Note that the information below describes the share class (I SEK), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class' return. The information below regarding returns therefore differs from the returns in other share classes.

Monthly Newsletter Coeli Absolute European Equity November 2021

November performance

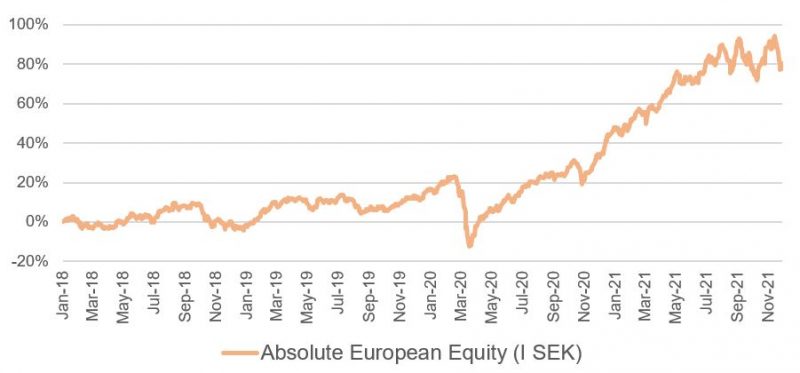

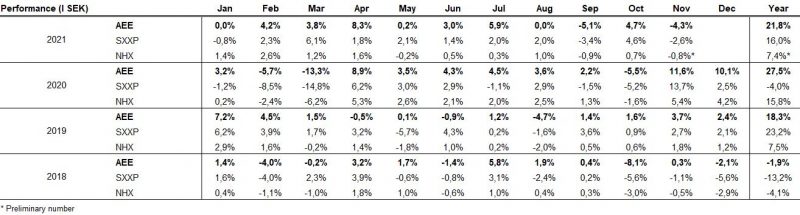

The fund's value decreased 4.3% in November (share class I SEK). The Stoxx600 (broad European index) decreased during the same period by 2.6% and HedgeNordic's NHX Equities fell provisionally by 0.8%. The corresponding figures for 2021 are an increase of +21.8% for the fund, +16.0% for Stoxx600 and +7.4% for NHX Equities.

EQUITY MARKETS / MACRO ENVIRONMENT

November was an unusually eventful month with Omicron, a new variant of the Covid virus, undoubtedly the event of the month. The broad European index returned -2.6% in November, while the S&P500 decreased by 0.8%. The fund had a weak return of 4.3% and we provide a detailed description of it in the summary section.

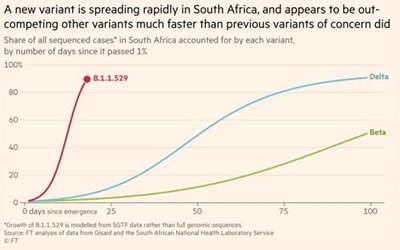

The Omicron variant was discovered in South Africa on Tuesday, November 23rd, and led to a sudden awakening on Friday the 26th of November. The belligerent headlines that hit investors around the world led to sharp price falls and we experienced the worst stock market day of the year so far.

Omicron was classified "as a worrying variant" by the WHO on November 26th, which has happened on four previous occasions. Alpha in the UK, beta from South Africa, gamma from Brazil and delta from India. With a clear disclaimer that we are not immunologists, we have read that Omicron displays 32 different spike protein mutations that the virus uses to enter the body. The delta variant showed nine different mutations. There are thus a very large number of mutations, which makes it difficult for the vaccine to achieve the desired efficacy. Nine of 32 mutations have been seen in other variants, eight have not been seen before and the rest are unknown. This is the reason why experts believe that there is a risk that this variant is more contagious and can get past the protection provided by vaccines or previous infections. Below shows the difference in how quickly the new variant spreads.

Source: Financial Times

It can be noted that the vaccination rate in South Africa is around 24%, so how it strikes in regions with a high vaccination rate is unknown. WHO also went out immediately and said that we should not overreact as we still have too few facts available to us. Over the weekend, the chairman of the South African Medicines Association also commented that the Omicron variant "is causing mild disease and no prominent symptoms". Let's hope so.

On the positive side, unlike other variants, Omicron can be detected by a simple PCR test, so the identification will be much faster than before. Those who understand this better than us believe that the most important thing for the near future is to follow the trend of hospitalization in the Gauteng province of South Africa where the outbreak took place. So far there has been no increase but, in a few weeks, we will know much more.

