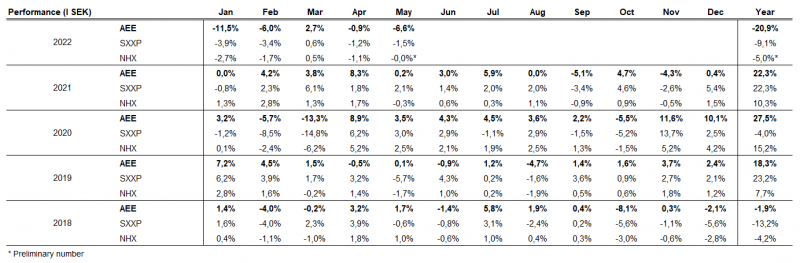

Note that the information below describes the share class (I SEK), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class' return. The information below regarding returns therefore differs from the returns in other share classes.

Before making any final investment decisions, please read the prospectus, its Annual Report, and the KIID of the relevant Sub-Fund here

This material is marketing communication

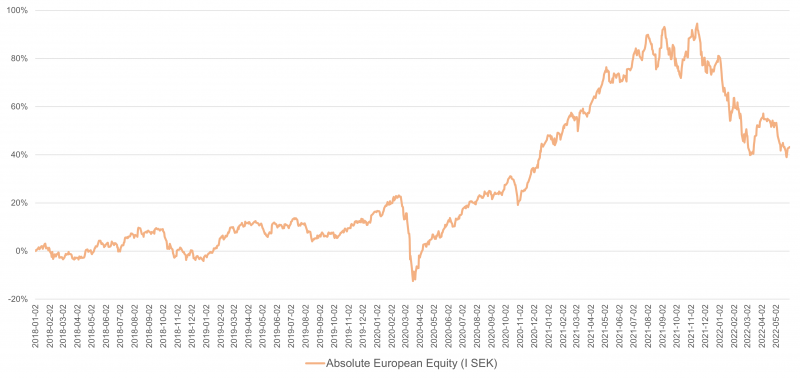

Monthly Newsletter Coeli Absolute European Equity – May 2022

MAY PERFORMANCE

The fund’s value decreased 6.6% in May (share class I SEK). The Stoxx600 (broad European index) decreased during the same period by 1.5% and HedgeNordic’s NHX Equities was provisionally flat. The corresponding figures for 2022 are a decrease of 20.9% for the fund, -9.1% for Stoxx600 and -5% for NHX Equities.

EQUITY MARKETS / MACRO ENVIRONMENT

The month of May began as April ended, which meant high volatility and super moody investors. The US long-term interest rate turned down in the middle of the month and the market changed character from a maximum fear of inflation to rising concerns about global growth. It was also the first month in which, even, the world's largest technology companies came under strong pressure. The end of the month offered a strong rebound where the catalyst was FED-minutes on May 25th.

If there was high volatility at index level, in many cases it was an extremely high volatility at stock level. We also experienced this, which we will return to later. Nasdaq had only five days in the past month where intraday movement was less than one percent. For a full seven days, the movement was greater than three percent. Owning shares during the company reports was in many cases a test for the owners with sharp declines in the share price for companies that did not deliver fully against expectations. By the end of the month, not much had happened at the index level, but the journey there offered very large price movements.

