Note that the information below describes the share class (I SEK), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class' return. The information below regarding returns therefore differs from the returns in other share classes.

Before making any final investment decisions, please read the prospectus, its Annual Report, and the KID of the relevant Sub-Fund here

This material is marketing communication

Monthly Newsletter Coeli Absolute European Equity – May 2023

MAY PERFORMANCE

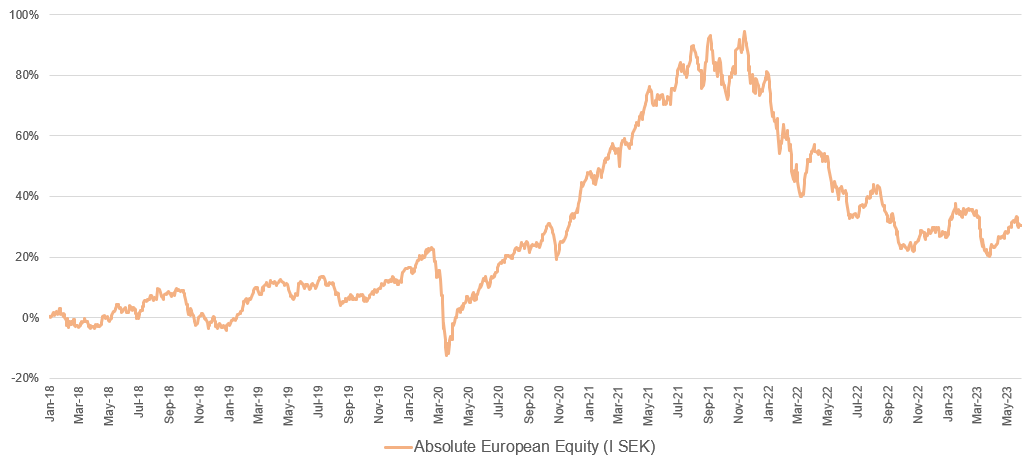

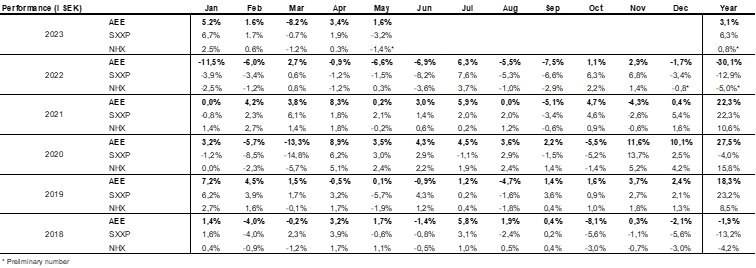

The fund’s value increased by 1.6% in May (share class I SEK). The Stoxx600 (broad European index) decreased during the same period by 3.2% and HedgeNordic’s NHX Equities decreased provisionally by 1.4%. The corresponding figures for 2023 are an increase of 3.1% for the fund, +6.3% for the Stoxx600 and +0.8% for NHX Equities.

EQUITY MARKETS / MACRO ENVIRONMENT

The reporting season continued in May with continued strong delivery from the companies. The Fed raised interest rates as planned on May 3rd by another 25 basis points to 5.25% after 10 rate hikes in 14 months. The following day, the ECB raised the key interest rate by 25 basis points to 3.75%.

The broad European index fell in May by 3.2%, while the S&P 500 rose by 0.2%. MSCI Europe Small & MidCap fell by 3.2%, while the Nasdaq rose by as much as 5.8%. The fund's strong momentum that began with LVMH's report on April 13th continued during May and the monthly return ended at +1.6%. Since then, the fund has risen by 4.8% while the Stoxx600 over the same period has fallen by 2.3% (local currency). As a point of reference, the Carnegie small company index fell by 4.4% during the same period. Last reporting season, which was in February, was internally viewed as the best since the fund's inception in January 2018, but this one was even better. More on that in the section on long positions.

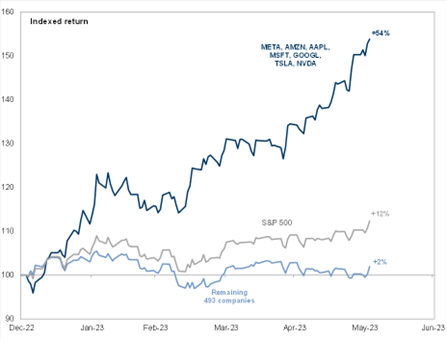

The buzz word of the month was undoubtedly AI, which affected technology stocks in an extreme and rare way. The Nasdaq has risen by as much as 23.5% this year. That's the strongest start to a year since 1991. Does anyone remember the Nasdaq's decline last year, which ended at 33.1%? Apple, Microsoft, Google, Amazon, Nvidia and Meta have this year added $3 trillion in market capitalization, which is more than the entire US industrial sector and on par with the entire Eurostoxx50. Unimaginable numbers.

Attached is a clip from Nvidia's Q1 presentation: https://twitter.com/gurgavin/status/1661481398228893696

Below is an unparalleled image that shows the development of the major technology companies YTD in relation to other companies in the S&P500. The clairvoyant notices a certain difference in the development.

Source: Goldman Sachs

For months, the market has had a rising anxiety about the USA's debt ceiling, which needed to be raised so that the country would not default on its payments. The process was surprisingly painless (compared to 2011 which we have in vivid memory) and on June 1st the Senate voted yes and now life goes on.

The development in May for the 500 companies included in the S&P500:

Source: Sven Henrich, Twitter

Another way to illustrate recent developments: https://twitter.com/wallstmemes/status/1661478278841126912

The development so far this year is not appreciated by the large investor collective as their positioning has been too cautious. Entering the second quarter, US hedge funds collectively had their highest exposure since Q1 2020 to defensive sectors such as pharmaceuticals and consumer staples. The opposite for technology where they had their lowest exposure since Q3 2007. It didn't turn out well, at least not so far.

