Note that the information below describes the share class (I SEK), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class' return. The information below regarding returns therefore differs from the returns in other share classes.

Before making any final investment decisions, please read the prospectus, its Annual Report, and the KIID of the relevant Sub-Fund here

This material is marketing communication

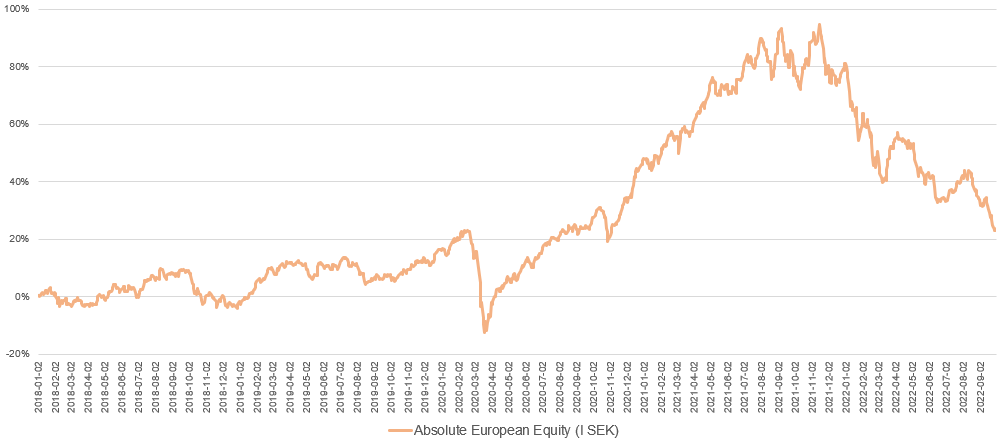

Monthly Newsletter Coeli Absolute European Equity – September 2022

SEPTEMBER PERFORMANCE

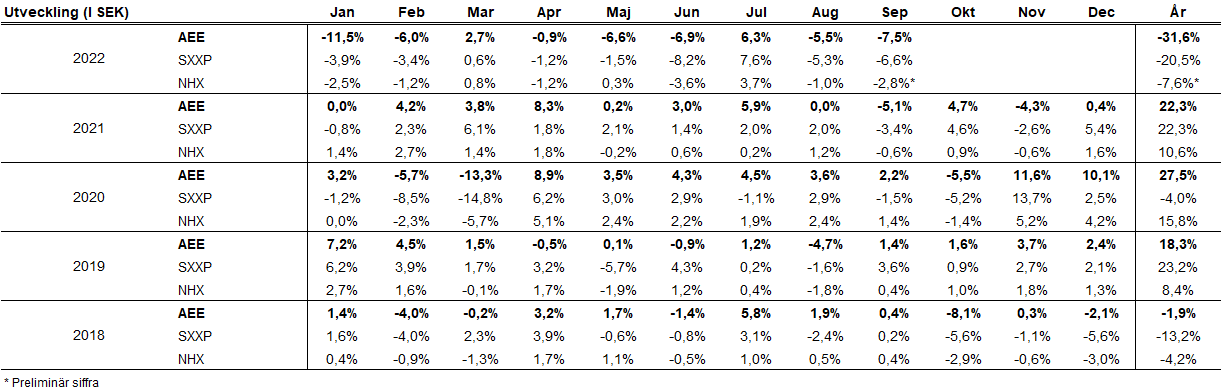

The fund’s value decreased by 7.5% in September (share class I SEK). The Stoxx600 (broad European index) decrease during the same period by 6.6% and HedgeNordic’s NHX Equities declined preliminary by 2.8%. The corresponding figures for 2022 are a decrease of 31.6% for the fund, -20.5% for the Stoxx600 and -7.6% for NHX Equities.

EQUITY MARKETS / MACRO ENVIRONMENT

This is the 57th monthly newsletter since our inception in January 2018 and the feeling is that there has been an exceptional number of big events in recent weeks. If we try really hard, we can see some glimmers of light in the form of a continued surprisingly strong economy, but otherwise the month brought mostly negative news. The uncertainty here and now is still high. From a positive angle and at the risk of being provocative there are now significant opportunities for the persistent and careful long-term investor. With each passing month we are getting closer to the tipping point. When the turn comes, as in the spring of 2003 and 2009, it usually happens quickly.

Bullets points outlining some of the events:

• Continued higher inflation data from the US and most of the Eurozone.