Source: Bloomberg

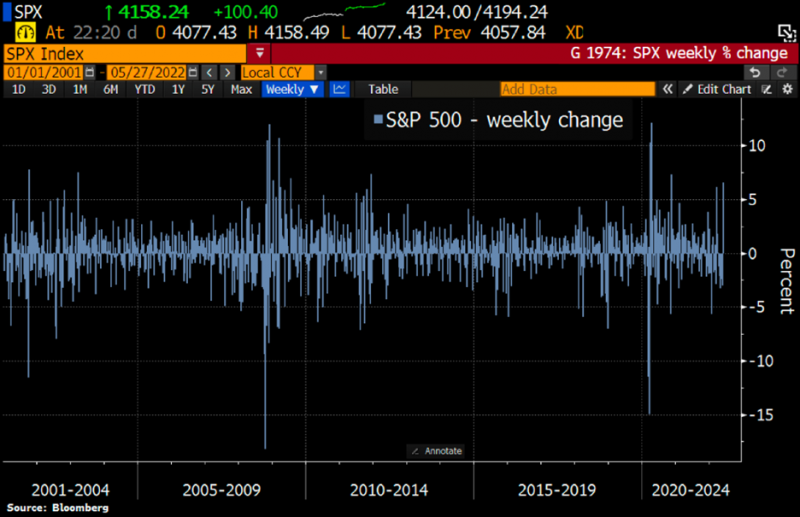

After a staggering seven negative weeks in a row and nearly the longest negative run in 100 years, the negative trend was broken with force at the end of the month. With an increase of 6.6% for the S&P500 it was the largest weekly increase since November 2020.

Source: Bloomberg

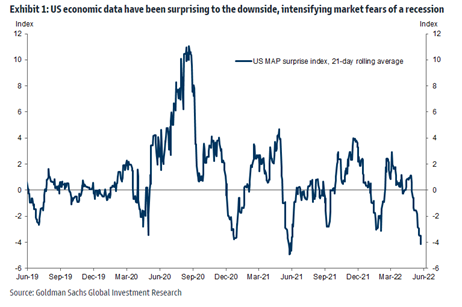

The main reason for the strong end-of-the month (apart from the fact that the market was heavily oversold) was the minutes from the last FED meeting. When FED-minutes was released, it became clear that the central bank intends to raise the interest rate as intended (50 basis points) in future meetings, but to then go data dependent. With an economy that is clearly unwinding (see picture below), the above was interpreted as meaning that the central bank can finish its increases much earlier than previously thought and thus the second half of the year would offer a positive market climate. In that case, it would also implicitly mean that inflation has passed its peak level.

The image below shows Goldman Sachs' financial surprise index. It clearly indicates that we are entering a cooler period, which is exactly what the Fed wants. Focus over the summer will now be on studying financial data.

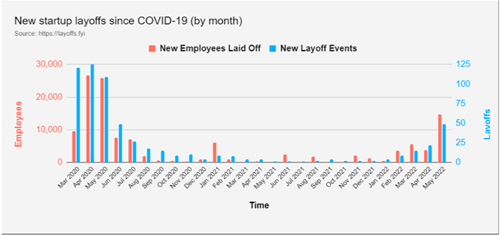

Another clear indicator of a calmer phase in the economy is the picture below, which shows that newly established companies are starting to lay off staff. However, the US labor market remains the strongest in 70 years.

Source: Goldman Sachs

A clear change in the stock market took place in the middle of the month and as usual with high speed. From six months of the market being completely dictated by inflation data and rising interest rates, the fear of inflation decreased at the same time as interest rates retracted and simultaneously shifted to focus on global growth. Despite a significant decline in interest rates from the middle of the month, share prices continued to fall due to a perceived increased risk of recession. The picture below shows the US 10-year interest rate during the second half of May. From the highest level of around 3.1%, it is now down to about 2.75-2.85%.

Source: Bloomberg

If you zoom out and seen from a two-year perspective, it looks as if US interest rates have reached their highest level.

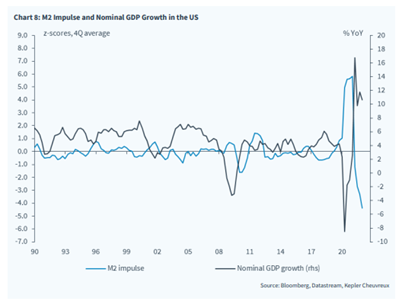

The picture below shows the unprecedented and extremely aggressive monetary policy from the Fed (and other central banks) where the money supply has literally exploded. It created massive growth in the economy, which was much needed during the first phase of the pandemic. The fact that they continued into the second phase has created the imbalances we now see with historically high inflation levels.