The European real estate sector was under pressure after a strong development in April and the Swedish real estate sector was at the epicenter. On Friday, June 2nd, Ilija Batljan finally had to leave the CEO post for SBB, and lenders and bond investors are now taking over. Interesting that Akelius CFO, Leiv Synnes, is jumping ship and joining as the new CEO of SBB. Swedish property shares rose that day by around 6% and SBB rose the most with 53%. In three days, 50% of the shares in SBB were traded. The verdict is clear, and the board has, to put it mildly, a lot to explain to its shareholders (and to the whole of Sweden). What a circus! An interesting development follows.

Source: Goldman Sachs

The Swedish krona was exceptionally weak in May, and much is due to the turbulence in the real estate sector. The correlation between SEK and the development in SBB is frightening, see picture below. In three weeks, the Swedish krona weakened a full four percent against the euro and has now fallen by 4% this year, 12% in two years and by nearly 30% in five years. It is particularly gloomy and serious for the Swedish economy and Swedish citizens. We note that the common man thinks the krona is extremely undervalued, while those who trade the krona continue to sell. The fact that the Riksbank (Swedish Central Bank) does not step in and start selling its dollar and euro assets and buy kroner is incomprehensible.

Source: Bloomberg, Coeli European

We note that the Riksbank, deservedly, a few weeks ago received scathing criticism in an appraisal commissioned by the Riksdag’s (Swedish Government) finance committee. The Riksbank acted too slowly to stop the rising inflation and, moreover, the inflation forecasts were inadequate. Well thank you, there were quite a few people who were out in the real world who told them at Brunkebergstorg that it might be time to stop buying housing bonds in a red-hot real estate market when they simultaneously had negative interest rates in the system. The next Riksbank meeting is on the 29th of June, and it would be extremely appropriate to stop the increases and study the after-effects for a while. Precisely because of that, it will probably be the opposite and a continued increase. So far, the interest rate hikes have affected the krone exchange rate, albeit in the wrong direction with further weakening. Perhaps it is because those who trade the krona are more concerned that the real estate problems increase further and break the systems in Sweden instead of, according to the textbook, buying up the krona as you get 0.25 percentage point more in return? But the Riksbank is certainly aware of that.

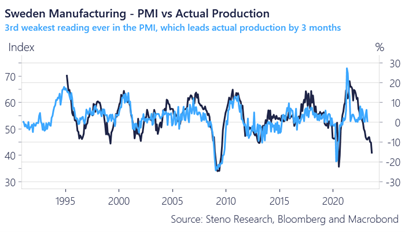

Further arguments for holding off on more interest rate increases are the image below. It will take a lot to avoid a recession if historical correlation continues to apply. We recently witnessed the third weakest PMI (purchasing data, black line) figure ever measured, which is likely to lead to production cuts in a few months. Incidentally, notifications are now increasing, not least in the construction industry. Continued interest rate hikes increase the likelihood of serious double mistakes from the Riksbank. Those of us who were there in 2008 when the Riksbank raised the policy rate a few days before Lehmann Brothers went under, tremble before their decisions in the coming months.

There was supposed to be a picture of CHF/SEK her, but it's too sad so we skip it.

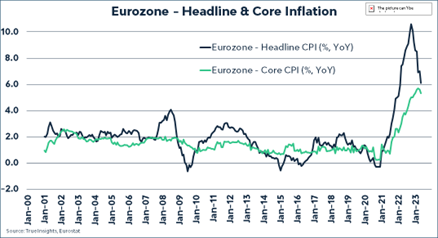

Inflation continues to fall in many areas, while the resilience of many economies surprised positively. What has surprised the most this year is the companies' ability to handle inflation, which in May dropped to 6.1% against the expected 6.3%. The decline was broad-based with food, energy and core inflation falling. The central banks will probably turn around within a few quarters and start lowering policy rates (our view). Worth mentioning is inflation in Spain. It has been seen as a drag on the eurozone and came in at a low 2.9% in May against an expected 3.3%. Good!

Source: TrueInsights, Eurostat

Spanish inflation over two years. From +2.5% up to +11% a year ago and now down to +2.9%. Good job and we look forward to similar developments in several areas during the autumn.

Source: Bloomberg

Several prices at the producer level are also now falling, including prices for many raw materials. A good example is the European gas price which exploded upwards in August, and which led to major problems. Since the top in August, the price has fallen by a not insignificant 90% .

Source: Bloomberg

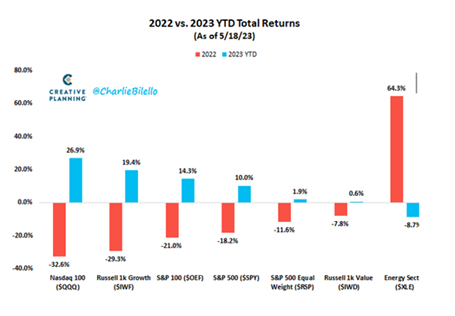

It is darkest before the sun rises. This year's development up until now in various asset classes is in many cases the opposite of last year.

Source: Creative Planning, @CharlieBilello

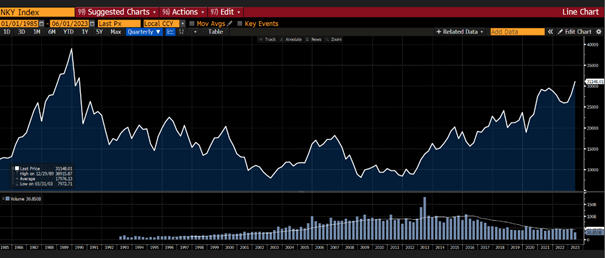

"So tonight I'm gonna party like it's 1989!" It's a party in Japan. After waiting 34 years for a new ATH and having risen by just over 20% this year, the Nikkei index is now near a new ATH. The one who waits for something good... A bit of a shame that it seems to have taken more than a generation.

Source: Bloomberg

At least it's less uncertain now compared to a few years ago.

The world's second largest economy is having a hard time getting out of the starting blocks. After a strong start following Covid restrictions being lifted, the economy has weakened again. Expect the Chinese state apparatus to inject something strong into the system soon.

Source: Kepler Cheuvreux

JP Morgan warns investors that the bank currently has enough capital to be able to absorb the equivalent of all US bank losses during the financial crisis. We take our hats off to Jamie Dimon, who has been the bank's CEO since 2005.