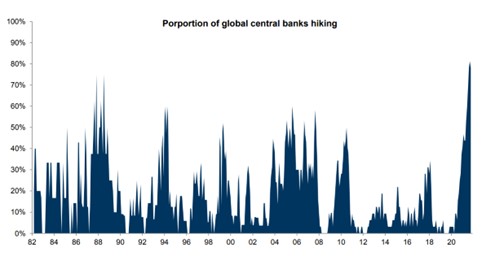

• A number of the world's central banks raised their respective key interest rates. Our tone-deaf Riksbank raised the most with a quadruple increase of 100 basis points.

• In practice, we now also have a currency war with the USD (so far) leading by far.

• The UK's new Prime Minister Liz Truss begins with record-breaking and unfunded tax cuts that make the development of the British pound look like a flash crash.

• The IMF (!) comes a few days later with an unusual warning to the UK government.

• The Bank of England came to the rescue, as the UK's pension system effectively received margin calls when interest rates rose sharply.

• After a month as Prime Minister, more than half of the UK population wants Liz Truss to resign. We, who thought it couldn't get any worse than with Boris Johnson.

• Putin annexes parts of eastern Ukraine and thereby raises the tone considerably.

• Nord Stream explodes underwater off the shores of Bornholm and the beaches of Österlen and sabotage is likely.

• Vague rumors that President Xi would be under house arrest. China's National Congress is on the the 16th of October, when Xi will be elected for a third time as leader.

• Italy held elections and it was a clear victory for the right-wing nationalists.

• Some profit warnings have started to appear, for example from consumer companies such as Thule and Nike.

• Queen Elizabeth II dies on September 8. Rest in peace.

The world's stock markets started the month with a slight positive trend, but on September 13, US inflation data came out and that changed the conditions. Instead of an expected improvement, there was a further acceleration in inflation which directly put pressure on the stock markets. The S&P500 fell in September by 9.3%, the Nasdaq by 10.6%, the SXXP600 by 6.6%, the Stockholm broad index by 7.4% and the SEB small cap index by 10.5%. The fund's value fell by 7.5% percent. More on that in the summary.

US Federal Reserve Chairman, Jerome Powell, raised interest rates in line with expectations, by 75 basis points at the end of September. It was the third triple increase in a row and in the press conference afterwards he was hawkish. "I wish there were a - a painless way to do that. There isn't. So what we need to do is get rates up to a - to the point where we're... putting meaningful downward pressure on inflation, and that's what we're - that's what we're doing."

We are now only a few increases from the highest level according to the FED's own forecast. On the last day of the month, differences of tone emerged for the first time from the various FED members where some of them began to speak a little more softly, that perhaps they should not maintain such a high speed in interest rate increases. We will not be surprised if the last increase comes this year, that is, earlier than the Fed's forecast.

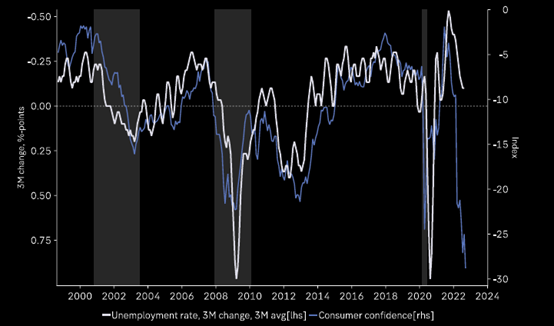

Below, consumer satisfaction in the eurozone coincided with unemployment. Here there is a clear lag in all economic data and it looks like unemployment will soon shoot upwards.