Finally, the ECB and Madame Inflation (Christine Lagarde) also stated that it is probably time to abandon the negative interest rate. Market expectations now are that the ECB will implement a first interest rate hike during the third quarter. Interest rate hikes by the ECB combined with stronger recent economic data from the euro area should mean that the euro starts to strengthen against the US dollar after a sharp depreciation in the past year. For example, the business climate in Germany unexpectedly turned positive at the end of the month. Above all, German corporates were very satisfied with the current turnover. As for the future, it was gloomier, but still no visible signs of recession in Germany.

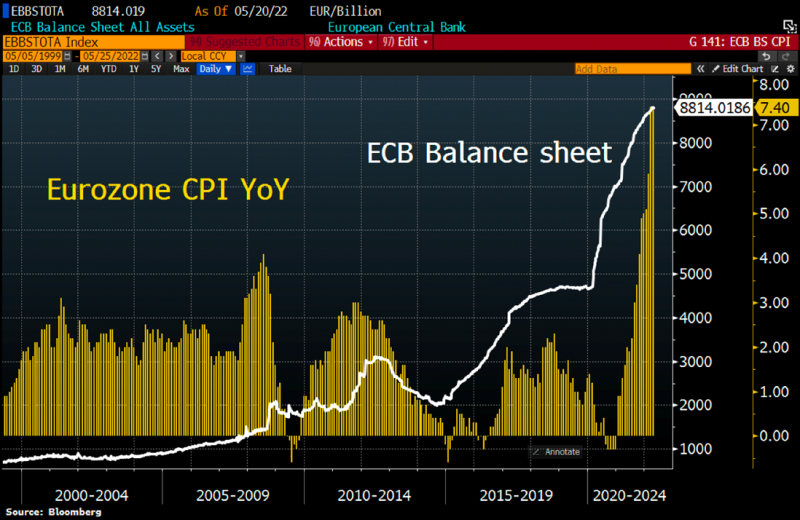

Despite very clear and accelerating inflation in many European economies, the ECB continues with its asset purchases. Not easy to understand with a rational mind. Below is inflation in the euro area together with the ECB's balance sheet.

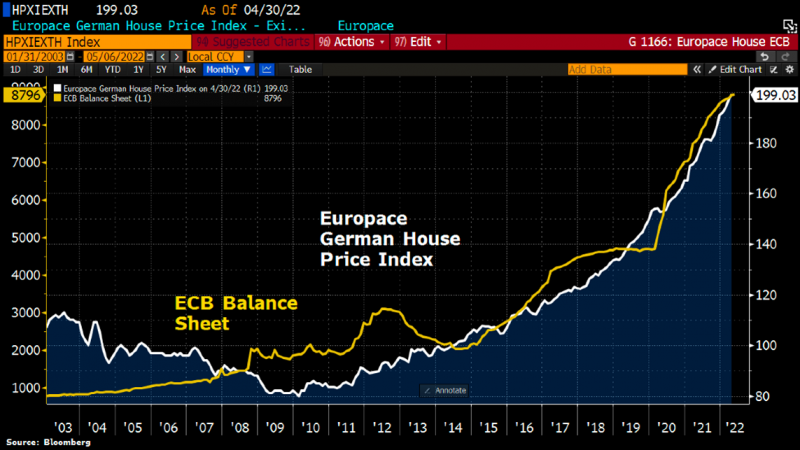

The Germans, who have bad experience with inflation, continue to buy real estate. Prices seem to have a certain correlation with the ECB's balance sheet (written with a slightly ironic undertone).

What's left in the central banks' toolbox?