Source: Twitter, Marc Rubinstein

Senator Kennedy was liberatingly clear at the hearing of Silicon Valley Bank CEO, Greg Becker. Will we see something similar regarding SBB's board? Probably not is likely the answer.

https://twitter.com/unusual_whales/status/1658709178859540480

Long positions

Surgical science

Since January this year, we are once again owners of Surgical Science. We have long liked the company, which deals with surgical simulation, but have sometimes struggled with the high valuation of the stock. At levels around SEK 150–160 per share, we again thought that the valuation had come down to a good level given the quality of the company. There's a lot to like here:

• A monopoly-like position in a fast-growing market, where Surgical Science's product is implemented by most of the companies dealing with robot-assisted surgery.

• The simulation market is still relatively small in a larger context, which should reduce the appetite for competition and, as such, is a barrier to entry.

• Leading technology. Around 20% of the company's sales are reinvested in research and development. This provides good conditions for maintaining the current lead.

• Expanded gross margins and strong operational leverage, with very high return on capital employed.

• An extremely talented management team.

In May, Surgical Science released one of the better reports we've seen this reporting period. Organic growth was 38% (30% adjusted for certain one-off effects related to the order book). In addition, the sales mix was good, as the highly profitable license revenues almost doubled to make up about 31% of sales (22% in the corresponding quarter of 2022). This helped to strengthen the operating margin significantly. Of the sales increase of around SEK 70 million, around half was converted into operating profit, which beat advance expectations by around 55%. Cash flow, which was at times questioned by the market last year, was very strong. Surgical Science has a strong balance sheet with a net cash of almost half a billion kroner.

During the month of May, the Surgical Science share rose by 22% and made a strong contribution to the fund's development, even though our initial position was relatively small. To buy the share at today's prices of around SEK 230 per share, you need to believe in the company's long-term goal; To reach a turnover of around SEK 1.5 billion in 2026 and this at an operating margin of 40%. After the company's two most recent reports, we feel ever so convinced that the company will succeed in this.

Storskogen

During the past 12 months, few stocks have been as hotly debated as Storskogen. And it has mostly been in negative terms; Rightfully so, we think. After several years of an extremely high acquisition rate, Storskogen had problems with cash flow generation last year, which in combination with a strained balance sheet, declining economy and a general skepticism towards the company's strategy caused the share to fall by 88% in 2022. We ourselves have been doubtful about Storskogen and understood the price drop.

During the autumn, we noted a change in tone from the company's management, which reduced the pace of acquisitions and placed a greater focus on cash flow conversion and cleaning up the balance sheet. After following up this new communication with a fourth quarter for 2022 that clearly showed improvements on these points, the first quarter numbers of 2023 were released in May. The report, which beat expectations for operating profit by around 15-20%, continued to show that cash flow had improved.

We bought a small observing position in Storskogen in March and despite the small position, the fund received a good contribution from the stock, which rose by 27% in May. This is still a high-risk stock and we retain a small position in the company. If management can follow up on the two most recent reports with continued good cash flow generation, we believe that the upside is large despite this year's price rise.

4Imprint

London-listed 4imprint has been one of the fund's top holdings over the past 12 months. In one year, the share price has risen by almost 80%, including a large one-time dividend. Technically, it's only the share price that has anything to do with the UK as basically all the business is based in the US. 4imprint is a distributor of promotional gifts (give aways), typically products used for marketing purposes, for example at conferences and events.

In May, the company released a brief update for growth in 2023, where order intake rose by 22% during the January-April period. Despite the good growth, the share initially fell by 8%, because the company forecasted for somewhat weaker growth in the coming months (mostly due to complex comparative figures). The stock subsequently recovered and closed the month 2% higher than during the beginning. We believe this is partly due to the stock being included in an important index, and we have taken advantage of the situation by selling off parts of our position.

Wincanton

The British logistics company has been one of the year's worst performing stocks after management was forced to issue a profit warning in March. At that time, the fund bought shares at low levels. In May, Wincanton released a report that confirmed the outlook given at the time of the profit warning, while the company's new CFO spoke positively about the opportunity for Wincanton to stop paying as much in deposits to its pension debt as it has done historically. The absence of a further profit warning was probably enough for the stock to recover. The stock rose by 15% in May and has thus fallen by 27% this year.

Bonesupport

The Bonesupport share continued to gain steam during the month of May and was one of the fund's strongest contributors. We have not noted any news that explains the price rise but believe that the share is still being discovered by the market after several strong quarters in the bag.

Rugvista

At the end of May, Rugvista held a capital markets day. The most interesting news revolved around the new website, which as of the capital market day had been launched in 5 out of 20 countries. In 2023, the website will be rolled out in the remaining geographies. The idea is that the new website will, over time, help the company convert more website visitors into paying customers.

The company has a clear focus on profitability during this period as the consumer market is currently hard hit by inflation, higher interest rates and pressured households. However, it maintains its financial goals, which include an organic growth of 20%. Once the market turns, the company will be ready to invest in growth. Extra focus was also placed on the DACH region (Germany, Switzerland, Austria). In that region, Rugvista sells as much as it does in the Nordics, but the market is several times larger.

Despite a tough market, Rugvista has the ability to control its own destiny. There should be very low-hanging fruit when it comes to, for example, the marketing mix (the company's brand advertising has until recently been basically non-existent). We also received more information about how Rugvista works within different parts of the organization, for example in purchasing, marketing, technology, and sustainability. They also provided an insight into how all parts of the organization work together to achieve both externally and internally set goals.

The Rugvista share rose 17% in May and made a good contribution to the month's results. The stock trades around EV/EBIT 11x/9x 2024/2025e on our estimates.

Corem

Real estate stocks have had a turbulent development this year, to say the least, which also includes Corem. After a strong April, the trend was reversed in May when the real estate index fell by around 10% and Corem by as much as 25%. A clear catalyst for the downward acceleration was when SBB was downgraded by S&P on May 8th.