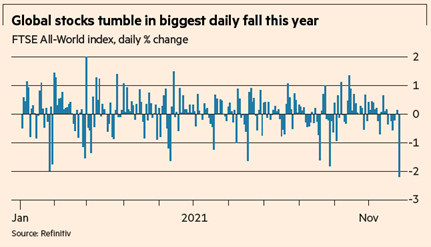

The combined led to sharp stock market falls on Friday the 26th of November and it was more than a year since we experienced something similar. It was also Thanksgiving in the USA, so the volumes were significantly thinner than usual which usually means larger movements in the market. Black Friday just got a new meaning.

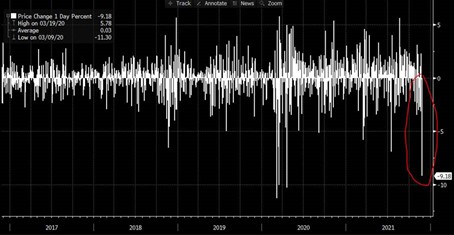

It was not just stocks that were under pressure. The price of oil fell by as much as 12% (!) in one day and the price of Bitcoin also fell by 8% (but this is not an unusual movement in the context of cryptocurrency). The picture below shows changes in oil prices in recent years. Circled is Friday's movement, which eventually ended up at -12%. This is the same magnitude that was experienced in March and April last year when everyone panicked, which feels like a real overreaction (despite being unusually humble here).

The demand for oil is about 100 million barrels per day. The decline in demand last year, when it was at its worst, was a modest 1 million barrels per day. It feels highly unlikely that the collapse in oil prices on Friday, when vaccinations have been running for almost a year, reflects a significant drop in demand. Rather, it is algos and speculators who pushed down the price considerably and as usual it will rise soon again. Does the same apply to shares in that case?

Source: Bloomberg

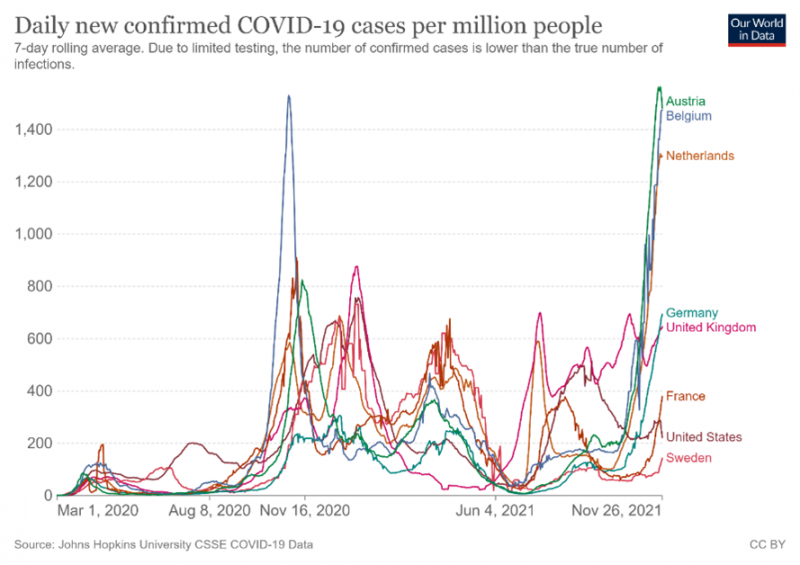

In the days before the Omicron news, the number of Covid cases in Europe had begun to rise. In some countries such as Austria, Belgium and the Netherlands, the rise was and is steep, see picture below. Austria, for example, has announced a lock-down from 22 November to 13 December. The Netherlands has a curfew in place between 17.00 and 05.00 for three weeks. So far, things are calm in Sweden.

The difference and gap in vaccination rates between areas with a higher level of education and more vulnerable areas is large in many countries in Europe. The gap in Europe is also significant. Several countries, including Sweden, have a vaccination rate of just over 80%, compared with low numbers in countries such as Bulgaria, Romania, Ukraine and Albania, which are at approximately 20-30%. The common dark political history is likely to contribute to people not trusting the state and elected representatives, thus ignoring the message about the importance of getting vaccinated.