Source: David Parkins

The EU's purchase of Russian oil continues and finances Russia's war. Many years of historical and significant wrong decisions among European politicians are a big part of the explanation. Finally, EU came to an agreement on the oil embargo against Russia. Hungary's Viktor Orbán, were given a few exceptions due to his country’s high dependency on oil.

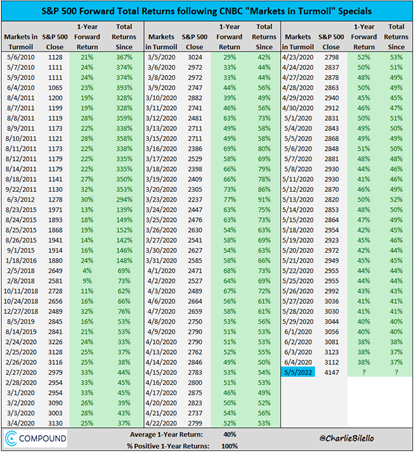

A historically excellent contraindication is to buy shares when CNBC starts broadcasting its Markets in Turmoil episodes. On May 5th, they started and at the time of writing, the S&P500 is unchanged.

Source: @CharlieBilello

Long positions

Truecaller

Truecaller's turbulent stock market journey continued in May. After another report that sharply beat expectations, the share was at its highest 23% higher than the closing price on the last trading day in April. Shortly afterwards, a major share sale was executed by a number of early venture capital investors in a similar way as we saw earlier in the year. This was followed by an article in the Indian press which said that the Indian telecommunications authority TRAI is looking at creating a competing app for Truecaller. By the end of the month, the share had fallen by 4.5%, but from the highest to lowest intraday price, the decline was as much as 45%. Incredible. To clarify, the fund dropped in a few days at most about 3.5% because of the above event alone. Due to the fact that the share recovered and because we increased our position in the tumult, the result for the month was basically unchanged.

In short, the article (which can be read here) states that the authority is trying to create a function that allows the user to see the name of the caller when a call comes, a similar functionality that Truecaller has today. At present, there are not many details about the potential service, but according to the article, it should be based on the KYC process (a brief background check) that customers go through when they buy a subscription or prepaid card.

Our view is that a service of the type described in the article will not have a negative impact on Truecaller. Some of the reasons for this are that the KYC process in India is not reliable, the function requires all telecom operators to join TRAI's service and the service will not detect spam and fraudulent calls, international or corporate calls. TRAI has tried to create a similar service several times historically and has failed on all occasions. Even if the service is released, it will take many years before it becomes a reality.

Truecaller's management was baffled as to the price reaction and has, among other things, commented on the spectacle in a press release and in Dagens Industri.

While at the same time technical factors have made it difficult for Truecaller's share price, the company is doing better than ever operationally. Since the listing, Truecaller has released three quarterly reports that have significantly outperformed analysts' expectations. We believe that Truecaller has some low-hanging fruit left to reap in the advertising business, while the company's new business segments look very promising. EPS growth in 2021–2024 is expected to be 45% per year (CAGR) and we believe that analysts are too conservative. For this you currently pay 15x / 11x EBIT 2023e / 2024e, which we think is very attractive.

Victoria

Victoria, our flooring company, continued its roller coaster during the month. In May, it was unfortunately downhill that took the lead. The reasons for the decline are probably due to gloomier macroeconomic prospects, combined with the fact that there have reportedly been some funds with large outflows that have required them to sell the Victoria share, regardless of price. With limited liquidity in the share, it had a large effect on the share price, which fell 19.7% in May. In addition to this, there is no major news to mention about Victoria in regard to the month of May, apart from the fact that the CEO and other people in the management team bought considerable amounts of shares across the market.