Since Q4 last year, Corem has sold properties for nearly 9 billion, all around book value, and now owns properties for around 70 billion. The fact that assets were sold is interesting as the share trades at a sky-high 75% discount to NAV. What is even more interesting is that at the closing price on the last day of May the cash flow is valued at around 8x and then you have an average interest rate of a relatively high four percent. Of the total loans of approximately 40 billion, 10 billion are bond loans. The bonds maturing in the current year will be bought back or terminated at maturity, which, other things being equal, will reduce the average interest rate. To be able to do the corresponding exercise with all the bonds maturing in 2024, you need to sell properties for an additional 10 billion, something we believe is doable. What has put extra pressure on the share is the fact that the main owner, Rutger Arnhult, has a high level of leverage, although significantly less than six months ago. The parent company has acted resolutely and in a short time has reduced the loans from 18 billion to 8 billion. Their own properties have a loan-to-value of a low 35%.

Corem will continue to sell properties and release capital. We are impressed so far with the speed of the sales and also the fact that they have done it at book value. The level of risk in this investment is high, but so is the potential. The position size is under four percent and with a number of short real estate positions against it, the net position is half of our holding in Corem. Compared to SBB, if anyone is thinking about it, Corem delivers well with cash flow and has a small part of the loan structure in bonds. For SBB, it is exactly the opposite and, moreover, they very likely have challenges in their book values.

Finally, it is also worth studying the development of Corem's bonds. The price development is significantly stronger than the corresponding development for the share and you can clearly see an improvement since December 2022 when they started announcing large divestitures. Those who lent money to the company are obviously far less concerned about the balance sheet than the shareholders are.

Source: Bloomberg

Short positions

The short portfolio contributed to a positive result during the month. The biggest contribution was made by our short positions in Swedish and European small company indices. Among the stock-specific positions, several property shares contributed positively to the month's results.

Exposure

The net exposure, adjusted for our unlisted holdings, at the beginning and end of the month was 77% and 73% respectively.

Summary

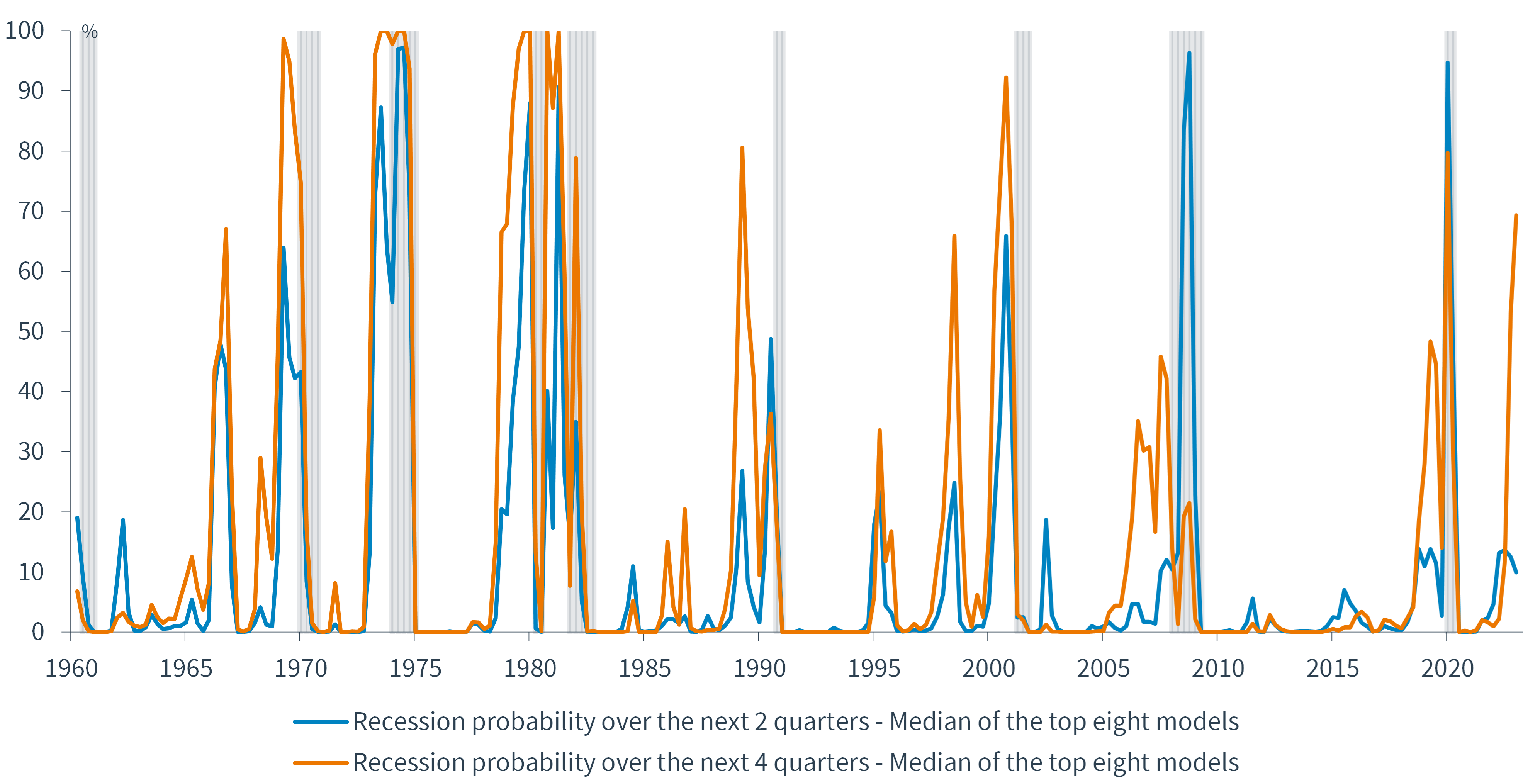

Investors have been waiting for over a year for a recession that has yet to materialize. The chart below shows expectations for a recession since 1960, and the yellow line on the far right means investors see about a 70% chance of a recession within four quarters. The problem with that view so far, has been that it's been over a year since the market swung to this view. This has led to the large collective being far too cautiously positioned, which in turn has led to a worse return than the broad indices.

Source: Kepler Cheuvreux

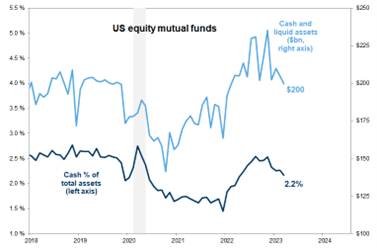

US equity funds' cash positions are now starting to decline, likely forced as US managers generally lag their benchmarks. The main underweight is the technology companies.