Source: Themarketear.com

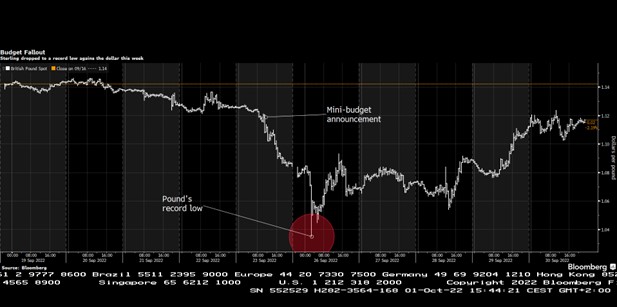

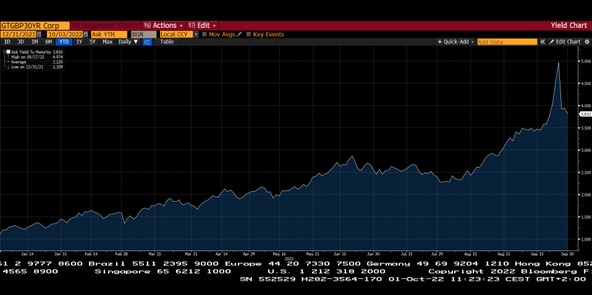

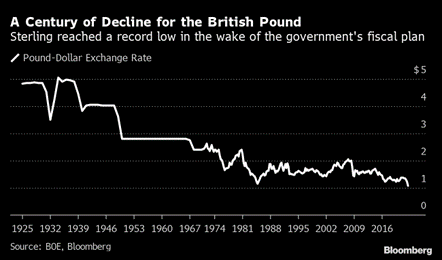

What actually happened in Britain? It started with the Bank of England raising its key interest rate by 50 basis points against the expected 65. This, despite the fact that inflation is running at around 10% and that the pound is the Western world's worst currency this year (the Swedish krona takes a dishonourable second place). The following day, the much-talked-about mini-budget came with extensive unfunded tax cuts, mainly for the wealth. Unfunded means that the supply of bonds will rise when funding is needed. The image below shows the drama for the pound over the past week. The decline came in 41st place measured over 160 years and 47,000 trading days!

Source: Bloomberg

After falling about 5% against the USD, most of the decline was recovered a week later. We guess that it is due to the market assessing the likelihood that the proposal will be withdrawn or that Liz Fross and/or Finance Minister Kwarteng will resign shortly. British tabloids are busy.

Late addition: on Monday 3rd of October, after this document was sent for editing, the UK Treasury apparently made a humiliating u-turn as they likely withdraw their tax proposal. Embarrassing to say the least, but very good. Interest rates are falling on a broad scale around the world in a form of relief rally.

Source: Daily Star

At the same time, the interest rate on Great Britain's government bonds rose sharply. Around the turn of the year, the interest rate on the 30-year-old was 1%. When the new proposal was announced, the corresponding interest rate reached 5% and a week later is around 3.8%.

Source: Bloomberg

Had the Bank of England not stepped in and bailed out more than £70 billion worth of bonds, large parts of Britain's pension capital would likely have come under a lot of pressure. When interest rates rise, the value of the bonds falls.

So we have gone from an extremely expansionary monetary policy that created an inflationary crisis, to a very strong and rapid tightening that is now creating a global economic crisis. That in turn prompts Britain's new government to launch an unfunded demand-stimulating tax package, which in turn prompts the Bank of England to make an emergency declaration not to topple the pension funds and support bond purchases while raising interest rates. It feels like a stubborn circular reference in an Excel sheet, but on a slightly larger scale.

Only since the financial crisis has the pound fallen from two dollars to just over one dollar. When King George V ruled, five dollars were paid for a pound. That says something about Europe's structural problems and challenges.

The Swedish krona is also (once again) in the running. It is only a little over six months since the Riksbank announced that the key interest rate would be kept unchanged until the second half of 2024. Most people in the financial market were very surprised given what was clearly visible at the time in the form of inflation. In September, the interest rate was raised by a whopping 100 basis points, which was shockingly unexpected. Despite that, the Swedish krona weakened further, probably when investors judged that it was too much and too fast, which of course damages the economy more than necessary. A weaker krona contributes to high inflation. Below, the Swedish krona against the US dollar, which has moved from 8.50 to just over 11 kronor in less than a year. The krona has never been weaker against the US dollar.

Source: Bloomberg

Our overall view is simply put that the world's central banks are trying to compensate for their grave mistakes by now acting forcefully and showing great action. It feels like a law of nature that they will make a double fault, which will be costly. Raising interest rates is absolutely right, but they are doing it far too aggressively, basing their decisions by studying economic data that has a lag of several months with an increased risk of recession.

We recommend watching the interview below with Jeremy Siegel, a well-known professor of finance at the Wharton School of the University of Pennsylvania. Watch the interview.

Turkey, with 80% inflation, is doing the opposite of everyone else and cut interest rates in September. Wonder what they were thinking? Fascinating.

