023