With the assumption that we are entering economically gloomier times and Victoria's exposure to the construction and renovation industry, historically high energy prices and inflation in Europe, it is a given that many wonder how Victoria will cope with the new situation. Historically, the company has succeeded well in getting price increases through to its end customers, and large parts of the company's energy costs are hedged 24 months into the future. Comments from relevant competitors and customers, such as Likewise Group and Headlam, also indicate that the market is still relatively strong. In April, the number of housing transactions in England (an important leading indicator) remained higher than before the pandemic. In our estimates, Victoria is now trading at single-digit profit multiples.

Lindab

Despite the good report for the first quarter of April, the Lindab share continued to fall in May by a further 18.3%. However, historical results are just that - history. The stock market is forward-looking, and fears of a gloomier economic climate are probably an important reason why the share has not functioned this year. However, we believe that the stock market is excessively gloomy in its view. Lindab is a relatively late-cycle company with a large element of renovation revenue, which is less sensitive to the economic cycle than new construction.

The share is now traded at single-digit profit multiples (!), which we think is incorrect given the large quality improvement that Lindab has undergone in recent years, not least regarding the return on capital employed. The insiders in Lindab also seem to think so, as they bought shares on a broad front during the month of May. We also note that Volution, a British ventilation company, recently came up with a positive market update that caused the share to rise by 7%. We have taken advantage of the weakness in the price and increased our holdings.

ISS

The ISS share ended on a positive note after the company released a market update at the beginning of the month. Organic growth was a good 5.4% and profitability continues to improve. Most positive was that the organic growth target for 2022 was raised to “over 4%” from “over 2%.” Since we bought into this turnaround case, management has met or exceeded the ex-ante estimates. They have also continued to buy shares across the market which is central to us from a risk perspective when being part of turnarounds.

We believe that the market is too worried about inflation and its impact on the ISS labor force, which is largely unionized and where the annual wage increase is known from the first day of the year. In addition, the majority of ISS contracts have embedded inflation clauses, which means that the company can relatively easily pass on price adjustments to customers. High inflation should also drive a certain positive effect on new customer intake as many companies review their cost items. The stock rose 6.8% in May and is now trading at a very low 9-10x P/E next year's profit on our estimate.

Teleperformance

For a couple of months now we have built up a medium-sized position in French Teleperformance, which deals with outsourcing of customer support services. The company is led by CEO and chairman Daniel Julien, who also founded the company in 1978. Today, it has over 420,000 employees with a global market share of 7-8 %. The financial history is very impressive; between 2011–2021, EPS grew annually by approximately 20% (CAGR). This year, the share has performed poorly, probably against the background of rising interest rates and inflation concerns. For similar reasons discussed above regarding ISS, we believe that the concern is excessive and have therefore taken advantage of the situation to buy the share. To conclude, the picture below is interesting. It shows analysts' profit expectations in the red line and the share price in the white. It is relatively unusual for them to trend apart as clearly as in the Teleperformance case. We hope to return to the subject later.

Source: Bloomberg

Short positions

The short portfolio contributed with a positive result during the month. The largest contributor was our futures in a Swedish small-cap index and Stoxx600. Some stock-specific short positions that contributed positively to the result were Cary Group and the wind power manufacturers Vestas and Nordex.

Exposure

The net exposure, adjusted for our unlisted holdings, at the beginning and end of the month was 62%, respectively.

Summary

We are of course very disappointed with our performance in May where we had the "wrong" shares in the short term. Our largest negative contributors were 1) Lindab with -18,3%) Victoria with -19,7% 3) Rugvista with -29,6% 4) The fund's put options also contributed negatively by -0,5% as volatility decreased while the index at the end of the month reached positive territory. To make matters worse, both SEK and GBP were reduced against the euro, which together cost about -0.7%. If not a perfect storm, it was many days of torrential rain. The best contributors were the Danish ISS with 0.5% and the French Total with 0.5%.

After a proper roller coaster during the month, the large broad indices ended largely unchanged. As mentioned earlier, several of the fund's large core holdings had very large price movements which, in our opinion, were solely flow driven. It ranged from funds that were forced to sell due to withdrawals from their investors to private equity funds that invested at significant discounts as they needed liquidity for new private investments (Truecaller for example).

