Note that the information below describes the share class (I SEK), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class' return. The information below regarding returns therefore differs from the returns in other share classes.

Before making any final investment decisions, please read the prospectus, its Annual Report, and the KIID of the relevant Sub-Fund here

This material is marketing communication

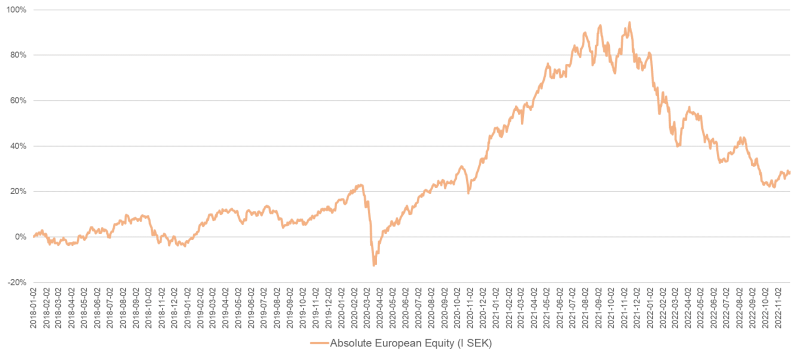

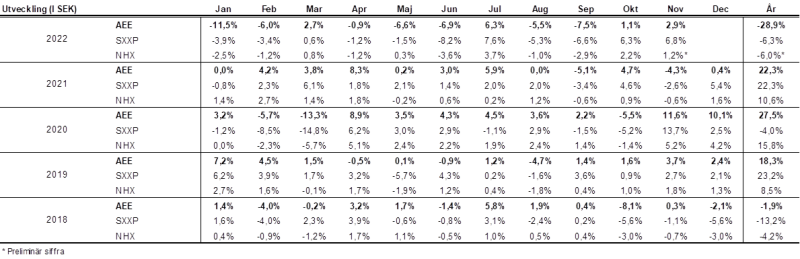

Monthly Newsletter Coeli Absolute European Equity – November2022

NOVEMBER PERFORMANCE

The fund’s value increased by 2.9% in November (share class I SEK). The Stoxx600 (broad European index) increased during the same period by 6.8% and HedgeNordic’s NHX Equities increased provisionally by 1.2%. The corresponding figures for 2022 are a decrease of 28.9% for the fund, -6.3% for the Stoxx600 and -6.0% for NHX Equities.

EQUITY MARKETS / MACRO ENVIRONMENT

The positive trend that began in mid-October continued in November. The Fed raised the key interest rate at the beginning of the month by 75 basis points, fully in line with expectations. At the press conference afterwards, central banker Powell had an unexpectedly hawkish tone, which caused the risk appetite, once again, to collapse. The sentence from Powell that lowered the stock market was "incoming data since our last meeting suggests that the ultimate level of interest rates will be higher than previously expected".

In the week after November 10th, all the world's financial eyes were on the US inflation data and for the first time in a long time the deviation was in the positive direction. Inflation on an annual basis came in at 6.3% against the expected 6.5%. This triggered huge relief among investors and the world's stock markets rose sharply while interest rates fell significantly. The Nasdaq stock exchange was the biggest winner, climbing by a whopping 7.5% that day!

Below is Nasdaq's development during November. Note the movements on November 2nd, November 10th and November 30th when inflation decreased and the economy in terms of GDP numbers was stronger than expected.

Source: Bloomberg

The above events have increased the likelihood that the US economy will escape a recession. Expectations for the Fed's next rate hike in December also fell from another 75 basis point increase to 50 basis points. The US dollar weakened sharply, completely according to the textbook and that drove the risk appetite even further. Below is a year's development for the US ten-year interest rate.

Source: Bloomberg

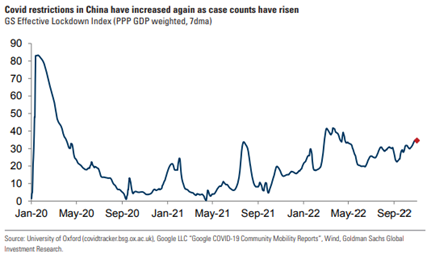

Around November 10th, there was also news from China that more lenient quarantine rules would be implemented which further contributed to increased risk appetite. For several years China's economy has had a weak development, much due to its extreme covid policy. Companies with exposure to China rose sharply. A new investment for the fund, the Finnish elevator manufacturer, Kone, with significant operations in China, was one of those companies that strongly performed those days.