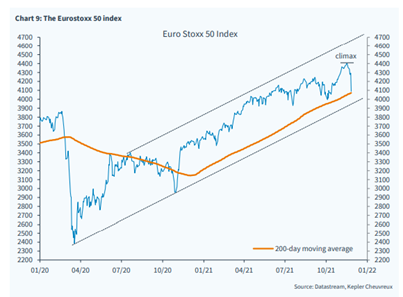

As customary nowadays, the shifts in market sentiment take place with ever higher speed and with ever greater force. The volatility index for Eurostox50 (important index in Europe) exploded when the Omicron news went over the wire. The price of our put options rose by just over 500% that day and that was one reason why we were down significantly less than the market that day.

Source: Bloomberg

It was interesting to note how different shares traded on Friday the 26th of November. Initially, everything was tanking, but already after an hour, the market had learned from last year which shares were Covid winners and losers, respectively. The picture below shows the relationship between value and growth shares on Friday, November 26. The magnitude is not far from November 9 last year, vaccine day, when Pfizer announced that the vaccine was ready. Fascinating!

Source: Bloomberg

Investor sentiment has moved very quickly from "greedy" to "fear".

In times of stress, our own Swedish krona behaves miserably. SEK decreased in value against the EUR by almost 5% in just a few weeks. This is a very large movement which has a negative effect on the fund's return as we do not hedge the shares we own, that are not euro denominated, such as our Swedish holdings.

Below is the development of the Swedish krona against the euro and it feels likely that it will recede soon (that the Swedish krona will strengthen). The tours in the Big Brother house, or the Riksdag as it is also called, have not improved the image of the Swedish krona as a safe haven (to put it mildly). The picture below indicates that foreign investors are moderately impressive of last week's political events.

Source: Bloomberg

To all those who point out how strong the Swedish stock market has been this year, we incline to agree, but only if we measure it in a small peripheral nomination unit called Swedish kronor. If we measure in USD, which should be done to understand how it is connected, it can be stated that the development on the OMX30 is relatively mediocre with only +8.4% return this year. Only a third compared to, for example, the S&P500.

Source: Bloomberg

The inflation ghost continued to elude the market in November. No one can be particularly surprised that inflation is rising, given that central banks and governments have pumped $10,000 billion into the world economy over the past 18 months (think one more time about how much money that is). Germany, among others, is now showing the highest inflation rate in decades. The history of hyperinflation in Germany in the 1920s has affected all subsequent generations' consumption behaviour, so the situation there is particularly anxious. In the 1920s, the large-scale war damages after the First World War were financed by reprinting banknotes. It was not a great success. This is also the reason why there has been a very negative attitude towards financing and supporting weaker European economies with loans and subsidies. But then came the pandemic and they felt compelled to participate, which Sweden also did for the first time.

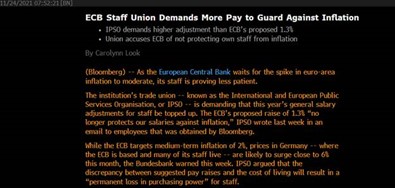

Even ECB staff demand higher wages due to rising inflation….

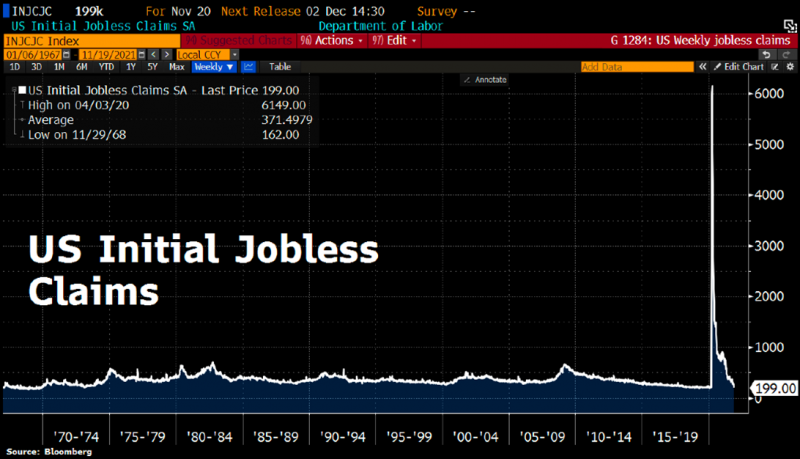

The US economy is under immense pressure and the latest labour market statistics show the lowest unemployment since November 1969! At the same time, we have an economic policy that continues to act as if there was a huge crisis in the system. It does not feel like clockwork but will probably benefit those of us who own fixed assets for many more years.