The declines created, as usual, additional sales pressure as owners became increasingly nervous when they noticed that the value of their holdings had decreased. One of many paradoxes in financial markets. The greater the decline, the higher the risk according to many. We can willingly admit that the feeling when Truecaller drops from over SEK 70 to SEK 39 in just over a week had a limited entertainment value for us and there was a certain rich use of language in the office. The fact that we bought about 20% more shares at the lowest levels meant that Truecaller's contribution remained unchanged. At the lowest level, the negative contribution for the fund from the highest to the lowest level was around 3.5%! A little too hysterical even for our taste.

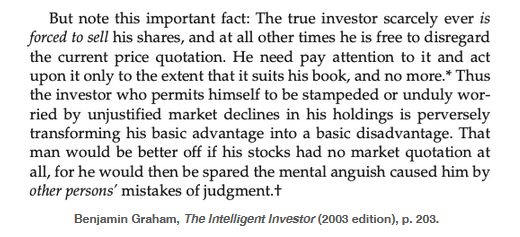

It is in moments like these when we open Benjamin Graham's legendary book from 1949, "the Intelligent Investor".

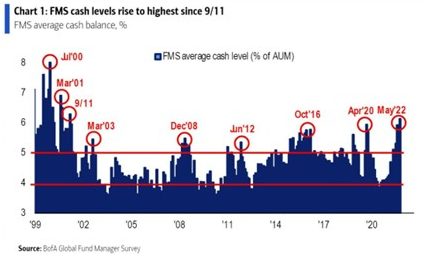

In May, the cash levels of asset managers were the highest since the terrorist attacks on September 11th, 2001! This of course contributed to us getting a rebound at the end of the month.

Source: BofA

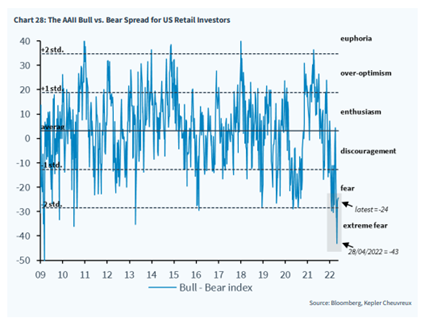

The reason for the high cash level is a record in terms of the relationship between a positive and negative view of the stock market. We have been at the "extreme fear" level where we were last during the financial crisis.

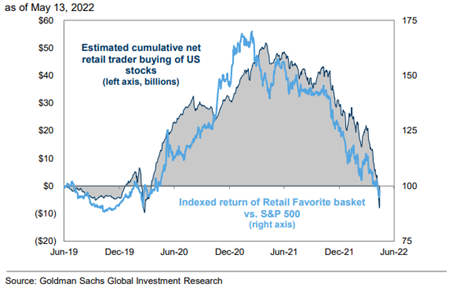

Perhaps the biggest concern in recent months has been (and continues to be) what will happen when US private investors start selling. The answer is that they have now sold all the shares they bought in the last two years, at least according to Goldman Sachs' estimate below. That estimate will be very interesting to track.

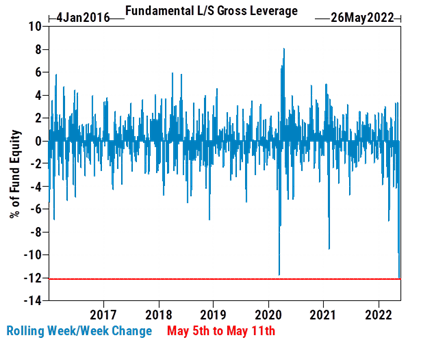

If you study Goldman Sachs hedge fund investors' exposure over the past few years, you can see that May showed a substantial reduction in the balance sheet. On the far right is a decrease of 12%, which is the strongest decrease in active risk in five days since they started studying data in 2016. Even a sharper decrease than in March 2020! Unbelievable.