At the end of November, unusual footage of citizens' wild protests against the country's harsh lockdowns was released. After almost three years in extreme hard lock-down, the line has been crossed for many and to us outsiders it seems undoubtedly insane. China's self-produced vaccine works poorly compared to that of the Western world. At the same time, the country refuses to buy foreign vaccines as it would have been a political defeat. Now it is speculated that a victorious exit from covid will soon be declared, where they will emphasize how harmless the infection has become. Below Chinese infection numbers.

The third major event this month was President Joe Biden meeting Chinese President Xi Jinping at the G20 meeting in Bali on November 15-16. It was the first meeting between them and even if the relations are not significantly better after the meeting than before, it can still be considered positive that they meet given the elevated tones that have been heard recently.

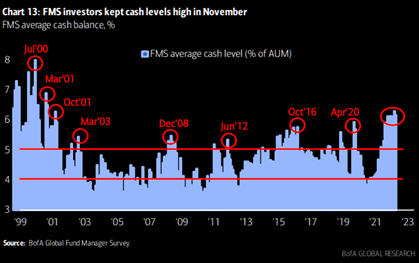

All in all, Thursday, November 10th provided large amounts of fuel to the world's stock markets, while the share of cash held by the investor collective remained very high and investors were generally very depressed. There was also a strong sector rotation where previous winning stocks were sold, and losers were bought (simplified). The following two weeks saw massive buying actions covering short positions and driving share prices. Rarely have so many short positions been closed (bought) in a two-week period (according to Goldman Sachs). That says a lot about how cautiously positioned the market was. The image below shows the share of cash some way into November.

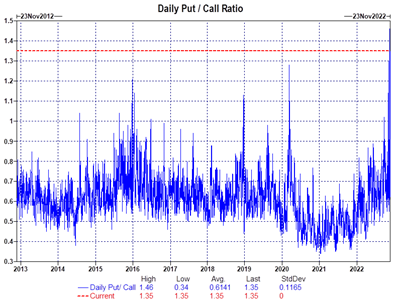

The image below is from November 24th and shows that investors continued to buy significantly more puts than calls. The positioning has been easy with a negative market view which in the short term was completely wrong as the stock market stubbornly continued to rise, volatility fell, and the option value quickly eroded. Undoubtedly, the pain trade is still on the rise. Many managers have thrown in the towel for 2022 and there is some stress in the system regarding index levels creeping upwards.

Source: Goldman Sachs

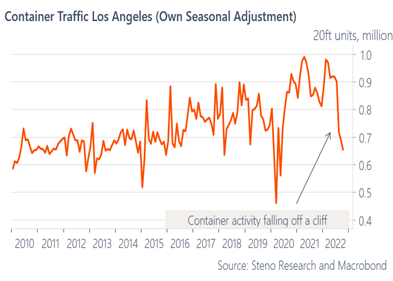

Economic activity is now slowing as interest rate increases from the world's central banks take hold. The slowdown has different effects, but simply put, the consumer is at the forefront of increased interest and energy costs, as well as general cost inflation. The reverse applied almost three years ago when Covid struck. Then the crisis hit some companies hard, while the consumer experienced unusually good conditions with subsidies and savings that soared.

Below is one of many examples that show a sharp slowdown in activity. Container traffic in Los Angeles port falling steeply.

Turbulent! A few months ago, the German producer price index showed the largest monthly increase on record, which was followed by the largest monthly decrease on record.

Source: Bloomberg, Societe Generale

Clear signs of declining inflation have led the world's central banks to indicate in recent weeks that they are now likely to enter a softer phase with interest rate increases. It is completely in line with our expectations. The risk that central banks around the world will break the economy has decreased in recent weeks, which has contributed to the rise in the world's stock markets. It is not unlikely that the Fed's last rate hike will be the one that comes on December 14th (not consensus).