Again, we had to endure a shameful battle in the Swedish political sandbox and the gap between citizens and the elected representatives probably increased a few units to a new record level. The quality is so low and the only reason we address the events in this noble forum is that the undersigned needs to sign off for a therapeutic purpose. A bizarre chaos was aired in real time for the Swedish (and international) audience and it is a mockery to us voters who also pay their salaries. These are basically the same people who sit there year in and year out with high service fees. They are in no hurry as they, it seems, see it more as an employment and less as a platform to change society. The policies of substance are completely subordinate, everyone involved can clearly see that.

Source: Jeander

Even the sympathetic and low-key speaker of the house, Andreas Norlén, after the debacle last week, sharply criticized the Green Party for not having flagged in advance that they would leave the government if the government's budget did not go through. "I think the fact that the Riksdag elected a prime minister in the morning who resigns seven hours later seems incomprehensible to the Swedish people." Indeed. Some politicians, journalists and political scientists in the world's most anxious country began to criticize the speaker for his views on the action. The Green Party will probably have to bring its own coffee and cakes to the speaker next time they are to explore the terrain.

Source: Steget Efter

Although one can discuss whether reduced petrol tax is the right way forward, it was excellent pragmatism for 96% of the Swedish people when the consequence was that the Green Party resigned. From an environmental perspective, the abolition of Swedish nuclear power is worse than a reduction in petrol tax.

The influential magazine Forbes also tears apart the Green Party and its energy policy.

We change direction and visit Boris Johnson instead, who has had a lot to do lately. He describes with empathy about Peppa Pig. You can think what you want about him, but the entertainment value isoften top notch.

Not everyone was impressed by Deutsche Bank's upgrade by the rating institute.

There was a certain similarity between the market participants and the turkey that Friday morning, November 26th. The turkey spends its entire life being fed and cared for by its butcher. With each passing day that he is fed, love and self-confidence increase. When the risk is greatest, the love for the butcher is highest. Many market participants were also full of confidence when the news came (and to avoid any readers getting upset, no similarities otherwise).

Long positions

Truecaller

One of the joys of the month was, again, Truecaller. We note that Truecaller has now reached over 300 million active monthly users globally. An impressive figure for a Swedish tech company that has only been around for just over ten years. Following the IPO, analysts have now taken up coverage of the company with neutral or positive recommendations. Given that the price has roughly doubled since the first trading day, it is not very surprising that some analysts do not dare to recommend buying. However, we still see potential in the share, which rose 40% in November.

Lindab

The Lindab share rose 5% in November despite the price surge in October when the company released another report that beat expectations. The news in November consisted of insider buying from a board member, a partnership with SSAB regarding fossil-free steel and two acquisitions of the Danish ventilation company Klimatek and the Swedish roofing manufacturer Profilplåt. We are pleased to see that the company has increased the acquisition rate while at the same time there are many years left of attractive organic investment opportunities in the company. The price development for 2021 amounts to 73%.

CVS Group

In November the British veterinary company reported on the financial development from July to October, which was better than analysts had expected. It seems, though, that the market expected more than they got, and the share fell on the message. We struggled to understand the market reaction and bought more shares. For the foreseeable future, CVS will be able to increase the number of customer visits with rising margins, as the annual price increases are typically higher than the wage inflation for the employed veterinarians. In addition to this, there is an acquisition idea based on clear purchasing synergies. The share fell 12% in November but has risen 47% year-to-date.

Victoria

Our English flooring company, Victoria, also released good numbers in November. For the first half of the company's non-calendar fiscal year, sales grew by 31% on a comparable basis. The company has a long and successful acquisition history. The integration strategy is based on cost synergies particularly in purchasing, distribution and administration, while the company is keen to maintain a decentralized organizational structure. During the year, five acquisitions were made, which together increase operating profit before depreciation by approximately £64 million. The share rose 11% in November and has risen 80% in 2021.