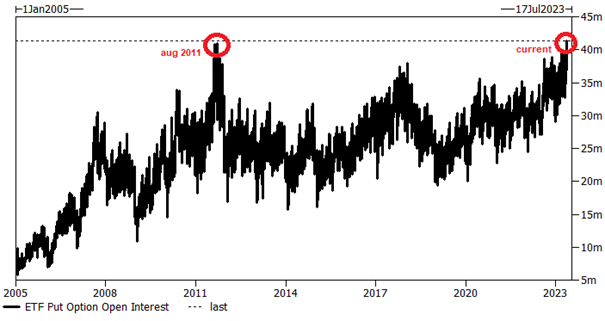

The image below also illustrates investor skepticism. Never before have there been so many outstanding put options as now. The last time the volumes were at these levels was in 2011, when the stock market fell by 15-20% in a short time due to problems with raising the debt ceiling in the US.

Source: Goldman Sachs

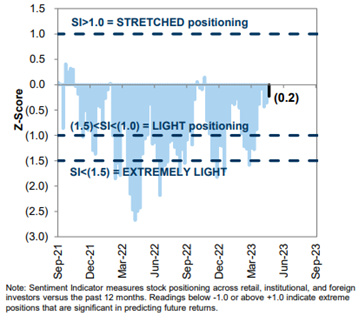

The market has gone from an extremely cautious positioning a few months ago, to one "commonly" cautious now.

Source: Goldman Sachs

It has been and continues to be relatively easy to paint a gloomy scenario for the world's stock exchanges. Earnings growth for the broad US and European indices is expected to be broadly unchanged in 2023, while the economy shows signs of slowing activity. Values in the US are higher than the historical average, while in Europe it is the opposite. The geopolitical risks remain significant.

The problem with the gloomy market view is that it has now been over a year since the conditions changed and we are approaching the time when the central banks are done with their interest rate increases. Arguably, the cuts will fuel any kind of risk when they come. We do not have a strong view on whether the American economy will enter a recession or not, but if it does, we think it will be relatively modest and the same applies to Europe. And if there is a milder recession, large parts of the economy and various geographic areas will not notice it. After a few quarters, when the recession is over, everyone will wonder what really happened. We note that the US economy continues to create around 300,000 jobs each month and as long as this is the case it is hard to see a recession happening. Our way of attacking this is to have a balanced portfolio and focus on our companies' performance and conditions.

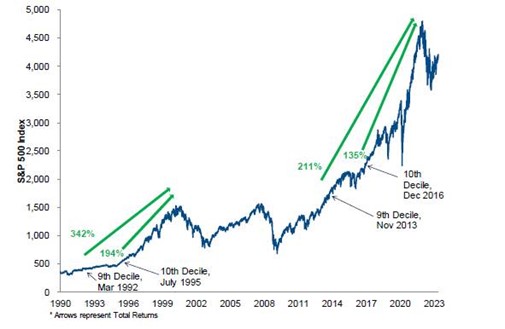

Historically, it has often been costly to exit the stock market in similar situations based solely on valuation. The image below shows the return after different time periods and at times when the market was considered too expensive (ninth and tenth deciles).

Source: Goldman Sachs

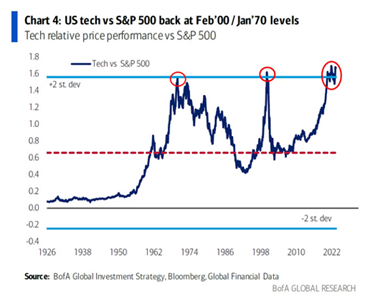

This year's rise began with good breadth in the market, i.e., most share prices rose. After the banking crisis in March, this changed and investors turned to the big companies, and then mainly American technology companies. Not since 2000 has the rise been so dependent on so few stocks. Our view here is that it is high time for the smaller companies to step up and make their contribution.

Historically speaking and relative to the market, the valuation for the American technology companies is starting to get strained.

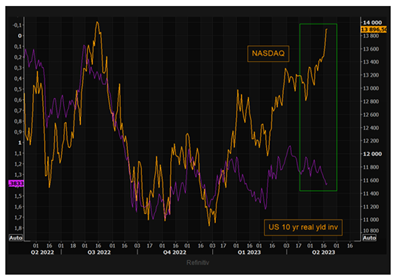

The co-variation between the interest rate and the valuation of the technology companies has been completely decoupled in recent months. Some of it will have to give way and after the summer we will know more.