Significant improvements in world bottlenecks also reduce cost pressures. If only China opens up too, it will be even better. When China picks up the pace, the price of oil will likely rise, which in turn will drive inflation.

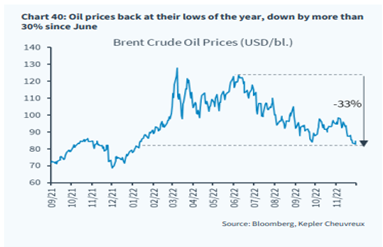

Oil prices are now around annual lows and lower than they were before Russia attacked Ukraine.

Despite all the challenges, the supply of various groceries has been surprisingly good, which has contributed to falling prices in recent months.

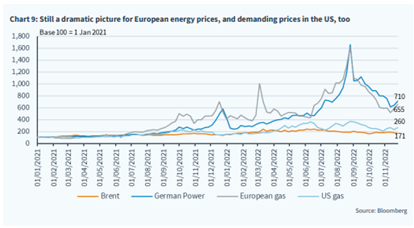

What continues to plague Europe are energy prices and that is on our naive politicians. It doesn't feel right when ECB chief Christine Lagarde is hoping for a warm and windy winter so that energy prices don't rise too much and key interest rates must be increased further. It feels somewhat blunt, very diplomatically put. The anger of the population is palpable and in order to remain in their well-paid positions, the politicians are now busy paying out various subsidies so that people can afford to pay their electricity bills. That in itself drives the inflation that central banks are fighting against. Professor John Hassler at Stockholm University makes the assessment that the various proposals for electricity price subsidies that have been discussed in Sweden have led to an extra 25 basis points increase in the policy rate. It's like a vicious circle reference in an excel model.

In the past few days, a report from the European system operators' cooperation organization was released which stated that Southern Sweden, electricity area 4, has the least installed electricity production capacity in relation to expected maximum use among all 50 European electricity areas! The impressive own goal is entirely self-inflicted, and the achievement has been in the making for a few years. One wonders what evil the population has done to deserve such mediocre political decisions that led to such extremely serious consequences? The new government does not impress either and has had a shaky start with diffuse deliveries of clear election promises.

The difference between the American 10-year-old and 2-year-old is now down to negative levels (below zero, far right), which has not happened at any time during the 2000s. It clearly signals a serious slowdown in the economy, and the relationship is usually an accurate indicator.

Source: Bloomberg

The Bank of England stated that Brexit is complicit in the high levels of inflation in the country, which in turn created a deficit in the labor supply and weakened the economy. Britain's growth potential has lagged all major economies except Mexico due to a collapse in productivity and major problems with a limited labor supply. The absence of the lost empire contributed to probably the worst political decision in Europe in the last 50 years.

In an attempt to lighten the mood, we recommend watching the following clip. A rebuttal from Nigel Farage, a fanatical Brexit supporter and instrumental in the entire political process.

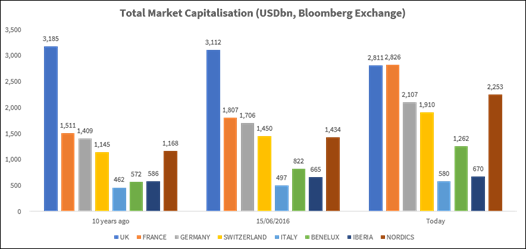

Another strong indicator of Britain's gradually reduced importance in the world is the image below. In just a few years, it has lost a superior lead in total market capitalization compared to other European countries. After all, the pound is (together with another currency) the worst currency in the Western world this year. The other currency is of course the Swedish krona. That has greatly contributed to the fact that the traffic over the Öresund Bridge (connecting Sweden and Denmark) is now back at levels from autumn 2019, which is very gratifying. However, it is mostly traffic from Denmark, as the Malmö/Lund region has turned into one big one-pound-land for Danes.

Source: Bloomberg

If you have the slightest interest in politics the below interview with the loyal former Vice President, Mike Pence, interviewed by ABC News is recommended. The interview was released in mid-November, the day before Donald Trump announced that he will run for president in 2024 (no coincidence). It is the first interview Pence has given since the storming of the Capitol on January 6th, 2021. According to Pence, the president acted ruthlessly towards him, his family and everyone else who was there that day because he was completely passive. It is a shocking interview and completely unimaginable that it could happen in the world's most powerful democracy. Donald Trump himself had the worst imaginable start to his announcement that he will aim for the presidency. Never count him out though.