Surgical Science

The precision in the company building Surgical Science has impressed us for a long time. The management has in the right order acquired the companies required to achieve the current monopoly position in the market in surgical simulation. During the month, a report was released that beat the preliminary predictions from the few analysts who cover the company. Sales grew by 36% on a comparable basis, to an operating margin of an impressive 31%. The integration with the major acquisition of Simbionix is going well and the CEO's note had an excited tone to it. The share rose 14% in November and has risen 212% in 2021. Surgical Science is so far the fund's best investment measured in rate of return. The block of shares we bought about three years ago from an aggressive seller has now risen approximately 20x. In more explicit terms: that purchase of roughly SEK 6 million plus now holds a value of approximately SEK 125 million. During the journey, we traded in and out but we still own the vast majority of shares. It should also be noted that when the company made its IPO in 2017, the market capitalization was 170 million. Now it is around 15 billion. Hats off and credit to everyone at the company for a phenomenal work. We also take this opportunity to send greetings to our network who chased us up and told us about the block that was for sale. Thanks!

Evolution

For a long time, we have held a medium-sized position in Evolution, which has served the fund well. In November, however, the share fell sharply due to anonymous accusations which, among other things, implied that Evolution operates in blacklisted countries. A lot has been written about developments in Evolution on various forums and news sites. We think that Evolution's written response to the allegations was good, but the subsequent conference call with analysts was not structured in the right way and did not reflect the confidence that the market was seeking. The share fell 32% in November and has risen 14% in 2021.

Atai

American Atai is one of the fund's major contributors this year, as we owned shares when it was unlisted thus received a substantial appreciation in connection with the stock exchange listing this summer. Unfortunately, the share hasn’t fared as well as expected in the public environment. The share now stands at about USD11, which should be compared with the subscription price of USD15. November was also a bad month for Atai as the price fell by 25%. We and other co-investors who have been with Atai for a long time entered into a lock-up in connection with the stock exchange listing, which expires in December. It is possible that the market has anticipated that this may give a certain sales pressure, which may have had an impact on the weak price development in recent times.

Knaus Tabbert

2021 has been a really tough year for our German motorhome manufacturer Knaus Tabbert, who has struggled with huge supply problems. As is well known, there is nothing wrong with the demand for the company's products - on the contrary, it is at record high levels. Unfortunately, it is difficult to sell motorhomes when there are not enough parts to build them. In November, the company was again forced to lower its full-year forecast. We can admit that we made a mistake with regards to the timing of our investment in Knaus Tabbert, but we still believe in the company long term. The share fell 19% in November and has decreased by 19% for the full year.

ISS

In November, the cleaning and catering company released a financial update in which the financial forecast for the full year was raised (and thus exceeded analysts' expectations for 2021). It is clear to us that the company under new management has always taken steps in the right direction. Unfortunately, these facts were overshadowed in November by fears of the new corona variant. More restrictions and closures of communities do not benefit ISS, whose share fell by 8% in November. We note that CEO Jacob Aarup Andersen bought shares towards the end of the month.

Blackrock Neurotech

During the month we made a new investment in an unlisted company, Blackrock Neurotech. The company develops technology for interfaces between the brain and computers and is the most advanced brain-computer interface (BCI) company in the world. This undeniably feels like science fiction, but the fact is that the company has successful studies behind it. With the help of our network we have the opportunity to be early investors, together with Christian Angermayer and Peter Thiel. Our allocation was almost 10 percent of the transaction. Those interested can read about Blackrock and Peter Thiel’s investment in this article.

Shortly after we invested, Blackrock received a so-called "Breakthrough Designation" from the FDA for its product "MoveAgain". The system is intended to help patients without mobility to control, for example, a computer mouse, mobile phone or wheelchair by just thinking. If everything goes according to plan, Blackrock hopes to be able to launch the product in 2022. Those interested can view this video or why not the website.

Source: Blackrock Neurotech

Bullish

Our unlisted holding in Bullish, which is a cryptocurrency technology company, is preparing for its listing and we estimate that this will happen at the beginning of next year. We follow the project with great interest. Link with new updated presentation for those who are interested.

Short positions

The short portfolio contributed with a positive result during the month. Our short term position in the broad Swedish OMXS30 had the largest contribution. Some share specific short positions that contributed positively to the result were Swedish Dometic, Dutch JDE Peet's and Danish Carlsberg.

Exposure

The net exposure, adjusted for our unlisted holdings, at the beginning and end of the month was 70 and 71%, respectively.

Summary

November was a frustrating month. The fund was negatively affected by weak price developments in several of our companies as well as unusually volatile and falling stock markets. In some cases, there were explanations for the declines as in Evolution and Photocure (although Q3 results with a small miss should not result in a 17% decline). In most cases there were no specific company news, as for ISS, Wincanton and Pebble.