Source: Themarketear.com

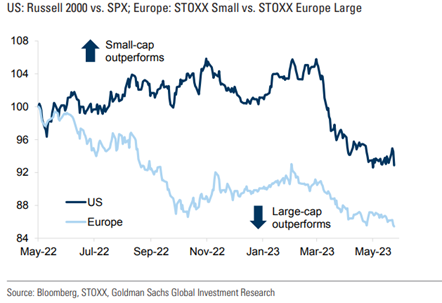

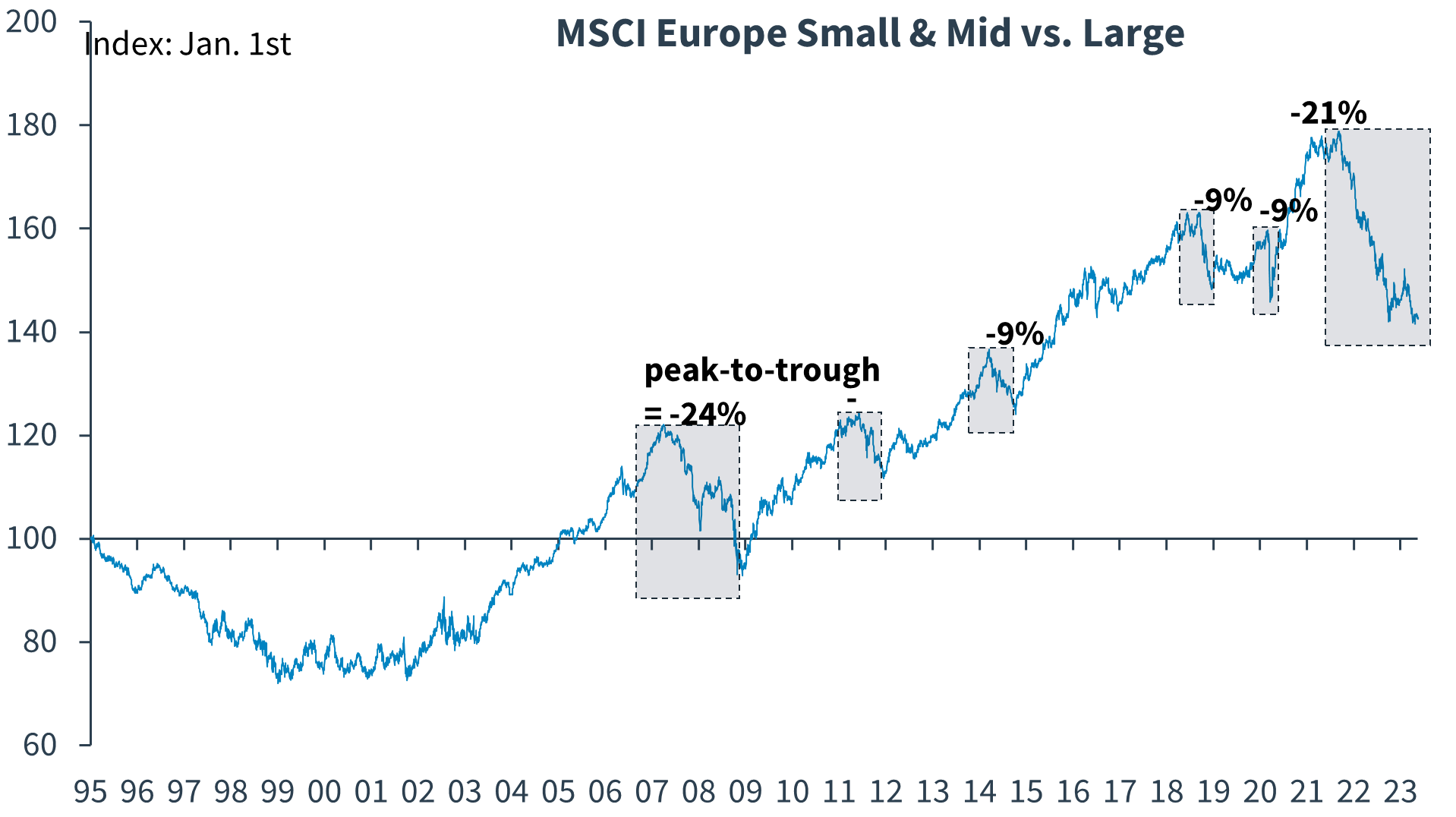

The smaller companies started the year strong, but after the banking turmoil in March have lost significantly, both in the US and Europe.

Illustrated in a different way and since 1995, relative returns of European small companies to larger companies. The time has come to increase allocation to smaller companies (our view).

Source: Kepler Cheuvreux

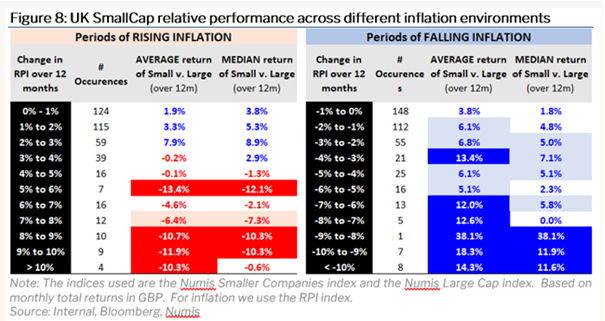

Below is an interesting picture that shows how small companies that are listed in the UK develop significantly worse than large companies in times when inflation rises and vice versa. It is probably because larger companies typically have an easier time dealing with inflation as they are more often price leaders and have a more diversified product portfolio. Inflation is now on the way down.