So to summarize the above pictures, in May 1) the cash balance of institutional clients was the highest since 2001 2) US private investors have sold everything they bought in the last two years and 3) hedge funds have in a short time reduced their gross exposure at a very fast rate 4) investors worldwide are super moody. It feels like all the ingredients to create a real boom in the market.

Before the stock market started to rise at the end of the month, even junk bonds had started to rise, which is a good indicator for understanding the stock market. The picture below shows the development for the last year.

Source: Bloomberg

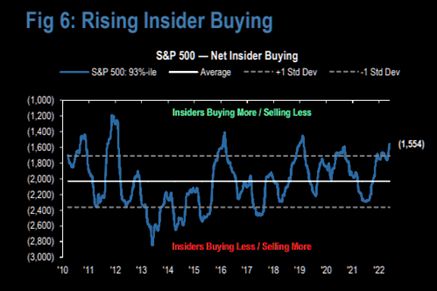

One group that clearly went against the negative trend were insiders who increased their purchases of shares in their own companies and are now well above a historical average. The purchases were made widely across different industries. Below are US companies and their insiders.

Source: JP Morgan

The repurchase mandate began during the month with new and large mandates. Volumes in May were 45% higher than the corresponding period last year and the total mandate is as much as 429 billion USD (there will be many shares). Undoubtedly a factor that supports the US stock market and if European companies had understood the power of using some of the capital (which is ours, not the company's) for value-creating repurchases, perhaps European values would have approached the US somewhat.

Suddenly it happens! Sharply falling stock markets eventually led to a real inflow in the last week of May. It may be worth mentioning that the majority of our team in recent weeks also invested significant amounts in the fund.

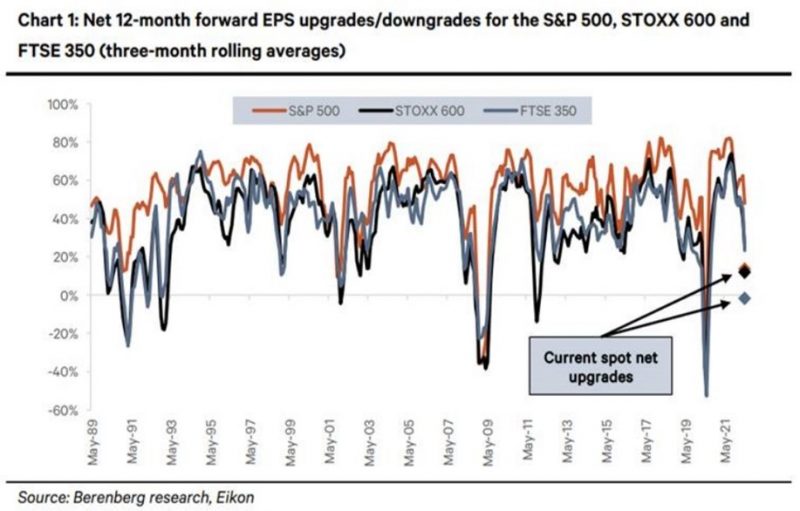

Downgrades of the profit estimate have been dripping for months and are now down in negative territory. Before adjustments begin, the stock market has probably swung for a more lasting upturn. It is still unclear when this will happen, but it is quite clear that risk/reward today is significantly much better than a few months ago.

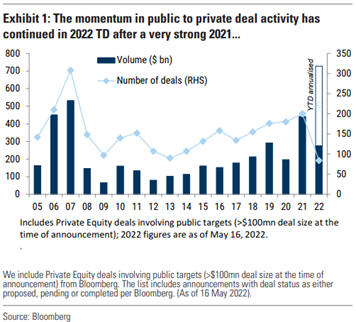

The acquisition of Swedish Match a few weeks ago will probably be followed up by several company acquisitions in coming months. Many companies have so far shown good resilience while values have fallen. Companies and private equity firms continue to have strong balance sheets and capital must be put to work. The picture below shows that with the current annual rate, 2022 will be a new record year.