Long positions

Accelleron

During October and November, we bought shares in the Swiss company Accelleron. The company was spun off from ABB as recently as October and sells turbochargers for large engines in the marine and energy segments. Every year, Accelleron delivers around 10,000 new turbochargers. Product revenue (which comes from the actual turbochargers) makes up about 25% of sales, while more stable aftermarket revenue (maintenance/service and spare parts sales) accounts for the remainder.

Because the revenue mix is so heavily weighted toward the aftermarket, Accelleron should have relatively stable revenue even in a recession scenario. Despite spending around seven percent of revenue on research and development, the company should be able to manage with an operating margin of around 25%. Combined with good capital efficiency, the return on capital employed is around 35%. The weak point in the investment case is the growth, which is not expected to be much higher than 2–4% per year (at profit level). However, it is more than compensated by the low valuation of around 9x operating profit, which can be considered very attractive.

In connection with the company being spun off, we saw an opportunistic opportunity to buy the shares at a discount. Since Accelleron is Swiss with a small market capitalization in relation to ABB's, there were probably many ABB owners (such as Sweden funds) who, due to fund restrictions and other reasons, did not want and/or were able to own Accelleron shares. This created initial selling pressure which we used to purchase our first shares. Since then, the stock has recovered. In November, the share rose by 13%.

4imprint

The best stock of the month is called 4imprint, which rose 22%. In our August letter we wrote about the company, which in many ways has an American operation even though the stock is listed in London. In short, the business is about distributing giveaways, i.e., items that are often given away as gifts for marketing purposes. Since we last wrote about the company, management has once again upgraded its outlook for the full year. Despite the share rising by roughly 50% this year, the company is still valued at 13-14x operating profit, which we think is attractive.

LVMH

Since the start of the fund almost five years ago, we have owned the luxury conglomerate LVMH on and off. This month was especially prosperous after there were increasing indications that China may be softening its hard-line post-pandemic stance. However, the news flow on this has been extremely ambiguous, with luminaries speaking in favour of an easing one day, followed by the opposite the next. Regardless, LVMH benefits if the Chinese consumer can come back to a greater extent. The stock rose 15%in November and is now trading around its highest level. With a market capitalization of 360 billion euros (roughly half of Sweden's GDP), it is undoubtedly one of the world's most successful companies. When Bernard Arnault started the business in 1987, the market capitalization was 500 million euros. Below is a picture of the course development over the past five years.

Source: Bloomberg

Wincanton

In November, our British logistics company Wincanton reiterated that it believes it will meet analysts' expectations for the full year. We think that is very good, given that expectations have been at the same high level all year despite the gradual worsening of the macroeconomic climate. Next year, there is a possible trigger in that the company's large pension debt will be reassessed. This will probably mean that Wincanton can reduce its provisions for the pension liability drastically (possibly completely), which will give the company a completely different cash flow profile.

ISS

One of our top stocks for 2022 is ISS. As of the end of November, the stock had risen 23% during the year and 12% for the month in isolation. In November, ISS held a capital market day where it announced its goal of growing by 4-6% annually, to an operating margin of five percent. As we mentioned briefly in the previous monthly letter the company also came out with a nice trading update at the beginning of the month which, in combination with a positive stock, caused the share to rise. Throughout the year, ISS has been one of the fund's largest positions and for long periods of time the largest. Below is a picture of this year's price development.

Source: Bloomberg

Pets at Home

One of our weaker stocks in November is Pets at Home, which fell 9%. Although the company's half-year report, released during the month (for the financial year ending in March), reiterated the forecast for the full year we guess that the result as such caused the market to question whether management can achieve what it has communicated. After several days of analysis, we feel confident that the company will do exactly this, and for that reason we have also taken advantage of the situation and increased our position by almost 50%.

Rugvista

Rugvista released their report during November. The stock has had a tough journey on the stock market this year, like many other consumer companies. Sales were in line with Carnegie's expectations, while operating profit came in just over 130% better, largely thanks to more effective marketing. The conversion rate (the number of website visitors who place an order) also improved significantly in the quarter. We continue to like Rugvista and increased our position following the report. The stock rose 22% during November, and as of today has risen roughly 60% in five weeks.