Source: Goldman Sachs

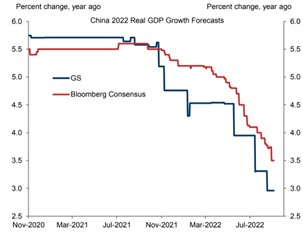

China continues with its astonishing Covid strategy with hard lockdowns, which has clear negative effects on the economy. From 1982-2012, China had an average annual growth rate of 10.3%. After that, growth has been 6.2%. This year, growth is expected to be a modest 3.0%. If you look at it from the bright side, oil prices would have been significantly higher if they were at a normal growth rate. Presumably, they need to stop the insanity of their Covid strategy soon, which, all things being equal, will contribute positively to global growth.

Source: Goldman Sachs

Source: KluddNiklas

A volatile market can lead to some frustration. We lighten up the mood a bit and offer a conversation between a slightly frustrated customer and its broker. Turn it up!

Frustrated with the Market part 1 and 2:

https://twitter.com/PriapusIQ/status/1572930760939651072

Long positions

Bonesupport

For some time, we have built up a position in the medical technology company Bonesupport which is headquarted in Lund in the south of Sweden. The company develops and sells the product Cerament, which comes in three product forms: BVF, G and V. Cerament is a so-called bone graft substitute that is injected into the bone in case of bone damage. After twelve months, the damage is completely replaced with the body's own bones. Cerament G & V contains antibiotics and has only been available on the European market. During May, the company received market approval for Cerament G for the treatment of bone infections in the USA. CEO, Emil Billbäck, describes this as "the most important milestone in the company's commercial history to date".

Bonesupport has a well-thought-out and elegant business model, which is quite unusual for a company in such an early commercial phase. During the last three years (Q2 19 to Q2 22), the company has grown on average by 34% per year while being heavily affected by the pandemic, quite a feat.

It can always be a bit difficult to bet on a new product launch, but we have noted some driving forces that make us feel confident in Bonesupport:

• Already established in the USA with sales there of Cerament BVF since 2018. Current turnover of approximately SEK 150 million annually in the USA. (In Europe, sales of Cerament G are roughly 6.5x greater than Cerament BVF.)

• Cerament G is a better product than the existing Cerament BVF.

• In the USA, there is a lack of a clear "standard of care" for the treatment of bone infections. Today's methods are sold off-label. Now Cerament G will be sold "on-label".

• Cerament G provides health economic benefits. Cerament G is a one-step operation, compared to today's treatment that requires double operations and all the complications that entails. The compensation system in the USA is greatly reduced for repeated visits for the same ailment - there is an incentive to make the patient healthy at the first treatment. Here, the clinical studies show that Cerament G is far, far better than existing treatment methods.

• Sellers have strong incentives to sell Cerament G over existing Cerament BVF, as they retain 30% of the sales price as commission. We estimate that the price is about double, so a seller makes twice as much on the newer product. In addition, Cerament G is likely to be one of the most profitable products in a seller's product catalogue.

• The company was awarded NTAP (new technology additional pay), an extra compensation to cover the extra cost arising from the use of Cerament G. It is worth noting that only about 10 products have been awarded NTAP out of several hundred applications this year.

We believe that Bonesupport is at the infancy of becoming a true quality company. We see several indications of this already. The company is building a platform from Cerament, so in the long run Bonesupport will not be a single product company. In addition, the company has good opportunities to become the "standard of care" for the treatment of certain skeletal injuries. There is a lot of clinical data that backs up the product's properties and the data is always presented through reputable scientific publications. Now the company has several growth legs to stand on, geographically, increased penetration with existing customers, new customers and new products as well as more indications. We think the market underestimates the opportunity that opens up in the US but also the duration of the business. The company can grow quickly for a long time with the possibility of reinvesting its capital at a high return.

Pets at Home

After we divested Musti (which we wrote about last month), we have replaced the company with British Pets at Home. Pets at Home has a strong position in the pet trade in England. Unlike Musti, the stores are larger, and they often also house a veterinary department. The veterinary and store operations create significant sales synergies because they complement each other and generate more traffic to the respective store.

Our view is that Pets at Home is an even better company than Musti, and also at a lower valuation. Pets at Home shares have fallen along with many other UK consumer companies (and the UK market in general). However, the pet industry is very resilient in times of consumer financial concern, and we believe that Pets at Home has been severely punished after the series of bad news that impacted all of our wallets.

We were a tad too quick to buy the share, which contributed negatively in September. We hope and believe that we will recover the losses as the company's financial updates come in.