Although share prices have been weak in several areas, most of our companies have delivered strong results and positive outlook. Continued positive price movement for Truecaller and Surgical Science was not enough to compensate for the others. The five largest negative contributors to the fund during the month were Photocure, Knaus, Evolution, Atai and CVS Group, which together lost more than the fund's total negative results for the month. In addition, the fund's return decreased nearly one percentage point due to the weakening of the Swedish krona.

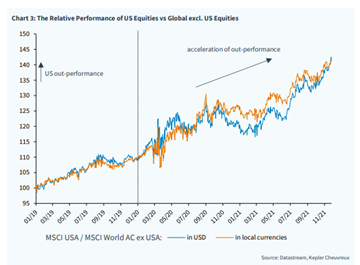

European equities as a collective showed a weak development in November and the various European indices were a few percentage points worse than their American counterparts. The main explanation is that demand for technology stocks increases when interest rates fall and there is significantly more of that in the US, compared to Europe which has more bank and cyclical stocks.

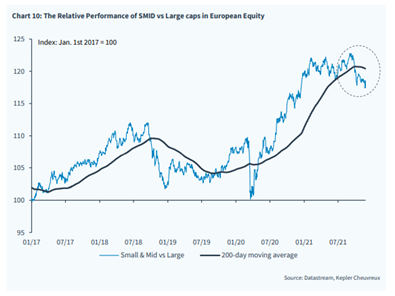

If we look at European companies by size we can see that small-caps continue to have a weaker development compared to large-caps. Right now the fund is not benefiting from that development, but it will probably change at some future price level; it is unclear when.

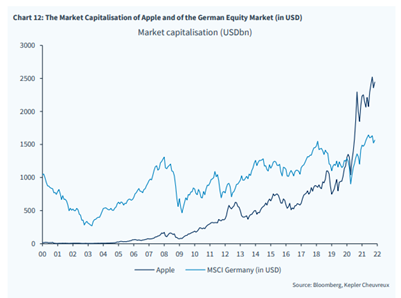

The lack of technology companies is noticeable in Europe and perhaps most in Europe's engine, Germany, which has undoubtedly lost some economic power in recent years. Below is the market value of Apple compared to the entire German stock market, which includes VW, Daimler, BMW, Bayer, BASF and Siemens to name a few.

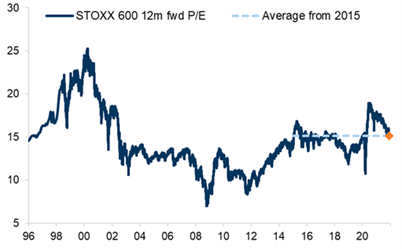

Values in Europe have come down after last week's falling prices and now indicate modest P/E 15x 2023e.

Source: Goldman Sachs

Compared with the historical valuation of the last 25 years, we are now at average levels. A big difference from before is that we have extremely low interest rates.

Source: Goldman Sachs

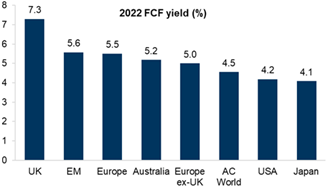

If you study the cash flow for each geographical market, Europe also excels here. The United Kingdom has the highest cash flow, which is one of the reasons why we have allocated almost 25 percent of the fund's capital there.

Source: Goldman Sachs

European profit estimates have been adjusted upwards to highest levels (unusual). Analysts have thus been lagging the development for a whole year, which probably indicates continued upward adjustments. A big question mark now; however, is how much the new virus variant will hinder economic development in the future.

All in all, there has been an unusual amount of noise in recent weeks and in the end, it became too much for the market, despite a very strong reporting period.

So what do we think about future developments? It can be stated that events and flow of information spread at a very high speed, which leads to ever faster trading and increasingly sharp throws in the world's stock markets. Algorithms and computer-controlled strategies, together with a record share of passive capital, are increasingly determining the stock market mood in the short term.

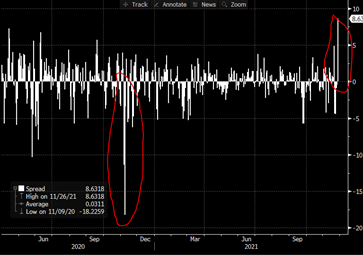

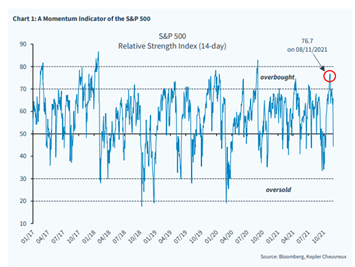

In just over a week, the market climate has changed from a record low volatility to suddenly showing the largest rise in the VIX index this year. The picture below clearly shows the latest sharp throw in sentiment. The picture gives the impression that there is a limited downside before a new turning point occurs in the market.