Teleperformance

Biggest disappointment for the month was Teleperformance, our (former) French holding that is in the business of outsourcing customer support and a range of related services. We had reduced our position ahead of the company's Q3 update, which was positive and in line with market expectations. Shortly afterwards, information was published by a newspaper which stated that the company did not treat its staff in Colombia well. We judged the company's response to the accusations to be inadequate. Since we could no longer form a good idea of risk versus return, we chose to sell the holding at a loss. The stock fell 21% in November.

Short positions

The short portfolio contributed with a negative result during the month. The largest negative contribution come from our short positions in a Swedish small company index and in the larger Swedish OMXS30 index.

Exposure

The net exposure, adjusted for our unlisted holdings, at the beginning and end of the month was 76% and 79% respectively.

Summary

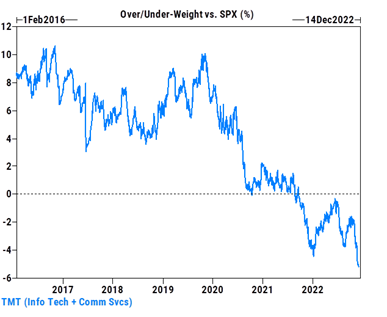

As expected, performance for November was positive and the fourth quarter is so far the third strongest quarter for the European stock markets in 30 years! The Nasdaq, which developed weaker than several benchmark indices, closed at +5.5%. The entire rise basically came on the last day of November as the big technology companies like Amazon, Google and Meta have been under pressure for a long time. The market value of these three companies now corresponds to the total value of Apple.

That development is also reflected in the fact that Goldman Sachs' hedge fund clients are now underweight the major technology companies by roughly 5% in relation to the S&P500. The biggest underweight since tracking began of the positioning in 2016.

Source: Goldman Sachs

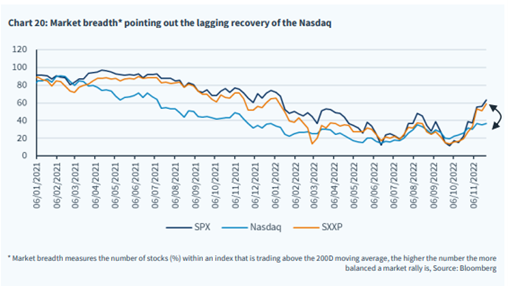

It is also clearly visible in the image below which shows the market breadth measuring the proportion of stocks that trade above the 200-day rolling average. Nasdaq lags Europe and the S&P500. The higher the number, market breadth, the more balanced/credible the rise in the market. The rise now therefore looks considerably more credible than in August. We also note that November offered by far the highest activity of the year in ABOs (Accelerated Bookbuilding Offerings) with a total of USD 25 billion from companies such as Pernod, Air France and Swedish Catena.

The reporting season is over, and the year is coming to an end. The general impression is that the companies have so far withstood the situation well, often maintaining profitability despite all the problems. Geopolitically the world is still in a dangerous situation, but at least it hasn't gotten worse. Europe has been a positive surprise in terms of unity towards Russia, which is gratifying. Bottleneck problems are gradually decreasing, the food supply is working better than feared six months ago and we now have, at least in the US, falling inflation. That pushes interest rates down and the USD has also lost value, which is positive. The picture below shows that the euro has strengthened by 7-8% against the dollar in the past month.

Source: Bloomberg

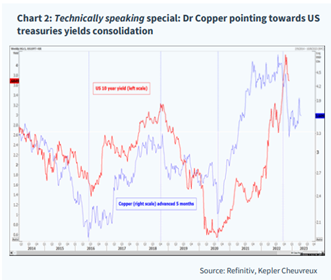

The price of copper, a strong indicator of the global economy at large, indicates that US interest rates are now set to consolidate (which they already appear to be doing).

At the end of November, the Financial Times had a large article in which leaders of the leading European companies stated that they had been too pessimistic in the last six months. The outcome so far has been better than feared. All of this together has of course contributed to the strong development during October and November. The recent rally has created some pain for investors who had too much cash, too defensive portfolio and short positions that developed very strongly in a short period of time.