Tate and Lyle

Tate and Lyle shares had a weak month following positive attribution earlier in the year. There are no obvious reasons for the decline, other than the stock performing better than many others this year, which surely made profit-taking palatable for some. On top of this, Tate and Lyle is listed on the London Stock Exchange, which famously had a turbulent September (for reasons detailed in our first section). Some are also worried about increased raw material and energy costs, but we believe that Tate & Lyle has good coverage for this via price increases. In addition, the company benefits greatly from its dollar exposure.

Short positions

The short portfolio contributed significally to a positive result during the month. The biggest positive contribution was made by our short positions in a Swedish small company index and in the German DAX. Several share-specific short positions made positive contributions to the result. Some of the names were Danish Vestas, Swedish Mips, German Puma and Finnish Qt Group.

Exposure

The net exposure, adjusted for our unlisted holdings, at the beginning and end of the month was 52% and 53% respectively.

Summary

In just over 10 weeks it's Christmas, but first we'll experience one of the most interesting reporting seasons in a long time. Some companies are still largely unaffected by what happened during the year, while others work under radically different conditions than when they entered 2022. Forecasting comments will determine much of the price reaction.

Inflation data in recent weeks has not yet given the market any fuel to lift share prices. Our clear impression when we talk to companies and other sources is that the economy has lost momentum after the summer, which is also what the central banks want to curb inflation.

What is still missing, but will probably come in force this reporting season, is for analysts to start adjusting down their earnings estimates, as they are way too high. The delicate question is how much is priced in already?

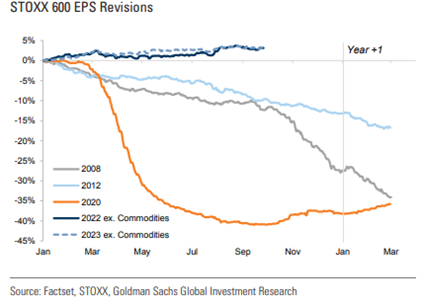

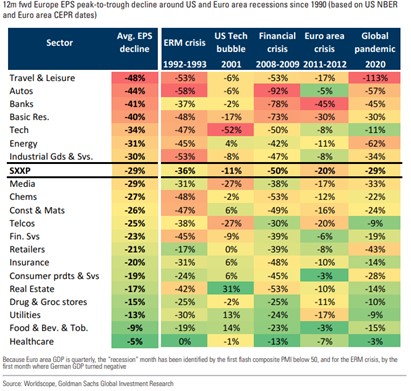

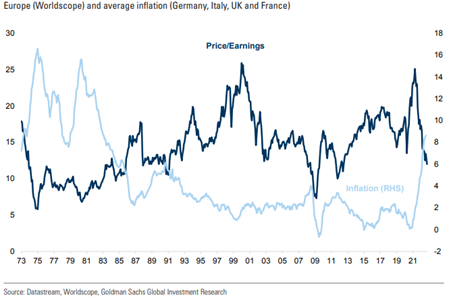

The other delicate question is: How much should the profits be adjusted? The table below shows that the average decline in profits when there has been a recession since 1990 has been 29%. The financial crisis stands out with 50% in profit decline.

Should we end up around the historical average this time around, Europe would trade at 13-14x earnings in 2023e, roughly matching the historical average valuation. Our conclusion is that with today's conditions, there is a lot of misery included in the stock prices.

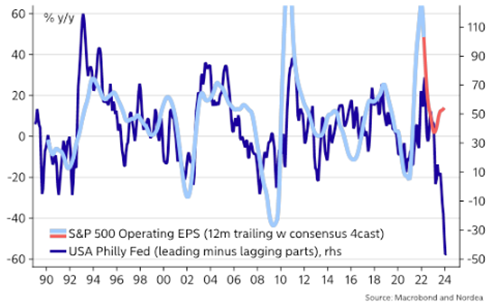

Another indicator that shows the Philly Fed (index that measures changes in the business climate) correlated with S&P500 earnings per share. Estimates are too high in the US as well.