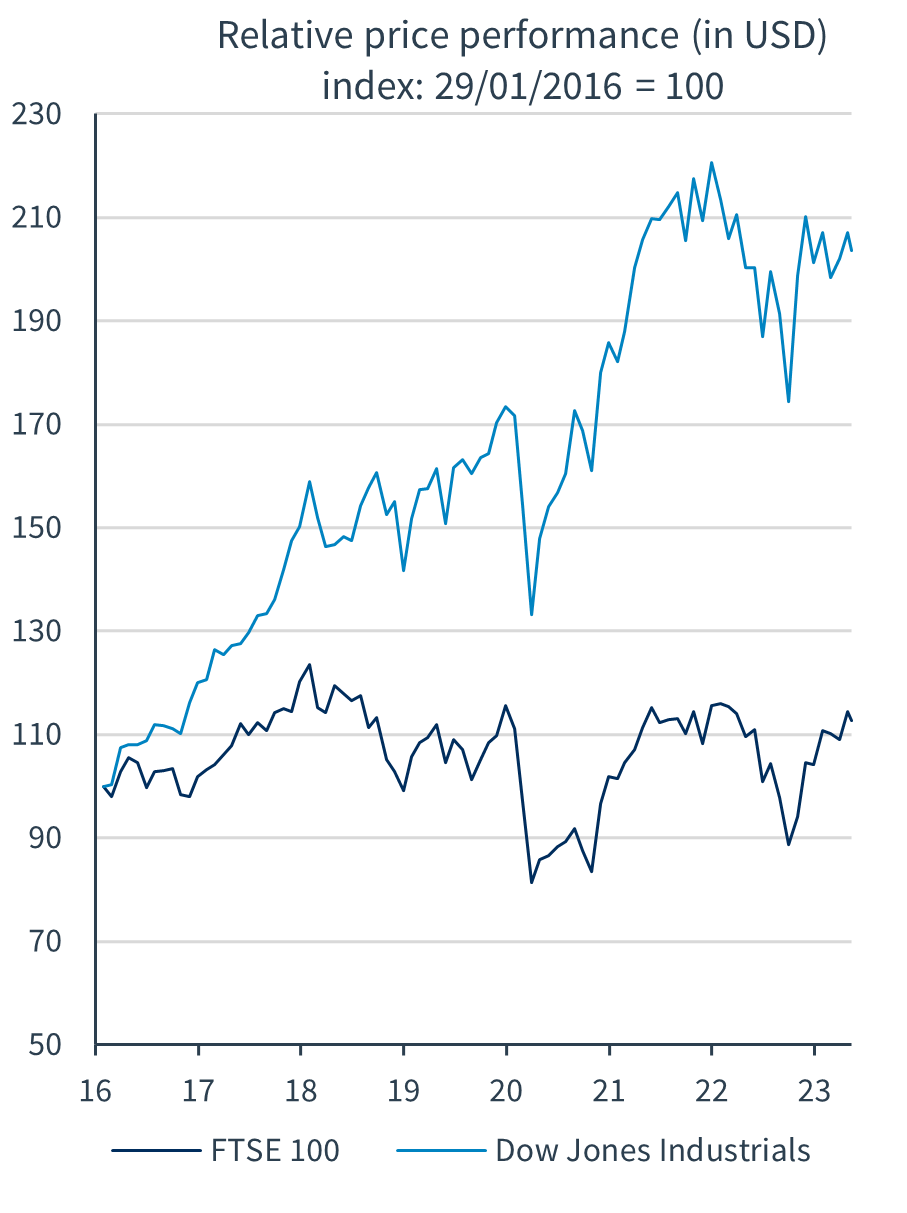

The fund has significant exposure to the UK in several companies with strong balance sheets and returns linked to a low valuation. Below FTSE 100 (UK) vs. Dow Jones (US) since 2016. A huge difference in returns.

Source: Kepler Cheuvreux

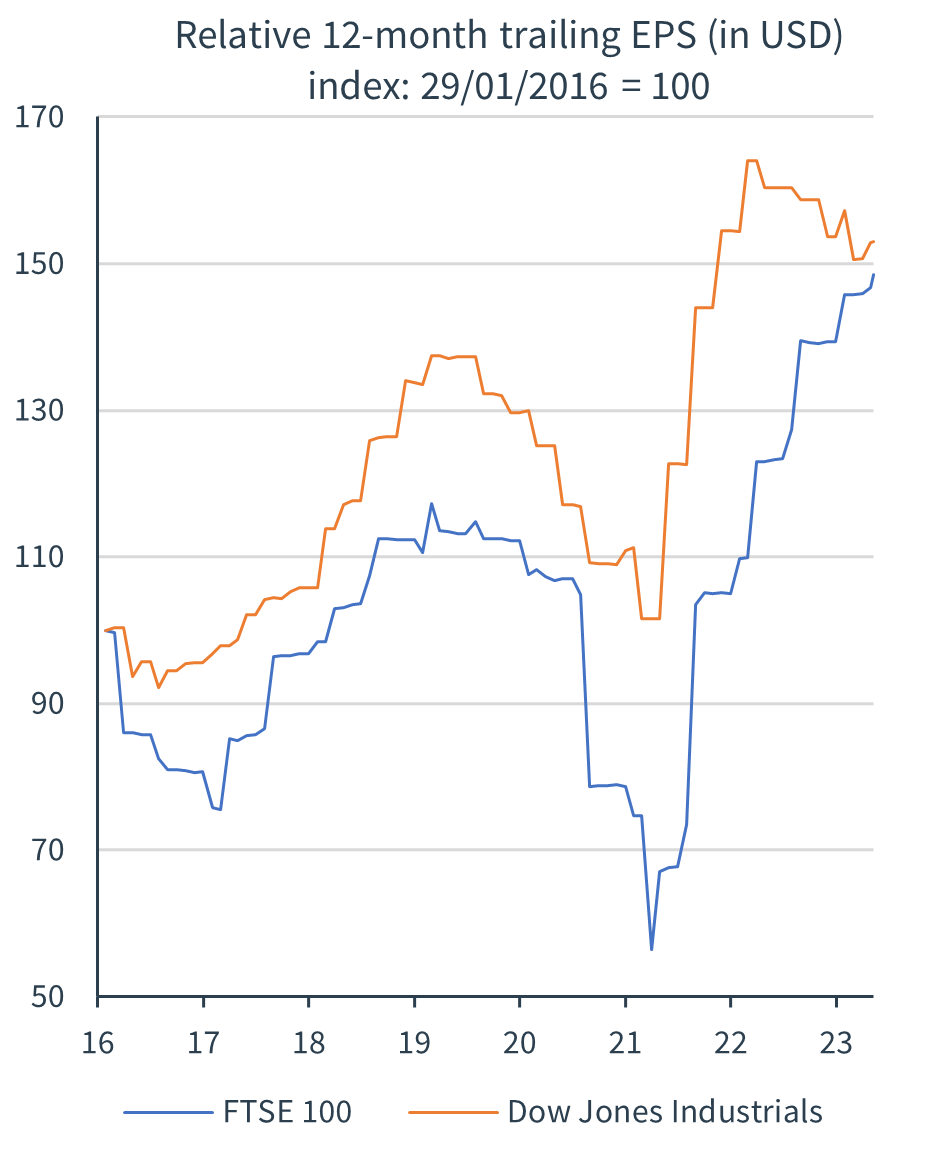

If, on the other hand, you study the development of earnings per share, the development is roughly the same. This should suggest that the stock market in the UK should be at least partially revalued.

Source: Kepler Cheuvreux

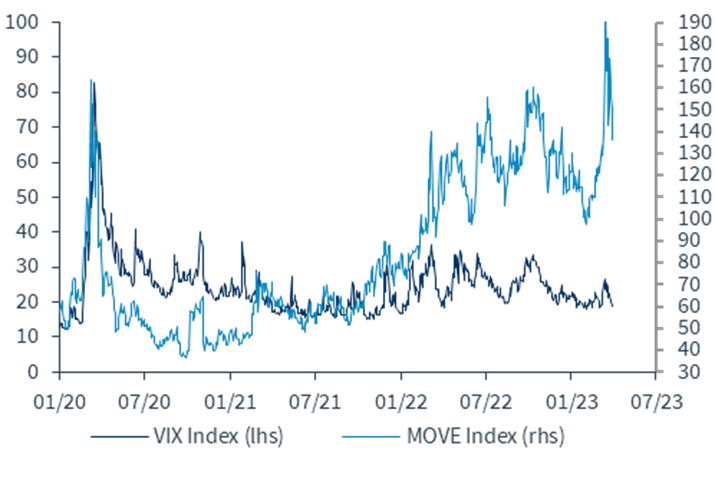

The VIX index, the volatility of the stock market, is at record lows while the MOVE index, the volatility of the bond market, is at high levels. The stock market (at least the broad indices) is currently sailing in surprisingly calm waters.