The US companies have massive buyback programs underway that are roughly double historical levels, and $10 billion worth of shares a day are being bought back. Systematic funds, non-fundamental and trend-following, have also picked up and bought a lot of stocks in recent weeks.

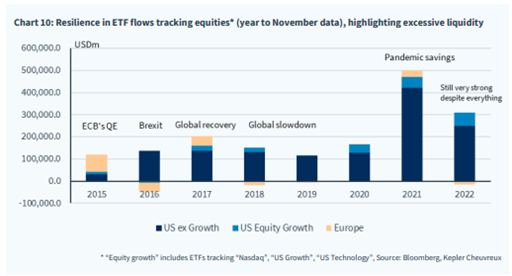

The inflow into equity funds has been a positive surprise. The image below shows inflows to various ETFs. Admittedly lower than the record year 2021, but about double compared to 2020. Pain trade is still on the rise.

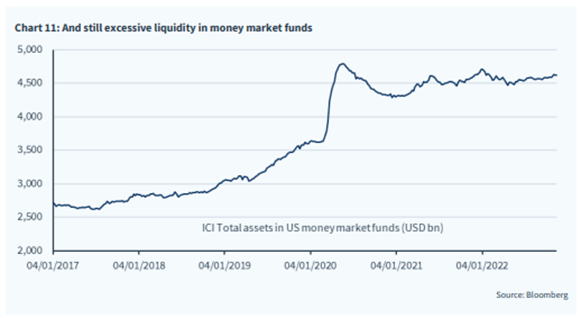

There is more liquidity to draw from. Continued record levels in US money market funds.

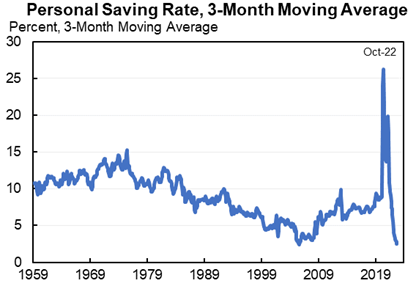

But in the real economy, it will get worse before it gets better. Below is the US household savings ratio since 1959. An unprecedented total crash and after paying $23 for an espresso in New York last week, it's understandable.

Source: Goldman Sachs

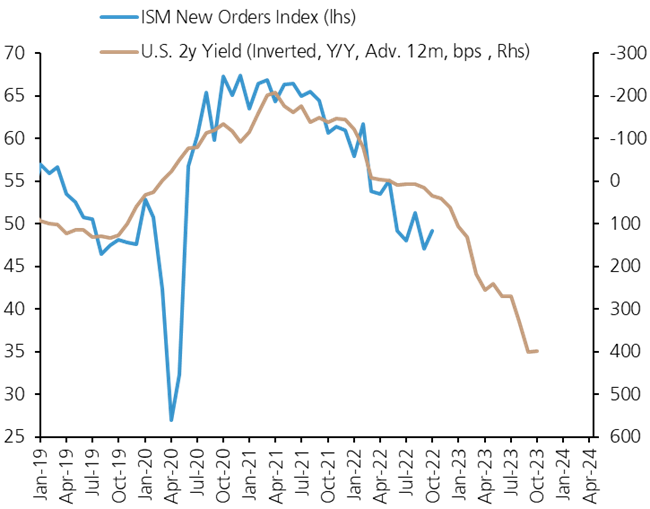

The inverted US two-year interest rate signals a continued sharp decline in economic activity.

Source: UBS

We assess that the recent rise is still considered a bear market rally by consensus, and we will go down to old (or new) lows again. This is because the downward adjustments of the profits must go down further and that the central banks will continue to raise interest rates.