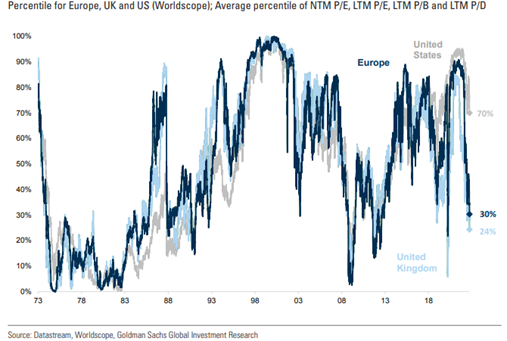

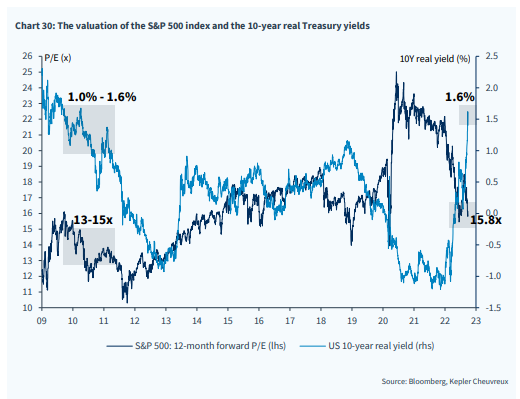

In the United States, valuations have in percentage terms decreased less than in Europe and Great Britain, where there has been a substantial multiple contraction.

The UK is trading around 8x earnings! Admittedly, there are more low-valued oil stocks there than in the rest of Europe, but these are very low levels. It is also one of the reasons we have 35% net exposure to British companies.

Source: themarketear.com

Rising inflation has a negative impact on company valuations and vice versa. Our view remains that we are around the highs for inflation (in the US).

Higher inflation has in the past been consistent with lower valuations:

Inflation drives up interest rates, which in turn puts pressure on values. We are not there yet, but there will be a time when it goes the other way.

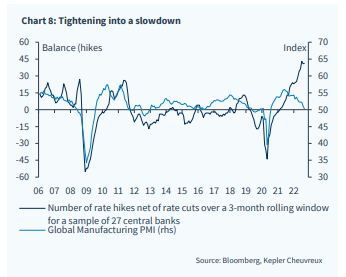

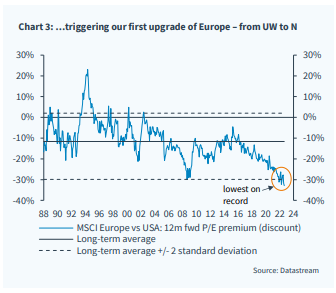

The record low European valuations are the reason why, for example, Kepler Cheuvreux last week upgraded European shares from underweight to neutral. However, they are still underweight stocks even if they are starting to get ready to increase the risk in the coming months.

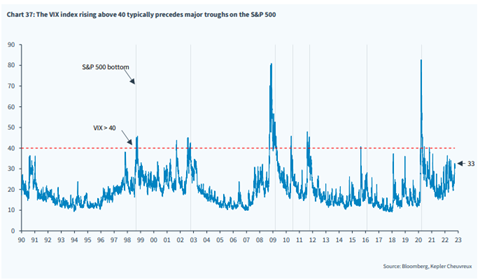

The VIX, volatility index, has risen recently along with other indicators such as the put/call index. There have been very large purchases of put options in the market which indicates a certain panic to protect against further market declines. It is usually a strong contraindication.

Our conclusion is that the likelihood of the US and Europe entering a recession has increased over the past month. The central banks are raising rates too aggressively and they are trying with all their might to make up for their mistakes from earlier this year. However, if the economy were to enter a recession we believe that the conditions for it to be a mild one are relatively good, as there are many positive indicators. For example, sharply falling shipping rates and raw materials, that both households and companies have a good economy and that China should soon be able to start up after almost three years of Covid chaos. For Europe, the big problem continues to be energy.

Our view since May, that we have a range-bound market is being tested right now as we are just below previous lows on several stock indices. Catalysts that can spark a rebound are an extremely defensive positioning of investors, that most investors are negative and that the stock markets are in most cases now well oversold. In addition, October is in the vast majority of cases a positive month on the stock market (which is far from a guarantee that it will be repeated this year).

Source: themarketear.com

In the end, it boils down to the long-term market reversing only when the FED turns up and we believe that the last rate hike is now close. Inflation should soon slow down, interest rates will then follow downwards as well as the US dollar which is currently plaguing US exporting companies. We believe that inflation will be significantly lower in 12 months from where we are today. The string is taut and it won’t take much for the market to shoot upwards.

Mikael & Team

Malmö on 7th of October 2022