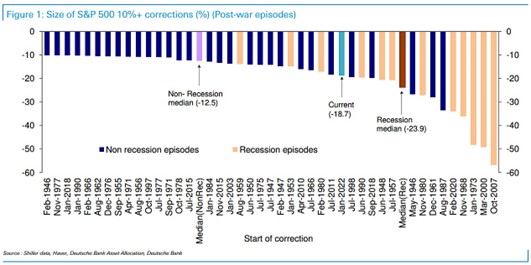

To put the current correction in a historical perspective. The picture below shows the corrections since 1946 that have been at least 10%. The blue bars to the left show how big the correction was when there was no recession. The median drop in those cases is -12.5%. Until the end of May, the decline this time was -18.7%. The median decline when it ended with a recession is -23.9% and during the financial crisis, the S&P500 fell as much as 57%.

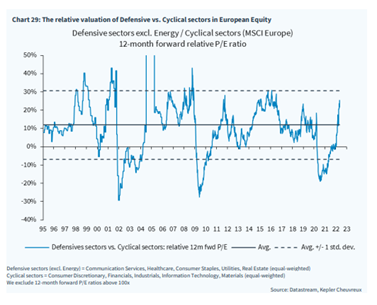

Defensive companies are now traded at very high premiums in relation to cyclical companies. When the curve is tilted as much as below, it usually reverses at high speed. A balanced portfolio is to be recommended.

So what is our conclusion after all the events these recent weeks? The short answer is that we stick to our market view that the lowest level in Europe was set on March 7th and that we will trade in a price range for the time being. The interest rate appears to have reached its peak in May and the central banks are starting to talk a little less hawkishly. The USD also appears to have reached its peak and a weaker dollar is generally positive for risky assets.

In May, the U.S. was the last major stock market to fall back. When the last generals fell in the form of the American FAAMG companies, the stock market also capitulated with steep declines as a result. With a very high concentration risk from a few companies in the S&P500 and Nasdaq, it hit the index hard. Nasdaq was, at most, down almost 15% from peak to trough in May and at the lowest point -29% YTD. The declines from the previous top level are for Netflix -72%, Facebook -50%, Amazon -40%, Alphabet -28%, Microsoft -23% and Apple -21%.

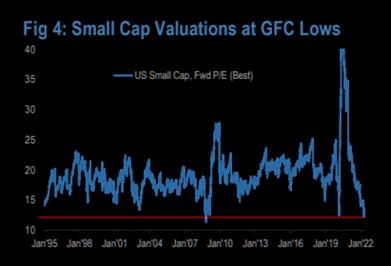

While the United States capitulated, many other segments actually stabilized when Europe (in our opinion) already have had its capitulation. Inflation data seemed to level off, interest rates fell and small companies, both in the US and in Europe, showed clear signs of stabilization. Somewhere the price is starting to become attractive even for the biggest pessimist. The image below shows the valuation for small companies over the past 27 years. The valuation does not seem strained.

Source: Goldman Sachs

We are not macroeconomists, but we consider it less likely that the U.S. will enter a recession this year as 1) the labor market remains very strong 2) positive effects from the post-covid continue to roll out 3) the housing market seems to be holding together 4) the profitability of the U.S. companies is still at high levels. In Europe, the picture is the same but on a smaller scale. We have not had such a strong economy, but not so high inflation, for example.

Finally, we continue to be close to our companies and follow them carefully. We have just started a recruitment for a third analyst who will work together with Fredrik and Gustav from the Malmö office, and we hope to be done by August.

Enjoy June with school graduations and upcoming sun and heat. Soon it will be midsummer, and we Swedes look forward to the herring!

Mikael & Team

Malmö, 3rd of June 2022