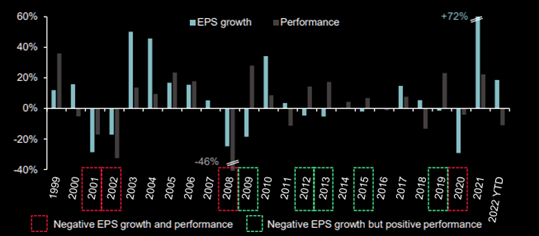

Rarely has a downturn in the economy been as expected as now. As everyone knows, the stock market is not in the real economy here and now, but rather 6-9 months into the future. The image below shows that it is entirely possible for the stock market to give a positive return despite falling earnings. Those of you who were there in 2009 will remember that, for example, cyclical shares gave a very strong return. It was really shaky in March 2009 when the stock market started its recovery.

bild 26

Source: Societe Generale

The image below shows that, based on historical data, the stock market begins to accelerate six months before the economy turns around, that is, at the same time that profit estimates are still being dialled down. It is clear that the declining phase in the economy has begun, and the debate is now when it can turn up again.

Source: Goldman Sachs

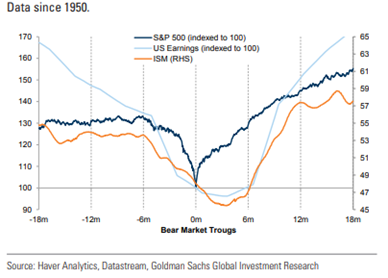

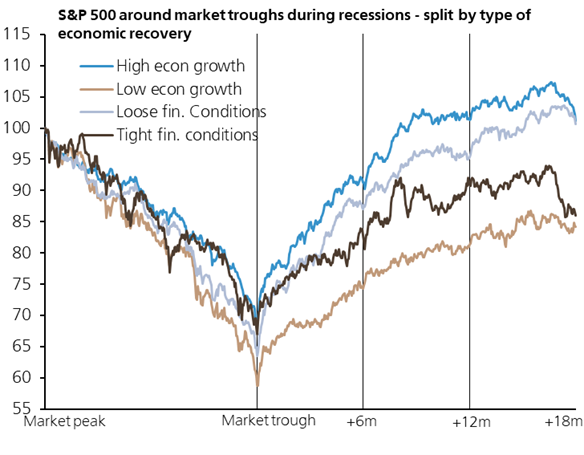

Below is a picture illustrating the historical returns after the market bottomed out in various economic recoveries. We guess that we will be in a lower economic growth phase when the economy recovers.

Source: UBS

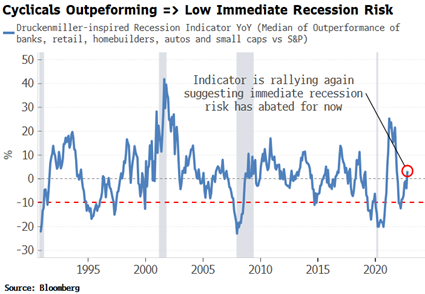

The market is surprisingly often right and in recent months banks, trading companies, construction companies, cars and small companies have had a stronger performance than the large broad indexes. It signals that the market's concern about a recession has diminished.

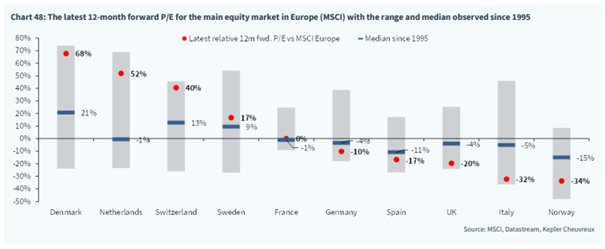

Below is the valuation level for the major stock markets. Denmark is at the highest level driven by Novo Nordisk, which weighs heavily in the index, and which has had a strong year behind it. Sweden is around the median value and Great Britain far below. Italy has its constant political problems. The US, which is not visible in the picture, is traded at around 18x earnings against the median value around 15x, clearly above and a factor that makes us significantly more positive about Europe's stock markets ahead of 2023 than the US's. The average for Europe at the time of writing is around 12x earnings.

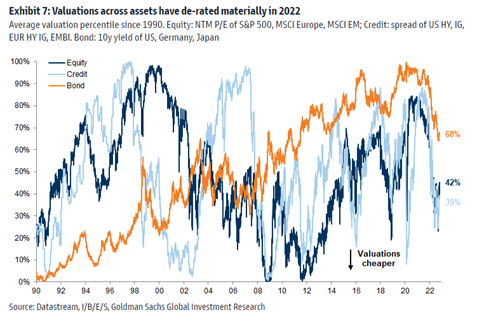

Below clearly shows the valuation difference between the US and Europe and the strong multiple contraction that took place during the year.