Source: Kepler Cheuvreux

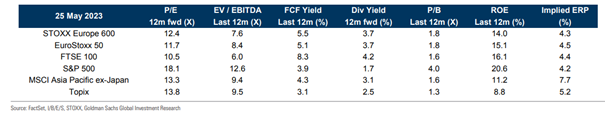

Below valuation levels from the end of May on some of the major global indices. The USA and the UK stand out with the highest and lowest ratings.

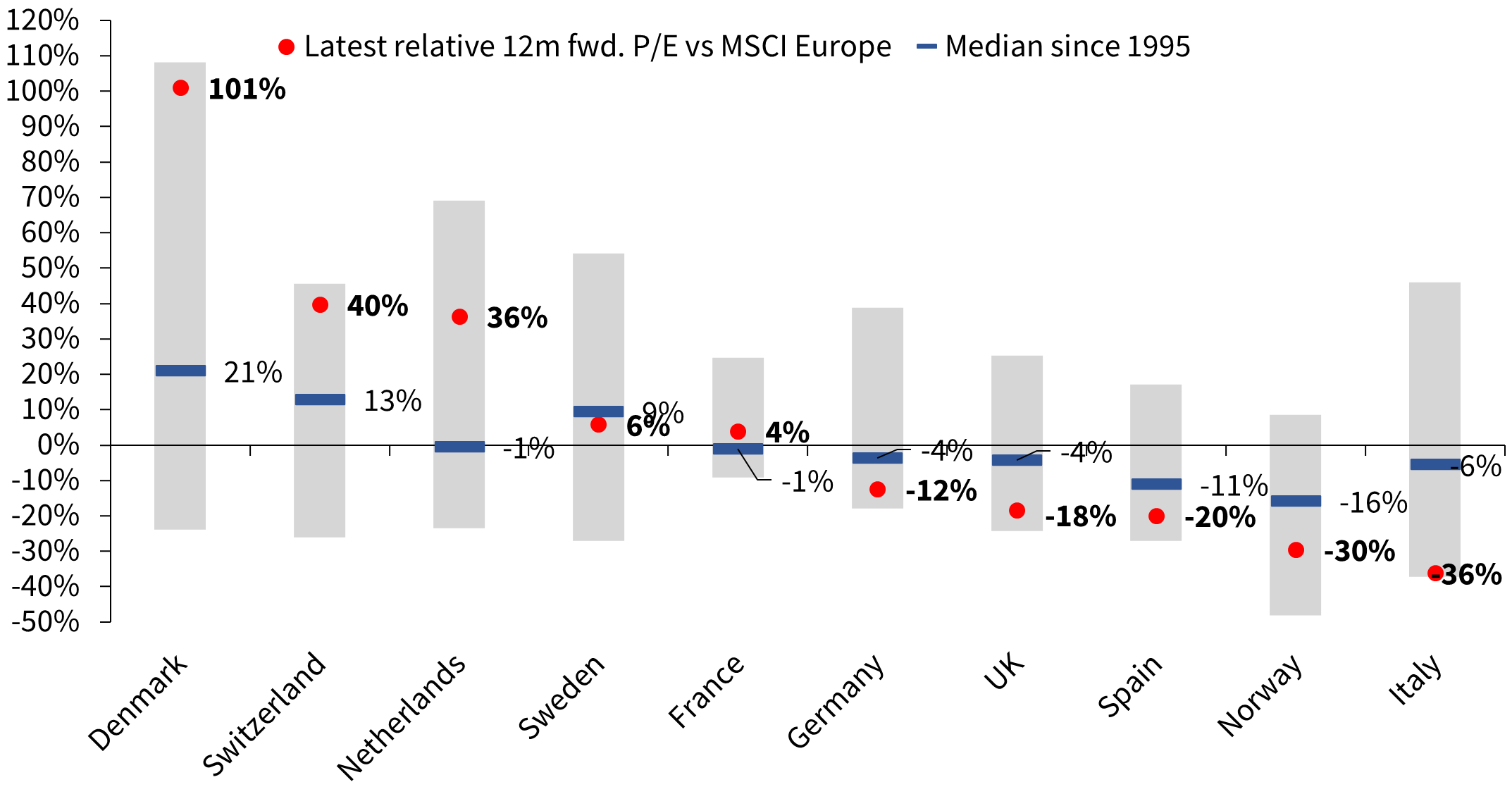

If we zoom in on Europe, the relative valuation for the various countries compared to MSCI Europe looks like below. For example, Denmark is valued a whopping 101% higher than MSCI Europe (Novo Nordisk), while Spain is valued 20% lower. Since 1995, Denmark has been valued 21% higher than MSCI Europe, while Spain has been valued 11% lower. Sweden is currently fairly on par with Europe, which also applies historically.

Source: Kepler Cheuvreux

In conclusion, the reporting season is now over, and we are likely entering a quieter period. We still do not have a strong idea of where the market is going, but right now the pain trade is pointing upwards, i.e., investors have too much cash and are being driven away from the market. The companies' ability to handle all challenges has undoubtedly been underestimated, the debt ceiling has been raised and in June we have interest rate announcements from the Fed, ECB, Bank of England and the Riksbank on June 29th. If either of them pauses, which the Fed seems likely to do, it could increase optimism and risk-taking (and vice versa). A seasonal pattern speaks against this, which usually means a weaker return during the summer months.

We put our focus in June on meetings with our companies as well as completing the analysis work with some new potentially interesting ideas.

We wish you a wonderful June with school graduations, student celebrations and not least midsummer!

Mikael & Team

Malmö on June 7th, 2023