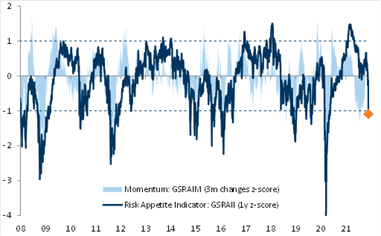

Illustrated in another way, Goldman Sachs' risk appetite indicator is showing the lowest levels since the crisis last spring. Again, the tighter the bow is tensioned, the stronger the reversals tend to be (however, this did not apply in 2008 when the reversal didn’t happen for a long period, which the undersigned experienced painfully).

Source: Goldman Sachs

The market has been out of balance since last year with an extreme monetary policy despite a boom of unseen proportions. The inflationary pressure is of course reaching new heights with that cocktail, but central banks claim (with the stubbornness of a fool?) that inflation is transient. It is becoming increasingly difficult for them to back down and as a collective they have basically painted themselves into a corner. All other central bank governors piggy back on the Fed, it will be easier then if you are wrong. "Madam Inflation", ECB President Christine Lagarde, has been repeating the Fed's message for a long time now. And a few weeks ago, it was topped by our own Governor of the Riksbank who communicated that he does not foresee any interest rate increases until 2024!

As I am writing this on the evening of November 30, Fed chief Powell has communicated to the market that he may have to bring forward the dismantling of the extreme policy by a few months as inflation may be more "sticky" than previously thought. The US stock market immediately fell about 2% on the news. This is the first time that one can discern a certain change in the denial that we have inflation in the system.

To further fuel the imbalances the United States has a leadership that, in an extremely strong economic environment, pushes through gigantic infrastructure investments to further stimulate the economy. In Europe, old rules on budget deficits and financial discipline have been completely abandoned. Instead, they borrow gigantic sums that will stimulate, above all, the countries in southern Europe. In both the United States and Europe, a large part of the population has been enormously enriched while a large part of the population, those who do not own assets, receive subsidies from the leaders to avoid too much criticism. That development will also not stop where we are today, but the differences will increase further. The EU has become a debt and transfer union.

Finally, it can be stated that there has historically been turbulence when there have been significant negative real interest rates, which we have now. Companies tend to make less talented investments when they get paid to implement them and politicians allocate capital to projects that do not add much value. With inflation now at around 5%, real interest rates are sharply negative, but at least that reduces the debt pressure (is that perhaps the agenda?) Overall, it is not a bold guess that volatility will increase next year, at least during the second half year. But it also creates opportunities.

In conclusion and in the short term, we have quickly ended up in a nearly oversold position in the world's stock markets. No information on viruses and vaccines from the major pharmaceutical companies will probably be presented until about two weeks from now. In addition, several important central banks will have meetings in December, and new information is likely to be issued that will affect the financial markets.

Our best guess is that we trade around today's levels until we have new substantial data on Omicron. The outcome of course determines the direction, but we guess that the most likely scenario is that the risk appetite will increase again. A joker from the deck is a clumsy politician who wants to demonstrate real action and shut down societies.

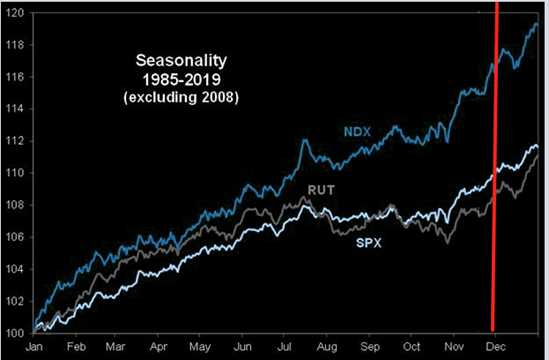

We end with Goldman Sachs' excellent picture that shows how the market has developed yearly over the past 36 years. If we are to follow the typical pattern, a final rise will soon begin this year.

We thank you all for your interest and wish you a very Merry Christmas!

Mikael & Team

Malmö December 6th