TINA (There Is No Alternative) has been in effect for several years. But not anymore. The image below shows the difference between the US one-year yield and the earnings yield for the S&P500. In Europe, the picture is totally different as the corresponding figure is just under 6%and one of the reasons why we favour Europe over the US now.

Source: Bloomberg, Goldman Sachs

Smaller and medium-sized companies are Europe's equivalent of growth stocks. After a miserable 2022 with a very weak price development for many smaller companies, that asset class has now started to perform better than the broad indices. For us, Lindab is a perfect example where the share has had a strong development in recent weeks. This year's decline is still a whopping 60%.

There is a lot that suggests that smaller companies will have a more favourable development in the coming year:

- In many cases, a very weak price trend in 2022. Lack of liquidity has punished many shares severely. It should be reversable in the next year

- Small companies have stronger growth over time

- They are more often the subject of takeovers and there is plenty of mispricing

- In the US, small companies are now traded at a record discount compared to larger companies.

- Smaller companies' excess returns have historically started in a recession

In addition to the above points, it can be stated that small companies in relation to large companies have had a strong period in recent weeks. Cyclical companies have also had this compared to more defensive ones. This coincides with a falling USD and strengthening euro. Inflation in the US, which is likely to have peaked, will also result in further falling interest rates. This in turn weakens the USD further and, all else being equal, is positive for risk appetite where smaller companies typically benefit more than larger companies.

Our thought from last month's letter that the market may be about to break out of a long period of range bound trading looks to be correct so far. Compared to previous bear market rallies during the year which were based on optimism which then failed, the latest rise is driven by an extreme pessimism where the development then surprised positively. The central banks have started to soften and just the fact that we are moving forward in time is positive as we approach a move towards a softer central bank policy. A decline in the market usually bottoms out when the previous winners, the generals, capitulate in the market and consolidate. This is quite true for the large FAANG companies in the US. All this is a very different compared to how it looked in August.

The total capitulation of Britain's political leaders regarding their budget clearly shows that it is the financial market that is largely dictating the conditions, especially for indebted countries. It is not unreasonable since it is the market participants who lend the capital. It was also very clear when Italy's new Prime Minister presented the budget that they do not want to repeat Britain's mistakes. The same also applies to the highest degree in Sweden, where the new government gave an unusually Lutheran and frugal message. The political risk has decreased.

Russia's vile attacks against Ukraine are still ongoing and the outcome of this is difficult to predict, but it seems less likely that Russia would win the war. China recently made a clear mark against Russia that the use of nuclear weapons is absolutely prohibited, which is of course positive (but this is a very difficult matter to understand).

The frequency of comments that China is beginning to ease its Covid restrictions is increasing all the time. Soon they may also become reality, which would be very positive for the world economy.

In the very short term, until the turn of the year, we will likely experience further positive returns. This despite the disappointment over the labour force figures that came on Friday, December 2nd. After the turn of the year, we roll into a new reporting season where the difference between the companies' conditions will become even clearer and which will likely lead to some turbulence but also new opportunities.

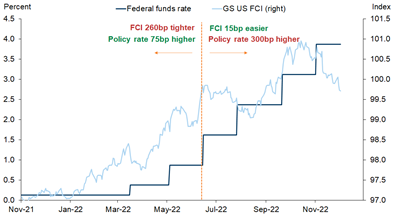

The positive Covid effects in society and economies are ebbing away, but at the same time the Goldman Sachs Financial Conditions (weekly compilation of stock and bond markets as well as the banking systems) have now improved so much that they are on par with what it looked like when the US the central bank began its record interest rate hikes before the summer. This is clearly positive, see below.

bild 34

Source: Goldman Sachs

Finally, after 10 years of growth for passive capital that buys and sells blindly and with a 2022 where macro has controlled most of the development for the stock market, we believe that the conditions for a significantly better working climate for stock pickers in 2023 will be good.

We thank you for all your support and communication during the year and wish you a very Merry Christmas and a Happy New Year!!

Mikael & Team

Malmö on 6th of December2022